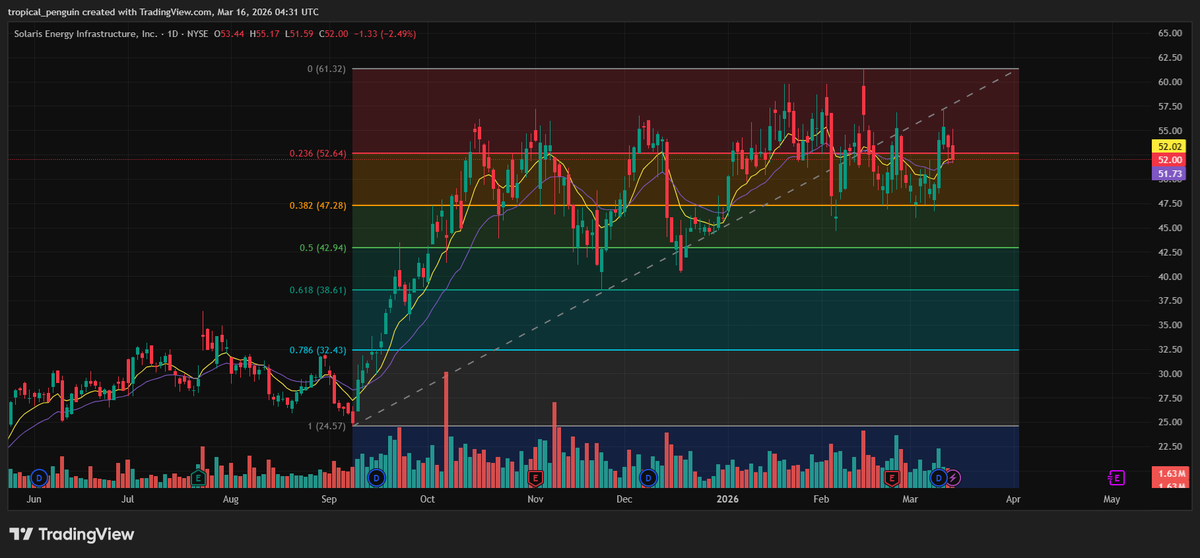

I've been long $SEI since March. Sold at the top and entered the trade again last week. Solaris provides behind-the-meter gas turbines power generation for both xAI's Colossus I and II. Keep this in mind with SPCX IPO tomorrow.

Solaris Energy $SEI has acted extremely well in this chop. This oil & gas company based on Texas is quickly turning into a power-as-a-service (PaaS) company in response to insatiable power demand in the US. When you think of Solaris, think about Uber, but for electricity.

From an operational standpoint, what differentiates Solaris in this space is their HVMVLV acquisition. Solaris is more than a raw source of power, they also have electrical control/distribution expertise. They are able to support complex 1+ GW loads with their modular turbines, reciprocating engines, BESS, and redundancy. They have a real competitive edge in rapid deployment and AI load matching versus alternatives.

Management's execution has been flawless, and the acquistion of HVMVLV opens up their TAM to other areas other than DCs. Current fleet at 760MW with a clear plan to deploy 2.2GW by 2028.

In their last quarter, Solaris has met and exceeded expectations. Full-year 2025 revenue rose to $622 million from $313 million in 2024 while adjusted EBITDA increased to $244 million from $103 million. Management also guided to $72–77 million of adjusted EBITDA for Q1 2026 and $76–84 million for Q2 2026, which suggests the growth trend is continuing. On a GAAP basis, the company was also profitable for full-year 2025, with $58.4 million of net income versus $28.9 million in 2024. The only thing that looks ugly at first glance is Q4 GAAP net income, which was negative $3.5 million, but that was distorted by a $41.5 million loss on extinguishment of debt tied to refinancing after the convertible issuance, not by an operating collapse.

There is a lot more to say about Solaris. I really enjoyed their last earnings and their mantra "from molecule to electron". They are transitioning fast from an Oil & Gas equipment company to a power solutions provider in perhaps the hottest theme in 2026. Companies are scrambling to contract power for hyperscalers, SEI is primed to be a huge beneficiary with their PaaS business and strong know-how and execution for quick power deployment.

I own shares, please do your own research.

The organic EBITDA growth from their power division will sit on top of a very strong growth foundation. Last quarter, FTAI sales was 64% vs Q1 2025. Margins took a hit, but that's because management has decided to pursue market share.

They have a profitable, growing main business and then FTAI Power should add tremendous upside moving forward. This is a real, profitable business, with strong execution. Perhaps not the sexiest name, or the next 4x, but the R/R is pretty strong IMO. Especially in this environment.

Here is my FTAI article, free on substack: https://t.co/HioB87ELOA

Please consider subscribing to my substack and support my work.

I want to reiterate how cheap FTAI is right now. PEG of 0.38, fwd P/E of 20. The best part? None of those multiples are factoring in their FTAI Power segment which should kick into full gear as early as Q1 2027. People keep complaining that stocks are overextended. There are still opportunities out there. FTAI is undoubtedly one of them. Stock is up 18.7% YTD. CEO bought shares at $155 in November (~50% since then). FTAI has largely not participated in the most recent rally. Probably due to higher oil prices. Guess what? Higher oil prices is a net benefit for FTAI as airlines look to cut costs by outsourcing the servicing and maintenance of their jet engines to FTAI.

Management said that prototyping and testing is ahead schedule for their first power turbine (Mod-1) . Management estimates that they will wrap things up by Q3, with commercial launch in Q4. This segment alone should add between 40-50% in EBITDA by 2027. They also revealed that their 2027 stock (100 units) are nearly sold out, with a meaningful portion of the 2028 stocks already spoken for.

@bubbleboi I suppose. The underlying theme is not compute, but power (and heat). EMIB-T is superior to CoWoS on those two vectors as well, we just need to get the execution going (I am on INTC as well)

@CapstackCapital This is a great company and is def a buy soon. I track them for a couple months now. Look at the insider buys. They are basically flashing the bat signal with a buy watermark on top of it.

@James1484553511@fundmyfund I don't know but the 43 support is now resistance. We may need some time here to fix the chart but the call was bullish, stock is attractive again for sure

@bubbleboi Not sure if you addressed this before but isn't CoWoS-L a decent approximation to EMIB-T because it also uses local silicon interconnects for dense die-to-die communication?

PS. This is my first post of my "Edge AI Trade Series." I will write a detailed post about companies that I believe are poised to benefit materially as Edge AI gets traction over the years. Hope you enjoy!

*NEW* Substack Post is OUT. Open to everyone.

My article is about a stock that I've been following since mid May. The company is Duos Technolgies ($DUOT). I believe this company has what it takes to execute in their vision of bringing Edge Data Centres (EDC) to regional and underserved locations.

I hope you enjoy. Support my work via substack, it helps me to keep going with more research on a regular basis.

Link follows...

*NEW* Substack Post is OUT. Open to everyone.

My article is about a stock that I've been following since mid May. The company is Duos Technolgies ($DUOT). I believe this company has what it takes to execute in their vision of bringing Edge Data Centres (EDC) to regional and underserved locations.

I hope you enjoy. Support my work via substack, it helps me to keep going with more research on a regular basis.

Link follows...

@fundmyfund I actually jyst finished AMSC earnings call. Very bullish and this dip may be a gift. LT hold if this bull market holds up for an extra year or two

@fundmyfund A big account here on FinX (very big) has a discord a large trading discord community. He can move small to mid cap stocks very substantially when he opens/closes his position. He closed AMSC on Fri and alerted the server.

@fundmyfund One of the big discord servers dropped AMSC from their port, which caused a bigger than expected drop IMO. I was surprised to see it losing support around the $43.