An elegant explanation for this is that everything is broken. Human institutions frequently don’t pursue their formal goal effectively, but rather spasm in its general direction.

4/n

William got margin called and pledged over $1B of his own stock to fund Column. He explains why extreme personal risk is what makes great founders, and why we see less of it today:

"I think that the good founders bet on themselves and take an extreme amount of risk to do that. The extreme amount of risk part is something that we no longer have.

But when there's literally only one door in front of you. You don't have a choice, and that fear and innate desire creates another part of you. It creates creativity, it creates inspiration. It's extremely valuable part of the founder journey. And in many ways, Silicon Valley we've actually removed that.

I don't know why we don't talk about it more.

If you go back to pre 2008, you're on the edge of the knife. We don't create environments where a founder has to bet themselves.

I think starting companies are just too f**king safe. It's caused a lot of companies to be super safe companies like, we're gonna pivot to AI...that's not bold, that's not ambitious.

It's because we are attracting founders that actually want to be employees. They don't think if I don't pull this off, I'm going to become bankrupt. My life is over and I think that's pretty healthy. That's when you bring out the rawness of humanity and I don't see that very much anymore.

The weird thing is an early stage employee takes way more risk than an early stage founder. And I don't think we should actually de-risk the early stage employee. I just think we need to increase the risk for founders. I think we need to make failure much more expensive."

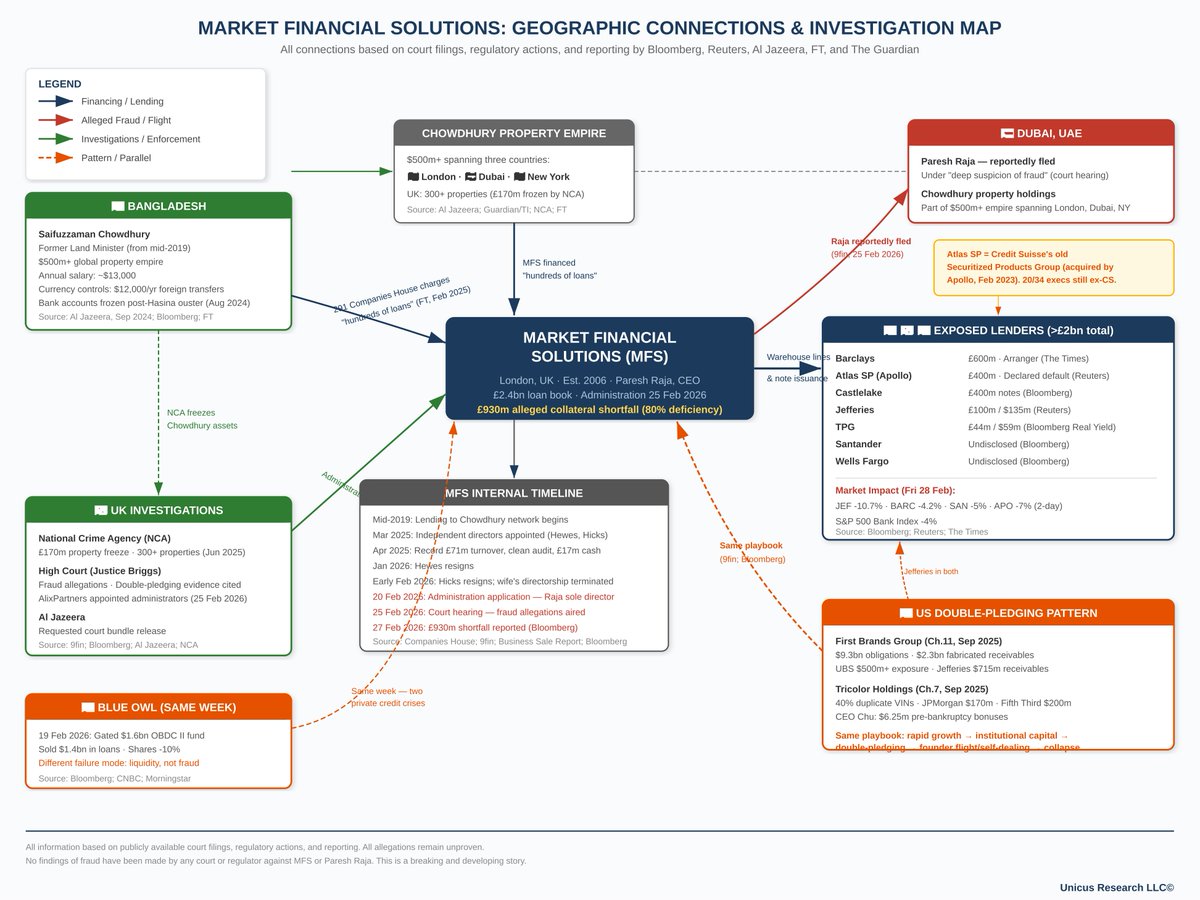

🚩Two days ago we shared what is unravelling with market Financial Solutions.

Atlas SP, Credit Suisse's old securitization unit reborn under Apollo, provided £400m in warehouse financing to MFS. It is worthy to mention that 20 of 34 execs listed on Atlas SP's website came from Credit Suisse.

Atlas has now declared default on two warehouses and is pursuing legal action after allegations of double-pledged collateral.

We continue to mention that FBG, Tricolor, Primalend were not isolated. Now, we have MFS. We suspect a fourth one is brewing.

See below.

Boston has the schools. SF has the companies. 21 of the Forbes AI 50 founders went to school in Boston—then left for San Francisco. If SF doesn’t learn from this cautionary tale, Austin and Miami will.

https://t.co/pmYxLaYXWy

This line hits hard: "Because the long run fruits of Western Keynesianism are the same as Soviet Communism, in the sense of wealth seizure and pauperization."

LIQUIDATION CONTAGION

Wealth taxes are even worse than you think. Any asset held by Californian billionaires or Dutch citizens is now at risk of experiencing forced liquidation pressure.

So: it’s not just that you don’t want to hold assets as a Dutchman. You also don’t want a Dutchman to hold your assets. Because the logic of forced liquidation is contagion.

Let’s think it through.

(1) First, suppose there is an asset with a total market cap of $10,000, with 10 shares total, of which 1 share each is held by 10 different holders, all in the Netherlands. To simplify the math, assume the Dutch holders bought those shares at par, or close to $0.

(2) Now suppose today is the unrealized cap gains tax day, and the share price is $1,000 per share. Each Dutch guy is hit with a 36% tax, and owes $360. The first guy sells his one share, gets $1,000, and pays $360 in tax while retaining $640.

(3) But the first guy’s sale reduces the market price to $960 per share. So when the second guy sells, he only retains $600 after paying $360 in tax.

(4) Now assume that by the 7th guy, all the selling has pushed the share price to collapse to $200 per share. This is a very reasonable scenario if 60% of the cap table has suddenly been dumped. Indeed it might go much lower.

(5) At $200 per share, the 7th guy actually has to go into debt to pay the tax as he owes $360. He sells his one share, pays all $200 of the proceeds in tax. And still owes $160 more in tax.

(6) The 8th, 9th, and 10th guys are even more screwed. By the time they sell, the price will likely have crashed to $100 per share or less. As with the 7th guy, even 100% liquidation will not cover their tax burden.

(7) So we immediately see many negative things about the Dutch unrealized cap gains tax bill.

(a) First, it will cause large simultaneous forced liquidations. Everyone must sell 36% of their stake near the same time.

(b) Second, it may be literally impossible to pay if a critical mass of the cap table is all subject to it at the same time. In the example above it was 100% Dutch holders, but has it been just 60% the result would have been much the same: a collapse in the share price.

(c) Third, that means it would be disastrous to have too many Dutch citizens (or Californian billionaires!) on the cap table. Their forced sales will crash your share price.

(d) So, you might have to start mass blocking those resident in wealth-taxing jurisdictions from investing in your companies.

(e) This in turn makes the poor Western European guy even poorer, as he gets locked out of high growth assets.

To be clear: I really do feel bad for the formerly Flying Dutchmen, now Crying Dutchmen. They invented much of modern capitalism. They founded New Amsterdam, now New York. They’ve punched way above their weight. I wish them only the best.

Nevertheless…they should prepare for the worst. This may be a tough century for Western Europe. The first ones out might get to freedom, while the slowest may be stuck behind a new Iron Curtain, spending a century paying off the debts their states incurred over the last century.

Because the long run fruits of Western Keynesianism are the same as Soviet Communism, in the sense of wealth seizure and pauperization.

I mean, if you knew the future, you wouldn’t want to co-own a farm with a Russian in 1916. For similar reasons, you might not want to co-own a share of stock with Dutch national in 2026. Or with anyone in a seizure-curious jurisdiction…which unfortunately includes much of Western Europe, Canada, and Blue America.

You instead want assets that are not held by those subject to forced liquidations. Now, I grant that this is an unusual way to rank assets…Dutch holders considered harmful?!? Yet it might sadly be necessary to minimize your exposure to liquidation contagion.

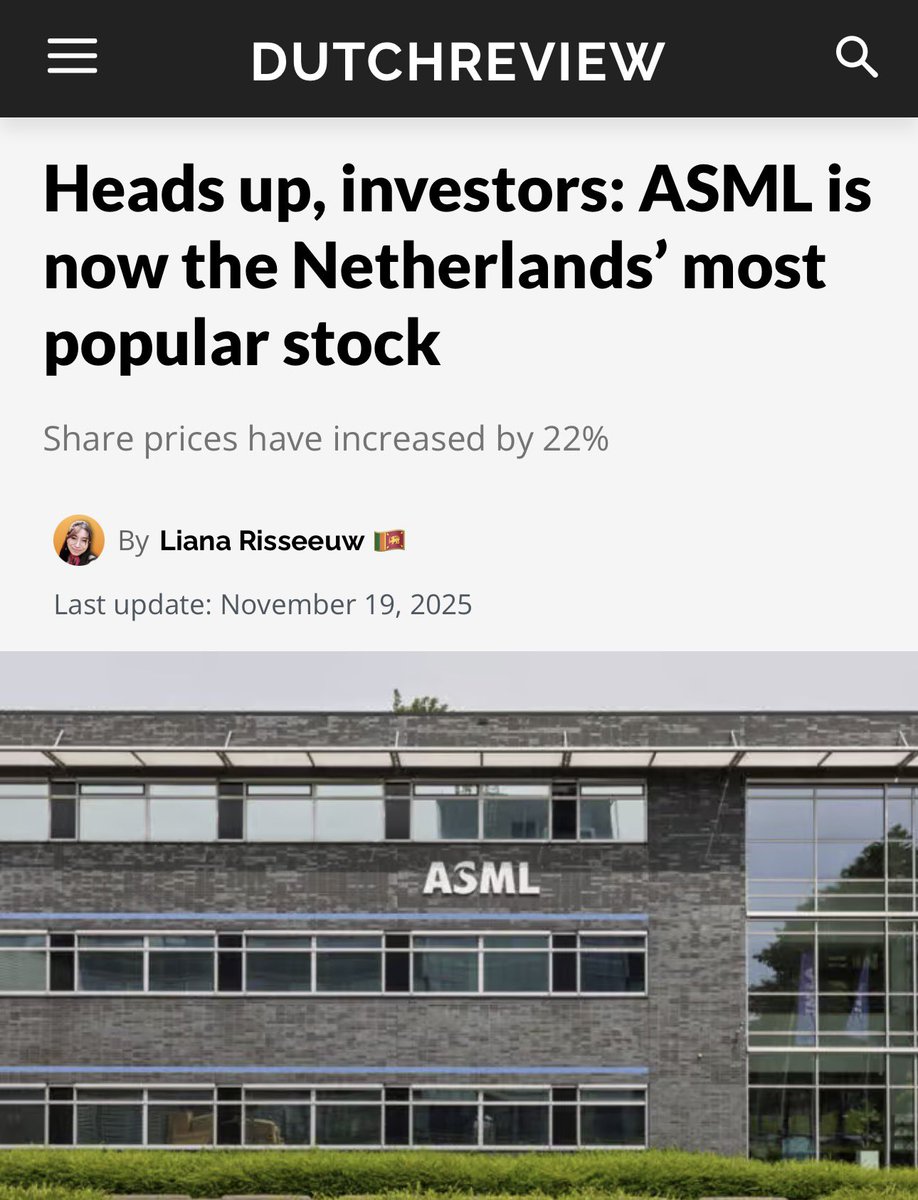

PS: guess which crucial stock is most held by the Dutch? ASML. So: this unrealized cap gains tax may not literally be a communist plot, but it would have the same effect.

Many of the most significant companies of the last two decades share a common DNA: they applied technology to essential services that had stubbornly remained offline.

From banking to transportation, the infusion of software fundamentally reshaped our daily lives. When we first met Peter Colis and Lingke Wang at the seed stage in 2017, they identified an industry overdue for this transformation: life insurance.

Despite 84% of Americans recognizing the need for coverage, the effort involved—blood draws, reams of paperwork, and month-long wait times—left millions unserved. Peter and Lingke’s vision was to make life insurance instant and frictionless, breathing technology into a massive, stagnant category.

Challenging the norms of an industry this established is a daunting task. It requires a rare level of grit. Over the last nine years, the @get_Ethos team has stayed true to that original insight, providing financial security to hundreds of thousands of families who previously lacked it.

Congratulations to Peter, Lingke, and the entire Ethos team on today’s IPO. It has been a privilege to partner with you from the beginning. Your journey is a powerful reminder of what happens when you combine a clear vision with relentless execution. $LIFE

"Because there's no history to restrain the imagination, the future can appear limitless for the new thing. And futures that are perceived to be limitless can justify valuations that go well beyond past norms"