We have been discussing that the highest probability of a correction will be in the August-October period heading into the mid-term election. The latest update from @NDR_Research of their S&P 500 Cycle Composite confirms the same.

h/t @ISABELNET_SA

Oracle 5Y CDS back at record highs. At the same time, NVIDIA's CDS is becoming interesting.

Has the AI sector hit a wall?

it is all about leverage🙄🙄

$orcl $nvda

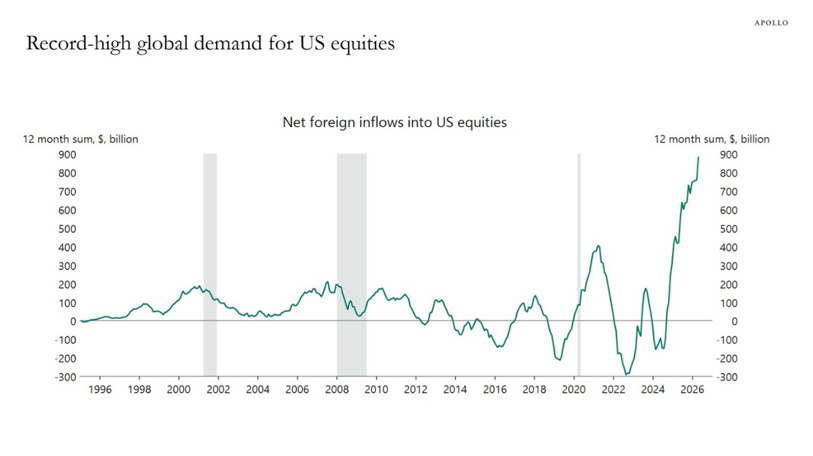

Important points from Apollo's Torsten Slok:

"Net foreign inflows into US equities have surged to a record high, driven in large part by overseas investors seeking AI exposure"

"With most foreign equity investors not hedging their FX risk, the bottom line is that if AI disappoints, the resulting pullback in these inflows would be a significant downside risk to the US dollar."

My take: It's not IF AI disappoints, the only question is when. And when that happens, the massively overbought dollar (hedge funds are also heavily long currently) could decline significantly and that would be an important propellant for gold (which is oversold and under-owned by hedge funds). Gold is currently signaling it may have already reached a bottom.

Remember when Scott Bessent said to judge him by the 10-year Treasury?

US 10-year real yields just reached their highest level in more than 2 years.

Markets are the ultimate judge of fiscal discipline.

Reminder:

The US simply cannot afford both a war and higher interest rates.

https://t.co/XL4PidBKZo

The semis have averaged a daily change of +/-3.36% over the last 50 trading days.

The only other times we've seen this much daily vol was in the lead up to the Dot Com peak and down the mountain, the Financial Crisis in late 2008, and in early 2020 during the COVID Crash.

Hyperscaler credit spreads continue to widen.

If you are a believer that CapEx can go on indefinitely, Mr. Market would like to have a word with you!

Source: Goldman Sachs

UBS on core CPI drop

The surprises relative to our expectations in this month’s release were largely in core prices where transportation services, communication services, and lodging away from home were all well below our projections. These are all categories that tend to be volatile (and even more so with the decline in CPI price quotes since April of last year), so we generally suggest paying little attention to them when thinking about the longer run-trend in inflation. That said, even accounting for these categories and the issues with seasonal adjustment, this was not a strong CPI and is consistent with our view that last month was likely the peak for US inflation.

The latest update from the @AtlantaFed shows a sharp deceleration in economic growth from the original estimate. Despite the market remaining very optimistic about forward earnings, the slowdown in economic activity is concerning.

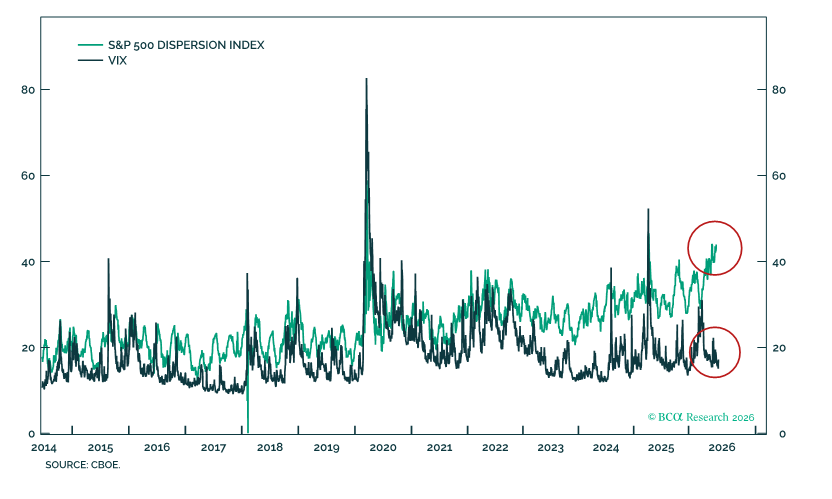

"The chart below from Citigroup tracks the number of S&P 500 companies each quarter that moved more than 10% in either direction on earnings day. For much of the past decade, that number was relatively low, often around 10 to 20 companies per quarter. Since 2024, however, the count has climbed sharply, with several recent quarters showing more than 30 or 40 companies making such large moves. The tally peaked above 60 during the first-quarter earnings season."

This data doesn't go back far enough. It's not a trend that began in 2024. In my February report on "Price Discovery" (https://t.co/kEx5Z4BbRz), I referenced a Stanford study that found that:“[There’s been a] striking increase in investor response to earnings announcements from 2001 to 2016, as measured by return variability and volume following [announcements].” Increased earnings reactiveness is also part of a broader trend of generally greater news-cycle reflexiveness. For one, upside or downside moves of five standard deviations or more amongst the 100 largest stocks in the S&P 500 have been increasing in frequency for more than a decade. Last year alone, there were 47 instances of such severe single-stock selloffs, the most in Barclays records going back to 1998.

I founded Sage Road Research roughly a year ago to focus on deep research into structural trends because I believe thinking longer term, more holistically, and with less bias is essential to exploiting the ever-increasing news-cycle reflexiveness of equity markets. Learn more here: https://t.co/Wgwz2xmY1y. Interested in subscribing? Message me.

MarketWatch link: https://t.co/m1DRlSzbRf

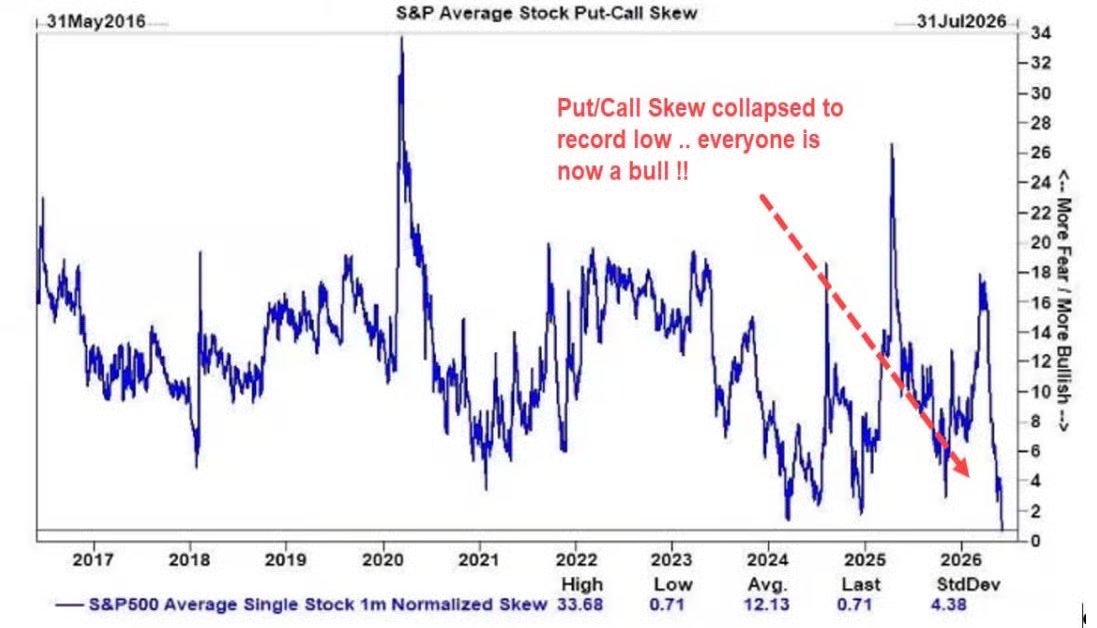

"The S&P put/call skew just collapsed to 0.71. Not a low. The lowest reading on record ... crash protection is essentially free. Nobody wants it."

Goldman Sachs via @ThierryBorgeat

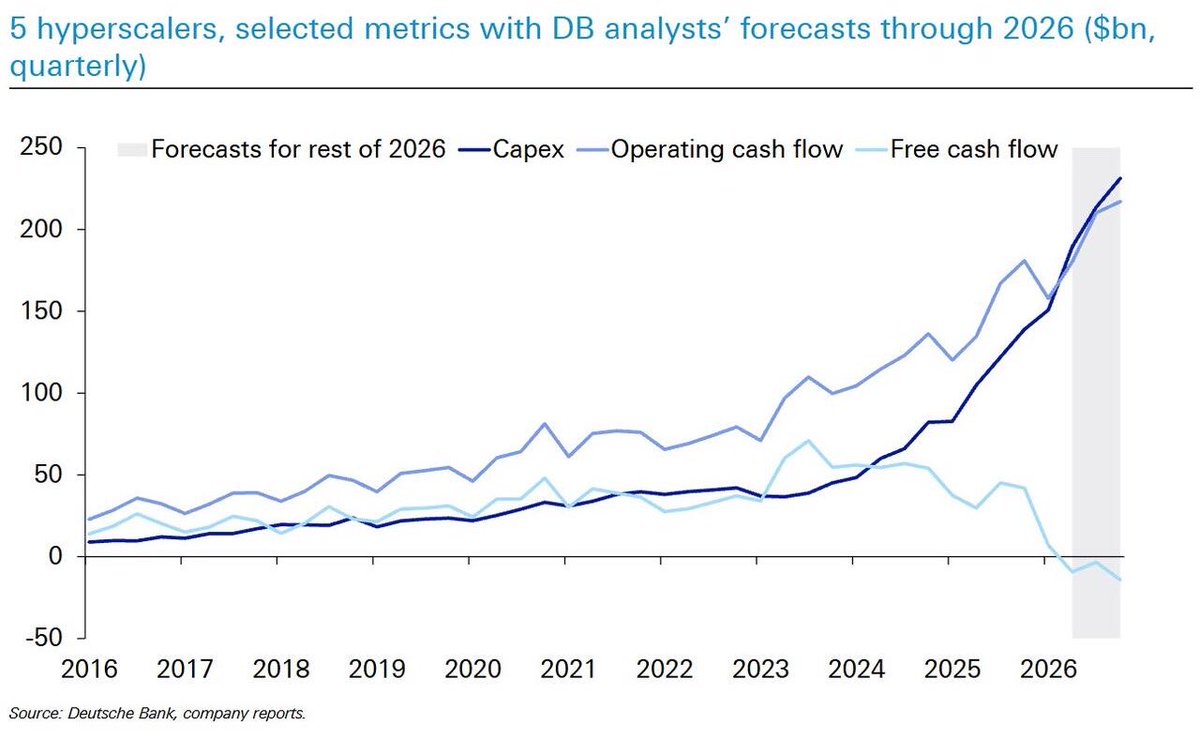

Shocking Stat of the Day:

“The 5 largest US hyperscalers are now spending more on Capex than their combined operating cash flow...”—DB

In other words, they spend more than they make. Somehow, Wall Street analysts will find a way to tell you this is ok.

Have a terrific Tuesday! 😊

Source: Deutsche Bank

![trevornoren's tweet photo. "The chart below from Citigroup tracks the number of S&P 500 companies each quarter that moved more than 10% in either direction on earnings day. For much of the past decade, that number was relatively low, often around 10 to 20 companies per quarter. Since 2024, however, the count has climbed sharply, with several recent quarters showing more than 30 or 40 companies making such large moves. The tally peaked above 60 during the first-quarter earnings season."

This data doesn't go back far enough. It's not a trend that began in 2024. In my February report on "Price Discovery" (https://t.co/kEx5Z4BbRz), I referenced a Stanford study that found that:“[There’s been a] striking increase in investor response to earnings announcements from 2001 to 2016, as measured by return variability and volume following [announcements].” Increased earnings reactiveness is also part of a broader trend of generally greater news-cycle reflexiveness. For one, upside or downside moves of five standard deviations or more amongst the 100 largest stocks in the S&P 500 have been increasing in frequency for more than a decade. Last year alone, there were 47 instances of such severe single-stock selloffs, the most in Barclays records going back to 1998.

I founded Sage Road Research roughly a year ago to focus on deep research into structural trends because I believe thinking longer term, more holistically, and with less bias is essential to exploiting the ever-increasing news-cycle reflexiveness of equity markets. Learn more here: https://t.co/Wgwz2xmY1y. Interested in subscribing? Message me.

MarketWatch link: https://t.co/m1DRlSzbRf](https://pbs.twimg.com/media/HM3-iAUWEAAgnHZ.png)