Funny to see Boomers on X in complete disbelief as everything they learned over decades gets invalidated because the government and Wall Street turned the economy into a casino the past 3 years

@TheFlowHorse Ryan, and what your thoughts?

I'm quite young and I'm interested in hearing the opinion/experience of someone who has seen something like this before

The only edge in markets that never gets arbitraged away — from a crypto quant running Sharpe ~4:

Leigh Drogen (@LDrogen), CIO of Starkiller Capital. Sharpe ~4. Started his career as a quant at a NY equity hedge fund.

Drogen:

"If the only thing you ever did was put a 50-day moving average on Bitcoin — long when above, out when below — you would massively outperform everything."

"You would stay out of the massive puke-inducing crashes."

"If you knew nothing — couldn't tell Ethereum from the Nth lending protocol — and just bought the top 20th percentile by 30-day return and shorted the bottom 20th, you'd make a whole bunch of money."

"What is the intrinsic value of Dogecoin? Nothing. You could make the case Bitcoin has no intrinsic value either."

"The vast majority of assets in digital asset space have no intrinsic value — which is why cross-sectional momentum works so well."

"Momentum is the only persistent alpha in all markets. All other alpha gets arbitraged away. Human behavior never will."

Markets are behaving as if volatility has been abolished. Meanwhile, bond vol is exploding, implied correlations remain depressed, and VIX is approaching what increasingly looks like a natural floor.

https://t.co/6i3ll8PdnY

This is a retarded view

Once you experience roundtripping a few times, you either learn to play defense or you quit

Keeping what you make and compounding that over time > Running it up massive and roundtripping

This should not need to be said

I've tweeted about this before but it's a good reminder

The founder of Tik Tok was running out of money trying to build an education start up. One day, he looked at the people on his train. Eyes blank. None of them were learning

the next day he pivoted to brain rot and won

@TraderMagus Magus, most of my trades on medium/high TF, stocks/crypto. It hard for me to find trades like yours in that post, intraday, I just can’t come up with ideas and don’t understand what to look at such TF, are they mostly based on flows? Any recommendations? Thx

Lazarus Group is the collective name for all DPRK state sponsored cyber actors.

The main issue is everyone groups them all together when the complexity of threats are different.

Threats via job postings, LinkedIn, email, Zoom, or interviews are basic and in no way sophisticated (DPRK groups: DPRK IT workers, Contagious Interview, Dangerous PW/Bluenoroff/SapphireSleet).

The only thing about it is they’re relentless.

If you or your team still falls for them in 2026 you’re very likely negligent.

The ONLY two DPRK groups you will see regularly doing sophisticated crypto attacks are TraderTraitor (Bybit/DMM) & AppleJeus (Radiant/Drift)

I always see companies write about how they stopped the most elaborate attempt by Lazarus Group and it ends up being a basic attempt by a low iq subgroup….

I have a working theory that when the market gets choppy it concentrates speculative behavior into just a few tickers and causes a kind of paradoxical squeeze in very select memes versus broad memes.

For example, back in 2022 while the index was down like 20% YTD, a scam IPO from Hong Kong trading under the ticker HKD went from $200M to having a larger market cap than Exxon Mobil. Started out as low float shenanigans but became the last refuge for meme stock traders searching for anything that would still go up.

Anyway, here’s a chart of VCX.

I figured out why the tape always shows fake and shallow flow: It's a means to probe whether informed participants have entered the market. The milliseconds after a trade is matched can tell you so much. If the mid is higher, for example, 200ms after a buy trade gets matched, that buyer might know something. If the mid is continually above subsequent buys, asymmetric information has hit the market; and it's time to take liquidity.

Also, if you're interested in microstructure: monitoring book speed -- the shelf-life of quotes: this will tell you much more than tape speed ever will. Tape speed is stale information. By the time tape speed spikes, market makers have already shifted liquidity surface curves, and taking liquidity in the direction of move has a high probability of being toxic fills.

These two metrics: fill-to-move ratio and quote lifetime, IME, are the most actionable when combined with OBI, CVD, etc. etc.

Anyways, I still prefer my retarded TA diagonals and Elliot Waves lol

@LSDinmycoffee 1 more question

Sometimes for me is hard to pull a trigger, i waiting for confirmation that sometimes won’t come and i miss, but analysis for good

What would u recommend?

@TheFlowHorse Much appreciate of ur opinion

Noticed that some stocks moving only on earnings, then dying, waiting for next earnings. Was thinking is there any edge with that type of single names, because all vol. happening before/on earnings

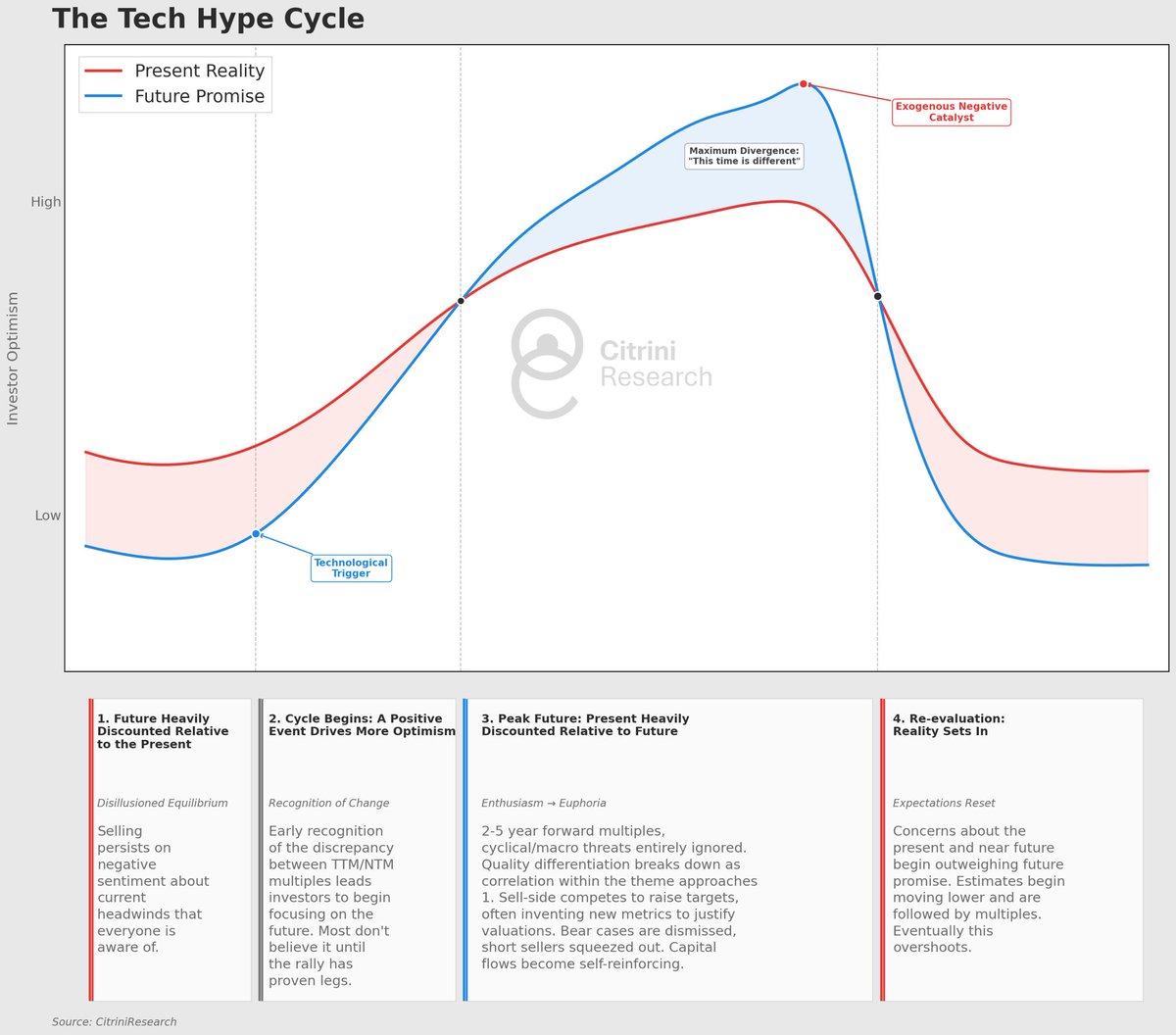

This is how I think about hype cycles in markets. It is basic, but that’s the point (frameworks shouldn’t be overly complex, I think).

Investors are always either discounting the promise of the future or the reality of the present. And they are never equally weighting them.

During the early part of a hype cycle, leading up to and directly following a technological advancement, investors are typically discounting the future while focusing on the present. A good example for this is Nvidia at the end of 2022: investors were solely focused on the headwinds presented by the crypto GPU glut, the anemic gaming PC market and the recent rise in rates causing fears about a near term recession.

Then, as the cycle begins, investors begin to shift to incorporate the future - they stop focusing so much on the present and see the promise. They move out in terms of valuing away from last twelve months current price / current earnings to next twelve months. Then, as price climbs and the technology becomes more exciting, their imagination takes hold. At a certain point they begin discounting the present much more heavily and the future becomes the only thing that matters. Valuation metrics over the next twelve months become useless in favor of 2, 3 or 5 years forward.

At the peak, the present is not considered at all, it is 100% driven by an imagined future (even when that imagination doesn’t necessarily align with a bullish outcome for the stocks driving the rally). Analysts aggressively raise estimates in ways that, at the time, seem fundamentally justifiable (if you take the assumptions at face value - for example, “everyone in the world will have two cell phones” was a good one from the mobile phone hype cycle). Capital is sucked in which ultimately forces performance chasing and crowds stocks with money that doesn’t really believe in the thesis. “A twilight period where people continue to play the game, but no longer believe in the rules” emerges, as Soros put it.

The valuation of SaaS stocks in mid-2021 is a great example of what happens when the future is overvalued relative to the present - nobody cared about climbing inflation, that rates had nowhere to go but up, that these companies were reliant on ZIRP or that software could become more competitive.

Then, a negative catalyst occurs - this can but doesn’t have to be related to the technology, macro, credit, underwhelming earnings. The estimates start to seem unattainable, and the present begins to matter more when the future seems more uncertain. That exact mechanism that drove future optimism to unsustainable heights mechanically reverses, everyone needs out. The future begins to be discounted until it results in a sense of disillusionment with not just the stocks but the technology itself. This overshoots to the downside, investors eventually become disillusioned and seemingly allergic to anything having to do with the technology. This happens in a very asymmetric manner to the climb (“stairs up, elevator down”).

This is the crucible in markets for truly transformative tech. If advancements persist, another opportunity to get long presents itself before capital once again begins flowing into the companies (the internet, for example). If they don’t - not necessarily “the tech goes away” but rather that it ceases to advance once the capital isn’t free or plateaus or the economics prove to be unfavorable - the cycle will still start again, just with a new technology.

Or maybe not…maybe this time is different.