Passionate about markets & psychology of money | Guiding people from financial anxiety to clarity | Behavioural economist at heart | Cricket & lens on the side.

At ~82% Debt/GDP, India has more fiscal headroom than most large economies. That means:

— Room to spend on infrastructure without a debt crisis

— Monetary policy flexibility when global cycles turn

— Less risk of a sovereign shock derailing corporate earnings. #structuraltailwind

Everyone talks about growth & market return, but only a few talk about how it is funded !

Check Debt/GDP of nations:

Japan: ~250%

US: ~123%

France: ~112%

UK: ~101%

China: ~95–100%

India: ~82%

Fast growth is good, but fast growth with some fiscal discipline is even better.

India still has enuf room to manoeuvre if the world hits another rough patch.

One thing I’ve noticed over the years is that a lot of companies look completely unstoppable for a period of time, perhaps a few years, before eventually slowing down much more than investors ever imagined possible. The revenue explodes, margins improve, every quarter looks incredible, the stock keeps increasing, and after a while people start believing the company is somehow different from every other business that came before it.

But growth gets exponentially harder at scale and I do not think most investors fully appreciate this while it is happening. Growing 30% on $500m of revenue is one thing. Growing 30% on $2b is an entirely different challenge and growing 30% on $6b is even more different because now the company needs billions of incremental revenue every single year just to maintain the same growth rate. The larger the business becomes, the harder the math becomes underneath the surface.

At smaller scale, growth can come from almost anywhere. More distribution, new geographies, favorable industry conditions, market share gains, adjacent products, early adopters, stronger brand awareness, and a few things going right can create explosive growth because the revenue base is still relatively small. But eventually the easy growth disappears and the business suddenly requires much stronger execution just to maintain the same trajectory it once achieved much more effortlessly.

Competition reacts, saturation appears, expectations become much harder to satisfy, and management teams start making mistakes because they begin operating as if the earlier growth rate is permanent. That is usually when empire building starts appearing, acquisitions become more aggressive, costs rise too quickly, and capital allocation begins deteriorating even while reported numbers may still look “good.”

What makes this difficult is that the narrative usually feels strongest right before growth actually starts slowing. Investors begin extrapolating relatively temporary momentum far into the future because the previous few years looked extraordinary, and the stock often gets valued as if the recent growth rate has become permanent. Ironically, the moment investors feel the most confident is often the moment the future is becoming the least predictable.

You saw this with $CSCO, $PTON, $ZM, $BYND, $GPRO and countless other companies that at one point looked like they were taking over the world before reality eventually caught up to expectations. Even many elite businesses went through long periods where investors believed the growth story was permanently broken. There were periods where people thought $SBUX had overexpanded, $GOOG had matured too much, $AMZN had become too large to continue compounding, and $WMT best growth years were behind it.

That is what makes investing difficult because the stock often peaks long before the business peaks. Markets price expectations, not current numbers, which means a company can still report strong results while the stock collapses because expectations had detached too far from reality years earlier.

I think one of the biggest mistakes investors make is spending all their time studying fast growers instead of studying what actually happens after companies become large. That is usually where the real lesson is because very few businesses successfully navigate multiple decades of high growth while still maintaining strong returns on capital after the easy growth eventually disappears.

The difficult part is not finding companies growing fast today because there will always be companies growing fast. The difficult part is figuring out which businesses will still be larger, stronger, more relevant and competitively dominant 10 years from now after the easy growth is already gone.

🌹

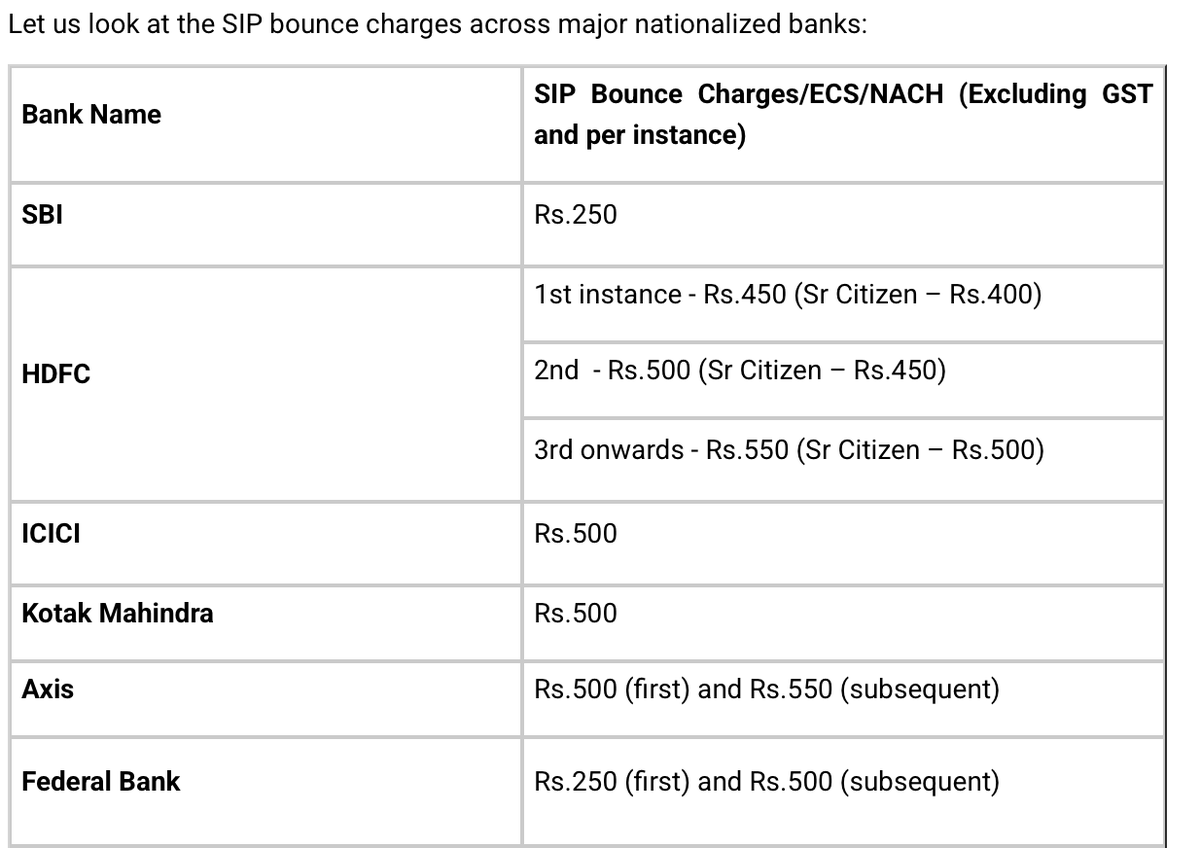

If your SIP runs via a NACH mandate, every failed debit can cost ₹250-₹750 + GST.

Now imagine this:

You have set up 5 SIPs through ICICI Bank

Due to some reason, balance is low... all 5 bounce…

ICICI Bank charges ₹500 per bounce.

That's ₹2,500 in charges.

+ 18% GST = ₹2,950 gone.

Imagine paying ₹590 as a penalty for a ₹1,000 SIP.

And because of such charges, some investors end up stopping their SIPs.

Isn't this daylight robbery by banks?

@equialpha Its 0%cagr return from inception till April 2025. Guess it was US deal benefit taiwan got. Extremely high standard deviation highly volatile. Many Indian funds in long run have given similar results with much lower risk.

@Nithin0dha request if agents can well trained. Have been telling there issue on sip manade verification on date of sip. And support informing processing will be done. Now telling it will be done next month as one cannot change date. Request if team can manage this things better.

@DisneyPlusHS dnt knw how to solve this. Just informing me i need to be logged in and after that app shuts of its own. What a plight of paid subscriber!!