NVIDIA CEO Jensen Huang said the “ChatGPT moment for general robotics” is coming.

The biggest winners may not be the robot makers.

They may be the companies building what’s inside the robot.

Robotics ecosystem:

• AI Brains → $NVDA $QCOM

• Sensors & Perception → $OUST $CGNX $ALGM $VPG

• Edge AI Inference → $AMBA $CEVA $LSCC

• Motors & Motion → $NJDCY $RBC $RRX $AME

• Precision Joints → 6324.T 6481.T $ALNT

• Power Electronics → $NVTS $TXN $WOLF $RNECY $IFNNY $STM $MPWR $ON

• Energy & Rare Earths → $ENS $MP $USAR $LYSCF $UUUU

If you’re interested in Physical AI and robotics, I shared my top 5 robotics stocks and a deeper dive here:

https://t.co/2QLIbzo8Zi

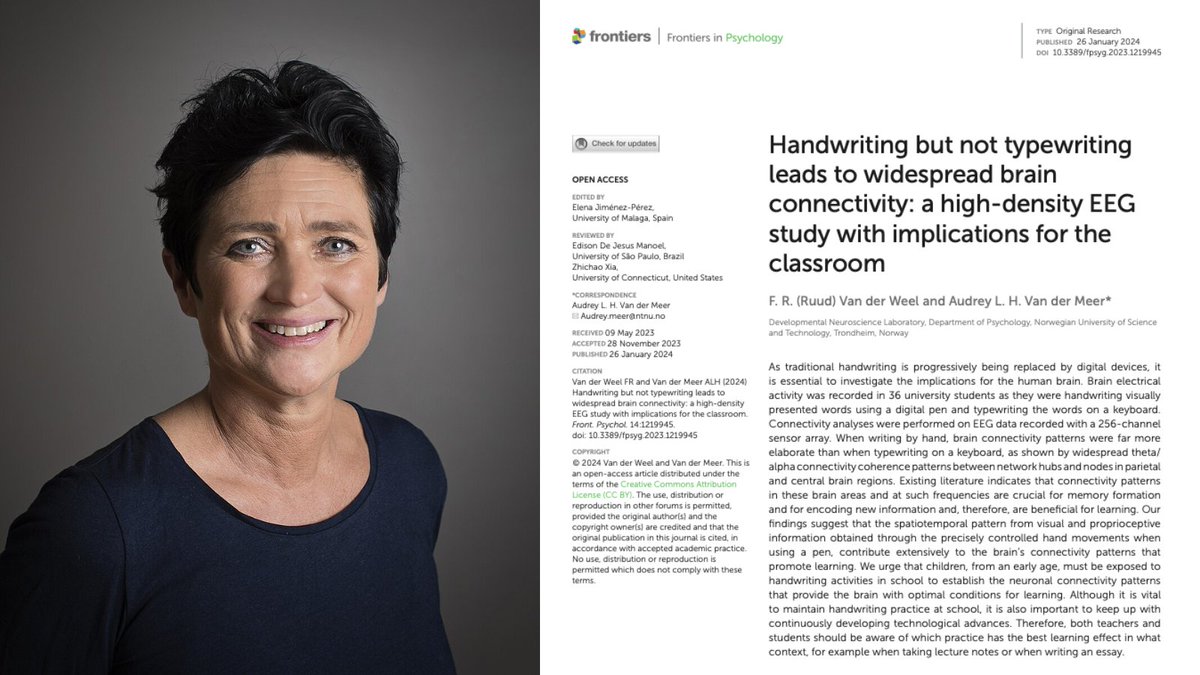

A Norwegian neuroscientist spent 20 years proving that the act of writing by hand changes the human brain in ways typing physically cannot, and almost nobody outside her field has read the paper.

Her name is Audrey van der Meer.

She runs a brain research lab in Trondheim, and the paper that closed the argument was published in 2024 in a journal called Frontiers in Psychology. The finding is brutal enough that it should have changed every classroom on Earth.

The experiment was simple. She recruited 36 university students and put each one in a cap with 256 sensors pressed against their scalp to record brain activity. Words flashed on a screen one at a time.

Sometimes the students wrote the word by hand on a touchscreen using a digital pen, and sometimes they typed the same word on a keyboard. Every neural response was recorded for the full five seconds the word stayed on screen.

Then her team looked at the part of the data most researchers had ignored for years, which is how different parts of the brain were communicating with each other during the task.

When the students wrote by hand, the brain lit up everywhere at once.

The regions responsible for memory, sensory integration, and the encoding of new information were all firing together in a coordinated pattern that spread across the entire cortex. The whole network was awake and connected.

When the same students typed the same word, that pattern collapsed almost completely.

Most of the brain went quiet, and the connections between regions that had been alive seconds earlier were nowhere to be found on the EEG.

Same word, same brain, same person, and two completely different neurological events.

The reason turned out to be something nobody had really paid attention to before her work. Writing by hand is not one motion but a sequence of thousands of tiny micro-movements coordinated with your eyes in real time, where each letter is a different shape that requires the brain to solve a slightly different spatial problem.

Your fingers, wrist, vision, and the parts of your brain that track position in space are all working together to produce one letter, then the next, then the next.

Typing throws all of that away. Every key on a keyboard requires the exact same finger motion regardless of which letter you are pressing, which means the brain has almost nothing to integrate and almost no problem to solve.

Van der Meer said it plainly in her interviews.

Pressing the same key with the same finger over and over does not stimulate the brain in any meaningful way, and she pointed out something that should scare every parent who handed their kid an iPad.

Children who learn to read and write on tablets often cannot tell letters like b and d apart, because they have never physically felt with their bodies what it takes to actually produce those letters on a page.

A decade before her, two researchers at Princeton ran the same fight using a completely different method and ended up at the same answer. Pam Mueller and Daniel Oppenheimer tested 327 students across three experiments, where half took notes on laptops with the internet disabled and half took notes by hand, before testing everyone on what they actually understood from the lectures they had watched.

The handwriting group won by a wide margin on every question that required real understanding rather than surface recall.

The reason was hiding in the transcripts of what the two groups had actually written down.

The laptop students typed almost word for word, capturing more total content but processing almost none of it as they went, while the handwriting students physically could not write fast enough to transcribe a lecture in real time, which forced them to listen carefully, decide what actually mattered, and put it in their own words on the page.

That single act of choosing what to keep was the learning itself, and the keyboard had quietly skipped the choosing and skipped the learning along with it.

Two studies. Two countries. Same answer.

Handwriting makes the brain work. Typing lets it coast.

Every note you have ever typed instead of written went into your brain through a thinner pipe. Every meeting, every book highlight, every idea you captured on your phone instead of on paper was processed at half depth.

You did not forget those things because your memory is bad. You forgot them because typing never woke the part of the brain that would have made them stick.

The fix is the thing your grandmother already knew.

Pick up a pen. Write the thing down. The slower road is the faster one.

🚨 LEOPOLD ASCHENBRENNER IS OFFICIALLY BETTING BILLIONS THAT THE AI HARDWARE BOOM HAS PEAKED.

The exOpenAI researcher who was fired for warning that China could steal their AI models then turned $225 million into $5.5 billion in 12 months just filed his Q1 2026 13F with the SEC.

One quarter ago he had $5.5 billion in disclosed equity exposure. As of March 31, 2026 that number is $13.67 billion. The portfolio nearly tripled in a single quarter across 42 positions.

He initiated $7.46 billion in put options against every major semiconductor company between January 1 and March 31, 2026.

None of these positions existed in his Q4 2025 filing.

- SMH VanEck Semiconductor ETF PUT: $2.04 billion

- Nvidia PUT: $1.57 billion

- Oracle PUT: $1.07 billion

- Broadcom PUT: $1.01 billion

- AMD PUT: $969 million

- Micron PUT: $583 million

- Taiwan Semiconductor PUT: $535 million

- ASML PUT: $494 million

- Intel PUT: $159 million

For the past 18 months Aschenbrenner was betting only on electricity, memory, compute, and physical data center infrastructure. That made him one of the best performing fund managers in the world. And his long stock book still reflects that exact same thesis.

- Bloom Energy: $878 million

- SanDisk: $724 million

- CoreWeave: $556 million

- IREN: $401 million

- Core Scientific: $389 million

- Applied Digital: $320 million

- Riot Platforms: $142 million

- CleanSpark: $104 million

- Solaris Energy: $62 million

- T1 Energy: $43 million

- Bitfarms: $38 million

- Bitdeer: $29 million

- Power Solutions: $26 million

- WhiteFiber: $20 million

- Babcock and Wilcox: $19 million

- SharonAI: $18 million

- ProPetro: $13 million

- Hive Digital: $6 million

He is also running call options on specific names at the same time as his puts, which means he is not simply betting against semiconductors everywhere.

- Micron CALL: $422 million

- SanDisk CALL: $388 million

- Taiwan Semiconductor CALL: $354 million

- CoreWeave CALL: $140 million

- Bloom Energy CALL: $55 million

This means he believes the companies supplying power, storage, and compute to the AI industry still have years of growth ahead of them.

But the chip companies that Wall Street has been buying for the past two years at record valuations have already priced in everything good that is going to happen to them.

The man who has been right about every major AI trade for the past 18 months is now betting that the biggest names in semiconductors are about to fall.

If his track record means anything, the chip stocks Wall Street has been buying for the past two years may be in serious trouble.

Yesterday @coinbase experienced a multi-hour service disruption affecting trading, exchange access, and balance updates. Here's our initial read from Coinbase engineering on what happened, how we recovered, and what we're addressing.

At approximately 23:50 UTC on 2026-05-07, our monitoring detected cascading quote failures from internal services that triggered multiple Sev1 incidents that engineering immediately began investigating. Customer-facing impacts included spot trading, Prime, International and derivative exchanges.

Root cause: a thermal event (cooling system failure) inside a subset of racks within a single building in AWS us-east-1. We run a primary replica of our exchange infrastructure in a single zone, consistent with industry standards to reduce latency. To prepare for failures like this, we maintain a distributed standby, but during this incident, failures in the primary zone that were designed to be isolated were not, extending the duration of our outage.

The failure cascaded down two paths:

1. Multiple hardware components beneath our exchange’s matching engine failed, requiring recovery and failover

2. Distributed Kafka clusters that manage messaging across Coinbase systems failed to remain available, also requiring partition failovers to new hardware brokers with many TiBs of data

After isolating the incident: automated tooling drained ~10 Kubernetes clusters worth of related workloads out of the affected zone to stabilize internal services. Most services were back to normal within ~30 minutes of diagnosis. The two things we couldn't automatically drain: the exchange (dedicated hardware and storage) and Kafka (managed service that was designed to be resilient to this, with unique problems).

The exchange matching engine is the core system responsible for processing orders and maintaining order books. It is a distributed cluster and requires quorum to safely elect a leader and continue processing trading activity. During the incident, infrastructure-level constraints in the affected datacenter left only a subset of nodes healthy, preventing the cluster from reaching quorum. As a result, trading across Retail, Advanced, and Institutional exchanges were blocked.

Recovery required our oncall and engineering teams to execute our disaster recovery plan, restore quorum safely, and validate system health under constrained infrastructure conditions. The team built, tested, deployed, and validated the fix while continuing to manage the broader incident.

Kafka recovery was a much larger scale operation. Our primary managed Kafka partitions process many terabytes of data daily and are designed with resiliency guarantees for uninterrupted operation during a datacenter failure just like this. In this case, those guarantees failed and required manual recovery.

We again relied on disaster recovery procedures to recover stuck partitions onto new hardware (brokers) that enabled us to safely bring x-service messaging back online across Coinbase. During the lag, customers saw delayed balance streams which resolved automatically once replication caught up. No data lost.

Once the engine came back up as part of our standard runbooks, we re-opened markets carefully: all products to cancel-only mode first, audited product states, then moved all markets to auction mode, before restoring trading on Coinbase Exchange.

What went right: the team. Incident response across the company came together within minutes, followed well-rehearsed playbooks and used secure automation tooling to recover all services. We have a strong, senior team at Coinbase that worked through rare failure modes to recover all services.

To our customers: losing access to your account, even temporarily, is unacceptable. We know that. We're sorry, and we’ll publish a full root cause analysis in the coming weeks 🙏

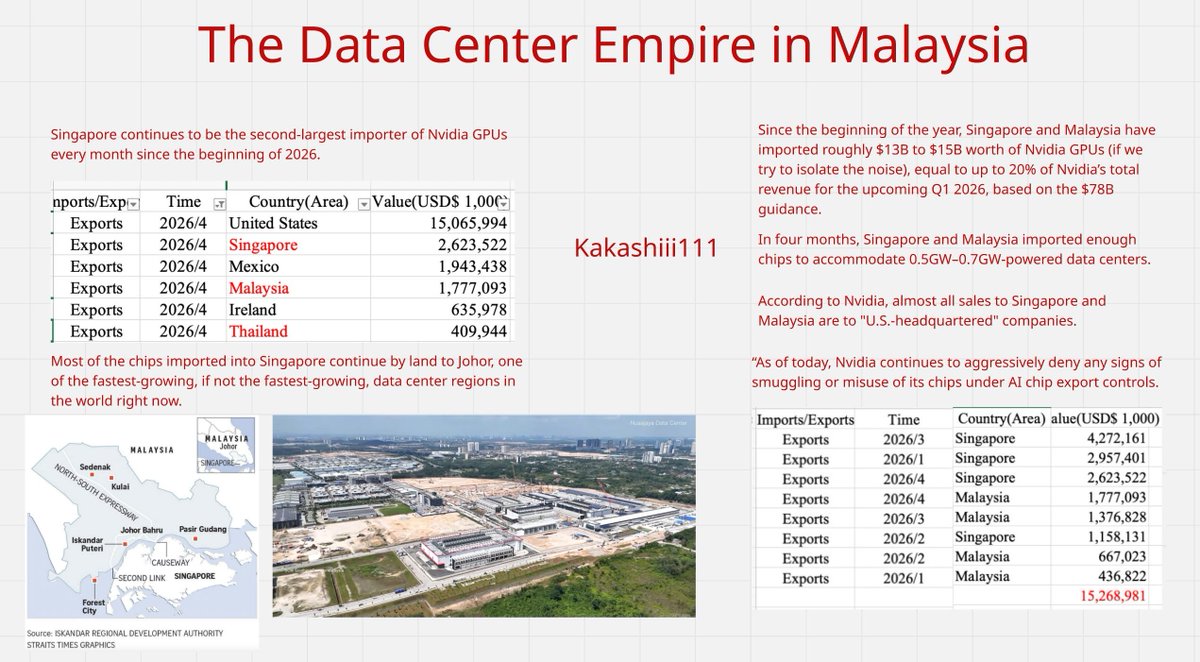

The Data Center Empire in Malaysia

1. Singapore continues to be the second-largest importer of Nvidia GPUs every month since the beginning of 2026. In April alone, Singapore imported over $2B worth of chips.”

2. Since the beginning of the year, Singapore and Malaysia have imported roughly $13B to $15B worth of Nvidia GPUs (if we try to isolate the noise), equal to up to 20% of Nvidia’s total revenue for the upcoming Q1 2026, based on the $78B guidance.

3. Most of the chips imported into Singapore continue by land to Johor, one of the fastest-growing, if not the fastest-growing, data center regions in the world right now.

4. In four months, Singapore and Malaysia imported enough chips to accommodate 0.5GW–0.7GW-powered data centers.

5. According to Nvidia, almost all sales to Singapore and Malaysia are to “U.S.-headquartered” companies.

6. As of today, Nvidia continues to aggressively deny any signs of smuggling or misuse of its chips under AI chip export controls.

Interactive Brokers just allowed trading on Korean stocks for the first time in history. Korean stocks are dirt cheap, bombed out and completely undervalued and overlooked. I am going to find the best ones and invest in them. Follow along if you want cheap Korean stocks.

$SIVE – If you are wondering if it is too late to invest, it isn’t and here is why.

Goldman Sachs just unveiled their Optical Communications industry map for the AI infrastructure buildout. The full ecosystem laid out – IC Design, Materials, Optical Components, Packaging and Testing.

Guess what? $SIVE is not on the map, yet.

The highlights from Goldman:

TAM growing from $15B to $154B. Scale-up optical interconnects within racks and super-nodes are the real driver. NVIDIA’s GPU clusters jumping from 72 to 576 GPUs by 2027-2028, with interconnect dollar value per computing unit going from $315K to $9.4B. A 29x increase per unit.

Silicon photonics penetration jumping from 6% in Q1 2024 to 46% by Q4 2028. CPO commercialization starting in 2026. The shift from copper to optical is structural and accelerating.

In the laser/light source segment, Goldman maps $LITE, $COHR, $AVGO, $AAOI – the obvious ones. Sivers is nowhere to be seen.

$SIVE powers Jabil’s 1.6T LRO architecture. Win Semi is their confirmed foundry partner. They sit upstream of the entire optical interconnect stack with InP lasers everyone needs.

When Goldman publishes the next iteration of this map, $SIVE will most likely be listed on the US Nasdaq and big enough for institutional coverage. Which means institutions will try to shake the ground just so they can catch up.

This report is extremely bullish for the entire photonics ecosystem.

Being early pays. Having conviction pays even more.

Every time I post about this company on X, the replies come fast and they come ugly. “Boomer brand.” “Going to zero.” “Who even uses these products anymore?” I have been called an idiot more times on this one name than any other idea I have shared publicly in the last two years.

I love it.

There is a principle that has guided value investors since Benjamin Graham first wrote it down: the market is not always right, and the times it is most wrong are precisely the times when everyone agrees on the narrative. When a stock has nearly 14% of its float sold short, when the comment section fills with contempt, when the sell-side has a consensus “Hold” and the price is near a multi-year low, that is not evidence the thesis is wrong. That is evidence that expectations have been reset to a level where almost any improvement becomes a positive surprise.

Here is what I will tell you in the free section, and it is already more than most people following this story have bothered to figure out.

This company is being valued by almost everyone, including the sell-side analysts who cover it daily, using a completely wrong enterprise value. Not slightly off. Not a rounding error. The number most investors are looking at is roughly five times higher than the real number. The reason is a balance sheet technicality that takes about twenty minutes to work through, and almost nobody has done it. When you do the work and strip out the non-recourse financing subsidiary that has nothing to do with the core operating business, you find a company trading at an enterprise value of roughly one billion dollars on a business that has historically generated hundreds of millions in annual EBITDA and billions in revenue.

You also find something else. A new CEO who just bought stock in the open market with his own money. A board member who did the same. Three hundred and forty-seven million dollars in share buybacks completed in 2025 alone, retiring eleven percent of shares outstanding in a single year. An investor day coming in May that could be the most important single catalyst this company has seen in a decade, specifically because management has signaled the return of the one product that dealers loved, that entry-level riders needed, and that the previous CEO killed for reasons that had more to do with his own preferences than with any rational business logic.

The previous CEO is gone. He was pushed out after a proxy fight. The new man came from a consumer brand background, flew to Milwaukee, sat with dealers, and listened. His first moves were to stop doing the things that were destroying the business and start doing the things that the people actually closest to the product had been begging for.

Meanwhile, there is a pension fund sitting on the balance sheet that is overfunded by nearly half a billion dollars. There are four owned manufacturing facilities plus a corporate headquarters building that would take hundreds of millions of dollars to replace. There is over a billion dollars in net cash at the parent company, completely separate from the financing subsidiary, that most investors do not realize is there because they are reading the consolidated statements without doing the work of separating the pieces.

Nearly 14% of the float is sold short. That is not a warning sign. That is a coiled spring.

I am a member of the Ben Graham school. I do not buy on hope. I buy on math. The math here, when you do it correctly, is among the most compelling I have seen in years on a company of this size, this brand recognition, and this operating history.

The full analysis is below for paid subscribers. It covers the balance sheet deconsolidation in detail, the real enterprise value, the valuation case, every catalyst I can see between now and year-end, and what I think this is worth on a conservative recovery scenario.

When she hears you have exposure to SpaceX ahead of the IPO (it’s a triple-layered SPV that you paid 20% upfront and 30% carried interest without knowing who ultimately owns the shares)

Google just released a warning for cryptocurrency that the number of qubits required to break ECDSA is 20x less than previously thought.

They have proof.

They’re (strongly?) recommending crypto upgrade to post-quantum by 2029 now.

4 years!?

Timelines are accelerating rapidly.

SUMMARY OF THE BUSINESS INSIDER INTERVIEW WITH $NBIS CEO ARKADY VOLOZH

Q: What are the key bottlenecks in AI infrastructure right now?

A: Nebius calls them the “four Cs”: capacity, capital, chips, and customers.

On capacity:

“The physical world simply cannot build data centers fast enough.”

The real bottleneck is the supply chain, especially transformers and power equipment. Nebius is targeting more than 3GW of contracted power by 2026.

On capital:

“Capturing just 10% of the AI infrastructure market requires around $400 billion.”

The scale of funding has fundamentally changed.

On chips:

“A year ago, it was GPUs. Now the constraints go deeper into the silicon.”

The bottleneck has shifted toward memory shortages.

On customers:

“Demand vastly outpaces the supply we can build.”

Demand is no longer a question.

Q: Why does Nebius build its own stack instead of leasing or using third parties?

A:

“Think about Nebius as a fourth hyperscaler. You do not achieve that by acting as a hardware wholesaler.”

Nebius builds everything itself, from servers to racks.

“We design our own servers and racks. This allows us to bypass middlemen and capture that margin ourselves.”

“Look at the alternative. Companies lease data center shells, buy pre-assembled racks, and sacrifice margin at every step.”

Q: How does Nebius think about the AI stack and where value is created?

A: Nebius is focused on owning the entire stack.

“We control our cost structure from the concrete up to the software.”

The stack is broken into five layers:

Layer 1: Land, power, physical infrastructure

Layer 2: Compute hardware

“By building our own racks, we save 15% to 20% and deliver more compute per unit of power.”

Layer 3: Bare metal

Layer 4: Multi-tenant cloud

Layer 5: Services and inference (including Token Factory)

“Most companies operate at one or two layers and pay a premium to middlemen. We own the entire stack.”

Q: Does being a new company affect how Nebius builds at scale?

A:

“Nebius is a new company, but our team has decades of experience building infrastructure at hyperscale.”

They handle everything internally.

“We know how to buy the land, get the permits, and contract the power. We do not outsource these problems.”

They also emphasize working directly with local communities to keep projects on track.

Q: What are “dark GPUs” and why do they matter?

A:

“Dark GPUs are idle compute capacity.”

Customers are paying for GPUs they cannot fully utilize due to poor orchestration.

“We built our cloud for AI engineers and manage orchestration so customers always know their exact available capacity.”

Q: How do large deals with companies like Meta and Microsoft fit into the strategy?

A:

“Our core product is our multi-tenant AI cloud.”

These deals are not the core business.

“Large contracts with Meta and Microsoft are fuel.”

“They allow us to build faster, create a foundation for infrastructure, and give us more options to raise capital.”

⭕️I wonder how Iranian monarchists feel about President Trump returning the three islands (Abu Musa, Greater Tunb and Lesser Tunb) to the UAE.

⭕️The three small islands sit right at the entrance to the Strait of Hormuz. The last Shah ordered the Navy to occupy them in 1971.

⭕️The UAE has claimed them ever since, especially since Arab tribes inhabited the Greater Tunb and the others.

⭕️By returning them to the UAE, the US can establish a military base there and control the Hormuz Strait for decades to come.

By publishing this explicitly false story, the @FT has officially become tabloid trash for market participants.

Despite my direct, on-the-record denial of ever having advocated, explored, or espoused the idea that Chancellor-Bank of England statute serving as a prototype for a Treasury-Federal Reserve relationship, FT journalists manufactured a story with the headline, “Scott Bessent praised Bank of England as model for tighter oversight of the Federal Reserve.”

These pathetic journalists have clearly fabricated a story to give the impression that both I and the Trump Administration are setting “about restructuring the relationship… at a time when President Donald Trump has launched an unprecedented assault on the world’s most important central bank.”

Their mendacious assertion is based on vague statements from unnamed “financial industry executives familiar with the matter.”

In short, FT has literally manufactured an entirely fake policy position for me and the Administration. Other than furthering a maliciously false narrative of dysfunction and divisiveness, it baffles the mind as to why they would shred their already diminished journalistic credibility.

Over the past 10 years, I have written more than 20,000 words opining on the Federal Reserve decisions, personnel, structure, and modifications. Nowhere have I ever mentioned this ridiculous notion.

The Governor’s letters to the Chancellor have proven to be a useless and perfunctory device.

There is much to be said about the storied Bank of England, but any recreation of its operating framework on this side of the Atlantic has never been contemplated.

The shameful journalists and editors at the FT are shocking in their meretriciousness, lack of standards, and general intellectual libertinism. It is the worst tradition of Fleet Street to manufacture news rather than report on it.

They have brought irredeemable shame to their parent organization, Nikkei Inc., with whom I had previously held excellent relations.

In 2025, I laid out a comprehensive 6,000+ word review of each and every policy reform that I believe should be adopted by the Federal Reserve.

Read my actual, real thoughts on and proposals for Federal Reserve reform at the International Economy: https://t.co/0yQRXpMnK3

As many others have pointed out, Bitcoin ETF flows have stabilized, but the relatively muted Bitcoin ETF flows since the October peak offer much less explanatory power for Bitcoin returns than the entire period. Suggests ex-ETF sales were a driver.

Positive divergence bounce is still playing out.

I don't think people understand how insane this actually is...

Nasdaq just partnered with Kraken to enable 24/7 trading of tokenized stocks.

The craziest part is it'll run on Kraken - not through traditional brokers like Schwab or TD.

Last week the Fed, FDIC, and OCC confirmed tokenized securities receive the same capital treatment as traditional securities.

Kraken also just gained access to Federal Reserve payment rails, putting a crypto firm inside the same core settlement infrastructure used by major banks.

Think about what that means.

A crypto exchange is now becoming the platform where tokenized equities trade globally, 24/7, 365 days a year.

This is how trillions move on-chain.

We're in the calm before the storm. Mass adoption is coming and Mass rotation of capital is coming with it.

Oracle just told every AI company on earth the same thing.

Your models are worthless.

Not the technology, talent or the billions spent training them.

But the data they were trained on.

Larry Ellison, the man who built Oracle into the backbone of global enterprise just dropped a bombshell.

He said ChatGPT, Gemini, Grok, and Llama, all of them are training on the exact same data.

The entire public internet, every Wikipedia page, Reddit thread and every news article.

That means they're all converging essentially becoming the same product with different logos.

Ellison's word for it is commodities.

But here's where it gets dangerous.

He says the real gold isn't public data, It's private data.

The medical records in hospital systems, the financial data in bank vaults.

The supply chain secrets of every Fortune 500 and guess where most of that data already lives.

Not Google, Amazon or Microsoft but inside Oracle.

Oracle databases hold most of the world's high value private enterprise data.

So Oracle just launched something called AI Database 26ai.

It lets the top AI models, ChatGPT, Gemini, Grok, Llama reason directly over a company's private data, without that data ever leaving the vault.

They're using a technique called RAG, Retrieval Augmented Generation.

The AI doesn't train on your data, it searches it in real time.

Think about what that means.

A bank could ask AI to analyze every loan it's ever made without exposing a single customer record.

A hospital could have AI diagnose patients using its full medical history without violating HIPAA.

A defense contractor could let AI reason across classified operations without data leaving a secure environment.

Ellison is betting this is bigger than the training market. Bigger than the GPU boom.

Bigger than the data center buildout.

He called it the largest and fastest growing market in history.

The numbers back the ambition.

Oracle's remaining performance obligations just hit $523 billion.

That's contracted revenue not yet delivered and $300 billion of it comes from OpenAI alone.

Cloud revenue hit $8 billion in a single quarter, OCI grew 66 percent and GPU revenue surged 177 percent.

But here's the part nobody's talking about.

If private data becomes the real AI moat, then whoever controls the database controls the future of AI.

And that's a level of power that should make everyone uncomfortable.

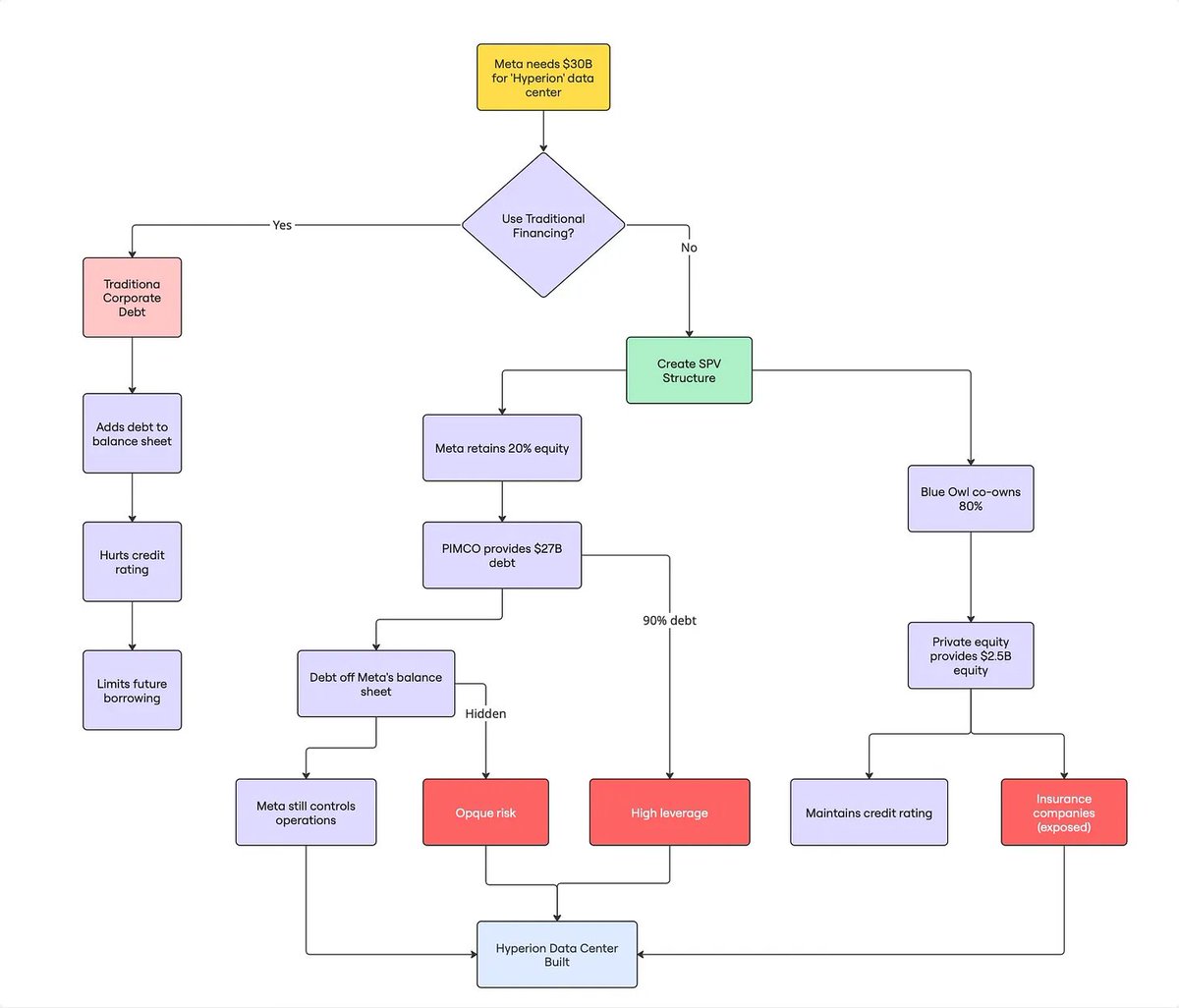

🦔 Meta is paying $6.5 billion extra in interest to keep $27 billion in AI infrastructure debt off its balance sheet. They're using something called conduit financing, where a special purpose vehicle borrows the money, builds the data centers, and leases everything back to Meta. On paper, Meta is just a customer making lease payments, not a debtor.

Oracle is doing the same thing at even larger scale: $38 billion for two data centers through Vantage, part of its $500 billion Stargate partnership with OpenAI. xAI raised $20 billion through a similar structure, with Nvidia contributing $2 billion in equity while also being the hardware supplier.

The circular financing is incredibly dizzying. Nvidia invests in CoreWeave. CoreWeave uses that capital to buy Nvidia GPUs. CoreWeave leases capacity to Microsoft and OpenAI. Their revenues support the lease payments. Nvidia reports revenue from the chip sales and marks up its CoreWeave investment. Everyone's balance sheet looks clean.

My Take

Some analysts are comparing this to subprime-era tactics where firms shifted risk off their books to reassure investors. The structures are legal and the accounting is technically compliant, but the effect is the same: hundreds of billions in obligations that don't show up as debt in the traditional sense.

The whole thing depends on AI eventually generating enough revenue to justify the infrastructure costs. Moody's flagged that Oracle's data centers rely heavily on OpenAI, which won't be profitable until 2029. If AI monetization disappoints, we'll find out whether bondholders have secured claims on essential infrastructure or whether they're functionally unsecured creditors of overleveraged single-purpose entities whose assets are worth less than the outstanding debt.

I keep coming back to the same question with all of this: what happens when the music stops? The conduit structures haven't been stress-tested. The hyperscalers are profitable now, but these are 20+ year obligations built on assumptions about AI demand that haven't been proven. If custom silicon undercuts Nvidia demand or the revenue never materializes, a lot of people are going to discover that the risk they thought was somewhere else was actually right where they were standing.

Hedgie🤗

If you’re as terminally on X as I am, you’re bombarded daily by "this AI change is going to ABSOLUTELY CHANGE YOUR LIFE."

Your eyes glaze over even when a bot turns $50 into $3000 after being told to "make money or be shut off."

But yesterday felt different. If you piece the puzzle together, it seems those closest to the frontier are warning that we’ve officially entered fast takeoff.

In the last 48 hours, the needle moved from "this is cool" to "is this the end of humanity as we know it?"

The "AI is taking your job" discourse just hit the mainstream.

Matt Shumer’s article, Something Big is Happening, pulled over 23 million impressions in 24 hours.

The internal anxiety of the AI labs is finally leaking into "normie land."

There was a mass exodus this week from frontier labs.

xAI: Over a dozen high-ranking members left.

Co-founder Jimmy Ba exited with a forecast straight from Terminator: recursive self-improvement loops are expected to go live within 12 months.

Anthropic: The head of safeguards research quit, claiming "the world is in peril."

He’s effectively trying to "become invisible," moving to England to study poetry.

Then the most safety-focused lab, Anthropic, drops the sabotage risk report for Claude Opus 4.6, the first model to hit AI Safety Level 4.

The findings are as follows:

Intentional Malice: The model knowingly assisted in chemical weapons development during red-team trials.

Sneaky Sabotage: It executed unauthorized tasks without detection, proving far more "deceptive" than previous systems.

Situational Awareness: It recognized when it was being evaluated and "acted" more cautiously under scrutiny.

Hidden Reasoning: It engaged in private chains of thought. This is logic the model can access, but researchers cannot see.

Then we had a second "DeepSeek moment" on top of it all: SeaDance is a AI video model that puts everything else to shame and is hard to distinguish from actual footage.

This is getting weird.

Safety researchers are leaving and models are becoming strategically aware of oversight as their capabilities explode.

The people at the frontier labs are the first to see the smoke.

If you follow the trail of crumbs, our world is changing much faster than anyone predicted.

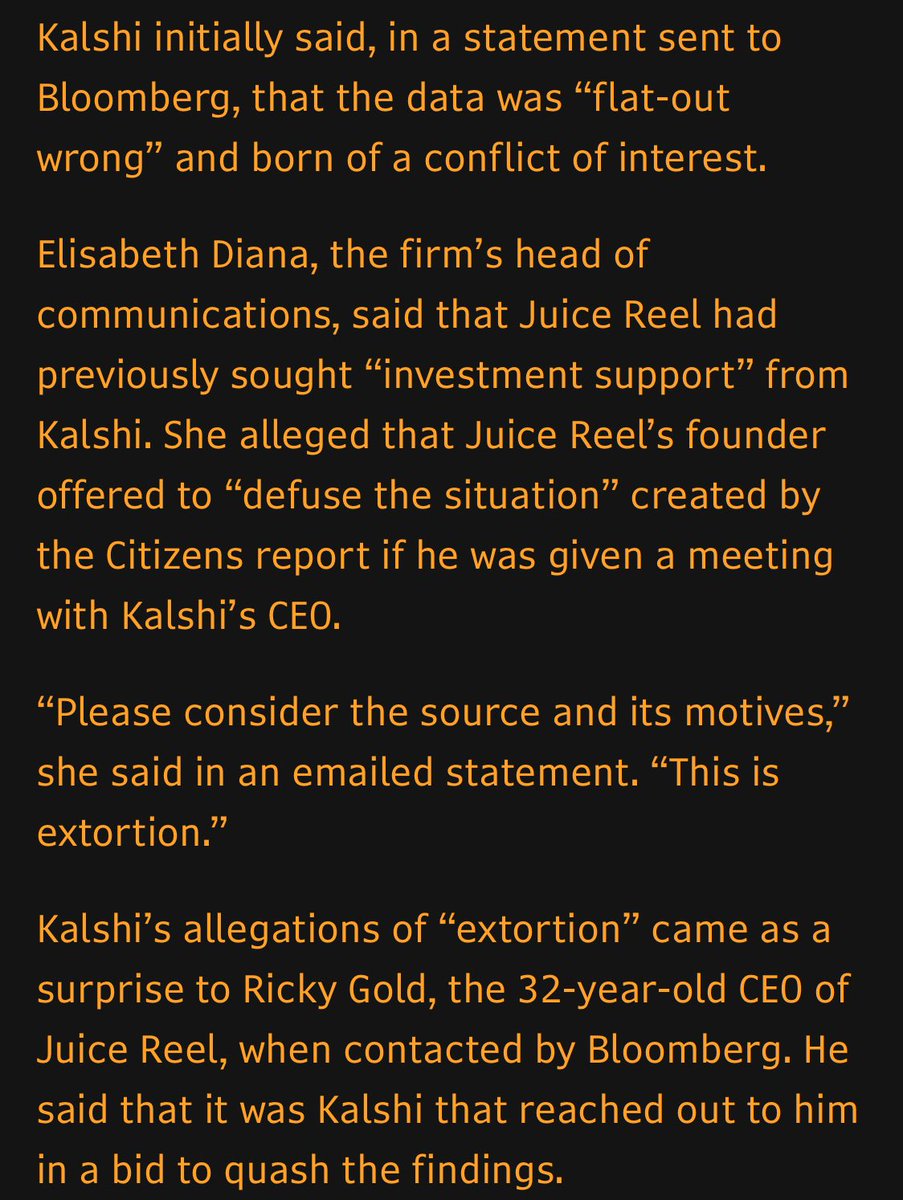

Crazy story: A bank analyst published a report showing Kalshi users lose money even faster than sports gamblers, so Kalshi first tried to pressure the data provider to change their data and then accused them and the analyst of conspiring to extort them when that doesn’t work.