there's 2 things you should do RIGHT NOW if you're unsure about your AI stocks

1. Buy the F'in Dip! This is an absolute gift from the markets

2. Unlock your trial at Milk Road PRO to get conviction and portfolio advice

there's no reason to be afraid about semis, neoclouds, etc. stocks rn

this bull market is not over

the AI build out is nowhere near over

we are going much higher

that's all you need to know and all you need to do

Milk Road PRO analysts have been guiding 1000's of members through this entire bull market

if you're afraid, unsure or have missed this run up... it's time to join and turn this market on easy mode

the link is in my bio to subscribe, see you on the inside!

Milk Road PRO analysts were super early to $MU, $BE, $NBIS and many more assets in this bull market

You can track our live trades and portfolios for just $1

Check it out here:

https://t.co/tsCY5Dq9IT

there's 2 things you should do RIGHT NOW if you're unsure about your AI stocks

1. Buy the F'in Dip! This is an absolute gift from the markets

2. Unlock your trial at Milk Road PRO to get conviction and portfolio advice

there's no reason to be afraid about semis, neoclouds, etc. stocks rn

this bull market is not over

the AI build out is nowhere near over

we are going much higher

that's all you need to know and all you need to do

Milk Road PRO analysts have been guiding 1000's of members through this entire bull market

if you're afraid, unsure or have missed this run up... it's time to join and turn this market on easy mode

the link is in my bio to subscribe, see you on the inside!

You missed the semiconductor trade because you were afraid, you missed the memory trade because you were afraid and now you are going to miss the next rally for the exact same reason (Save this).

Look at what just happened this week alone.

ASML beat Q2 2026 estimates and raised its full year revenue outlook to €43-45 billion, up from prior guidance of €36-40 billion, the second time this year they have raised guidance.

Their CEO said on the call that "ongoing AI-related investments and continued progress in AI technologies are driving demand for advanced logic and memory chips" and that their customers are "accelerating their capacity expansion plans."

Memory revenue alone is expected to grow 75% this year.

TSMC raised 2026 capex guidance to $52-56 billion, at least 25% above 2025 levels and guided for nearly 30% revenue growth.

Meanwhile, Meta is doubling its data center deployments in 2027.

OpenAI's GPT-5.6 compute literally cannot keep up with demand, Codex went from 5 million to 9 million users in a single month, and Sam Altman confirmed agentic product usage rose 2.5x in a single week.

Anthropic is approaching profitability meaning even the companies spending the most on inference compute are starting to turn the corner on monetization, which means the demand cycle extends further.

This is the pattern and it repeats every single time.

In 2023, people missed Nvidia because they said valuations were too high and AI was overhyped meanwhile Nvidia hit 5T in market cap.

In early 2025, people missed Micron at $80 because they said the memory cycle was peaking while Micron crossed $1 trillion in market cap.

The pattern is always the same and the data is always clear.

The fear is always louder than the data and the people who let the fear win are always the ones watching from the sidelines when the rally resumes.

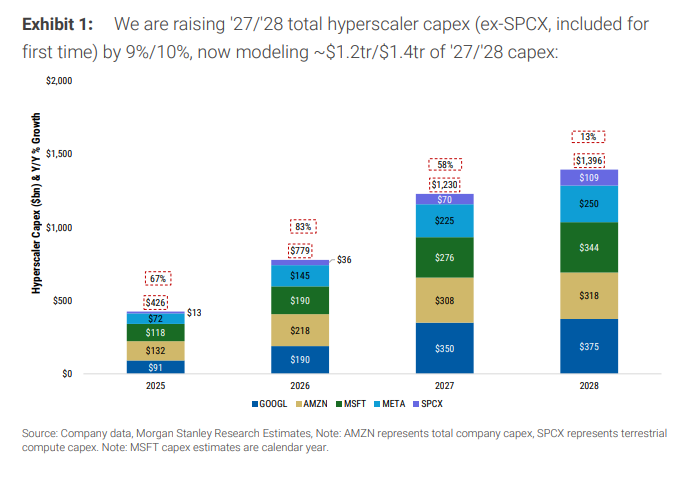

The AI thesis is completely intact, hyperscalers are still guiding to $1.4 trillion in capex by 2028.

The foundational infrastructure, chips, memory, data centers, power is being built out faster than any previous technology cycle in history.

The applications consuming that infrastructure, from autonomous coding agents to physical AI to agentic workflows, are growing faster than even the most optimistic projections.

What is keeping the market down right now is also some Iran war noise and rate hike fears.

Neither of those things changes the fact that Meta is doubling its data centers, ASML is raising guidance for the second time this year, TSMC is spending $56 billion in capex, Micron's HBM is sold out through 2027, and OpenAI's infrastructure literally cannot keep up with how fast people are using it.

This is a temporary dip within a stronger upcycle and the people who act on the data instead of the fear are the ones who will look back at this week as one of the better buying opportunities of the year.

I am a buyer at these levels and make sure to follow me @MelvinInvests for more market insights.

if @GavinSBaker tells you the risk/reward in semis is attractive

you should assume that the risk/reward in semis is attractive

enjoy this mid-cycle, summer gift from the markets

there's 2 things you should do RIGHT NOW if you're unsure about your AI stocks

1. Buy the F'in Dip! This is an absolute gift from the markets

2. Unlock your trial at Milk Road PRO to get conviction and portfolio advice

there's no reason to be afraid about semis, neoclouds, etc. stocks rn

this bull market is not over

the AI build out is nowhere near over

we are going much higher

that's all you need to know and all you need to do

Milk Road PRO analysts have been guiding 1000's of members through this entire bull market

if you're afraid, unsure or have missed this run up... it's time to join and turn this market on easy mode

the link is in my bio to subscribe, see you on the inside!

dont try and navigate this bull market alone

the market is hard, but the advice from our analysts is straight forward

track all 5 of their portfolios in real time here:

https://t.co/tsCY5DpBTl

Medicare just started paying for GLP-1 weight loss drugs for the first time and 2 of the 3 are Eli Lilly's

The bear case for $LLY was always "nobody can afford these drugs long term and Medicare doesn't pay for weight loss drugs"

That's changing

On July 1 the Medicare GLP-1 Bridge went live. Eligible Part D beneficiaries now get covered GLP-1 obesity drugs for $50 a month flat, no matter their income, with prior authorization, running through December 2027

KFF found 3.8 million Medicare beneficiaries already met the eligibility criteria (from 2023 claims data). That is a brand new patient pool that was priced out at list price

But more importantly, Eli Lillys newer drugs like Retatrutide are not only having even better effects on weight loss, but also on metabolic diseases.

This would open up the door to a much wider base of patients and even more funding from Medicare

Even better, Foundayo is live and it's one of the only GLP-1 pill for weight loss you can take any time of day with no food or water restrictions

A pill you take whenever you want is the one patients actually stay on, and staying on is the whole revenue model

So Eli Lillys best products are turning into even better products, in more accessible forms and its starting to get covered by insurance and medicare

Is there a better product in the world to sell? And none of this accounts for what happened when Eli Lilly succeeds at turning into an AI platform for the rest of the pharmaceutical and biotech industry.

Milk Road PRO members are up on $LLY after getting the call to buy its most recent dip. You can also get these calls for just $1 by joining Milk Road PRO.

There's 5 analysts inside where you can track their real-time portfolios and get live trade signals (see link in bio)

Everyone thinks Chinese open source models are killing OpenAI and Anthropic (they are wrong)

The US share of AI usage on OpenRouter fell from 70% a year ago to 30% today

But what people miss is that the entire token market is growing so fast that both sides are winning at once

OpenRouter went from around 5 trillion tokens a week in April 2025 to over 20 trillion a week a year later (4x in twelve months)

So even with the US share cut in half, the actual tokens flowing to OpenAI and Anthropic still went up (not to mention the use of these tokens within the platforms themselves, which both continue to gain adoption)

Part of the reason companies keep buying more tokens is that they are being subsidized, but it's also because they are finally paying for themselves

we've seen many examples of companies finding ROI with AI, the biggest example is the growth in Meta and Amazons ad business, which continues to improve and scale because of AI

companies will get smarter about their token usage, routing from frontier models to open source models and the better they get at this, the most tokens they will consume from both sides

They're both just going to keep growing and thats why the AI trade is still far from over.

We need WAY MORE COMPUTE!

Follow me @kylereidhead for more insights on AI, semis and the next big market themes

track my real-time portfolio at Milk Road PRO (link in bio)

$NVDA just launched two new chips that push it into the one AI market it doesn't yet own (Save this)

Nvidia already owns AI in the data center

Now they're coming for edge, the chips inside robots and machines in the real world

The launch is two new Jetson Thor modules, the T3000 and T2000

They pack the same Blackwell architecture as Nvidia's flagship robot brain into about half the size and power, built to drop into mass market robots and edge devices at volume

And the market it's chasing keeps growing

Count the software and services Nvidia actually sells and the edge AI market runs about $25 billion today, heading toward $119 billion by 2030

Robots and cars are its fastest growing slices, exactly where Jetson points, and Nvidia already leads both

It prints the money where AI gets trained, now it wants the layer where physical AI actually runs

To be fair, edge and robotics was barely 1% of revenue the last time Nvidia shared earnings, but that's because the market is early (and the data centre revenue is so big)

The more the edge business grows though, the more the data centre business will need to grow to support it.

At sub 20 forward earnings, $NVDA is a steal imo. I've been buying on dips and adding to my Milk Road portfolio. You can track this real-time portfolio along with 4 other analyst (see link in bio)

Follow me @kylereidhead for more insights AI, semis and robotics

Medicare just started paying for GLP-1 weight loss drugs for the first time and 2 of the 3 are Eli Lilly's

The bear case for $LLY was always "nobody can afford these drugs long term and Medicare doesn't pay for weight loss drugs"

That's changing

On July 1 the Medicare GLP-1 Bridge went live. Eligible Part D beneficiaries now get covered GLP-1 obesity drugs for $50 a month flat, no matter their income, with prior authorization, running through December 2027

KFF found 3.8 million Medicare beneficiaries already met the eligibility criteria (from 2023 claims data). That is a brand new patient pool that was priced out at list price

But more importantly, Eli Lillys newer drugs like Retatrutide are not only having even better effects on weight loss, but also on metabolic diseases.

This would open up the door to a much wider base of patients and even more funding from Medicare

Even better, Foundayo is live and it's one of the only GLP-1 pill for weight loss you can take any time of day with no food or water restrictions

A pill you take whenever you want is the one patients actually stay on, and staying on is the whole revenue model

So Eli Lillys best products are turning into even better products, in more accessible forms and its starting to get covered by insurance and medicare

Is there a better product in the world to sell? And none of this accounts for what happened when Eli Lilly succeeds at turning into an AI platform for the rest of the pharmaceutical and biotech industry.

Milk Road PRO members are up on $LLY after getting the call to buy its most recent dip. You can also get these calls for just $1 by joining Milk Road PRO.

There's 5 analysts inside where you can track their real-time portfolios and get live trade signals (see link in bio)

Eli Lilly is going much HIGHER and it has almost nothing to do with weight loss drugs (Save this)

Zepbound & Mounjaro are the reason the stock sits near ATHs

but the AI platform $LLY is building under the drug business is what matters

it started w/ Lilly Pod, a 1,000 GPU Nvidia Blackwell supercomputer at its Indianapolis HQ, the most powerful supercomputer owned by any pharmaceutical company on earth

In January 2026 Lilly and Nvidia committed $1 billion over five years to a new AI co innovation lab running on Nvidia's BioNeMo platform and Vera Rubin architecture

The lab pairs robotic wet labs with AI models in a closed loop: propose a molecule, synthesize it, test it, feed the result back in, and repeat at machine speed instead of human speed

The next wave is data:

Lilly CEO Dave Ricks has pointed out that Lilly alone holds data on roughly 3 million failed drug candidates, while the entire pharma industry has only ever produced about 4,000 approved drugs total

No AI startup training on public internet data can replicate 150 years of proprietary clinical and safety data like that. This is their moat in an AI world

And finally, wave 3 is about distribution:

TuneLab launched in September 2025, giving outside biotechs access to AI models built on over $1 billion of Lilly's proprietary drug discovery data through federated learning

Over 70 biotech partners are already on it

That is Lilly starting to look like infrastructure the rest of the industry builds on, closer to what AWS became for cloud computing than a normal drug company

Even better is that Eli Lilly is funding this bet entirely off cash flow from drugs that already work, Zepbound, Mounjaro, and the new oral pill Foundayo, so the AI platform is optionality stacked on top of a business that does not need it to succeed

The drug franchise is already crushing, the AI platform is the option most of the market has not priced in yet and what will take $LLY much higher

Follow me @kylereidhead for more analysis on AI, robotics and markets. Also, you can track my real-time portfolio (which includes $LLY) for just $1 at Milk Road PRO (see link in bio to join)

Everyone thinks Chinese open source models are killing OpenAI and Anthropic (they are wrong)

The US share of AI usage on OpenRouter fell from 70% a year ago to 30% today

But what people miss is that the entire token market is growing so fast that both sides are winning at once

OpenRouter went from around 5 trillion tokens a week in April 2025 to over 20 trillion a week a year later (4x in twelve months)

So even with the US share cut in half, the actual tokens flowing to OpenAI and Anthropic still went up (not to mention the use of these tokens within the platforms themselves, which both continue to gain adoption)

Part of the reason companies keep buying more tokens is that they are being subsidized, but it's also because they are finally paying for themselves

we've seen many examples of companies finding ROI with AI, the biggest example is the growth in Meta and Amazons ad business, which continues to improve and scale because of AI

companies will get smarter about their token usage, routing from frontier models to open source models and the better they get at this, the most tokens they will consume from both sides

They're both just going to keep growing and thats why the AI trade is still far from over.

We need WAY MORE COMPUTE!

Follow me @kylereidhead for more insights on AI, semis and the next big market themes

track my real-time portfolio at Milk Road PRO (link in bio)

Milk Road PRO analysts were super early to $MU, $BE, $NBIS and many more assets in this bull market

You can track our live trades and portfolios for just $1

Check it out here:

https://t.co/tsCY5Dq9IT

$NVDA just launched two new chips that push it into the one AI market it doesn't yet own (Save this)

Nvidia already owns AI in the data center

Now they're coming for edge, the chips inside robots and machines in the real world

The launch is two new Jetson Thor modules, the T3000 and T2000

They pack the same Blackwell architecture as Nvidia's flagship robot brain into about half the size and power, built to drop into mass market robots and edge devices at volume

And the market it's chasing keeps growing

Count the software and services Nvidia actually sells and the edge AI market runs about $25 billion today, heading toward $119 billion by 2030

Robots and cars are its fastest growing slices, exactly where Jetson points, and Nvidia already leads both

It prints the money where AI gets trained, now it wants the layer where physical AI actually runs

To be fair, edge and robotics was barely 1% of revenue the last time Nvidia shared earnings, but that's because the market is early (and the data centre revenue is so big)

The more the edge business grows though, the more the data centre business will need to grow to support it.

At sub 20 forward earnings, $NVDA is a steal imo. I've been buying on dips and adding to my Milk Road portfolio. You can track this real-time portfolio along with 4 other analyst (see link in bio)

Follow me @kylereidhead for more insights AI, semis and robotics

$NVDA grows 85%/year and trades at 19x forward earnings. It's one of the cheapest stocks in the market (save this)

Everyone thinks custom AI chips will eat NVIDIA alive

This JP Morgan chart shows where they are wrong

The bear case sounds smart: Google, Amazon and OpenAI are building their own chips, so NVIDIA's moat is cracking

Let's start with the left side of this chart

JPMorgan projects NVIDIA holds 90% of the AI training market through 2028. They own that market for years to come

The right side is where the bears think they have a point. NVIDIA start to lose market share to custom ASICS in the coming years (Sure, they are right)

But they are still wrong on where NVIDIA ends up

Inference chip revenue is compounding at 122% a year through 2028 while training grows at just 30%

So NVIDIA "losing share" means taking 40% of the fastest growing chip market instead of 46.5% of a much smaller one today

So NVIDIA's "shrinking" inference business is actually going to continue to grow incredibly fast.

Last quarter revenue hit $81.6 billion, up 85% year over year. Data center alone did $75.2 billion, up 92%. They're guiding to $91 billion next quarter with mid-70s gross margins (insane)

All while analysts are raising their 2027 expectations for AI capex...

Morgan Stanley just raised its 2027 and 2028 hyperscaler capex estimates to $1.23 trillion and $1.4 trillion, and Meta alone is spending up to $145 billion this year

NVIDIA is undervalued, plain and simple.

This should be one of the easiest holds in the market as long as you think AI compute demand keeps growing (which I do)

NVIDIA remains a big part of my portfolio, which you can track in real-time. every position and every move, inside Milk Road PRO for $1 (link in bio)

Milk Road PRO analysts were super early to $MU, $BE, $NBIS and many more assets in this bull market

You can track our live trades and portfolios for just $1

Check it out here:

https://t.co/tsCY5Dq9IT

$AAPL hit new ATHs today on China approvals for Apple Intelligence

I explained below why Apple is positioned to dominate in AI, specifically consumer agents

the one issue has been regulatory setbacks in Europe and China, which is now changing

Apple simply needs to use a Chinese AI model, Qwen from Alibaba

which makes sense and further solidifies my theory that Apple will become an aggregator of AI models. Routing to certain models based on costs, regulation, privacy, etc.

Something like 300m iPhones are in mainland China, so this is a huge unlock for Apple

Enabling Apple Intelligence in China offers a larger set of phones to push consumer agents to, which it looks more and more like Apple is going to win this category and have yet another massive revenue stream

This time taxing the entire agentic economy

Apple sits pretty here with no AI Capex, yet so much potential from AI. This is why I was buying Apple earlier this year in my Milk Road PRO portfolio

You can track my real-time portfolio for just $1 at Milk Road PRO (see my link in bio)

and make sure to follow me @KyleReidhead for more updates on AI, agents, robotics and markets!

Everyone thinks Apple is losing the AI race because it skipped the AI capex

But I think they are positioned perfectly to dominate AI (Save this)

In fact, Apple is the best performer of the Mag 7 YTD, so the market is starting to figure it out

I bought $AAPL earlier this year for the AI-demand device upgrade cycle, but I'm realizing they are positioned to dominate in something much bigger:

Consumer Agents

Apple just shipped App Intents, the framework that lets Siri take real actions inside any app, book something, buy something, complete a task, not just answer a question.

My bet is that consumers will want to just talk to their agents without actually touching their phone "hey Siri" rather than picking up their phone, opening it, clicking on chatGPT app and then talking/typing

Apple has a moat on devices with iPhone, Macbook and iPods. This is where consumer agents will be used.

And because Apple doesn't have their own AI, they can become an aggregator of AI's, similar to Openrouter. Routing to the cheapest/most efficient models depending on the task

plus, it can live locally on the device for privacy and speed.

So Apple has spent no money on AI, yet is sitting in the perfect position to be the winner of how consumers use AI agents on daily basis.

If Apple owns that layer, it gives them yet another (and likely one of their biggest) revenue streams. they become a platform that taxes the entire agentic economy, monetizing through tiered subscriptions and/or taking a cut of every transaction an agent completes inside the apps.

And not only that, if the Agentic economy takes off through Apple, it will force the largest device refresh in Apple's history.

Morgan Stanley says roughly 850 million iPhones can't run Apple Intelligence, and 1.3 billion can't run the new agentic Siri, out of about 1.4 billion active iPhones worldwide.

Now of course, Siri is still dumb, so they have not achieved this yet. But the potential and roadmap is there.

This is why I bought $APPL months ago and shared this with the members inside Milk Road PRO. I just shared a detailed update on my position inside the platform too.

You can track my real-time portfolio and get all my live updates for just $1 (see link in bio)

On July 6th, @ethereumJoseph came on @milkroaddaily and told me that there were a lot of very bullish things happening that he couldn't share publicly yet.

A week later, a new for-profit company called @eth_systems was launched to build institutional-grade privacy product solutions for institutions directly on Ethereum.

This is a continuation of the most important theme of this bear market.

Institutions have never been more bullish on Ethereum, and the fundamental value proposition of $ETH has never been stronger.

Meanwhile, retail sentiment is disastrous, and no one is paying attention.

This is why I've been calling this "bullish divergence."

Because once the market begins to understand the multi-trillion-dollar ecosystem that's rapidly coming to Ethereum, ETH is going to reprice violently higher.

There are between 200-300 million global mid-sized businesses that are currently leveraging the internet to conduct business.

What do you think happens when these businesses start using the products that ETH Systems builds and all of that activity migrates on-chain?

If you're in AI, pivot to crypto 🥛

Everyone thinks AI token consumption will slow down bc it's getting too expensive, they have it completely wrong

Goldman Sachs just projected the opposite, token usage grows 24x to 120 quadrillion tokens a month by 2030

Token costs have already fallen over 90% since 2023 and the drops keep coming

Grok 4.5 launched last week at $2 input / $6 output per million tokens, roughly 80% cheaper than Fable 5, and it's almost as smart

Enterprise token usage grew 1,001% from January 2025 to April 2026 while prices fell the entire time, and total dollar spend still grew 497%

Every price drop unlocks use cases that weren't economical the day before (this is Jevons Paradox playing out in real time)

And remember, usage today is still mostly people chatting and coding

The next wave of demand is agents

An agentic task burns 5 to 30x more tokens than a chatbot answer because agents loop, retry and chain calls on their own

There's another wave to follow which is autonomy in the physical world

Every humanoid robot and autonomous vehicle is a machine that consumes inference continuously, all day, with no human in the loop. Chat demand is capped by 8 billion humans, autonomy isn't capped by anything

the demand for intelligence is infinite and that's why AI Capex will continue to grow, not shrink. Semis, neoclouds and other bottleneck trades will bounce back as a result.

Follow me @kylereidhead for more insights on AI, semis and the next big market themes. You can also track my real-time portfolio for $1 at Milk Road PRO (link in bio)

Milk Road PRO analysts were super early to $MU, $BE, $NBIS and many more assets in this bull market

You can track our live trades and portfolios for just $1

Check it out here:

https://t.co/tsCY5Dq9IT

The AI trade just entered its mid-cycle reset and I think it's handing out the best entry points since the rally began!

Memory, power semis, Neoclouds, materials all sold off hard. The market reads that as the buildout cooling.

The supply chain shows demand still outrunning supply everywhere I look!

In the past two weeks alone (among others):

TrendForce forecast another 13-18% rise in conventional DRAM prices this quarter and 10-15% for NAND, while memory suppliers reportedly notified customers of increases as steep as 20-30% for DRAM and 35-40% for NAND.

SK Hynix now expects 2027 to bring the worst memory shortage in industry history, with customer demand exceeding its production capacity beyond 2030.

And the bottleneck is spreading beyond chips. US utilities are ordering transformers years in advance as lead times stretch past 160 weeks.

Meta signed multi-year memory, storage, and fiber agreements to lock in the components it needs to double its computing capacity by 2027.

The squeeze is also reaching downstream income statements too.

Ericsson for instance warned this week that AI-driven memory inflation is pressuring telecom-equipment margins.

To give you some more alpha, here are names I'm looking at during the consolidation phase:

$Q Complex chips consume more, and more expensive, specialty chemicals, packaging, and thermal materials.

$Infineon. Racks heading toward hundreds of kilowatts turn power conversion into a gating component.

For more names join Milk Road AI PRO 1$ trial to see what I'm buying (link in bio).