@Biohazard3737 It has to do with certain safety features.

Certain cybersecurity and biology related chats/projects get shifted down to Opus 4.8 automatically.

I watched this video this morning that goes over it and says which tasks you should reserve for fable.

https://t.co/2PVwKFh0CU

CRPO (Commercial Remaining Performance Obligation) is contracted revenue not yet recognized.

MSFT CRPO: $627B (+99% YoY), bigger than Google Cloud’s $462B, but ~45% comes from OpenAI.

Size supports the bull case. Customer concentration is the bear case.

Cloud growth rates, Q1 2026:

Google Cloud: 63% YoY, accelerated 16 points sequentially

AWS: ~21%, accelerated 4 points

Azure: 40% constant currency, accelerated 1 point

All three are running faster. Azure is running the slowest right now.

Roughly 45% of Microsoft's $627B Commercial Remaining Performance Obligation backlog is OpenAI.

Google Cloud's $462B backlog is more broadly distributed across enterprise customers.

Concentration risk always becomes more salient during a downturn.

Three concentrated stock pickers. Same company. Same quarter. Opposite conclusions.

→ TCI: cut MSFT from 10% → 1% of the portfolio

→ Egerton Capital: full exit

→ Bill Ackman: initiated a ~$2.1B position

Bull vs Bear

Chris Hohn vs @BillAckman

The risks to Office and Azure that Hohn sees

vs

The misrpiced fortress and OpenAI stake that Ackman sees

https://t.co/nue9dRcASZ

Tomorrow's post, bull vs bear on $MSFT

TCI cut $MSFT from 10% to 1% while @BillAckman initiated a $2.1B position.

I'll focus on:

1. What Chris Hohn said about the risks to Office.

2. What he meant by "azure risks"

3. Why Ackman thinks the "fortress" is mispriced.

Subscribe 👇

All three eventually mean-revert.

Acquisitions get written down.

Returns on incremental Capex drift toward cost of capital.

Stock issued at peak multiples re-rates.

Cooper, Gulen & Schill (2008) found these firms underperform by ~8 percentage points a year for five years.

🚨🚨🚨🚨🚨 Big time shenanigans going on in UTAH‼️

Utah speaker of the house Mike Schultz owns hundreds of acres of land right near the Stratos data Center site‼️

THIS IS JOURNALISM‼️

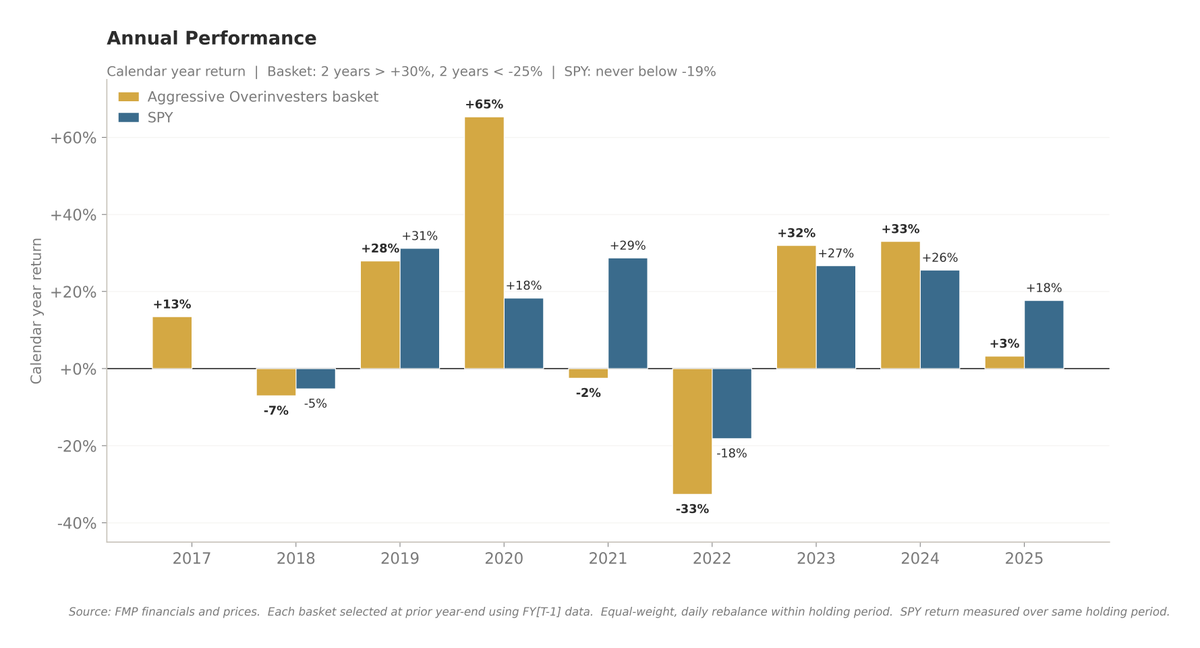

It still couldn't keep up.

Cumulative: 2.66x vs 3.50x for SPY. Annualized: 11.5% vs 14.9%. Through a favorable regime for aggressive corporate investing.

Tomorrow’s post dives into the bear case for Paychex (PAYX)

✔️ The AI disruption story that isn’t the immediate threat

✔️ The 2 bigger threats

✔️ & what the market is pricing it today.

Subscribe at

https://t.co/vnmwbFb3mu

The basket of 30 similar names rebalanced annually lagged SPY by 3.4 pp annualized over 9 years.

Even through a favorable period for aggressive corporate investing too.

https://t.co/52bX39PNKu

The 3 filters that flagged $CVNA, $APP, $W, and $ROKU in the year before each lost 80%+:

1. Top quintile asset growth (ex-acquisitions)

2. Top quintile external financing as % of prior-period assets

3. Top quintile EV/Sales