Perhaps a contrarian thought but is the reason we are still seeing so much money sloshing around VC (namely the mega multi stage funds) based on strategic access sought by certain LPs (namely sovereign wealth funds) rather than purely profit seeking? #VentureCapital#vc

@lessin@JTLonsdale Can we get a merit based test for legal too? At a corporate boutique firm, always hard to screen for true talent when all we see are resumes with white shoe law firms / T14 law schools.

THE COMING SOFTWARE M&A WAVE

Software private equity investor here. I've talked to 53 software founders in the last 3 weeks (can't believe that's a real number).

After these conversations, I have a new take that a lot of M&A might be coming to software...and not necessarily in the most optimistic way.

First things first: after 53 conversations with founders of $5mm+ ARR businesses, here are some observations:

-Founders are seriously in a tough place due to large rounds raised in 2020/2021/2022

-Founders routinely say they are having problems growing

-Founders are routinely saying they had to hard pivot to break even because the next raise isn't guaranteed.

-Founders pivoted to break even maybe too quickly, and now growth has slowed

-Couple that with the fact that software is LITERALLY harder to sell now (13 touch points to 30 touchpoints for a close)

-Existing customers are playing hardball on expansion/existing ACV. Net retention becoming a bit tricker.

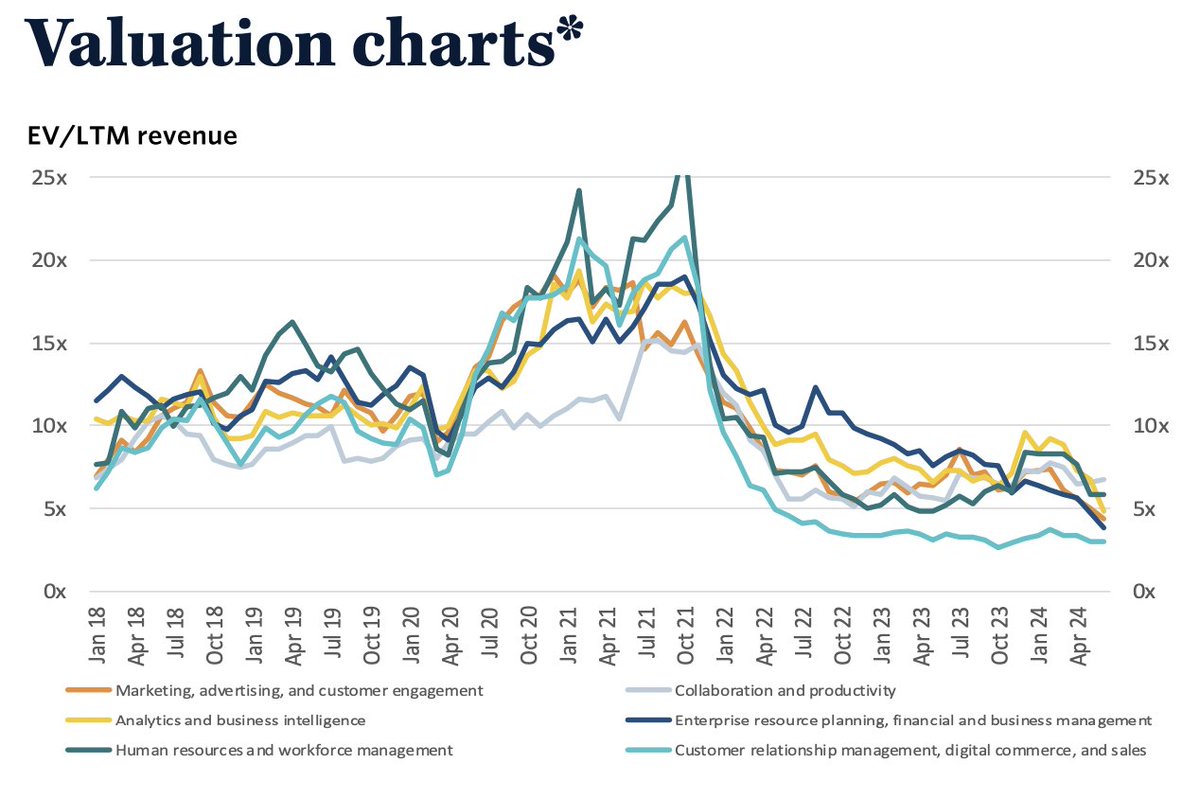

Finally, founders keep telling me they will sell for 6-8x ARR. Well, what does the public market think about that? Below, you'll see a graph that shows ARR Multiples (EV/LTM Rev) for public companies.

If expensify and other large PRETTY SCALED saas are trading <5x ARR, how are you supposed to command that value? Back in 2021 some of those businesses were trading at >20x ARR (!!!)

So, why will there be a wave of M&A? There are SO many venture funded SAAS businesses that have decelerating growth and busted cap tables. Eventually, they will realize they are kinda 'stuck', and they will have to sell.

They will go to market and realize that there are very few bids >5x ARR, their growth is in trouble, there's no more VC money, and the choice will become obvious. Finally, couple that with the private equity data I will show below, and 30% of bidders simply can't pay what they used to for software businesses. The main people preventing these talented CEOs from selling? The VCs who don't want to book a loss. Irony abounds.

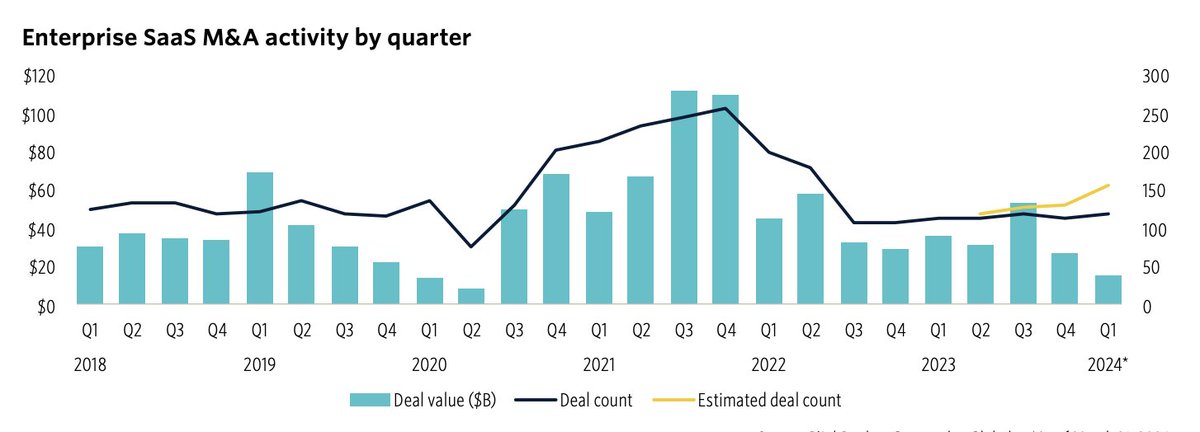

Now, let's move to software PE as a whole, who I also think will be forced to sell at sub optimal prices. Time for a short history lesson on M&A in software PE. 2021/2022 were INSANE. In the graph below, you'll see that total deal values were tremendously elevated and deal counts were almost off the page. Software PE went on a SPENDING SPREE. Fast forward to today, and what does the data show: the average disclosed deal value in Q1 2024 was $202.4 million, significantly lower than the $398.9 million average in Q1 2023. Oof.

However, what's more interesting, is that while deal counts have rebounded, the total value of those deals is DRAMATICALLY lower. Deal values are coming in MUCH lower. Why? Well the public markets (in the image above) tell the story. Software PE bought these companies at elevated valuations and now the public markets are screaming: 'THESE AREN'T WORTH AS MUCH AS YOU THOUGHT THEY WERE BUDDY'. They can't IPO them, and they can't easily sell them. The market for 200m+ ARR businesses is a lot smaller than you might think. This also impacts the tinier SAAS businesses as one of their potential buyers is having their own issues.

The crazy part? PE funds will HAVE to sell soon or roll them into continuation funds. That's another fun part of the narrative.

I'm a value based software investor. If you know of anyone with >$10mm arr willing to sell who wants off the treadmill, I'm happy to have a conversation. Anyway, shameless plug over.

Summation:

-VC backed software companies are having trouble growing and have slightly busted cap tables.

-PE funds that bought in 2020/2021 are going to have a tough next few years unless public market comps recover (who knows)

-Sell me your >$10mm ARR SAAS business :)

***Data from Pitchbook's Enterprise SAAS M&A report and Enterprise SAAS Public Comps report

Legacy Silicon Valley Wealth Management + Premier Alternative Investment Manager joining forces to scoop up cheap secondaries of former VC darlings. Should be fun to watch!

https://t.co/nbDg1pO2Oi

@WSJ The next year + will see strategics buy equity in the secondary market at decent “value” prices again and again as the crossover funds such as Tiger, Coatue, etc. continue with a need to provide some modicum of liquidity to their LP.

12 year old post but still rings true today on why we need fractional reserve banking. Society cannot prosper without collective risk taking, an activity that wouldn’t be taken if everyone knew the risks. Banks play the ever important intermediator.

https://t.co/rbeO6hPs8i

But all seriousness, the Fed likely announce Monday (probably before market open) that they are buying out SIVB’s MBS and holding to maturity as a solution to the issue. Depositors made whole and equity vaporized. Doubt they allow major boutique bank to fail and start contagion.

Who would have thought that funding risky venture debt (particularly in the economic climate we’ve been in for the past year+) with customer demand deposits would create a huge asset / liability mismatch! They say the third criteria for a black swan is it’s obvious in hindsight…

@Samirkaji Any idea if the SVB “Sweep Accounts” have a higher insurance limit under SIPC? Or if those accounts are held in trust and then payable to the ultimate beneficiaries (I.e. the depositors)?

We had a great dinner in Park City with our client @AtlasRTX and Leonis Partners last week. We always appreciate the opportunity to get together in person! @BassamSalem@JennRosenthal@logan_desouza

A lot of newsworthy layoffs have happened recently at big, well-known companies that attract a lot of media coverage — this turns out to be a very bad guide to the state of the labor market, and could actually be useful in steering toward a soft landing.

https://t.co/Na49MZzOtS