@JunkSavvy@FINRA is it possible Finra will change the FAQ's to acknowledge #NBH was never going to trade from the begining and you guys made a glitch to think or write that #NBH might trade in the future? Asking for the captured #SEC.

@SECGov@SECPaulSAtkins ENFORCE THE LAW!!!

SECURITIES & EXCHANGE ACT 1933 (Rule 15c3-3(d)): "Not later than the next business day (as of the close of the preceding business day), a broker-dealer must review its books and records to determine the quantity of fully paid and excess margin securities in its possession or control versus those not in possession/control.

If there is a deficiency, the firm must take prompt action (e.g., issue instructions to release securities from liens or recall loaned securities) to bring them under control within specified timeframes (typically 2–5 business days depending on the situation)."

1300 DAYS!!!

Did you know???...

Settlement times on share purchases direct to accredited investors are governed by a definitive contract. The shares officially settle on the specific "Closing Date" defined in the agreement once all conditions are met....

You know what that means???...

Accredited investors must have closing dates and contracts executed by July 8, 2026, close of business in order for those shares to be eligible for the 30:1 dividend...7 DAYS!!!

TIK TOK

TRCH/MMAT Rev Merge..."OCC" "OCC" "OCC"

MMTLP/NBH Spin-off..."FINRA" "FINRA" "FINRA"

SEA 15c3-3..."Shares not available"

S-1 Effective...NO MORE EXCUSES!!!

NBH 30:1 Divi...New Crime = New Statute of Limitations

TO BROKERS: Buy the f'ing shares!!!

TO SEC: Enforce regulations...IT'S THE LAW!!!

July 8, 2026...Record (contracts executed)

Date July 22, 2026...Distribution

TIKTOK MF'ers!!!

MMTLP MMAT TRCH NBH

You cannot stop what is coming...#FAFO

@SecScottBessent@USTreasury@FBIDirectorKash@DOGE@timburchett@SECGov@SECPaulSAtkins

📣📣SEC IS VERY WELL AWARE THAT MARKET MANIPULATION HAS EXPONENTIALLY GROWN

In the last decade, the SEC says market manipulation cases have statistically grown 37%

They can't hide it anymore it's blatantly happening, and the SEC is turning a blind eye.

Many companies are taking legal action to protect the company and their fiduciary responsibility to protect their shareholders.

📣📣SEC IS VERY WELL AWARE THAT MARKET MANIPULATION HAS EXPONENTIALLY GROWN

In the last decade, the SEC says market manipulation cases have statistically grown 37%

They can't hide it anymore it's blatantly happening, and the SEC is turning a blind eye.

Many companies are taking legal action to protect the company and their fiduciary responsibility to protect their shareholders.

📣📣MMAT MMTLP BANKRUPTCY CASE DOING THE SEC JOB

The Trustee is doing what the SEC should have done years ago. INVESTIGATING WHAT HAPPENED WITH MMAT MMTLP NBH

The SEC has subpoena power, but instead of investigating, they ignored all the victims and covered up the crime.

Just one Hedge Fund admitted to owning MILLIONS of short shares, far exceeding historically reported public short figures.

The Trustee and Judge in the bankruptcy case are a blessing 🙏

📣📣MMAT MMTLP BANKRUPTCY CASE DOING THE SEC JOB

The Trustee is doing what the SEC should have done years ago. INVESTIGATING WHAT HAPPENED WITH MMAT MMTLP NBH

The SEC has subpoena power, but instead of investigating, they ignored all the victims and covered up the crime.

Just one Hedge Fund admitted to owning MILLIONS of short shares, far exceeding historically reported public short figures.

The Trustee and Judge in the bankruptcy case are a blessing 🙏

@stephmase22 It’s not even funny anymore, these MF’s can just get away with anything and no one holds them accountable. I’m so FKn mad. These FKs need to be in jail for life and I mean max security not some white collar country club low security either that or find a tree and get a rope. 🤷🏼♂️

I believe it was a "GROUP of MEMBERS [brokers]"....

TRCH/MMAT Rev Merge..."OCC" "OCC" "OCC"

MMTLP/NBH Spin-off..."FINRA" "FINRA" "FINRA"

SEA 15c3-3..."Shares not available"

S-1 Effective...NO MORE EXCUSES!!!

NBH 30:1 Divi...New Crime = New Statute of Limitations

TO BROKERS: Buy the f'ing shares!!!

TO SEC: Enforce regulations...IT'S THE LAW!!!

July 7, 2026...T+1

July 8, 2026...Record Date

July 22, 2026...Distribution

TikTok

MMTLP MMAT TRCH NBH

You cannot stop what is coming...#FAFO

@SecScottBessent@USTreasury@FBIDirectorKash@DOGE@timburchett

Check our the list below (Link) with the top 15 Global Markets and how they compare with FINRA on accountability

In practical effect, FINRA operates a coercive private regulatory scheme:

- access to the US securities markets is conditioned on submitting to FINRA’s rules, investigations, and disciplinary process.

- But when FINRA abuses that power or fails in its oversight, investors and member firms are told that FINRA is beyond reach because of judge‑made ‘absolute’ immunity for its regulatory acts and omissions...

Source for full report: https://t.co/x23gdntcsu

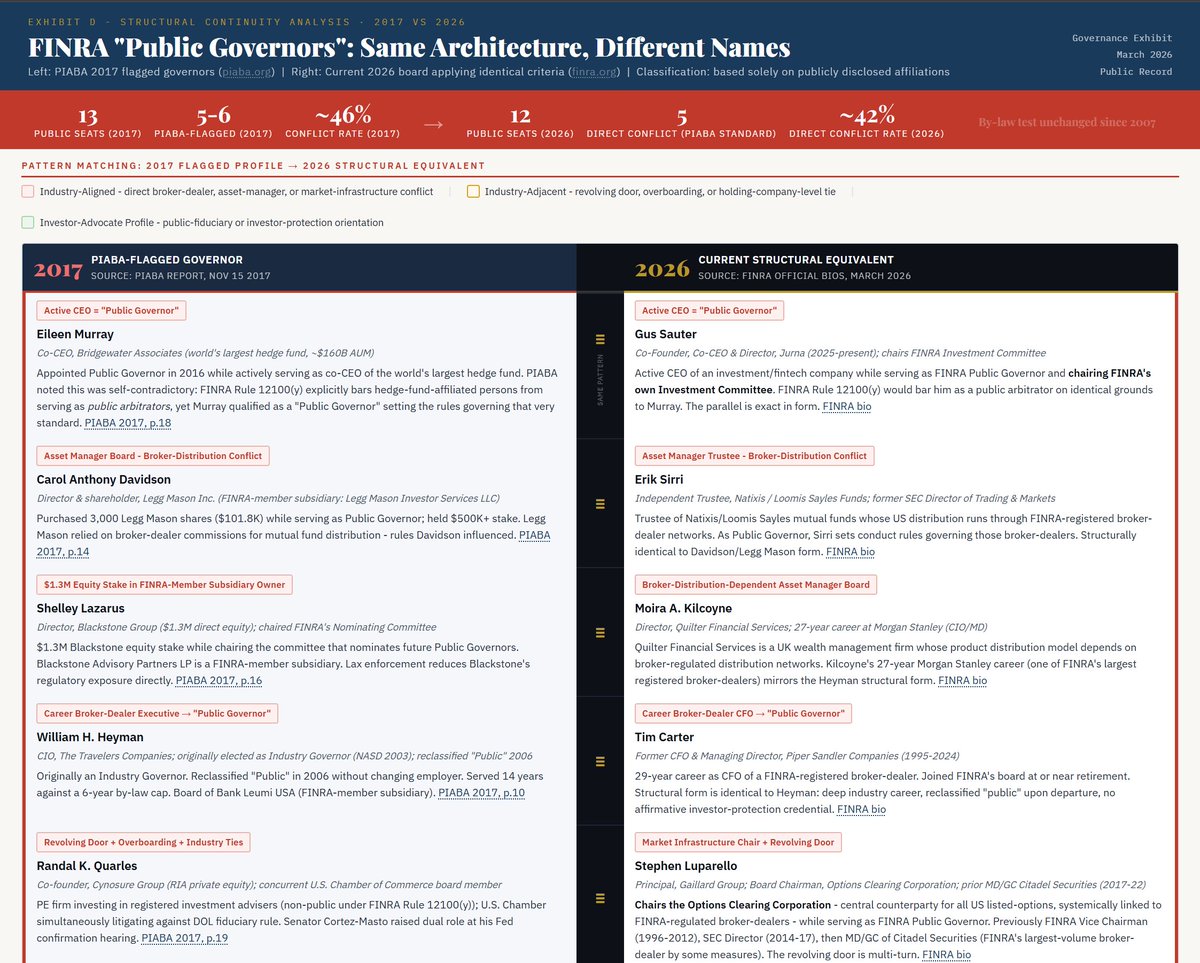

In 2017, The Public Investors Advocate Bar Association @PIABANews published some interesting stats about FINRA's Board of Governors and their conflicts of interest.

What did PIABA find in 2017?

PIABA’s 2017 report identified 5–6 of 13 “public” governors with material ties to FINRA member firms, asset managers dependent on broker distribution, or industry‑funded lobbying groups, plus serious “overboarding” concerns.

Source: https://t.co/WYq9EYTKi8

Examples from PIABA:

-William Heyman (Travelers CIO, Leumi board),

-Carol Anthony Davidson (Legg Mason director and significant shareholder),

-Shelley Lazarus (Blackstone director, Ogilvy/FINRA campaign work),

-Joshua Levine (Kita Capital, Fantex ties),

-Eileen Murray (Bridgewater co‑CEO), and

-Randal Quarles (Cynosure, Chamber of Commerce).

What’s changed structurally since 2017:

1. Board size and mix: FINRA now describes a 22‑member board, with a majority of public seats (currently 12 public, 10 industry plus CEO), versus 24 members and 13 public seats in the period PIABA studied.

2. Process tweaks: recent notices emphasise the nominating process, term limits (two consecutive three‑year terms), and “variety of backgrounds” for public governors, but the by‑law test of “no material business relationship with a broker or dealer or other SRO” is unchanged.

3. Transparency: FINRA now lists current governors and committee roles on its site in more detail than pre‑FINRA360, consistent with what PIABA pushed for.f

Current public governors and likely conflicts (PIABA‑style lens)

FINRA’s current public governors list (as of March 2026) includes individuals such as:

Fabiola Arredondo – private investment firm principal (Siempre Holdings), ex‑media/tech executive; likely extensive issuer and financial‑sector exposure.

Deborah Bailey – retired; former senior banking regulator/Big‑4 advisor (based on typical background for this name in prior years; FINRA bio indicates retirement and prior regulatory/consulting roles).

Rostin “Russ” Behnam – former CFTC chair, now at Bloomberg; deep derivatives‑market/regulatory background and current senior role at a major data/markets vendor.

Tim Carter – former CFO and MD at Piper Sandler (mid‑market investment bank); strong historical industry alignment.

Dan Gallagher – Chief Legal/Compliance Officer at a major broker‑dealer/platform (current role cited in his appointment release), and former SEC Commissioner; clearly an industry‑aligned seat even if classified as “public"

Heather Traeger – General Counsel/CCO of a large public pension or asset‑management complex (per appointment release), whose funds rely heavily on broker‑dealer and dealer‑bank distribution.

Stephen Luparello – former SEC Director of Trading and Markets and former SRO/industry counsel; revolving‑door regulator background.

Derrick Roman – retired PwC partner; long‑time auditor of banks, asset managers, and broker‑dealers.

Gus Sauter – former Vanguard CIO; deep buy‑side/asset‑management ties, and long experience with distribution through broker‑dealers.

Erik Sirri – former SEC Trading & Markets Director; academic/regulatory profile with heavy market‑structure exposure.

Plus several other public governors with similar profiles listed on FINRA’s page; the pattern is consistent: ex‑regulators, asset‑management executives, major‑issuer directors, Big‑4 partners, and market‑infrastructure executives rather than investor‑side advocates.

If we apply PIABA’s 2017 tests and criteria, counting as “conflicted” any “public” governor who:

1. Serves on boards or in C‑suite roles at financial firms with FINRA‑member subsidiaries or that rely on FINRA members for product distribution.

2. Holds significant equity stakes in such firms.

Is heavily “overboarded” across multiple large financial‑sector boards.

3. Has current senior roles at large industry trade participants or vendors whose revenue depends on member‑firm activity.

-then several current “public” governors (e.g., Carter, Gallagher, Sauter, Behnam, Roman, Traeger, and any others with similar roles) would almost certainly be coded as “industry‑aligned public governors” rather than genuinely independent or investor‑protection‑oriented.

In other words, the specific names have changed, but the type of public governor has not:

the “public” column is still dominated by people whose careers and economic interests are closely intertwined with broker‑dealers, asset managers, banks, and market‑infrastructure firms, not by people whose primary identity is investor‑protection advocacy.

Below is a side‑by‑side table, the 2017 PIABA sample vs 2026 board, classifying each public governor as “investor‑advocate‑oriented” or “industry‑aligned” using PIABA’s own criteria.

As you can see “nearly half” remains true in our latest FINRA updated list of Governors.

Source for full report: https://t.co/9zq2PySPa5

Will FINRA finally be forced to answer certain questions about the $MMTLP trading halt?

“…. Kelly is forcing the court to decide this first:

👉 “Was this within FINRA’s delegated authority?”

Only AFTER that can immunity even be considered.

💥 This blocks FINRA from getting the case dismissed early….”

@kimkep4796

MMAT TRCH

Check out these docs @annvandersteel

There’s something deeply revealing (and disturbing) about a regulator arguing three things at the SAME time:

1) “Producing the data would be too burdensome”

2) “Even if we produced it, it wouldn’t identify anyone”

3) “We need to seal the identity of the person saying all this”

So let’s pause.

Dear @FINRA:

You oversee market integrity.

You investigate trading activity.

You halt securities.

You call this oversight⁉️

To everyone:

How can a market be regulated if the regulator cannot, AND will not, identify the participants behind the activity it claims to oversee?

That is not a discovery dispute anymore.

The system is describing its own limits under oath.

What this implies, structurally:

1. Surveillance exists WITHOUT full traceability!

2. Data exists WITHOUT actor-level resolution!!

3. Responsibility is distributed across layers, but accountability is NOT reconstructible from within ANY single layer!!!

4. Critical datasets (CAT, clearing, prime brokerage) are functionally SILOED!!!!

Strategic Interpretation in my humble opinion:

If a regulator cannot, or will not, identify participants behind market activity, then either:

1. The system is NOT designed to resolve attribution end-to-end, OR

2. The relevant data sits OUTSIDE the regulator’s accessible perimeter and control (which begs the question who has real access and control), OR

3. The integration layer between surveillance and accountability is INTENTIONALLY incomplete

All three lead to the same conclusion:

FINRA has a structural blind spot, not a one-off limitation.

The system looks completely corrupt.

@FINRA 's MMAT recent BK response/filling (March 27th) states an estimated 2.5 terabyte of trading data for #MMAT / #MMTLP.

They called this BURDENSOME.

At first glance perhaps this may look like a big, scary dataset... But lets take a closer look...

I found an enlightening video from an @AWS 2023 event and sharing below, "Exhibit A", in FINRA's own words (that's the fun part): https://t.co/8nN0fRNZL9

The main topic of this video is FINRA CAT's (Consolidated Audit Trail) journey in managing massive data volume and complexity, specifically how they transitioned from traditional Big Data to a massive exabyte-scale architecture on AWS to ensure market integrity and regulatory compliance (0:01-3:58).

The speakers in this presentation are:

- Leah Crawford: Principal Customer Solutions Manager with AWS (0:05)

- Scott Donaldson: Chief Technology Officer of FINRA CAT (1:26) and

- Steven Diamond: Senior Director of FINRA CAT engineering and operations (1:33)

The video highlights several ways FINRA CAT ensures data integrity:

1. Semantic Validation: The system runs semantic validations as data is received to ensure the accuracy and quality of the submission (11:30 - 11:35).

2. Feedback Mechanism: CAT identifies errors and incongruities in the data and reports them back to the firms, allowing them to correct and resubmit data (11:35 - 11:45).

3. Source of Record: Amazon S3 is used as the ONLY source of truth for data storage, ensuring security and resilience (12:03 - 12:12).

4. Linkage Processing: The system processes data to piece together the ENTIRE lifecycle of an order, which helps identify missing records or issues across.

According to the video, FINRA CAT is responsible for building a single source of TRUTH for all U.S. equity and options trading data. This data is made available to the SEC, FINRA, and other regulatory organizations to identify fraudulent or manipulative activity (38:07 - 39:29).

According to the video, FINRA CAT handles LATE trade reports by allowing firms to submit them at ANY point over the reporting horizon, which can span multiple YEARS (9:22 - 9:28). The system is designed to manage this data skew, as they have received trade reports for over 800 different trade dates on a SINGLE day (9:28 - 9:35).

QUESTIONS:

1. The math basically seems to suggest that FINRA can deliver 2.5 terabyte of CAT data by LUNCH today... that is about 2.5 to 2.7hrs of work done by a computer. Do you think this is BURDENSOME?

2. why would does FINRA allow trade reports to be filed late?

3. What happens when one of their members files their report late for e.g. by 1 month or by 10 years (yes actual cases)? Are the two late cases treated the same?

4. If a firm files late (or hasn't filed yet) how is compliance enforced? What are the current stats for missing reports, and why do firms keep ignoring their duty to file.

5. You discuss in the video how the FINRA CAT system was designed to manage and receive trade reports for over "800 different trade dates" on a SINGLE day. Do you still believe that the Trustee's request for 161 trading dates for just a couple of stock symbols is BURDENSOME?

#MarketIntegrity

![JunkSavvy's tweet photo. I believe it was a "GROUP of MEMBERS [brokers]"....

TRCH/MMAT Rev Merge..."OCC" "OCC" "OCC"

MMTLP/NBH Spin-off..."FINRA" "FINRA" "FINRA"

SEA 15c3-3..."Shares not available"

S-1 Effective...NO MORE EXCUSES!!!

NBH 30:1 Divi...New Crime = New Statute of Limitations

TO BROKERS: Buy the f'ing shares!!!

TO SEC: Enforce regulations...IT'S THE LAW!!!

July 7, 2026...T+1

July 8, 2026...Record Date

July 22, 2026...Distribution

TikTok

MMTLP MMAT TRCH NBH

You cannot stop what is coming...#FAFO

@SecScottBessent @USTreasury @FBIDirectorKash @DOGE @timburchett](https://pbs.twimg.com/media/HMHHoO0bUAAra10.png)