Bridge → Stripe. BVNK → Mastercard. Reap → Kraken (today, $600M). 4 acquisitions in 18 months, $3B+ deployed. The stablecoin infrastructure market is consolidating before most fintechs have even noticed it exists.

Stripe's $1.1B acquisition made Bridge the obvious answer. The non-obvious answer is that the rest of the world isn't waiting for Stripe.

Stablecoin infrastructure isn't one product. It's virtual accounts, on/off-ramps, local rails, FX, stablecoin orchestration, issuance, custody, and compliance, each requiring a different layer. That's why the category has split into a full stack of specialized providers across every region.

Bridge is still the reference. But its share of the global market keeps shrinking as regional champions pick up corridors Bridge doesn't reach.

The Stablecoin Infrastructure Stack reflects the diversity of corridors and use cases:

- USA & Canada: Sphere Labs, Mural Pay, Brale, Modern Treasury, Layer2 Financial, Iron, Conduit, Routefusion, Crossmint, Cybrid

- Europe: BVNK, Due, Currencycloud, Rapyd, Merge Money, Fipto, OpenPayd, Wise Platform, AMINA Bank

- LATAM: Bitso, dLocal, Pomelo, CambioReal, BlindPay, Koywe

- UAE & Middle East: Hubpay, TransFi, Fuze

- Africa: Yellow Card, Flutterwave, ivorypay, Quidax, Paychant, VALR, Kotani Pay

- Asia: Tazapay, Stables, Triple-A, PhotonPay

Aggregators connecting them all: Borderless xyz plugs regional liquidity providers into a single global stablecoin network, turning the fragmentation above into one API.

Capital and consolidation explain this shift. 4 acquisitions in 18 months, $3B+ deployed:

- Bridge → Stripe ($1.1B)

- BVNK → Mastercard ($1.8B closing late 2026)

- Iron → MoonPay

- Reap → Kraken

By 2026, the global B2B stablecoin payment volume breaks down roughly as:

- ~60% Asia ($245B, concentrated in Singapore, Hong Kong, Japan)

- ~23% North America ($95B)

- ~12% Europe ($50B)

- The rest split between LATAM, Africa, and MENA, growing fastest

Stablecoin infrastructure is no longer a single product. It's becoming a critical infrastructure layer of every cross-border business, and the map is global.

PS: I post about payments with @Subyhq, stablecoins & the reality of building a payment startup, every week. Follow for more!

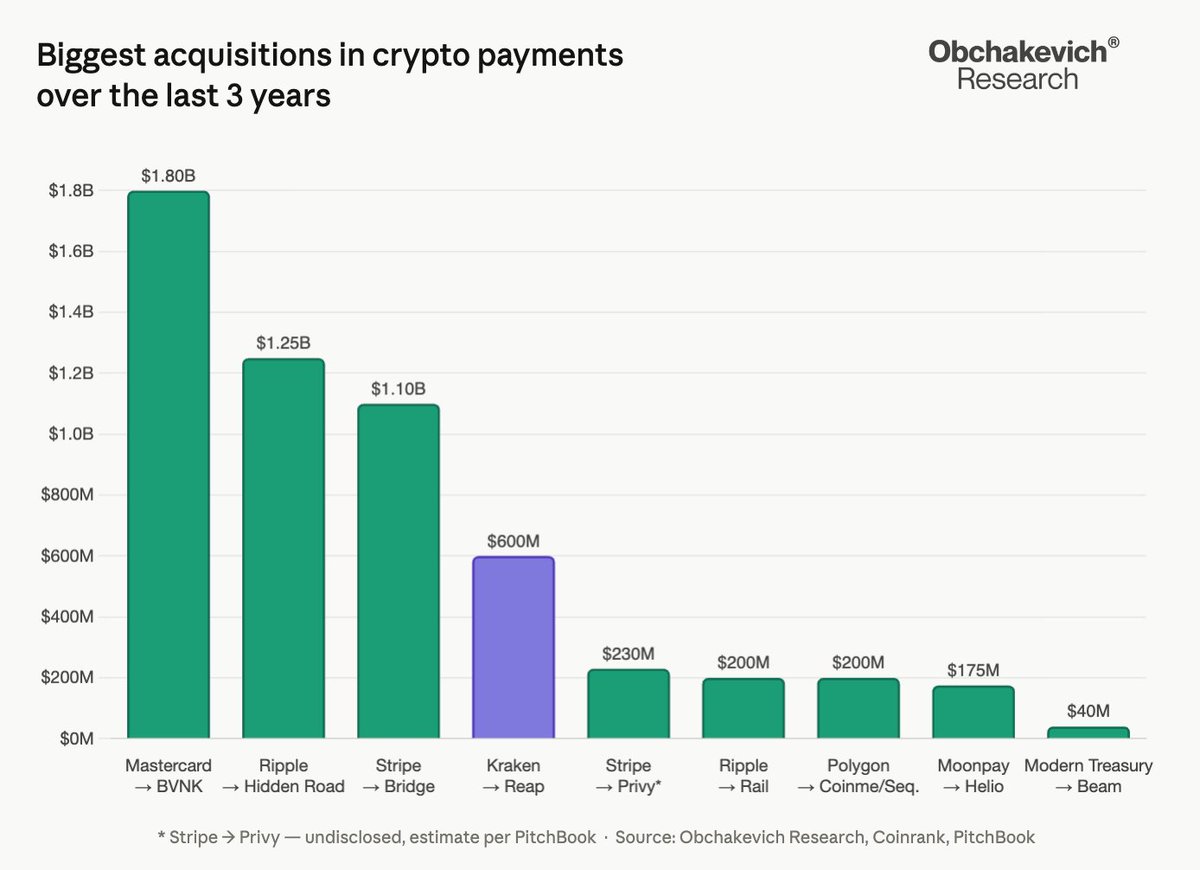

Kraken just acquired Reap for $ 600M - and it's not just a bold move, it's a signal.

@reapglobal builds payment infrastructure for businesses: corporate cards, expense management, cross-border settlements. For @krakenfx, this is a direct entry into the B2B payments stack - territory that crypto exchanges rarely touched before.

But zoom out, and Kraken isn't alone.

Over the past three years, the payments sector has become the most active M&A battleground in crypto. Nine major deals, over $5.5B deployed:

@Mastercard → @BVNKFinance ($1.8B): the clearest sign yet that card networks are buying into stablecoin infrastructure rather than building it.

@Ripple → Hidden Road ($1.25B): a prime brokerage play, but with settlement and payments at its core.

@stripe → @Stablecoin ($1.1B): the deal that set the tone for everything that followed, stablecoins as serious payment rails, not a crypto experiment .

@stripe → @privy_io (~*$230M): wallets as the missing layer on top of Bridge's orchestration

@Ripple → Rail ($200M) and @0xPolygon → @Coinme / @0xsequence ($200M): infrastructure bets on on/off-ramp and wallet layers.

@moonpay → Helio ($175M): doubling down on merchant-facing crypto payments.

@ModernTreasury → @beam_cash ($40M): quiet but telling - a $ 2B fintech adding stablecoin rails for corporates.

The pattern is consistent. Whether it's a card network, a crypto exchange, or a payments fintech, everyone is acquiring the same thing: the infrastructure to move money onchain.

The consolidation phase has started. What used to be fragmented startups building isolated pieces of the stack is now becoming integrated platforms owned by well-capitalized players.

The question isn't whether stablecoin payments will go mainstream. It's who controls the rails when they do.

The final rewards text in the CLARITY Act is now public.

We’ve been clear throughout this process: much of this debate was based on imagined risks, not real evidence, nor was it based on a real understanding of how crypto actually works.

Nevertheless, the crypto industry showed up to engage. Through months of meetings, the @WhiteHouse, @USTreasury, @BankingGOP, @SenThomTillis and @Sen_Alsobrooks finally arrived at a compromise.

In the end, the banks were able to get more restrictions on rewards, but we protected what matters – the ability for Americans to earn rewards, based on real usage of crypto platforms and networks. We also ensured the US can be at the forefront of the financial system – which in this competitive geopolitical era is paramount.

That’s important for innovation, consumers and America's national security.

Now that this issue is behind us, it’s time to focus on the broader bill. While this debate has been underway, lots of progress has been made on other areas like token classification, defi, and tokenization. We’re excited to review the full, final text, and for the bill to move forward.

It’s time to get CLARITY done.

1. Stablecoin Payments boosted by Stableport

On April 20th, Stableport a platform that helps companies pay each other across borders using stablecoins launched

It is backed by Polygon to replace slow traditional banking processes

Check it out here: https://t.co/AswbFawkNV