@studley21ep@EO_Farmer@SoFi Alec, the math is simple. I earn an extra 1.4% on the 20k in my savings act (4.5% vs 3.1% normally). That’s a no-brainer as it’s worth $280 per year. So the $120 I give them makes absolute sense. As a kicker, I also earn 10% extra on my SoFi credit card. The logic is very clear.

$sofi and other fintech down 9-10% because jobs grew 100,000 more than forecasted and much of that had to do with local government increases? Lol. Ok…..

$NFLX down 8 strait. Last time that happened was Nov, 2022. From Gemini:

“After snapping that eight-day losing streak on November 7, 2022, Netflix stock went on a massive, multi-year bull run, ultimately skyrocketing by more than 400% to hit an all-time high in mid-2025.”

$SOFI just launched SoFiUSD to members, built on $ETH and $SOL. The press release below has more details and plans for the product over the coming weeks.

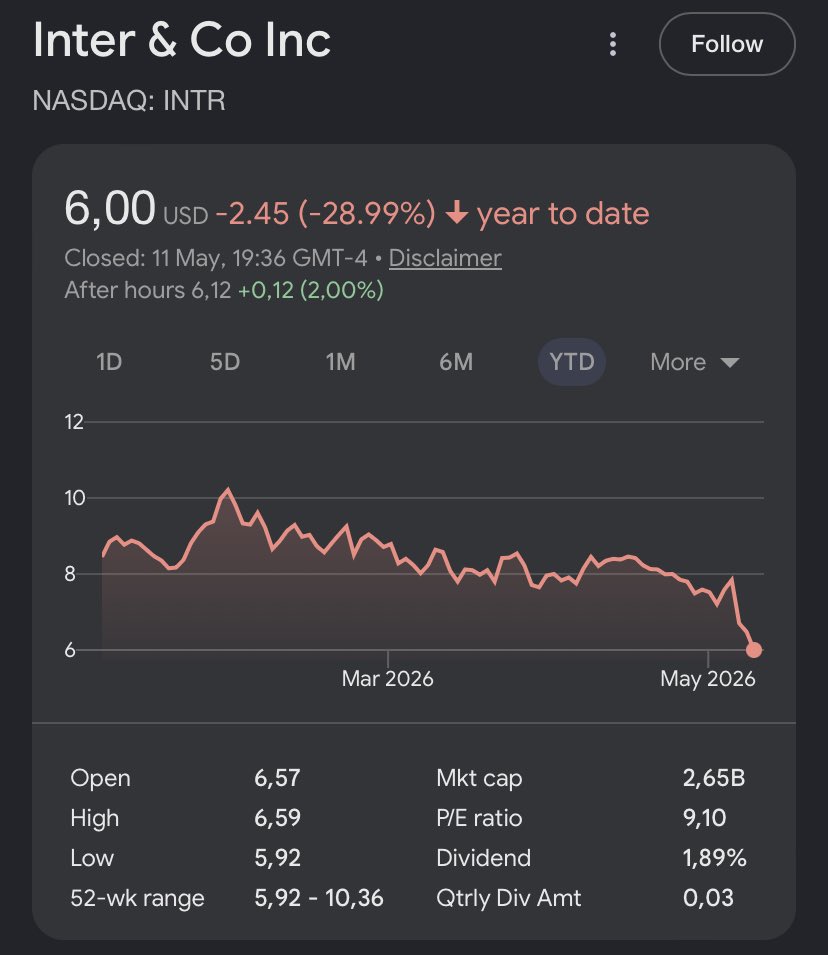

$SOFID

Yesterday $sofi rallied hard at open and then gave it all back. Today, dropped like a rock. So a mirror of yesterday would mean we rally! lol, I’m kidding of course!

We are likely getting the biggest opportunity in fintech in years.

What’s happening with $SOFI, $KLAR, $INTR, and even $MELI are all the same.

They are growing interest bearing products where they front-load expected losses but recognize revenue gradually over time.

$SOFI lending accelerated because they wanted to make up for the slowing technology platform business; $INTR did the same with private payroll loans to accelerate growth; $KLAR did it to offer longer term loans to compete with $AFRM; $MELI is doing it to expand market share across LatAm.

What happened in all of them is the same:

- Higher lending increased loss provisions.

- Margins declined temporarily.

- Delinquincies increased as they are experimenting with broader borrower profiles.

Result? Heavy algorithmic selling compounded by stop losses as the stocks declined.

This is exactly what is creating the opportunity.

People don’t understand that these businesses should push their limits to see exactly where their models start to break. Up until that point, they are leaving money on the table.

To see this, they have to grow loan portfolios. They are doing this gradually to minimize risk.

They are taking risk and they may even incur additional losses because of this but this is something necessary for the long term growth of these businesses.

They all are strong enough to make these experiments and step back with no damage to the business if things don’t go well.

The market doesn’t want to get to this level of understanding, creating opportunities for those who are willing to see a bit deeper and have patience.

A few years from now, people will look back and be surprised to see they could buy a fast growing neo-bank like $INTR at 9x earnings.

Apparently Truist Securitulies knows more about $sofi business than @anthonynoto. I’ll go with the CEO buying shares four times in the last couple months…..