The course @MattFizell and I built for new financial planners is open again! We used the feedback from the Beta Group to make it even more valuable.

Level up your career for less than the cost of a college textbook ($97).

🚀

What if just the 10 'right' people seeing your content could grow your firm faster than 10,000 random viewers? Growing an advisory firm doesn’t always require reaching the largest audience. In many cases, the right audience—clearly defined and intentionally engaged—can be far more powerful than broad visibility. https://t.co/jFUr3ko6CF

In today's #FASuccess episode, Justin Brownlee, founder of Brownlee Wealth Management, shares how he built a $500 million RIA serving just 75 households by targeting a specific niche and using LinkedIn with intention. In this episode, we break down how he created focused blog and podcast content for his ideal target client, strategically built a LinkedIn network inside target companies, and prioritized quality engagement over vanity metrics. #podcast #financialadvisorpodcast

New Planner Collective has teamed up with Zahn Associates Inc. to offer a scholarship for a live review for the CFP® Exam for July 2026!

This scholarship will provide 1 candidate with everything needed for exam prep in-person or virtually: Pre-study Materials, 4-day class, and Post Study Materials.

Link in the comments!

Share with your favorite future CFP®

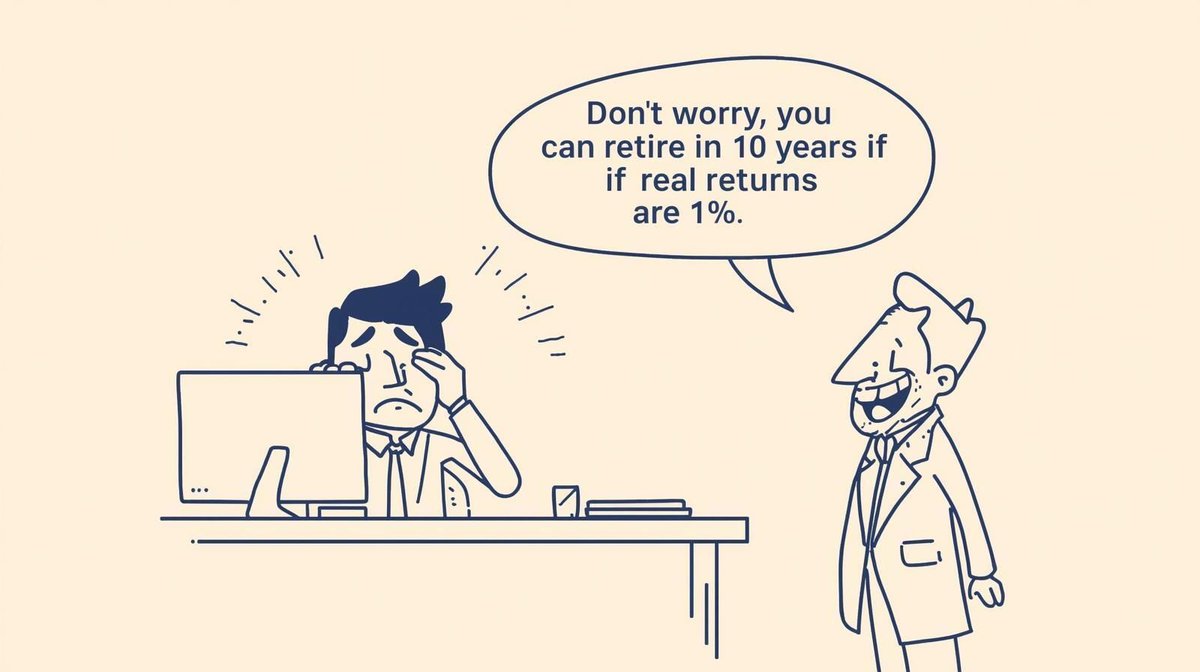

Retirement projections (or a financial plan) that are too conservative are just as dangerous as those that are too aggressive.

If your projections are unrealistic either way, they don't really give you any actionable information. Just a false sense of security or fear.

The downside of an advisor being overly conservative is that a client may accumulate more than they need. Which is infinitely less painful than the downside of an advisor being overly aggressive, leading their client to run out of money. Advisors often prefer to build plans with a margin of safety, which can be beneficial. But if the margin of safety is unreasonably wide, it can do real damage:

- Leave clients working longer than they need to in a job they don't like

- Prevent clients from spending money in retirement that would meaningfully improve their quality of life

- Create a baseline amount of anxiety as your perception is that you're walking a financial tightrope that isn't actually there

This is why the right financial planning assumptions aren't a single set, but rather several different sets, so clients can begin to understand the range of potential outcomes.

Ideally, none of our employees are operating at 100% capacity.

Every person needs time to step back and think through how to optimize their work.

Excellence isn't cultivated by people who execute endlessly, but by iterating and ideating endlessly until everything is flawless.

Business isn’t about endlessly optimizing; it’s all about finding the right places to choose friction.

"This activity doesn't scale well, but it would really go a long way in making Client X a raving fan of ours."

"I could do this and it’d take 20 minutes, or I can delegate this and it takes me an hour."

The magic happens through discernment, and knowing when and where to choose friction.

My biz partner @brwnjst saw it in me before I saw it in myself. I always have been entrepreneurial and worked with smaller teams. But only when I partnered with a true visionary did I see how complimentary my skill set was with my energy and value directed at building infrastructure and systems.

Finding the perfect career is overrated.

For much of human history, there were two jobs: hunter and gatherer.

If the work allows you to be present for your family when they need you, is intellectually stimulating, it gives you the balance to pursue your other interests, and you’re well compensated for it; that’s a pretty stellar job.

What are you going to do in retirement?

People make the mistake of thinking it needs to be one big thing.

A better way to think about it is "What 6-10 rhythms or activities can I incorporate in my life to enhance it?"

The best lists include:

Things you’ve already done that you want to do more of (mastry)

Things you've never done that you've always wanted to try (trying new things)

Things you've never done and have always rationalized away seriously considering (bucket list)

Things you lament not doing in your working years (minimizing regret)

These lists also put way less pressure on the one thing to check all your needs in retirement.

Surefire way to fail with “finding a niche”.

Find a demographic you think you’re interested in working with and start making content.

Your prospective niche knows what you need better than you do. So, interview them, listen, ask questions, THEN build to solve their stated pain points.

@SMB_Attorney@BrentBeshore Brents quote is one my favorite biz quotes.

Biz ownership isn't about starting when you've figured out. It's about starting with no certanty and continually seeing past the mess of your business to the addressable market that desparatlley needs what your building.

@KyleSMoore I feel like this legislation is always in a vacuum.

We have X billionaires. If we tax Y it will raise Z in revenue.

But there is always someone on the other side of that rule that can change their behaviors.