Iran’s senior official Mohsen Rezaee: “The war will continue until all damages are compensated, all economic sanctions are lifted, and a guarantee is obtained that the United States will not interfere in Iran’s affairs. This is the decision of our nation, our leader, and our armed forces.”

@Ksidiii Companies in the UK publish semi annually but they are not more volatile vs their European peers. I think this move will kill some of the dispersion pods.

@Ksidiii Call it regime shift might be exaggerated. With uncertainty goes up, thx to Trump’ intraday tariff policy, this just push VIX spot swings above/below front end future like crazy. So whoever use that as signal(without smoothing) got killed both ways.

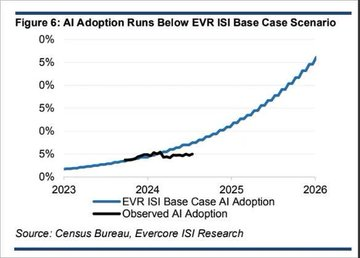

Equities are pricing in a boom in AI adoption, productivity gains, and corporate margin expansion. If that goes slower than expected, it's going to be hard to justify current forward earnings & multiples. h/t @TXMCtrades

https://t.co/585sqqaTid

It's time for an independent review with cross party support & concluding after the next election. Along the lines of the successful Turner Review which brought together a higher state pension age, earnings uprating (ie above inflation) & auto-enrolment

https://t.co/a9wHgwFJG7

This has now happened - UK wage growth back above inflation.

Having said that, clear signs (eg vacancies falling) that the UK labour market is cooling off which will reassure the Bank of England.

I have been surprised how low US long-term rates have remained in light of structural changes that are likely to lead to higher levels of long-term inflation including de-globalization, higher defense costs, the energy transition, growing entitlements, and the greater bargaining power of workers. As a result, I would be very surprised if we don’t find ourselves in a world with persistent ~3% inflation.

From a supply/demand perspective, long-term Treasurys (T) also look overbought. With $32 trillion of debt and large deficits as far as the eye can see and higher refi rates, an increasing supply of T is assured. When you couple new issuance with QT, it is hard to imagine how the market absorbs such a large increase in supply without materially higher rates.

I have also been puzzled as to why the @USTreasury hasn’t been financing our government in the longer part of the curve in light of materially lower long-term rates. This does not look like prudent term management in my opinion.

Then consider China’s (and other countries’) desire to decouple financially from the US, YCC ending in Japan increasing the relative appeal of Yen bonds vs. T for the largest foreign owner of T, and growing concerns about US governance, fiscal responsibility, and political divisiveness recently referenced in Fitch’s downgrade.

So if long-term inflation is 3% instead of 2% and history holds, then we could see the 30-year T yield = 3% + 0.5% (the real rate) + 2% (term premium) or 5.5%, and it can happen soon. There are many times in history where the bond market reprices the long end of the curve in a matter of weeks, and this seems like one of those times.

That’s why we are short in size the 30-year T — first as a hedge on the impact of higher LT rates on stocks, and second because we believe it is a high probability standalone bet. There are few macro investments that still offer reasonably probable asymmetric payoffs and this is one of them.

The best hedges are the ones you would invest in anyway even if you didn’t need the hedge. This fits that bill, and also I think we need the hedge.

Great to chat to East West Rail in #Bicester today about the vital London Road crossing.

I'll be working closely with @VictoriaPrentis as new plans are developed - we can't allow our town to be cut in half, and any new proposals need to work for local residents.