Top 5 online savings accounts by APY as of 6/1/2026

& thread on online savings account (OSA) yields and how OSA & money market fund (MMF) yields have changed since the first Fed rate cut (9/18/2024):

Top 5 Status: CineFi falls to 4.00% & is replaced by 316 Financial (4.05%).

Big 5 Status: No changes from last week

It’s “Jobs Friday” in the US. Consensus forecasts expect what I would characterize as a “steady state” report for April, including:

Solid job growth of 88,000.

Unchanged unemployment rate (4.3%), labor force participation (61.8%), and average weekly hours (34.3).

Annual earnings growth edging down to 3.4%, based on a 0.3% monthly increase.

#economy #markets #jobs #employment #unemployment

🚨 JUST IN: JPMorgan, Citi, Bank of America and Wells Fargo are building a shared blockchain to keep deposits from leaving the banking system.

The Clearing House will run it. Target launch is the first half of 2027.

Interestingly, this appears led by being defensive rather than clients, at least according to some quotes. Bank of America's head of global payments, Mark Monaco, told the WSJ that clients aren't "beating down the door" for tokenized deposits.

The reason they're building it anyway sits in what they walked away from. A year ago this same group explored a joint bank stablecoin through The Clearing House and the operator of Zelle. They dropped it and picked a blockchain for deposits instead.

Remember deposits are money that stays still. They sit on the bank's balance sheet as a claim you hold against the bank. Stablecoins are money that moves. A bearer instrument that can leave your bank on Saturday and settle somewhere else by Sunday.

And given they're working with The Clearing House (TCH) that makes sense. Deposits can't leave a bank and go anywhere, but through clearing, banks can figure out all of the possible transactions that need to happen, and "net" them into one single efficient transaction multiple times per day. So instead of sending $10m one way, and $9m back. The banks send the difference or "net" of $1m.

But I don't get why they need a blockchain to do this?

The Clearing House already clears deposits in the USA between the member banks?

Tokenized deposits DO have demand if you talk to JP Morgan, their clients have cleared $3 trillion to date, but all cross-border. So again, what is the clearing house adding here?

Meanwhile, you have SoFiUSD which is live, and 1:1 exchangeable for its Tokenized Deposit, 24/7. Meaning, they enable instant, global exchange of dollars that can be off-ramped to any other payment system.

The US banks in the clearing house won't have that same cross-border advantage. To me, this looks like the clearing house got a tech upgrade, that maybe it didn't need?

Stablecoins are open loop. Global. 24/7. *That* is their advantage.

Tokenized deposits are 24/7 and safer. But closed loop.

These two things should co-exist not compete.

JPMorgan, Citi and Big Banks Plan New Tokenized Deposit System to Answer Crypto | @ginaheeb & @Vlajournaliste for @WSJ

“The new network could help banks contend with a wave of new competition from stablecoins and crypto firms”

https://t.co/ldn1KhfO3N

One note on DQ’s CD leaderboard: Merrick Bank was noted for its recent rate hikes and cuts. Its 4-year CD continues to be the rate leader for banks.

One interesting thing to note is that Merrick just started to offer CDs on the Raisin platform, with rates that are slightly lower than what it offers directly. The advantage for consumers is that Raisin’s CD minimum deposit is only $1, whereas the minimum on Merrick’s website is $25,000.

Merrick’s aggressive rate pricing indicates a need for funding its credit card business. In 2025, its brokered deposits increased 77% while its other deposits declined 28%. Since deposits on Raisin are not considered brokered deposits by regulators, Merrick may have decided to focus on Raisin and direct CDs instead of brokered CDs.

My last review of Merrick Bank was in April.

https://t.co/CWQlmPZKSU

Holders of S&P 500 index funds are understandably nervous about mega-high-cap SpaceX entering the index soon. This is an unproven, risky investment with a loss of $4.9 billion in 2025. (Early backers will reap huge rewards, however.) https://t.co/DrmwiT9RO0

Revolut plans 2027 US🇺🇸 bank launch with FDIC accounts, stablecoins, multi-currency deposits & crypto trading.

1M US customers now confirmed.

No branches, ATM access, HQ in Stamford, CT, office in New York.

Targeting global currency users.

Source: CEO Cetin Duransoy to Reuters

This article provides some insights in how online banks decide deposit rates. This was surprising:

“online account holders tend to be sleepier than people who open accounts at branches”

https://t.co/qgcRfxMMTA

This has been a busy week for savings account rate cuts at the major online banks.

Ally Bank just cut today. Capital One and Marcus cut yesterday:

APYs:

Ally Bank Savings: 3.10% → 3.00%

CapOne 360 Performance Savings: 3.10% → 3.00%

Marcus Online Savings: 3.50% → 3.40%

Perhaps the banks determined they needed to cut now before the Fed starts hiking.

Marcus by Goldman Sachs just lowered the rate of its Online Savings Account to 3.40% APY.

It had been 3.50% APY since April 22nd when the APY fell from 3.65% to 3.50%. Its peak had been 4.50% from Dec 2023 to Apr 2024.

Marcus had a long stretch of holding its rate steady that extended through last fall’s Fed rate cuts. It had a 3.65% APY that lasted from May 28, 2025 to April 21, 2026. Sorry to see Marcus now being quick to cut.

@getderb IMO, It's a trade-off of keeping deposits vs maximizing net interest margins. The bigger they get, the easier it is for them to keep deposits.

You're right about CIT Bank. Their Platinum Savings account rate has been one of the leaders for a major online savings account.

Ally Bank just lowered its savings account and money market account rate by 10 bps to 3.00% APY. It comes just one day after Capital One made the same cut.

Ally savings had been 3.10% APY since April 16th when the APY fell from 3.20% to 3.10%. Its peak was 4.35% APY in early 2024.

Ally's 11mo No Penalty CD rate was also lowered 10 bps. It’s now 2.70% APY.

If you're an Ally Invest customer, you have free access to many mutual funds, including $VUSXX. It's easy for Ally customers to use VUSXX instead of the Ally savings account for their savings. VUSXX’s current compound yield is 3.66% and since it holds mostly Treasuries, the interest can generally be exempt from state and local income tax.

@adorkssssss IMO, for these banks it's a game of keeping their depositors somewhat content while maximizing net interest margins. Once serious hike talk starts at the Fed, cutting savings account rates will look especially bad from a PR point of view.

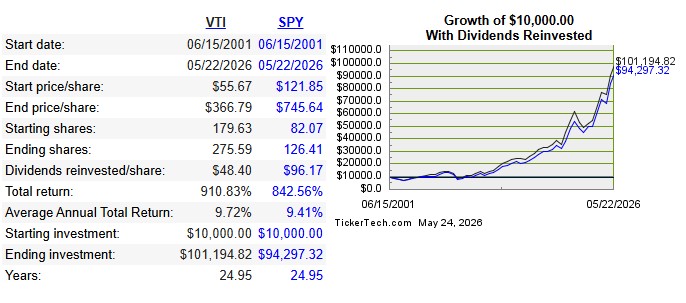

The Vanguard Total Stock Market ETF (VTI) turns 25 today!

VTI was launched on May 24, 2001. It’s now the 4th largest ETF by assets under management ($637B). It’s a share class of the Vanguard Total Stock Market Fund which includes the mutual fund VTSAX. It’s the largest mutual fund with $2.2T in assets. Vanguard 500 Index Fund is the second largest with $1.6T in assets, while its share class ETF, VOO, is the largest ETF with $957B in assets.

VTI is based on the CRSP U.S. Total Market Index. The Index was designed by the Center for Research in Security Prices (CRSP). CRSP was under University of Chicago until last February when it was acquired by Morningstar. The Index has around 3,500 U.S. stocks ranging from microcaps to bluechips.

In the last 10 years, VOO has slightly outperformed VTI (15.21% vs 14.73%), but in the last 25 years, VTI has slightly outperformed SPY (9.72% vs 9.41%). Note, SPY was used for comparison since VOO didn’t begin until 2010.

References:

https://t.co/86E5TjhtSU

https://t.co/ADpyUk5zmU

https://t.co/vdq55eQtwI

https://t.co/Ez5mv6vI2k

https://t.co/XATbdrvQe9

https://t.co/muWOpHZmAY

https://t.co/mTGYjJP8Zc

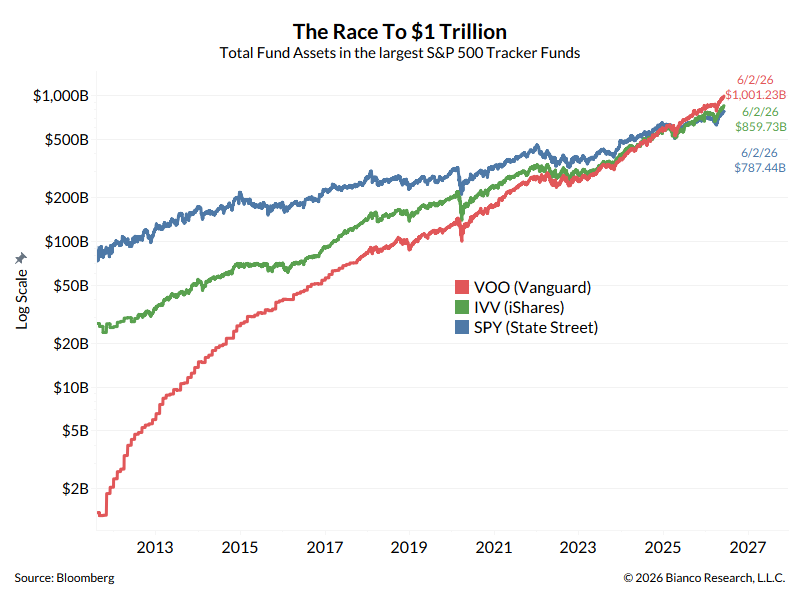

Yesterday, VOO, the Vanguard S&P 500 ETF, surpassed $1 trillion dollars in assets. The first ETF to hit this milestone.

IVV and SPY are in second and third place; they are all S&P 500 tracker ETFs.

@EricBalchunas@JSeyff@DaveNadig

Jamie Dimon said JPMorgan Chase is “on the lookout” for an acquisition. I've put together a shopping list for Jamie. At the top of the list: Ramp and Betterment.

See the new Fintech Snark Tank post to find out who the other acquisition targets are:

https://t.co/L2pK9R88g7

Key point: Investors in TIPS usually also have sizable investments in equities. TIPS fulfill a specific need for inflation-protected cash flow into the future. Adam Grossman is a good guy, though. @christine_benz https://t.co/LcmXykxky5

@TipsWatch@christine_benz Allan Roth (@Dull_Investing) has done a good job at describing how TIPS ladders and stocks can coexist in a portfolio:

"While I think TIPS and TIPS ladders are great, I also tell people not to put more than 25% of their fixed income in TIPS."

https://t.co/T2l4MKztED

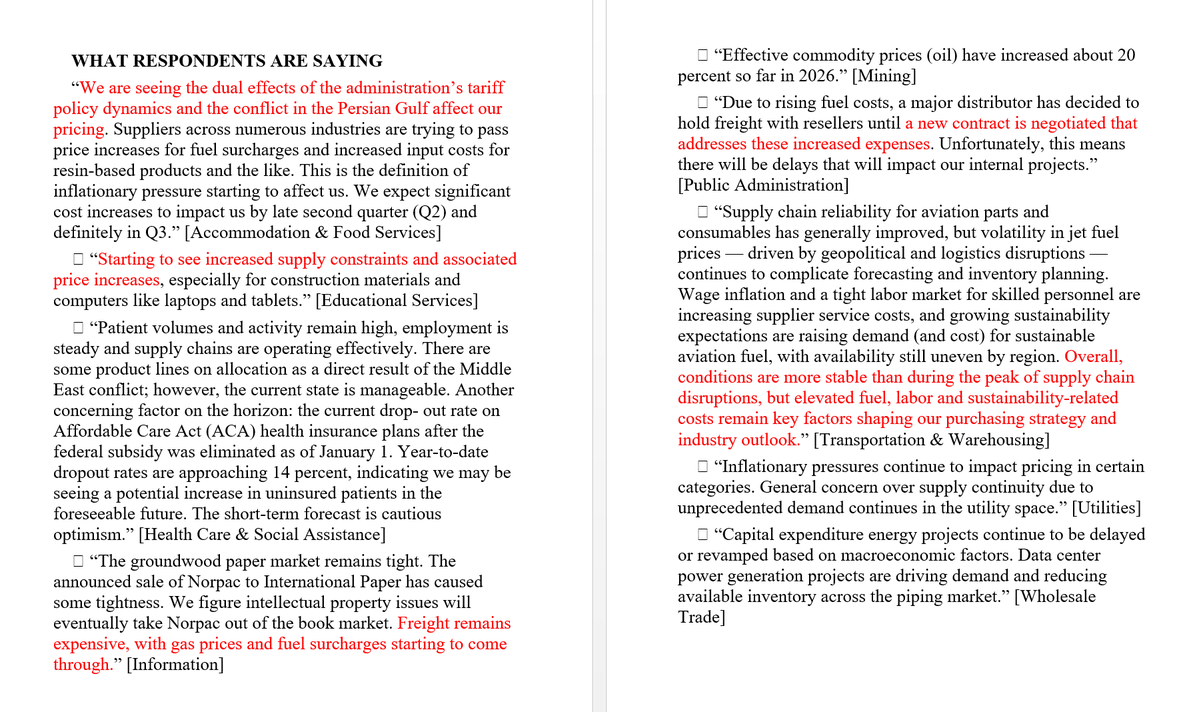

Across the 10 responses included from this month's ISM survey of service-industry purchasing managers (the people who buy things on behalf of businesses), the dominant theme is rising costs, driven by fuel and energy prices, tariffs, and AI-related demand.

No respondent reports prices easing or falling. A few comments focus more on supply tightness than on prices directly, but none point in a disinflationary direction.