$META: upcoming AI model “Watermelon” has caught up to OpenAI’s GPT 5.5.

Wang noted it uses an "order of magnitude" more compute than its predecessor “Avocado”.

Who said they were out of the AI race again?

Just this hour:

BlueCrest Capital Management and its Billionaire Michael Platt crossed the threshold and disclosed a 5.6% stake in $CCXI.

I knew Agility Robotics would be popular…

Just dropping these 3 slides from Agility Robotics ( $CCXI ) presentations.

For the US robotic program doomposters:

1. “75% of parts” - sourced from the USA

2. Just eyeballing the graph, looks like <$30k BOM mass production.

People were just looking at the ~$145K cost.

3. 10,000 RoboFab capacity, and they build in Salem/Pittsburgh/Fremont (USA).

So looks like majority US supply chains with targets of <$30K mass production

It does help they’re backed by $AMZN / SoftBank / Foxconn / $NVDA as investors to get this done.

Just personal thoughts as a shareholder in $CCXI (NFA):

My personal biggest fear were US humanoid leaders like $TSLA were just building out their entire supply chains in China.

So US robotics could just be export controlled/halted down the road.

eg. South China Morning Post: ‘Optimus chain’: Chinese suppliers form the backbone of Tesla’s humanoid robot initiative and engaged with hundreds of Chinese component suppliers.

And that Western companies are not able to lower costs to a competitive level + are forced to use Chinese components.

I'm still not sure how they're going to do it but if Agility can achieve those mass production targets with that BOM cost in the USA/West.

It would be a great validation for Made in America US robotics programs.

IMO the top 5 US humanoid programs right now in terms of commercialization potential are:

1. Tesla Optimus

2. Figure

3. Agility Robotics

4. Boston Dynamics (yeah KR parent)

5. Apptronik

Tesla is a $1T+ company. Figure is private and valued around ~$39B. Owning Boston Dynamics through Hyundai is a bit messy.

And I’d prefer not to invest in adversarial programs just as a personal preference.

So I’ve been personally excited for Agility to be listed as early as September.

this is just a beta selloff for $MU and $SNDK -- there is a @vector__news story out that explains plainly why $META is not going to be renting out cloud compute anytime soon. if the market was taking this seriously $NVDA would be -10% to -20%, recommend buying momentum

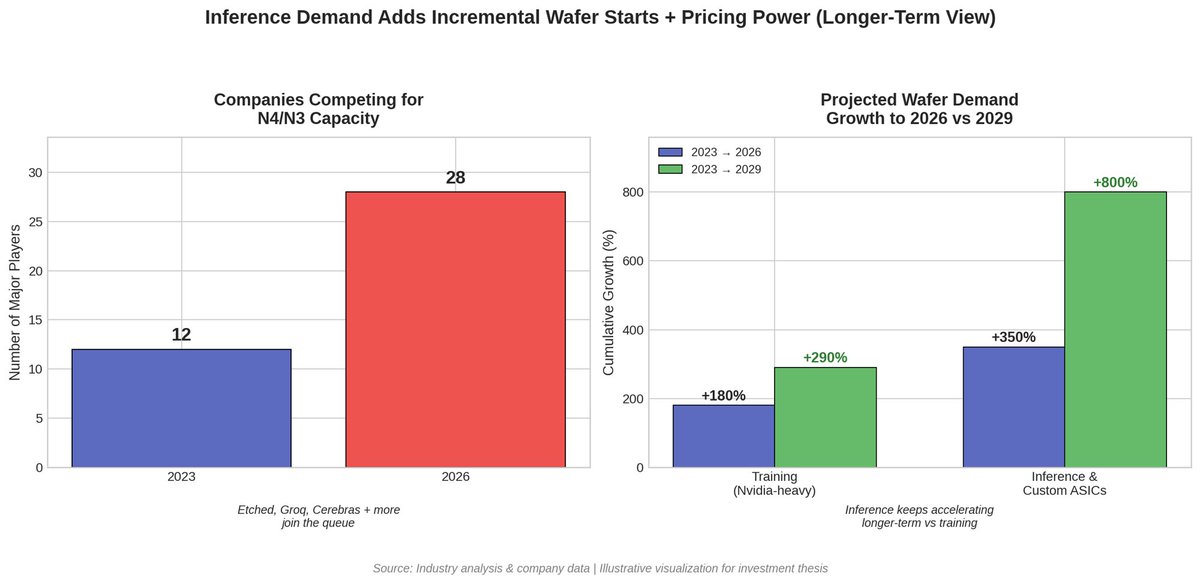

Etched just made $TSM leading-edge capacity even scarcer. $1B in contracts means real wafer demand hitting a queue that is already full. Pricing power follows.

Inference scales with usage, not capex cycles. More AI adoption = more inference chips = more N4P/N3 wafer starts at TSMC. TSMC has been raising advanced node pricing 5-10% annually. That’s about to accelerate. The street is not modeling this. When those margins inflect, $TSM re-rates.

Etched working silicon is on TSMC N4P. First-pass (A0) success, no respin needed. Already running DeepSeek, Qwen, Mamba, and Llama on their inference systems.

Etched secured a trategic investment from TSMC’s affiliated venture arm. This is a capacity commitment signal. TSMC backing a chip startup means they see real wafer volume coming.

Morgan Stanley: Electronic Components

> AI server accelerator boards require roughly twice the total capacitance with each new generation of GPUs. Because installation space is limited, compact, high-capacitance MLCCs are seeing surging demand.

> Murata holds a 40.8% total MLCC market share (followed by SEMCO at 22.5% and Taiyo Yuden at 11.3%). Murata is currently the only company capable of stably mass-producing all the ultra-compact, high-capacitance components needed for AI servers.

> Murata's sales to AI/data centers are projected to jump 85–90% YoY in F3/27, comprising 20–25% of its total MLCC sales. This includes ~40% volume growth and ~50% ASP growth driven by a richer product mix.

> Unlike some regional competitors (in China, South Korea, and Taiwan) that maximize short-term profits through indiscriminate price hikes on commoditized parts, Murata adjusts pricing flexibly to protect long-term market share and prevent lower barriers to entry.

Ibiden:

> Ibiden began volume shipments of ABF package substrates for NVIDIA’s Blackwell and Rubin architectures. Sales for Rubin are expected to eclipse Blackwell in 1Q F3/27.

> Despite clear earnings growth, Morgan Stanley notes that FactSet consensus numbers are too high. For example, for F3/28, Morgan Stanley forecasts operating profit (OP) at ¥128.5bn compared to the company forecast of ¥150bn and consensus of ¥151.5bn.

> Meaningful profit contributions from EMIB-T products are not expected to materialize until F3/29 onward, and achieving profit margins comparable to NVIDIA’s legacy offerings may prove difficult.

Taiyo Yuden:

> Taiyo Yuden froze its capital expenditure during the second half of 2024. As a result, its MLCC production capacity growth was bottlenecked at only ~5% for F3/26.

> This capacity constraint has actively limited the company’s ability to capture new high-volume business during the current AI server demand surge.

> While demand for critical AI server MLCC specifications (like the 1608 size 100μF, 1005 size 47μF, and 0603 size 10μF) is soaring, Taiyo Yuden's timeline for stable mass production remains unclear. Analysts note that by the time Taiyo Yuden matches Murata's current tech, Murata will likely already be mass-producing even smaller, higher-capacitance models.

Might I add for no reason.. could this be related to the SPAC $CCXI & robotics sector as a whole? Price targets since May indicate an average ~$47.29, with the most recent being a restricted analyst/broker with a $75 target June 17th.

Estimates per FactSet

A $100B fully diluted market cap was insane

$CBRS is now coming back down to reality

For those interested...

If they achieve $6B in revenue by 2028 at their targeted 60% gross margin, that would imply $3.6B in gross profit

So now it’s trading at 10x 2028 estimated gross profit (optimistically) on a basic market cap basis. On a fully diluted basis, it’s 15x

Operating leverage will still be far from optimal by then, but $AMD and $AVGO trade at roughly 30x and 20x 2026 gross profit, respectively

So Cerebras isn’t necessarily insanely expensive anymore, but it has relatively weak market positioning compared with others, and its operating margins will take a long time to match competitors

They’ll also probably never match the margins of pure fabless designers, because they run their own AI cloud, which naturally brings depreciation and utilization risk

$GOOGL has reportedly limited Meta’s use of Gemini after $META sought more AI compute capacity than Google could provide, per FT.

The limits have disrupted and delayed some of Meta’s internal AI projects, while Meta has pushed staff to use AI tokens more efficiently.

🚨APPLE AND MICRON GO HEAD TO HEAD IN AN ALL-OUT PUBLIC CLASH

Apple CEO Tim Cook went public blaming memory suppliers for the company's latest price hikes.

Micron's Chief Business Officer Sadana fired back, telling the WSJ that "certain customers" forced memory prices to rock-bottom levels during the last market downturn, preventing the Micron from investing as profits collapsed.

Without naming Apple directly, Micron executive says those aggressive pricing demands starved the industry of investment, forcing today's global memory shortage and the very price hikes now hitting consumers.

Recommended reads for the week

SemiAnalysis — China’s CXMT Is Set to Challenge DRAM Incumbents

Goldman Sachs — Americas Technology: Hardware — Expert Network Series: CPU Server Demand Driven by Refresh, Agentic AI

Morgan Stanley — Old Memory: Better to Buy More

J.P. Morgan — First Principles — AI Power Infrastructure: Following the Power