When most humanoid makers are private, you know we're early to robotics/physical AI.

(Figure AI, Apptronik, 1X, Sanctuary, Unitree, etc.)

Also helps when...

> Software bottleneck broke (Nvidia GR00T, RT-2, OpenVLA gave robots general-purpose intelligence)

> Economic crossover just started (humanoid lease costs are below human labor costs)

Our public exposure barely exists...

$VPG - Sensors, like precision strain gauges and foil resistors.

$CCXI / $AGLT - Agility Robotics going public at $2.5B valuation.

$OUST - LiDAR sensors for autonomous systems.

$AMBA - Vision/AI chips for edge devices.

Certainly biased because I have a position, but IMO $VPG is more asymmetric than other U.S-listed tickers.

They're already profitable, already supplying humanoid makers, positioned to scale on multiple fronts, and it's still under ~$2B MC.

Good hedge against getting replaced by AI/robots is to invest in them?

How to create billions of dollars from air (space) $SPCX

Step 1:

Buy Twitter for $44B (Oct 2022), fire most staff, lose most ad revenue.

Step 2:

AI startup xAI “acquires" X for $125B - $1B cash generated, zero value created. (Mar 2025)

Step 3:

SpaceX "acquires" xAI at $250B -$1.25T combined valuation.

Nice 100% return in a year. (Feb 2026)

Step 4: List SpaceX at $1.75T, 4% float, get index inclusion rules changed, shorten lock-ups, let leveraged ETFs squeeze it higher. Increase valuation $500B in 4 months. (June 2026)

X stake now up 180%.

Financial engineering masterclass.

Step 5: Combine with Tesla.

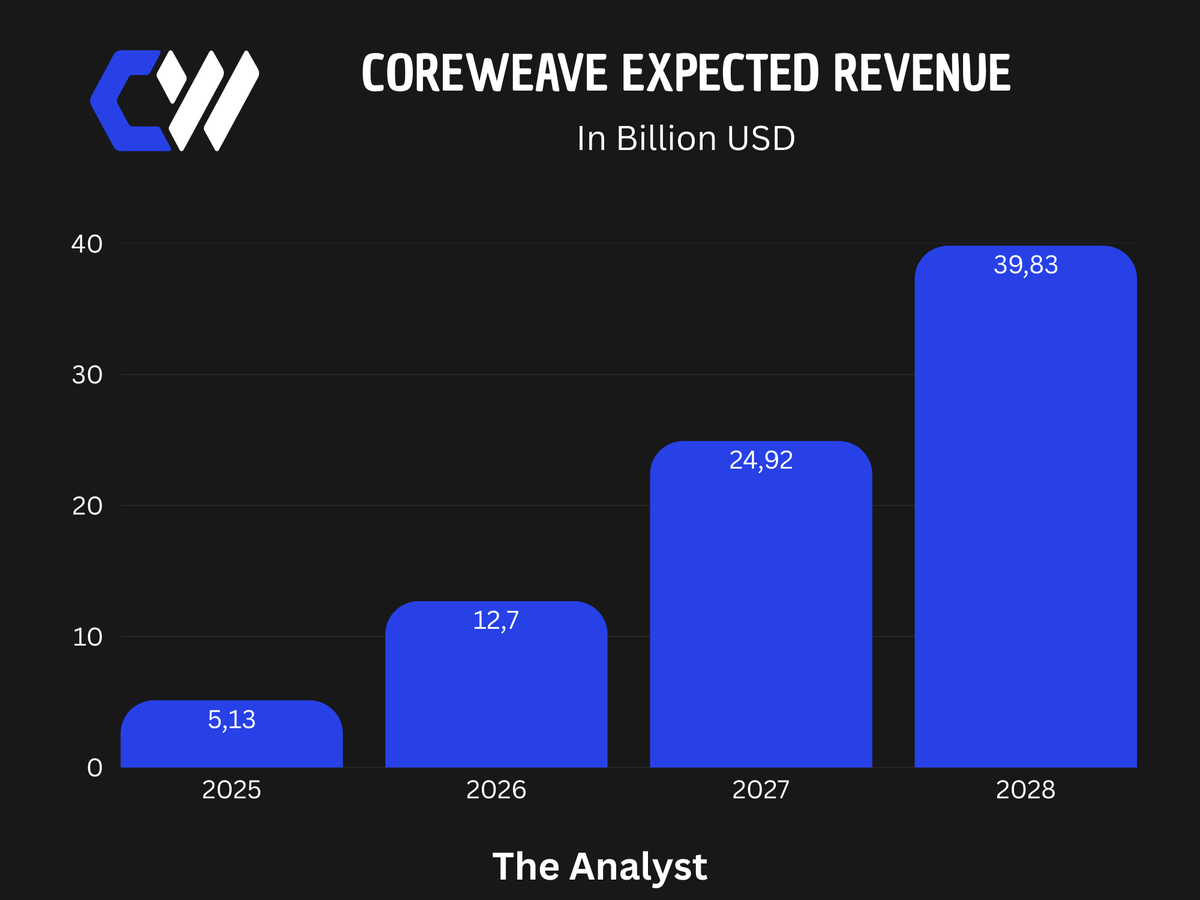

$CRWV is the most interesting stock to watch right now.

The Revenue-ramp is looking absolutely insane:

2027 Revenue will be around $25B

Meanwhile the company is only valued at $53B right now.

The valuation gap is absolutely insane when compared to $NBIS.

There is just no reason for it to have a lower MC.

- Trading at less than half the Fwd EV/EBITDA

- Will do 2.5x more revenue in 2027

This will go down as a generational entry.

You NEED to listen to me right now.

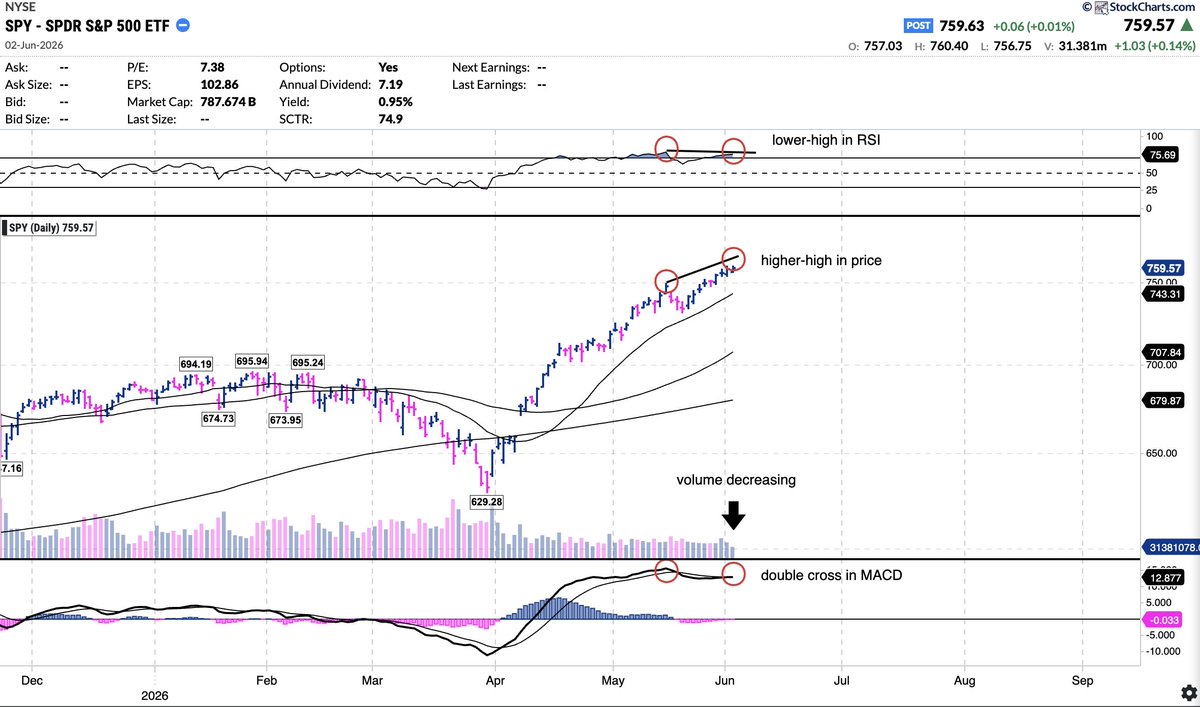

We are in LATE-cycle territory for the overall markets / $SPY.

Bearish divergences are forming with EACH new marginal high.

VOLUME is drying up, candles are getting smaller. This is HESITATION from the bulls.

Momentum is starting to FADE.

Markets will STILL keep going up long-term, but SHORT-TERM, we're in the 8th - 9th inning.

I expect a 5% HEALTHY pull-back.

What should you do?!

1. Keep your AI-winners!!!! Trim 20% to lock-in GAINS, never sell fully. They are WINNERS for a reason

2. Look for CONTRARIAN buys. The stocks that have been LAGGING. They will go down LESS, or even outperform.

3. BALANCE your portfolio with AI leaders + AI laggards + defensives!!!!

All you need to do is SURVIVE, and you will be rewarded with the BIGGEST bull-run in history over the next 5 years.

- Keep companies and consider trimming 20% like $ARM, $NBIS, $MRVL, $MU, etc.

- Slowly positions in companies like $CRWV, etc.

- Build positions in lagging companies like $NOW, $NKE, etc.

- Build defensives like $WMT, etc.

Get ready to buy amazing companies like $AMZN, $GOOGL, and many many others soon.

- $AAOI at $12B

- $SIVE at $2B

- Foci at $2.8B

- Shunsin at $2B

Usually the best risk/reward to me currently. Lot of my answers before like $AXTI already 10x’d, so different lineup this time.

$AAOI due to absurd H1 2027 revenue projections from capacity ramp, doing everything from laser fab to assembly in America.

$471M/month… that’s in 2027, the TAM increases exponentially in 2028.

$SIVE is also ramping absurdly high, 77% revenue pipeline growth of the entire company’s history to ~$799M

Primarily from photonics… in a single quarter. And they’re projecting 60% gross margins off that.

Foci - $NVDA / $TSM primarily FAU supplier and bottleneck for COUPE. Genuinely not sure how this is $2.8B.

BOM share for their passive components + FAU are massive in 2028. Just a bit early H1 2026.

Shunsin - Legit you see Foxconn get CPO/photonics related orders over and over for $NVDA and others.

Just nobody knows the packaging/testing gets done by Shunsin.

A lot of contracts are also under Shunsin’s subsidiary too.. so markets/algorithms don’t know what’s coming imo.

Runner up is $XFAB, they’ll probably be central to EU CHIPS act 2 for silicon photonics at ~$1.5B MC.

And of course SiC/GaN foundries should go brr with 800vdc push by Nvidia.

Especially if they’re the only high volume one in United States per Dpt. Of Commerce.

And it’s such a low price/book ratio so you’re kinda getting the company upside for free, while US Gov/EU Gov subsidize their capex.

2 years ago, I called out $ASTS at $2. Its up 6500% so far at $130.

My target at least $200+ when $SPCX IPOs.

Right now, $ORCL is the most obvious play. Its earnings is on June 10 then $MU on June 24.

This year, I explained these would 10x-20x:

$INTC — $AAPL chip deal + foundry turnaround tripled the stock in months (Trump)

$DELL — Pentagon contract + AI server orders created a multi-catalyst monster (Trump)

$MU — HBM memory sold out through 2026, AI supercycle just getting started (Trump)

$NOW — Enterprise AI agents replacing entire IT workflows, 22% revenue growth accelerating (Trump)

$PLTR — Government + commercial AI contracts exploding, revenue up 56% in 2025 (Trump call)

$TE — nuclear power is the only answer to AI's insatiable electricity demand (Leopold call)

♻️ RESHARE this post and write 1 comment, I'll DM you my exact 1000% play for $ORCL