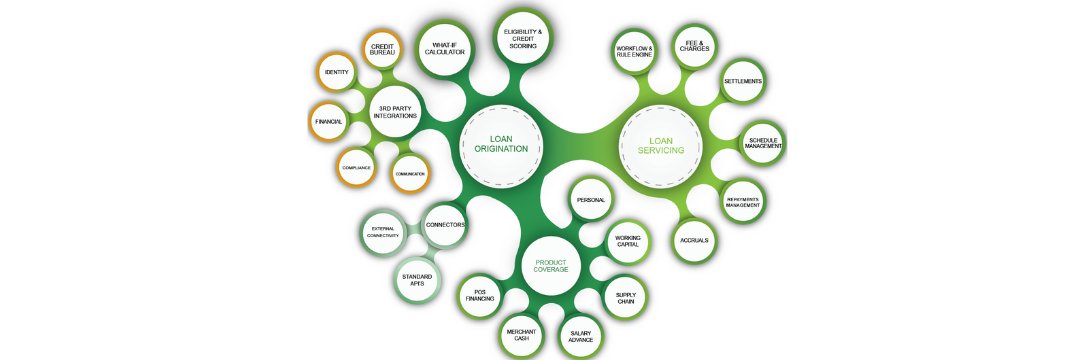

AI doesn't solve fragmented lending operations on its own.

Workflow orchestration and connected systems are what make AI scalable. https://t.co/c3TsXUfiHY

#AILending#DigitalLending#WorkflowAutomation

Manual approvals and disconnected processes create lending bottlenecks that don't scale.

Leading lenders are building workflow-driven operations. https://t.co/w8gJm0QFOd

#DigitalLending#LoanOrigination#WorkflowAutomation

POS lending is no longer just a checkout feature.

It’s becoming core lending infrastructure.

Scalable POS lending depends on coordinated underwriting, servicing, integrations & operational control.

https://t.co/8SZNMWlarl

#POSLending#EmbeddedFinance#DigitalLending

Working capital lending rarely breaks on demand.

It breaks on fragmented workflows, inconsistent underwriting & weak servicing visibility.

Scalable lending needs coordinated operations.

https://t.co/xnxYI2Syap

#WorkingCapital#DigitalLending#CreditRisk

Working capital lending rarely breaks on demand.

It breaks when operational responsiveness can’t scale with volume.

Strong lenders coordinate underwriting, servicing & workflows before bottlenecks appear.

https://t.co/MQN8tE3Yyt

#WorkingCapital#DigitalLending#Fintech

Lenders don’t lack data.

They lack operational control.

Modern lending analytics turns fragmented signals into real-time decisions across risk, servicing & portfolio management.

https://t.co/Dlph93BQ0O

#BusinessAnalytics#DigitalLending#Fintech

Working capital lending rarely breaks on demand.

It breaks on coordination.

Scalable lenders align origination, servicing, decisioning & risk into connected workflows—not fragmented systems.

https://t.co/rJaxgCvmMp

#WorkingCapital#DigitalLending#Fintech

Credit reporting issues rarely start at reporting.

They begin with fragmented servicing, inconsistent updates & poor operational coordination.

Reporting accuracy depends on aligned workflows.

https://t.co/yF3wLg0TGo

#CreditReporting#LoanServicing#Fintech

Lending friction rarely starts at approvals.

It appears later—across underwriting, servicing, compliance & borrower workflows.

Scale needs orchestration across the full lending journey.

https://t.co/5hGVL2ZFcu

#DigitalLending#WorkflowAutomation#Fintech

Hard money lending scales on control—not speed alone.

As portfolios grow, manual oversight creates risk across collateral, disbursements & servicing.

Strong systems embed discipline directly into workflows.

https://t.co/ZiOaKOuUZa

#HardMoneyLending#DigitalLending#CreditRisk

SME lending challenges rarely start with demand.

They start with operational friction—manual underwriting, fragmented workflows & delayed approvals.

Scale needs coordination, not just speed.

https://t.co/dpR88o5Bj6

#SMELending#DigitalLending#Fintech

Lenders don’t lack data.

They lack coordinated visibility.

Modern analytics platforms surface risk, servicing trends & bottlenecks in real time—turning data into operational control.

https://t.co/4NxrfvAvwR

#BusinessAnalytics#DigitalLending#Fintech

Collections issues rarely start at recovery.

They begin with fragmented servicing, poor visibility, and disconnected workflows.

Strong servicing resilience starts before pressure escalates.

https://t.co/MYoiIsC6yw

#CollectionsManagement#LoanServicing#DigitalLending

High-volume lending doesn’t scale through efficiency alone—it scales through infrastructure.

Cloud-based platforms reduce manual ops, streamline workflows, and support growth without added complexity.

https://t.co/9MaxwGWZln

#DigitalLending#CloudComputing#Fintech

Equipment finance isn’t just a growth lever—it’s a structural risk advantage.

Asset visibility, lifecycle alignment, and cash-flow-based structuring are reshaping portfolio performance.

https://t.co/o2ShK3JWbh

#EquipmentFinance#AssetBasedLending#Fintech