$FFH I was asked how I got to calculated my $200 per share run rate on Fairfax. Here are my assumptions: $1.6 billion in underwriting profit based upon $26.7 billion in net written premiums at 94% combined.

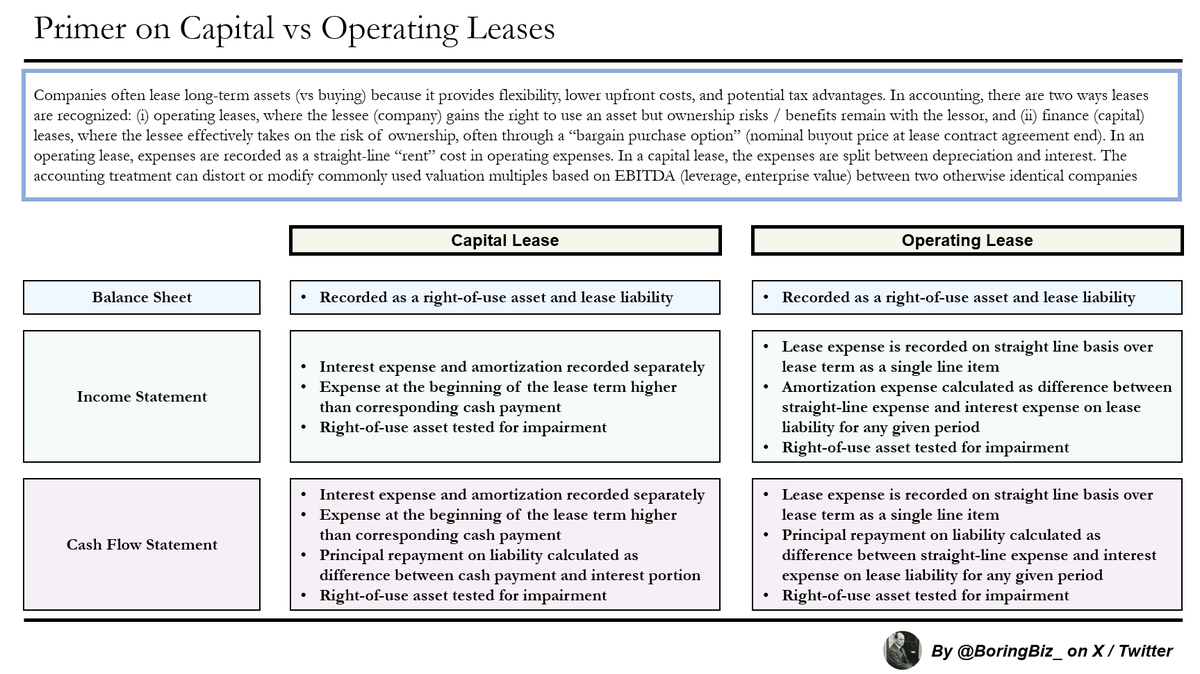

Leases are one of the most misunderstood line items on the accounting statements

Here is my quick primer on financing vs operating leases, and how they are treated on the financial statements

This whole framing is asking the wrong question.

In a world where automation, AI, and geopolitical shocks are rewriting the labor map in real time, “safest path” doesn’t exist in the way it used to.

The old upper-middle-class conveyor belts (law, medicine, engineering) are no longer guaranteed fortresses - they’re slowly being eroded by technology, outsourcing, and collapsing institutional trust.

The only real security is in cultivating meta-skills that can’t be commoditized: adaptive thinking, systems analysis, persuasion, capital allocation, and building networks that transcend job markets.

Majors can be a vector for those skills - economics, applied math, maybe even philosophy with a heavy dose of statistics but the degree itself is becoming a weaker moat.

If I had to give an answer to a 17-year-old today, it would be this: pick a field that gives you deep quantitative fluency and narrative control, then pair it with early exposure to real-world capital flows.

Because the next upper-middle class won’t be defined by job titles - it’ll be defined by who can navigate chaos while everyone else is still waiting for the syllabus.

@Scott_K_Rodgers Thanks. They've been a bit elusive in their public disclosures about this. I was guessing between 8-10% like utilities. I'm surprised their other margins are so low, given that bird construction is aiming for 7%.

@sockfeetrsrch I suspect their purpose was to create confusion. I agree their report was very weak. To my calculations, brackish water sales are $0.30/bbl, sand sales $3-8/ton, easements $35k/pipeline miles and $40/bbl o&g

@sockfeetrsrch The easement revenues are not directly proportional to produced water volume but rather the pipeline miles, roads& utility lines in place. If you disaggregate this with surface royalties, the royalty is $0.13-14/bbl of produced water. This value is > tpl bc of skim oil royalties

Electric run drilling rigs, gas compression stations and well pumps consume A LOT of power. Just imagine what happens if they have a blackout? Electric everything sounds good just keep those backup generators on hand.

The Permian is actually making 21 million barrels of water per day now. To put that into volume context…that is volumetrically equivalent to 20% of the oil the entire world consumes each day being pulled from shale and pushed into sand layers already full of hundreds of thousands of old wells = insanity. #EFT #OOTT

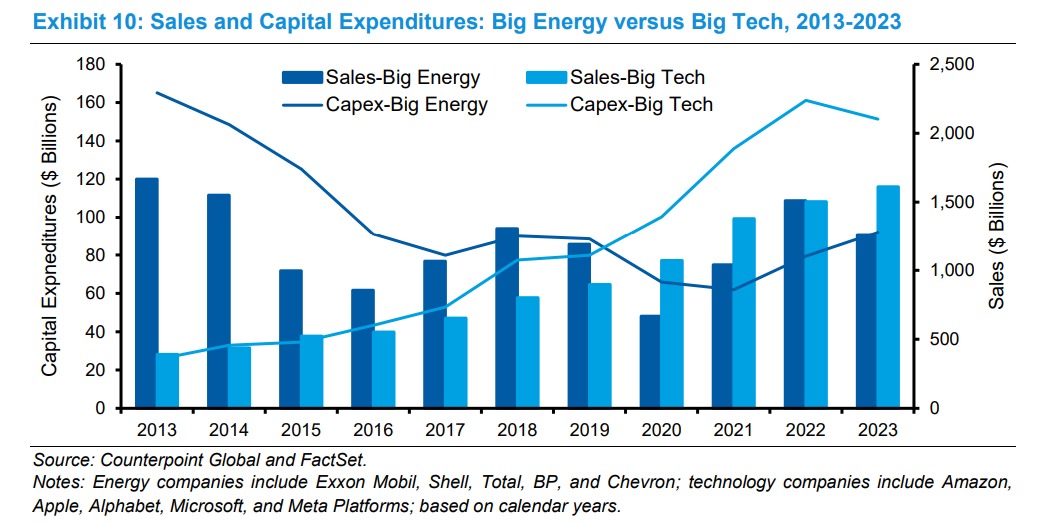

"Capital expenditures for the energy companies were 6.5 times those of the technology companies in 2013. By 2019, the capital expenditures were at rough parity, and in 2022 the technology companies spent twice as much as the energy companies. In a decade, the ratio of energy versus technology capital expenditures went from 6.5 to 1 to 0.6 to 1"

@kab604 Nor do they have to invest in new EV plants (Ford) or develop a bev platform (Toyota). Hopefully their 30b capex over the past 3 years was well spent. They just have to build average vehicles at non premium prices so that they can take advantage of all that operating leverage

@kab604 Hopefully they correct these marketing mistakes with better leadership. The question that I toil with is will their 4 multi energy platform and global flex manufacturing truly cost effective? They seemed positioned correctly given that they don't have to build more plants (byd)