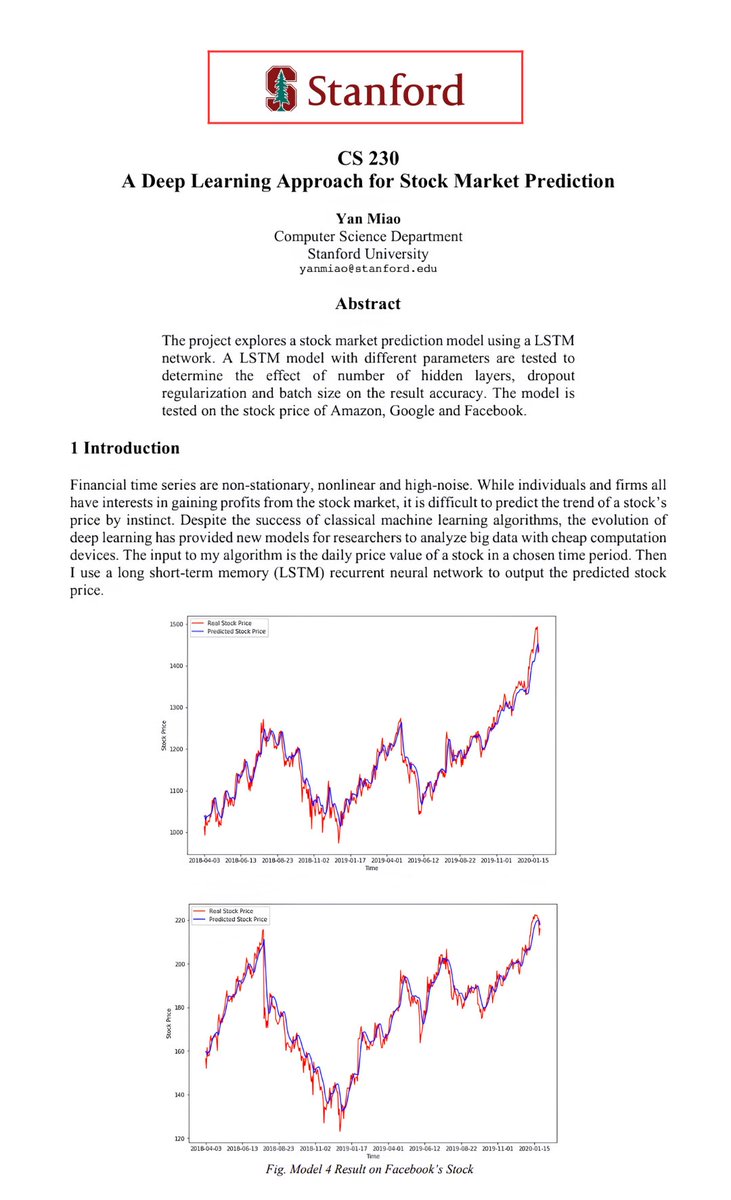

The secret of Hedge Funds is revealed in a 6 page PDF.

Stanford released the complete LSTM neural network framework for trading that quants at firms like Citadel & Two Sigma are known to use & released it for free.

Bookmark & read article below before someone takes it down.

CLAUDE CODE CAN NOW PULL LIVE DATA FROM 17,000+ STOCKS, CRYPTO PRICES, AND FINANCIAL STATEMENTS IN SECONDS.

One command. 60 seconds. Done.

Here is the exact setup:

Step 1: Open Claude Code and paste this:

claude mcp add --transport http financial-datasets https://t.co/cupUKrWK0C

Step 2: Authenticate

Type `/mcp` inside Claude Code and complete the OAuth flow in your browser.

Verify the connection anytime:

claude mcp list

Step 3: Start prompting

- "What is Apple's current P/E ratio and market cap?"

- "Show me Tesla's income statement for the last 4 quarters."

- "How has Bitcoin's price changed over the past year?"

That is it.

Claude Code now has direct access to real financial data across 17,000+ stocks, earnings reports, balance sheets, income statements, cash flow data, and crypto prices.

The analysts paying $24,000 a year for a Bloomberg Terminal are not going to be happy this exists.

Before this you needed a Bloomberg Terminal or a complex financial data API or hours of manual research across multiple sources.

Now you need one command and 60 seconds.

The quants, analysts, and portfolio managers who figure out how to combine Claude Code's reasoning with live financial data access will have a research edge that compounds every single day.

Bookmark this before you open your next brokerage account.

Docs if you run into errors: https://t.co/CgF6B3dS5V

Follow @cyrilXBT for every Claude Code integration that changes how you work with data.

This 2-hour Andrej Karpathy lecture will teach you how to build a Neural Network from scratch better than most engineers at top AI companies will ever bother to learn

No frameworks. No libraries. Just pure code and math

The same guy who built Tesla's Autopilot AI and co-founded OpenAI recorded this for FREE on YouTube

Bookmark & give 2 hours, no matter what. It'll be the most productive thing you do this week

Link to the repo: https://t.co/BSbuzHIgAN

Follow me @dr_cintas for more AI gems like this.

And if you want more, everyday I send a full email with the lastest AI resources, tutorials and news in my free newsletter. You can join here: https://t.co/kCad4bQXyg

LLM Knowledge Bases

Something I'm finding very useful recently: using LLMs to build personal knowledge bases for various topics of research interest. In this way, a large fraction of my recent token throughput is going less into manipulating code, and more into manipulating knowledge (stored as markdown and images). The latest LLMs are quite good at it. So:

Data ingest:

I index source documents (articles, papers, repos, datasets, images, etc.) into a raw/ directory, then I use an LLM to incrementally "compile" a wiki, which is just a collection of .md files in a directory structure. The wiki includes summaries of all the data in raw/, backlinks, and then it categorizes data into concepts, writes articles for them, and links them all. To convert web articles into .md files I like to use the Obsidian Web Clipper extension, and then I also use a hotkey to download all the related images to local so that my LLM can easily reference them.

IDE:

I use Obsidian as the IDE "frontend" where I can view the raw data, the the compiled wiki, and the derived visualizations. Important to note that the LLM writes and maintains all of the data of the wiki, I rarely touch it directly. I've played with a few Obsidian plugins to render and view data in other ways (e.g. Marp for slides).

Q&A:

Where things get interesting is that once your wiki is big enough (e.g. mine on some recent research is ~100 articles and ~400K words), you can ask your LLM agent all kinds of complex questions against the wiki, and it will go off, research the answers, etc. I thought I had to reach for fancy RAG, but the LLM has been pretty good about auto-maintaining index files and brief summaries of all the documents and it reads all the important related data fairly easily at this ~small scale.

Output:

Instead of getting answers in text/terminal, I like to have it render markdown files for me, or slide shows (Marp format), or matplotlib images, all of which I then view again in Obsidian. You can imagine many other visual output formats depending on the query. Often, I end up "filing" the outputs back into the wiki to enhance it for further queries. So my own explorations and queries always "add up" in the knowledge base.

Linting:

I've run some LLM "health checks" over the wiki to e.g. find inconsistent data, impute missing data (with web searchers), find interesting connections for new article candidates, etc., to incrementally clean up the wiki and enhance its overall data integrity. The LLMs are quite good at suggesting further questions to ask and look into.

Extra tools:

I find myself developing additional tools to process the data, e.g. I vibe coded a small and naive search engine over the wiki, which I both use directly (in a web ui), but more often I want to hand it off to an LLM via CLI as a tool for larger queries.

Further explorations:

As the repo grows, the natural desire is to also think about synthetic data generation + finetuning to have your LLM "know" the data in its weights instead of just context windows.

TLDR: raw data from a given number of sources is collected, then compiled by an LLM into a .md wiki, then operated on by various CLIs by the LLM to do Q&A and to incrementally enhance the wiki, and all of it viewable in Obsidian. You rarely ever write or edit the wiki manually, it's the domain of the LLM. I think there is room here for an incredible new product instead of a hacky collection of scripts.

Dan Sundheim manages $30B+ across public and private markets. He just sat down for ~75 minutes on Invest Like the Best with Patrick O'Shaughnessy

Just one of the sharpest investors alive explaining exactly how he sees AI, markets, and the biggest risk nobody wants to talk about.

My notes:

𝟭. 𝗛𝗲 𝗯𝗮𝗰𝗸𝗲𝗱 𝗔𝗻𝘁𝗵𝗿𝗼𝗽𝗶𝗰 𝘄𝗵𝗲𝗻 𝗲𝘃𝗲𝗿𝘆𝗼𝗻𝗲 𝗰𝗮𝗹𝗹𝗲𝗱 𝗶𝘁 𝘁𝗵𝗲 𝗟𝘆𝗳𝘁 𝘁𝗼 𝗢𝗽𝗲𝗻��𝗜'𝘀 𝗨𝗯𝗲𝗿.

Smart people told him investing in the second player was not the path to glory. Sundheim disagreed because the models were not differentiated enough at that stage to crown a winner. His conviction came from reading Dario Amodei's essays and pattern-matching them to Jeff Bezos's 1997 Amazon shareholder letter, which was the only sign of greatness in a sea of red ink.

The best investors I've studied almost always point to the same thing: the CEO letter, the founder essay, the written artifact. The clarity of thought behind them. If you want an edge, read what founders write and ignore everything else. Bezos, Dario, Zuckerberg's Metaverse letter, Satya's memo. The signal is always in the writing.

𝟮. 𝗟𝗟𝗠𝘀 𝗮𝗿𝗲 𝗡𝗲𝘁𝗳𝗹𝗶𝘅 𝗽𝗹𝘂𝘀 𝗦𝗽𝗼𝘁𝗶𝗳𝘆.

The Netflix part: massive upfront capital to train a model, then sell access at high incremental margins. Reinvest the cash flow to build the next model. Early movers compound this advantage until it becomes nearly impossible to catch them.

The Spotify part: the actual model outputs are not that differentiated. What creates lock-in is personalization. The more an AI knows about your life, your health, and your preferences, the harder it becomes to switch, just like Spotify turned commodity music into a sticky product worth paying a premium for.

This is the most elegant framing of the AI business model I've heard. The Netflix layer explains the capex. The Spotify layer explains the moat. Together, they explain why four or five players will dominate, and everyone else will lose.

𝟯. 𝗧𝗵𝗲 𝗿𝗲𝗮𝗹 𝗟𝗟𝗠 𝗱𝗲𝗯𝗮𝘁𝗲 𝗶𝘀 𝗻𝗼 𝗹𝗼𝗻𝗴𝗲𝗿 "𝗶𝘀 𝘁𝗵𝗶𝘀 𝗮 𝗴𝗼𝗼𝗱 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀?" 𝗜𝘁 𝗶𝘀 "𝗱𝗼𝗲𝘀 𝘁𝗵𝗲 𝗰𝗮𝗽𝗶𝘁𝗮𝗹 𝗶𝗻𝘁𝗲𝗻𝘀𝗶𝘁𝘆 𝗽𝗮𝘆 𝗼𝗳𝗳?"

The commoditization fear is dead. Gross margins are high, APIs are durable, and Claude Code has proven these are sticky products. The remaining question is whether the unprecedented capital spent on training models will generate returns or whether enterprise adoption will be slower than expected. And at this level of financial leverage, slower-than-expected is a serious problem.

Two years ago, the smart-sounding bear case was "AI will be huge but the companies won't make money, just like airlines." That debate is over. The margins are real, the switching costs are real, and the competitive field has narrowed to four or five players. But Sundheim is not relaxing. The new worry is simpler and scarier: you are burning cash at a rate no business in history has ever burned cash, and the payoff depends on enterprises adopting fast enough to justify it. If adoption is even 18 months slower than the models assume, the math will get ugly.

𝟰. 𝗙𝗼𝗰𝘂𝘀 𝗯𝗲𝗮𝘁𝘀 𝘀𝗰𝗼𝗽𝗲. 𝗔𝗹𝗺𝗼𝘀𝘁 𝗮𝗹𝘄𝗮𝘆𝘀.

OpenAI is going after consumer, enterprise, Apple hardware, robotics, and science all at once. Anthropic recognized early that consumer was not working, pivoted to enterprise, and built a dominant position in coding. Sundheim struggles to name historical examples of a company succeeding at everything simultaneously. Amazon waited seven years after its IPO before launching AWS.

The person trying to be a founder, an investor, and an influencer at the same time should read this point three times. Focus compounds. Optionality is a trap when it becomes a substitute for commitment.

𝟱. 𝗛𝘆𝗽𝗲𝗿𝘀𝗰𝗮𝗹𝗲𝗿𝘀 𝗮𝗿𝗲 𝗯𝗲𝗰𝗼𝗺𝗶𝗻𝗴 𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗮𝗹𝗹𝘆 𝘄𝗼𝗿𝘀𝗲 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀𝗲𝘀.

AWS and Azure will grow rapidly in the near term because their largest customers, the LLMs, are expanding rapidly. But those same LLMs will eventually generate massive free cash flow and insource their compute. The customer base is concentrating from "every corporation in the world" to a handful of AI giants. Meta already insourced everything. The LLMs are actually better at running GPU clusters than the traditional hyperscalers, who built their expertise around CPUs.

Contrarian take, but the logic is airtight. The hyperscalers are financing their own displacement. Their best customers are their future competitors. Never ask a barber if you need a haircut, and never assume your biggest customer will stay your customer forever.

𝟲. 𝗦𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗶𝘀 𝘁𝗵𝗲 𝗳𝗶𝗿𝘀𝘁 𝗔𝗜 𝘀𝗵𝗼𝗿𝘁.

Before 2026, you could not make money shorting anything because of AI. Now you can. Software is the first wave. But Sundheim's view is nuanced: systems of record like ERP and CRM are hard to displace. He literally asked the LLM companies if they were building their own ERP. They said no, they were buying from a vendor. That is a powerful signal.

The Walmart analogy is the one that will stick. Walmart did not die from e-commerce. It adapted painfully over the years and came out the other side. Software companies with real distribution and system-of-record status will do the same. But sitting back and assuming the moat holds? That is how you become Blockbuster.

𝟳. 𝗘𝘃𝗲𝗻 𝗶𝗳 𝘀𝗰𝗮𝗹𝗶𝗻�� 𝗹𝗮𝘄𝘀 𝘀𝘁𝗼𝗽𝗽𝗲𝗱 𝘁𝗼𝗱𝗮𝘆, 𝗔𝗜 𝘀𝘁𝗶𝗹𝗹 𝗿𝗲𝘀𝗵𝗮𝗽𝗲𝘀 𝘁𝗵𝗲 𝗲𝗰𝗼𝗻𝗼𝗺𝘆.

Three years of adoption alone, people just learning how to use current models, would produce profound economic changes. And betting that scaling laws will stop requires ignoring all available evidence. To really think about what is coming, Sundheim says you have to think like a science fiction writer, not an investor.

This is an underrated framing. Most AI skeptics argue that models must keep improving for the thesis to hold. Sundheim flips it: the installed base is already good enough to change everything. The improvement curve is just a bonus.

𝟴. 𝗧𝗵𝗲 𝗚𝗮𝗺𝗲𝗦𝘁𝗼𝗽 𝗰𝗿𝗶𝘀𝗶𝘀 𝘁𝗮𝘂𝗴𝗵𝘁 𝗵𝗶𝗺 𝘁𝗵𝗮𝘁 𝗵𝗮𝘃𝗶𝗻𝗴 𝗮 𝗽𝗹𝗮𝗻 𝗰𝗵𝗮𝗻𝗴𝗲𝘀 𝗲𝘃𝗲𝗿𝘆𝘁𝗵𝗶𝗻𝗴.

D1 went from top of the world to "everyone thinks we're going out of business." The pivotal moment: LP dinners scheduled at the exact trough of the drawdown. His president said to cancel them. Sundheim said no, this is the most important time to face investors. He laid out a plan for singles and doubles. Slow recovery, lower risk, sustainable. And then he just executed, one day at a time.

The emotional insight here is universal. When the world is collapsing, and there is nothing you can do, helplessness is unbearable. But the moment you have a plan you believe in, even if the numbers are still terrible, the perspective shifts entirely. This applies to investing, startups, careers, health, basically everything.

𝟵. 𝗧𝗵𝗲 𝗺𝗼𝘀𝘁 𝗯𝗲𝗮𝘂𝘁𝗶𝗳𝘂𝗹 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀 𝗶𝘀 𝗮 𝗹𝗼𝘄-𝗰𝗼𝘀𝘁 𝗽𝗿𝗼𝗱𝘂𝗰𝗲𝗿 𝘄𝗶𝘁𝗵 𝗮 𝗳𝗹𝘆𝘄𝗵𝗲𝗲𝗹.

Not Moody's. Not S&P. Those are great businesses. But the truly beautiful ones are SpaceX with launch, Costco with groceries, and Amazon with e-commerce. Low cost drives volume, volume drives lower cost, and the feedback loop becomes impenetrable.

This is pure Munger energy. Most people think beautiful businesses are high-margin toll booths. Sundheim says the real beauty lies in relentless cost reduction at scale. The companies that seem to be leaving money on the table are actually building the deepest moats.

𝟭𝟬. 𝗧𝗮𝗶𝘄𝗮𝗻 𝗶𝘀 𝘁𝗵𝗲 𝗯𝗶𝗴𝗴𝗲𝘀𝘁 𝘁𝗮𝗶𝗹 𝗿𝗶𝘀𝗸 𝗶𝗻 𝘁𝗵𝗲 𝘄𝗼𝗿𝗹𝗱.

Taiwan makes 90%+ of the world's most advanced chips. That supply chain is fragile, easy to destroy, and hard to replicate. If it breaks, we get a depression-level event. Sundheim's preferred path: replicate the supply chain domestically over 10-20 years while buying time with China. The problem: there is no scenario where everyone, the US, China, and Taiwan, is happy.

And AI just raised the stakes to the stratosphere. Every dollar spent on frontier AI training runs through TSMC. This is not a geopolitical curiosity. It is the single point of failure for the entire AI revolution. If you are allocating capital right now and not stress-testing your portfolio for this scenario, you are not doing your job.

𝟭𝟭. 𝗛𝗲 𝗴𝗼𝘁 𝗵𝗶𝘀 𝗳𝗶𝗿𝘀𝘁 𝗷𝗼𝗯 𝗯𝘆 𝗰𝗿𝗮𝘀𝗵𝗶𝗻𝗴 𝗮 𝘀𝘁𝗼𝗰𝗸 𝗳𝗿𝗼𝗺 𝗮𝗻 𝗮𝗻𝗼𝗻𝘆𝗺𝗼𝘂𝘀 𝗳𝗼𝗿𝘂𝗺 𝗽𝗼𝘀𝘁.

In 2002, Sundheim was a nobody analyst at Bear Stearns. He discovered Value Investors Club, consumed every idea posted, then wrote up Orthodontic Centers of America as a fraud case for an interview. Before presenting, he posted it on VIC. The stock halved. Mutual fund managers started calling Bear Stearns, looking for answers. He walked into his interview, and the hedge fund just asked, "What did you do?" That write-up became his calling card for getting hired at Viking Global.

The internet is still the single best place to build a career from nothing. Write something so good that it moves markets, changes minds, or just makes one important person pay attention. Sundheim did it in 2002 from an anonymous forum. You can do it today from a Substack, a tweet thread, or a GitHub repo. The barrier has never been lower.

𝟭𝟮. 𝗣𝘂𝗯𝗹𝗶𝗰 𝗺𝗮𝗿𝗸𝗲𝘁𝘀 𝗮𝗿𝗲 𝗹𝗲𝘀𝘀 𝗲𝗳𝗳𝗶𝗰𝗶𝗲𝗻𝘁 𝘁𝗵𝗮𝗻 𝗲𝘃𝗲𝗿.

Passives, retail, quants, and multi-manager pods have replaced fundamental investors as the dominant market participants. These players are not making decisions based on long-term intrinsic value. Short-term price moves now exaggerate the true change in value, creating an enormous opportunity for anyone with a fundamental view and the right duration.

If you are a young fundamental analyst wondering whether there is still room for you, this is your answer. The arena is less crowded than ever. The players left are mostly momentum-driven, algo-driven, or too short-term-oriented to compete over a 3-5-year horizon. The inefficiency is real. Always has been, arguably more so now.

Sundheim's closing line says it all: he has tons of cash flows and no terminal value. His portfolio companies have tons of terminal value and no cash flows. And so they are good together.

A beautiful partnership model in one sentence.

The full podcast is worth your time. Link in thread.

> be random guy on the internet

> makes decisions purely on vibes

> misses a few huge opportunities in crypto

> wonders why his life keeps looking random

> stumbles on a weird article about probability theory

> realizes every decision has expected value

> realizes markets are just Bayesian machines

> realizes most "genius trades" are survivorship bias

> realizes most people size bets completely wrong

> realizes he’s been playing the game with no math at all

> opens Polymarket

> starts thinking in probabilities instead of opinions

> suddenly the world starts looking like a giant EV calculator

turns out most life outcomes are just probability problems people never bothered to model:

> career decisions

> investments

> relationships

> risk

all of it is just EV + Bayes + Kelly

> the crazy part?

none of this math is complicated

> you can literally learn the models in this article

> use AI to help you apply them

> and completely upgrade how you think in a few months

but most people will keep making decisions the same way

> vibes

> emotions

> scroll Twitter

> one lucky success story

and wonder why nothing compounds

I accidentally discovered how to compress a semester of learning into 48 hours.

A grad student at MIT showed me his NotebookLM setup. I thought he was just organized. Then I watched him pass a qualifying exam on a subject he'd never studied before.

Here's exactly what he did:

First: he didn't upload a textbook.

He uploaded 6 textbooks, 15 research papers, and every lecture transcript he could find on the subject.

Then he asked NotebookLM one question:

"What are the 5 core mental models that every expert in this field shares?"

Not "summarize this." Not "explain this topic."

Mental models. The stuff that takes professors years to develop.

But the next part is what broke my brain.

He followed up with:

"Now show me the 3 places where experts in this field fundamentally disagree, and what each side's strongest argument is."

In 20 minutes he had a map of the entire intellectual landscape of the field:

the debates, the consensus, the open questions.

Most students spend a full semester just figuring out what those debates even are.

Then he did something I've never seen before.

He asked:

"Generate 10 questions that would expose whether someone deeply understands this subject versus someone who just memorized facts."

He spent the next 6 hours answering those questions using the source material. Every wrong answer triggered a follow-up:

"Explain why this is wrong and what I'm missing."

By hour 48, he could hold a conversation with his thesis advisor without getting destroyed.

The tool didn't change. The questions did.

Most people treat NotebookLM like a fancy highlighter.

These students are using it like a private tutor who has read everything ever written on the subject.

The difference between a semester and 48 hours isn't the amount of content.

It's knowing which questions to ask.