Just a reminder: 99% of X was bearish on memory 3 months ago...

Since then:

$MU $380 -> $1122 (+195.26%)

$SNDK $565 -> $2155 (+281.42%)

$EWY $132 -> $219 (+65.91%)

SK Hynix 849K -> 2.685M KRW (+215.5%)

Samsung 172K -> 362K KRW (+110.7%)

If you see a bunch of projections on memory names like Samsung becoming the most profitable company in the world in 2028.

Might be a good idea to think independently outside of the narratives at the time like "Oil, LNG, Helium, Iran, etc."

Probably same thing now with optical names and their projections into 2027, 2028.

I do think photonics and memory are the 2 top themes though, with optics being very early into the supercycle.

따라하면 꼭 주식부자가 될 공무원의 워렌버핏의 노하우.

88년생 9급 공무원. 박봉 외벌이었지만 성공적인 주식투자로 30대에 금융자산 7억 6천 모음.

영상 보면서 이분의 자산증식 비결 두가지를 정리해봄.

1. 빠질수록 산다

보통 주식 파랗게 빠지면 스트레스받고 손절각부터 보는데,

근데 이 사람은 월급날마다, 자기 자산 중에 "제일 많이 빠진 걸" 골라서 삼.

떨어지는 거 보면 무서워서 던지는 게 본능인데,

이분은 "떨어졌네 → 싸졌으니 산다"가 그냥 규칙임. 감정이 없다.

→ 미국·한국·중국·인도 주식, 채권, 금, 비트코인을 비율 정해놓고(주식60/채권25/금12/비트3), 월급 올 때마다 빠진 칸만 채우는 거.

가장 중요한 분할매수 + 리밸런싱임.

2. 포모가 진짜로 없다

이게 더 놀라움. "나만 못 벌고 있나" 싶은 조급함(=포모) 때문에 다들 고점에 들어갔다 물린 경험이 많을것임.

근데 이 사람은 다 갖고 있어서, 미국 빠지면 한국 오르고, 한국 빠지면 금 오르고, 그 사이 비트 터짐. 항상 뭐 하나는 오름.

→ 그러니까 부러울 게 없음. 포모가 생길 구조 자체가 아님.

여기서 내가 느낀 거.

분할매수, 존버, 포모 금지가 정답인 거, 머리로는 다 앎.

근데 왜 다들 못 하��? 무서울 때 사고 좋을 때 참는 게, 사람 본능이랑 정반대라서 그럼.

근데 이 사람은 그걸 의지로 꾹 참는 게 아니라, 아예 "빠진 거 산다"는 규칙으로 박아버림.

감정이 낄 틈을 없앤 거임. 그래서 한 달에 10분이면 끝나고, 하락장에도 안 흔들림.

배울 점 정리하면:

1. 예측을 포기함 → 어디 오를지 맞히는 게임을 아예 안 함. 다 사두고 빠진 거 채우니까 틀릴 일이 없음.

2. 감정을 규칙으로 바꿈 → "무서우면 산다"를 머리로 버티는 게 아니라 시스템으로 만들어버림.

3. 그래서 안 흔들림 → 한 번도 안 흔들리고 7~8년 똑같이 한 게, 사실 제일 어려운 거임.

결국 투자 실력 = 종목 보는 눈이 아니라, 자기 감정을 시스템으로 눌러버리는 능력이라고 생각함.

연 13%, 7억 6천이 그 증거고.

AI Infrastructure Roadmap

What you need to research to outperform over the next few years

Now → memory + optical transceivers

2027 → 800V + early CPO

2028 → PLP + scale-up optical

2029 → glass substrates + HBM5

2030 → optical I/O chiplets + embedded cooling

2031 → 3D DRAM + microfluidic cooling

📌 순자산 1억, 5억, 10억, 30억 모으면 인생은 어떻게 바뀔까?

많은 사람들이

"1억만 모으면", "10억만 있으면"

인생이 통째로 바뀔 거라 생각

하지만 연 매출 2천억 원, 13년 차 투자자 신현욱 대표가 말하는 자산 구간별 진짜 현실은

내 자산 위치와 앞으로의 로드맵을 점검

1️⃣1억 원 : 인생은 안 바뀐다, 하지만 '근간'이 바뀐다

1억으로 차 사고 집 사면 남는 게 없습니다.

당장 소비 수준을 바꾸기엔 너무 작은 돈입니다.

📌인생은 안 바뀌어도

‘미래를 디자인하는 능력’이 생깁니다.

영원에서 1억을 모으는 과정에서 얻은 몸값 높이는 법,

��친 듯한 절약과 저축 습관은 평생 부자로 살아갈 '기초 체력'이 됩니다.

2️⃣5억 원 : 생존 ��안의 끝, '선택권'의 시작

연 복리 7%만 굴려도 월 300만 원 상당의 현금 흐름 가치.

"우리 가족이 굶어 죽진 않겠구나" 하는 압도적인 안정감이 찾아옴

📌싫은 직장을 때려치우거나 새로운 사업·투자형 인간으로 거듭날 수 있는 ‘인생 선택권’이 주어집니다.

내 집 마련이나 레버리지 투자를 제대로 굴릴 수 있는 기본값이기도 합니다.

3️⃣10억 원 : 경제적 자유? 아니, 욕망의 '입장권'

순자산 10억 번 사람 중 경제적 자유를 느꼈다는 사람은 단 한 명도 없습니다.

이 단계에 오면 인간의 욕망은 더 커지고, 자산 규모를 키우느라 유지 비용이 늘어 소비 수준은 오히려 그대로인 경우가 많습니다.

📌소액 투자자는 구경도 못 하던 우량 기관 펀드나 대규모 투자 기회에 참여할 수 있는 '진짜 부자 세계로의 입장권'을 거머쥐게 됩니다.

4️⃣30억 원 : 내가 쓰는 속도보다 돈이 구르는 속도가 빠르다🚀

대한민국 상위 1% 자산.

숨만 쉬고 기존대로 살아도 내가 돈을 쓰는 속도보다 자산이 스스로 불어나는 속도가 훨씬 더 빨라짐

📌30억을 모았다는 건 이미 완벽한 ‘돈 버는 시스템’을 가졌다.

시간의 문제일 뿐, 100억 자산가로 가는 고속도로에 올라탄 단계.

가족의 건강을 프리미엄으로 챙기며 '인생의 불행'을 돈으로 막을 수 있는 안전망이 생깁니다.

✅ "내가 만약 다시 0원으로 돌아간다면?"

"5억, 10억, 30억은 생각지도 마십시오. 오직 '첫 1억'을 가장 빠르게 모으는 데만 미치셔야 합니다."

📌초기 3년은 딴생각 금지

머리 박고 내 분야 역량을 키워 소득(본업+부업)을 극대화하세요.

📌지출은 통제 대상

소득은 세전으로 들어오지만 소비는 세 후로 나갑니다. 가계부를 쓰고 새는 돈을 완전히 틀어막으세요.

첫 1억을 모으는 순간, 당신 몸에 이식된 능력·절약 습관·투자 경험이라는 시스템이 그 다음 5억, 10억으로 가는 리드타임을 압축해 줄 것입니다.

👉 오늘부터 나의 목표는 오직 하나, '가장 빠른 첫 1억'입니다.

#재테크 #자산관리 #동기부여 #시드머니 #경제적자유 #자기계발

https://t.co/5777iLmcBD

$UAI is shaping up to be one of the strongest plays in the market right now. this project is quietly building real value. Don't be surprised if $UAI outperforms $LAB and $RAVE in the coming days. Strong fundamentals, growing attention, and still massively undervalued.💎

골드만삭스 AI 슈퍼 롱 떴음😘

• 이번 사이클은 역사상 가장 크고 가장 긴 반도체·전자부품 업황 사이클 중 하나가 될 가능성이 높음.

• 1차 성장 동력은 AI 서버 및 데이터센터 인프라 투자 확대.

• 2차 성장 동력은 Device Proliferation.

- Edge AI

- Physical AI (로봇, 자율주행, 스마트 디바이스)

• 현재 업황은 사이클의 초기 단계(Early Stage)로 판단.

"AI 인프라 투자 → Edge AI → Physical AI로 이어지는 초대형 장기 성장 사이클이 시작됐으며, 아직 초기 국면에 불과하다."

출처 : 텔레 채널 프리라이프

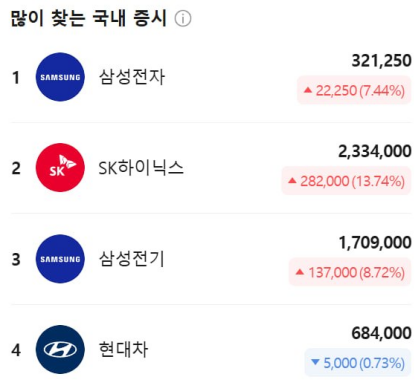

[속보] “2028년 삼전+하닉 영업익 1000조 시대 온다”…골드만삭스의 ‘파격 전망’

골드만삭스가 삼성전자(005930)와 SK하이닉스(000660)의 중장기 실적 전망을 한달만에 대폭 상향 조정했다. 인공지능(AI) 투자 확대에 따른 고대역폭메모리(HBM) 수요 급증과 범용 메모리 호황이 예상보다 오래 지속될 것으로 판단하면서다. 골드만삭스가 제시한 2028년 연간 영업이익 전망치는 삼성전자 610조 원, SK하이닉스 454조 원으로 두 회사를 합치면 1000조 원을 훌쩍 넘는다.

1일 금융투자 업계에 따르면 골드만삭스는 지난달 31일(현지시간) 보고서를 통해 “D램·낸드(NAND)·HBM 업황이 ‘Higher for Longer(예상보다 오래 지속되는 호황)’ 국면에 진입했다”며 삼성전자와 SK하이닉스에 대��� 실적 전망과 목표주가를 상향 조정했다. 삼성전자와 SK하이닉스의 목표주가는 각각 45만 원, 350만 원으로 제시했으며 투자의견은 ‘매수(Buy)’를 유지했다.

골눈길을 끄는 것은 골드만삭스가 불과 한 달 전 제시했던 영업이익 전망치를 대폭 끌어올렸다는 점이다. 특히 전망치 상향 폭은 올해, 2027년, 2028년으로 갈수록 커지고 있어 메모리 업황의 정점을 당분간 예상하지 않고 있음을 시사한다.

골드만삭스는 삼성전자의 연간 영업이익이 올해 374조 원, 2027년 530조 원, 2028년 610조 원에 이를 것으로 전망했다. 한 달 전 전망치와 비교하면 올해는 5.4% 상향 조정에 그쳤지만 2027년은 21.0%, 2028년은 23.3% 높여 잡았다.

SK하이닉스에 대한 전망도 공격적이다. 골드만삭스는 SK하이닉스의 영업이익이 올해 271조 원, 2027년 401조 원, 2028년 454조 원에 달할 것으로 ��상했다. 기존 전망 대비 상향 폭은 올해 3.7%에서 2027년 21.4%, 2028년 24.0%로 확대됐다. 두 회사 모두 메모리 슈퍼사이클 장기화로 인해 시간이 갈수록 수익성이 더욱 가파르게 높아질 것으로 본 것이다.

이번 보고서가 주목받는 이유는 최�� 시장에서 제기된 ‘메모리 피크아웃’ 우려를 정면으로 반박했기 때문이다. 최근 두 기업의 주가가 가파르게 오르며 고점 부담을 느낀 시장에서는 인공지능(AI) 투자 확대에 따른 HBM 호황이 올해 하반기 또는 내년 이후 둔화될 수 있다는 전망이 꾸준히 제기돼 왔다. HBM 공급 확대와 빅테크의 AI 투자 속도 조절 가능성 등이 근거로 거론됐다.

그러나 골드만삭스는 HBM뿐 아니라 범용 D램과 낸드 호황까지 장기화할 것으로 재확인했다. 골드만삭스는 특히 메모리 업종 전반의 가치 재평가 가능성에도 주목했다. 실적 개선뿐 아니라 메모리 업체들에 적용되는 밸류에이션 멀티플도 확대될 수 있다고 분석했다.

특히 메모리 가운데 낸드플래시의 영업이익이 기존 전망 대비 더욱 높아질 것으로 예상했다. 골드만삭스는 삼성전자 반도체(DS) 부문의 영업이익 전망치를 2027년과 2028년 각각 기존 전망 대비 21.9%, 24.1% 상향 조정했다.

특히 이 가운데 낸드 영업이익 전망치는 2028년 기존 대비 31.6%나 높여 잡았다. SK하이닉스 역시 낸드 영업이익 전망치를 2028년 기준 36.8% 상향 조정됐다. 골드만삭스는 이에 따라 일본 낸드플래시 메모리 반도체 기업인 키옥시아에 대해서도 ���자의견을 ‘매수(Buy)’로 상향했다.

15 sectors defining the next decade of investing

The megatrend map.

1. AI

$NVDA · $PLTR · $APP

The infrastructure king, the data layer, and the monetization engine. Three different ways to own AI.

2. Chips

$AMD · $AVGO · $MU

Compute, custom silicon, and memory. The full semiconductor stack.

3. Space

$RKLB · $ASTS · $PL

Launch infrastructure, satellite broadband, and geospatial intelligence. Pre-SpaceX IPO re-rating still unfolding.

4. ₿ Crypto

$COIN · $MSTR · $GLXY

Exchange infrastructure, BTC treasury play, and mining leverage. Three different risk profiles.

5. Energy

$VST · $NEE · $FSLR

AI power demand is the new oil shock. These three sit at the intersection of grid scale and renewables.

6. Drones

$AVAV · $KTOS · $ONDS

Autonomous defense and dual-use tech. Defense budgets are only going one direction.

7. Nuclear

$OKLO · $SMR · $LEU

The only baseload clean energy that hyperscalers can actually contract. Still early, still underpriced.

8. Robotics

$ISRG · $SYM · $PATH

Surgical precision, warehouse automation, and enterprise AI workflows. Labor replacement at scale.

9. Quantum

$IONQ · $RGTI · $QBTS

Highest risk on the list. Longest time horizon. Size accordingly — the upside is generational if it works.

10. Batteries

$QS · $LAC · $BE

Solid-state technology, lithium supply chain, and grid-scale storage. The energy transition needs all three.

11. Healthcare

$HIMS · $UNH · $LLY $MRNA

Diversified pharma cash flow, next-gen biologics, and mRNA platform optionality beyond COVID.

12. Photonics

$AAOI · $COHR · $LITE

The most underowned layer of AI infrastructure. Data centers need optical interconnects — demand is accelerating.

13. Rare Earths

$MP · $USAR · $FCX

Supply chain sovereignty is the new geopolitics. The West needs domestic rare earth and copper supply. Now.

14. Manufacturing

$ETN · $CAT · $GE

The physical backbone of AI buildout — power distribution, heavy equipment, and aerospace. Old economy, new tailwind.

15. Critical Minerals

$FCX · $UAMY · $CRML

Copper, lithium, and battery metals. Every AI data center, EV, and grid upgrade runs on these. The commodity cycle is structural.

This isn’t a buy list. It’s a framework.

Find your highest-conviction themes. Size appropriately. Think in years.

Not financial advice.

$POET is going to $50 this year.

The flow has been bullish for weeks. The photonic interposer thesis got validated by Marvell's call. And the chart is setting up a multi-year base breakout.

$50 is the conservative target.

I called out $IONQ when it was $7, its spiked up 1000% already. I think it can hit 10,000%

There's 3 more massive plays exactly like it under $20:

1. $POET - POET Technologies

Catalyst 1 – 30,000+ optical engine shipmentsManagement is targeting 30,000+ Infinity optical engine shipments in 2026, marking the inflection from lab demo to real commercial revenue. A follow-on order cascade from hyperscalers would collapse the current 1,000x P/S multiple and force a full institutional re-rating.

Catalyst 2 – LITEON + Lessengers 1.6T transceiver partnershipsPOET is jointly developing 400–800G+ and 1.6T optical modules targeting the AI data center connectivity market directly. Completed module samples + a volume supply agreement with a Tier-1 networking name validates the platform at scale and unlocks institutional accumulation.

Catalyst 3 – US redomicile + Malaysia manufacturing rampPOET is redomiciling from Canada to the US, eliminating PFIC tax risk that has suppressed US institutional ownership. Paired with the Malaysia high-volume manufacturing buildout funded by $430M cash, a successful ramp opens the door to index inclusion and a dramatically larger buyer base.

2. $TE – T1 Energy Inc.

Catalyst 1 – G2_Austin first production late 2026 T1's $400–425M G2_Austin facility in Rockdale, Texas is under construction targeting 2.1 GW of TOPCon solar cell capacity, with first production expected by year-end 2026. Once online, it feeds directly into the existing 5 GW module line at G1_Dallas completing the only fully integrated domestic US solar supply chain and unlocking a massive margin expansion story.

Catalyst 2 – 45X tax credit eligibility → business model validationT1's entire profitability thesis hinges on qualifying for the IRA's 45X advanced manufacturing tax credits, which reward domestic solar cell production at scale. Confirmed FEOC compliance + first 45X credit sales would be the single biggest re-rating catalyst, turning TE from a speculative build into a cash-generative manufacturer overnight.

Catalyst 3 – Tariff tailwinds + long-term offtake contractsTrump-era tariffs on Chinese solar imports have made domestic cell manufacturing a national priority, and T1 already has 3.0 GW of components contracted at G1_Dallas. Securing major utility-scale offtake agreements for G2_Austin output with visibility into multi-year revenue would force a full analyst re-rating and bring in infrastructure-focused institutional capital.

3. $RGTI – Rigetti Computing

Catalyst 1 – Lyra 336-qubit system → quantum advantage demoRigetti's Lyra processor targets 336 qubits and 99.7% two-qubit gate fidelity, making it the first system with a realistic path toward demonstrable quantum advantage on a real-world problem. A published proof-of-quantum-advantage in logistics, finance, or drug discovery would be the most explosive single catalyst in the entire sector expected late 2026.

Catalyst 2 – Government contracts cascade: DoD, UK, India C-DACRGTI already has the C-DAC India deal in hand and is pursuing a UK deployment of a 1,000+ qubit system. A material DoD or NATO-affiliated contract would validate Rigetti as a national security asset and trigger accumulation from defense-focused and security-cleared institutional funds.

Catalyst 3 – $NVDA/hyperscaler integration → QCaaS revenue inflectionNvidia's launch of open-source Ising quantum AI models directly validated Rigetti's architecture and drove the April 2026 re-rating. A deeper co-sell or integration agreement with Nvidia, Google, or Microsoft — baking Rigetti's QPUs into their AI stack — transforms revenue from grant-dependent to subscription-recurring, the fundamental shift needed to sustain a 10x move.

반도체 주식, 마지막 매수 기회는?

(이형수 대표)

- 5월까지는 시장을 긍정적으로 봤지만 6~7월 중 한 차례 조정이 올 수 있다고 전망함

- 그 조정이 마지막 매수 기회가 될 것이고 이후 시장은 버블 단계로 진입할 가능성이 높다고 봄

- 현재 수급은 대형주와 소부장 사이에서 힘겨루기 중이고 대형주가 쉬어가는 시기엔 국민성장펀드 자금이 소부장으로 이동할 수 있음

- 관련 기업 상장 직후에는 재료 소멸로 주가가 잠시 밀릴 수 있지만 하락이 지속되기보다 강하게 반등할 가능성이 높음

- 사이클 후반부로 갈수록 미처 매수하지 못한 투자자들의 FOMO 매수세가 유입되면서 주가를 끌어올리는 패턴이 반복됨

- 코스피는 펀더멘탈 기준 상단으로 15,000선까지 도달할 수 있다는 시각을 제시함

- 2,500에서 5,000까지는 반도체 실적이 동력이 되고 5,000에서 10,000까지는 배당 분류과세와 주주환원 정책이 변곡점 역할을 할 것으로 봄

- 10,000에서 15,000 구간은 MSCI 선진국 편입과 외환시장 24시간 개방 등 자본시장 글로벌화가 뒷받침돼야 가능함

- AI 인프라는 에이전틱 AI를 넘어 현실 세계와 연결되는 피지컬 AI로 확장되는 중임

- 자율주행보다 휴머노이드 로봇이 제조 현장에 먼저 투입될 것이라는 전망도 나옴

- 로봇과 자율주행 관련주로는 현대차, 현대모비스, 현대글로비스, 현대오토에버를 주목할 만한 종목으로 꼽음

- 하반기 리스크로는 빅테크 CAPEX 증가율 둔화, 메모리 가격 역기저 효과, 금리 및 환율 변동성을 복합적으로 살펴야 함

- 변동성이 큰 시기인 만큼 섣불리 한쪽으로 치우치기보다 현금을 일부 확보하면서 기본 물량을 지키는 자세가 중요함

AI가 커질수록 돈이 몰리는 곳이 바뀜 (AI 사이클)

처음엔 AI를 똑똑하게 만드는 게 중요했음

그래서 GPU가 필요했고

엔비디아가 미친 듯이 주목받았음

근데 GPU가 빨라지니까

다음 문제는 메모리로 넘어감

데이터를 빨리 주고받아야 해서

HBM이 중요해졌고

그래서 하이닉스, 삼성전자 같은 기업들이 주목받는 중임

그다음 병목은 전력이라고 함

AI 데이터센터는 전기를 엄청 먹고

발열도 심함

그래서 앞으로는

발전소

송전망

변압기

냉각 기술

SMR 같은 원자력

액침 냉각

광통신

이런 쪽으로 관심이 옮겨갈 수 있음

초보자 기준으로 쉽게 말하면

AI 돈의 이동은 이런 순서에 가까움

AI 모델 경쟁

→ GPU

→ HBM 메모리

→ 전력

→ 냉각

→ 데이터센터

→ 통신

→ 온디바이스 AI

지금 엔비디아만 보고 따라가기보다

AI가 커질수록 어디가 막히는지 보는 게 중요해 보임

돈은 보통

이미 뜬 곳보다

다음에 부족해질 곳으로 먼저 움직이는 듯

AI를 기술 뉴스로만 보지 말고

어디서 병목이 생기는지 보면

시장 흐름이 훨씬 쉽게 보임

![ohmahahm's tweet photo. [속보] “2028년 삼전+하닉 영업익 1000조 시대 온다”…골드만삭스의 ‘파격 전망’

골드만삭스가 삼성전자(005930)와 SK하이닉스(000660)의 중장기 실적 전망을 한달만에 대폭 상향 조정했다. 인공지능(AI) 투자 확대에 따른 고대역폭메모리(HBM) 수요 급증과 범용 메모리 호황이 예상보다 오래 지속될 것으로 판단하면서다. 골드만삭스가 제시한 2028년 연간 영업이익 전망치는 삼성전자 610조 원, SK하이닉스 454조 원으로 두 회사를 합치면 1000조 원을 훌쩍 넘는다.

1일 금융투자 업계에 따르면 골드만삭스는 지난달 31일(현지시간) 보고서를 통해 “D램·낸드(NAND)·HBM 업황이 ‘Higher for Longer(예상보다 오래 지속되는 호황)’ 국면에 진입했다”며 삼성전자와 SK하이닉스에 대��� 실적 전망과 목표주가를 상향 조정했다. 삼성전자와 SK하이닉스의 목표주가는 각각 45만 원, 350만 원으로 제시했으며 투자의견은 ‘매수(Buy)’를 유지했다.

골눈길을 끄는 것은 골드만삭스가 불과 한 달 전 제시했던 영업이익 전망치를 대폭 끌어올렸다는 점이다. 특히 전망치 상향 폭은 올해, 2027년, 2028년으로 갈수록 커지고 있어 메모리 업황의 정점을 당분간 예상하지 않고 있음을 시사한다.

골드만삭스는 삼성전자의 연간 영업이익이 올해 374조 원, 2027년 530조 원, 2028년 610조 원에 이를 것으로 전망했다. 한 달 전 전망치와 비교하면 올해는 5.4% 상향 조정에 그쳤지만 2027년은 21.0%, 2028년은 23.3% 높여 잡았다.

SK하이닉스에 대한 전망도 공격적이다. 골드만삭스는 SK하이닉스의 영업이익이 올해 271조 원, 2027년 401조 원, 2028년 454조 원에 달할 것으로 ��상했다. 기존 전망 대비 상향 폭은 올해 3.7%에서 2027년 21.4%, 2028년 24.0%로 확대됐다. 두 회사 모두 메모리 슈퍼사이클 장기화로 인해 시간이 갈수록 수익성이 더욱 가파르게 높아질 것으로 본 것이다.

이번 보고서가 주목받는 이유는 최�� 시장에서 제기된 ‘메모리 피크아웃’ 우려를 정면으로 반박했기 때문이다. 최근 두 기업의 주가가 가파르게 오르며 고점 부담을 느낀 시장에서는 인공지능(AI) 투자 확대에 따른 HBM 호황이 올해 하반기 또는 내년 이후 둔화될 수 있다는 전망이 꾸준히 제기돼 왔다. HBM 공급 확대와 빅테크의 AI 투자 속도 조절 가능성 등이 근거로 거론됐다.

그러나 골드만삭스는 HBM뿐 아니라 범용 D램과 낸드 호황까지 장기화할 것으로 재확인했다. 골드만삭스는 특히 메모리 업종 전반의 가치 재평가 가능성에도 주목했다. 실적 개선뿐 아니라 메모리 업체들에 적용되는 밸류에이션 멀티플도 확대될 수 있다고 분석했다.

특히 메모리 가운데 낸드플래시의 영업이익이 기존 전망 대비 더욱 높아질 것으로 예상했다. 골드만삭스는 삼성전자 반도체(DS) 부문의 영업이익 전망치를 2027년과 2028년 각각 기존 전망 대비 21.9%, 24.1% 상향 조정했다.

특히 이 가운데 낸드 영업이익 전망치는 2028년 기존 대비 31.6%나 높여 잡았다. SK하이닉스 역시 낸드 영업이익 전망치를 2028년 기준 36.8% 상향 조정됐다. 골드만삭스는 이에 따라 일본 낸드플래시 메모리 반도체 기업인 키옥시아에 대해서도 ���자의견을 ‘매수(Buy)’로 상향했다.](https://pbs.twimg.com/media/HJrXac9boAAFXlh.jpg)

![ohmahahm's tweet photo. [속보] “2028년 삼전+하닉 영업익 1000조 시대 온다”…골드만삭스의 ‘파격 전망’

골드만삭스가 삼성전자(005930)와 SK하이닉스(000660)의 중장기 실적 전망을 한달만에 대폭 상향 조정했다. 인공지능(AI) 투자 확대에 따른 고대역폭메모리(HBM) 수요 급증과 범용 메모리 호황이 예상보다 오래 지속될 것으로 판단하면서다. 골드만삭스가 제시한 2028년 연간 영업이익 전망치는 삼성전자 610조 원, SK하이닉스 454조 원으로 두 회사를 합치면 1000조 원을 훌쩍 넘는다.

1일 금융투자 업계에 따르면 골드만삭스는 지난달 31일(현지시간) 보고서를 통해 “D램·낸드(NAND)·HBM 업황이 ‘Higher for Longer(예상보다 오래 지속되는 호황)’ 국면에 진입했다”며 삼성전자와 SK하이닉스에 대��� 실적 전망과 목표주가를 상향 조정했다. 삼성전자와 SK하이닉스의 목표주가는 각각 45만 원, 350만 원으로 제시했으며 투자의견은 ‘매수(Buy)’를 유지했다.

골눈길을 끄는 것은 골드만삭스가 불과 한 달 전 제시했던 영업이익 전망치를 대폭 끌어올렸다는 점이다. 특히 전망치 상향 폭은 올해, 2027년, 2028년으로 갈수록 커지고 있어 메모리 업황의 정점을 당분간 예상하지 않고 있음을 시사한다.

골드만삭스는 삼성전자의 연간 영업이익이 올해 374조 원, 2027년 530조 원, 2028년 610조 원에 이를 것으로 전망했다. 한 달 전 전망치와 비교하면 올해는 5.4% 상향 조정에 그쳤지만 2027년은 21.0%, 2028년은 23.3% 높여 잡았다.

SK하이닉스에 대한 전망도 공격적이다. 골드만삭스는 SK하이닉스의 영업이익이 올해 271조 원, 2027년 401조 원, 2028년 454조 원에 달할 것으로 ��상했다. 기존 전망 대비 상향 폭은 올해 3.7%에서 2027년 21.4%, 2028년 24.0%로 확대됐다. 두 회사 모두 메모리 슈퍼사이클 장기화로 인해 시간이 갈수록 수익성이 더욱 가파르게 높아질 것으로 본 것이다.

이번 보고서가 주목받는 이유는 최�� 시장에서 제기된 ‘메모리 피크아웃’ 우려를 정면으로 반박했기 때문이다. 최근 두 기업의 주가가 가파르게 오르며 고점 부담을 느낀 시장에서는 인공지능(AI) 투자 확대에 따른 HBM 호황이 올해 하반기 또는 내년 이후 둔화될 수 있다는 전망이 꾸준히 제기돼 왔다. HBM 공급 확대와 빅테크의 AI 투자 속도 조절 가능성 등이 근거로 거론됐다.

그러나 골드만삭스는 HBM뿐 아니라 범용 D램과 낸드 호황까지 장기화할 것으로 재확인했다. 골드만삭스는 특히 메모리 업종 전반의 가치 재평가 가능성에도 주목했다. 실적 개선뿐 아니라 메모리 업체들에 적용되는 밸류에이션 멀티플도 확대될 수 있다고 분석했다.

특히 메모리 가운데 낸드플래시의 영업이익이 기존 전망 대비 더욱 높아질 것으로 예상했다. 골드만삭스는 삼성전자 반도체(DS) 부문의 영업이익 전망치를 2027년과 2028년 각각 기존 전망 대비 21.9%, 24.1% 상향 조정했다.

특히 이 가운데 낸드 영업이익 전망치는 2028년 기존 대비 31.6%나 높여 잡았다. SK하이닉스 역시 낸드 영업이익 전망치를 2028년 기준 36.8% 상향 조정됐다. 골드만삭스는 이에 따라 일본 낸드플래시 메모리 반도체 기업인 키옥시아에 대해서도 ���자의견을 ‘매수(Buy)’로 상향했다.](https://pbs.twimg.com/media/HJrXb5ZbsAAn-5l.jpg)