Buffett’s Goodwill Lesson

When $BRK bought See’s Candies in 1972, the numbers looked strange on paper. Berkshire paid about $25m for the business, but the tangible net assets were only around $8m. That meant roughly $17m had to be recorded as goodwill.

Goodwill is the extra money a company pays when it buys another company above the value of its assets. Things like brand name, reputation, and customer relationships.

Accounting rules at the time said goodwill had to be amortized over 40 years. Every year Berkshire had to run an accounting charge through the income statement that made earnings look artificially lower.

On paper it looked like value was disappearing. In reality the opposite was happening because See’s turned out to be one of the most extraordinary businesses $BRK ever bought. It required very little capital to operate and it produced steady profits. The brand, the customer loyalty, and the pricing power allowed the business to earn far more than the assets on the balance sheet suggested.

That difference is what Buffett calls “economic goodwill”. Accounting goodwill slowly shrinks every year because accountants force you to write it down. Economic goodwill can grow enormously if the business is great, and See’s proved that point perfectly.

The company started with about $8m of tangible assets and produced millions of dollars in earnings every year. Over time Berkshire was able to raise prices, maintain customer loyalty, and keep the capital requirements extremely low.

And that leads to the real insight. Most businesses are not limited by demand, they are limited by capital. A steel mill might have enormous demand for its product, but every time it grows it needs to build another factory, buy more equipment, hire more workers, and finance more inventory. Growth requires more capital.

But businesses with economic goodwill grow very differently. Demand increases, prices rise, profits expand, and the capital required to support that growth barely changes.

This is why inflation destroys capital intensive businesses. Factories, equipment, inventory, GPUs, logistics networks and warehouses all become more expensive over time. To maintain the same level of output those businesses constantly have to pour more money back into themselves.

But businesses like See’s operate differently because they rely on intangible assets such as brand, habit, and customer perception. When inflation increases prices they can raise prices without needing to build new factories or warehouses. The result is that much of the additional revenue flows straight to the bottom line.

This leads to a counterintuitive idea that many investors still miss. Investors often feel safer owning businesses with lots of assets. Factories, land, machines, inventory because they feel tangible and real. But paradoxically those assets are often the problem. They constantly need to be replaced, repaired, expanded, and financed. The greatest businesses in the world are often the ones with the fewest physical assets.

This is why Buffett eventually moved away from buying statistically cheap businesses loaded with assets. Instead he started searching for companies with strong brands, durable competitive advantages, and the ability to raise prices without needing heavy reinvestment.

That insight later led to investments in companies like $KO and eventually $AAPL. These businesses do not dominate because they own the most factories. They dominate because of brand, ecosystem, habit, and customer loyalty.

Those are all forms of economic goodwill. Once you understand this idea, you start to see businesses differently. You stop asking how many assets a company owns and start asking a far more important question.

How little capital does this business actually need to produce extraordinary profits? The greatest businesses in the world do not grow because they own more assets, they grow because they need fewer.

🌹

"To think that I've wasted years of my life, that I've longed to die, that I've experienced my greatest love, for a woman who didn't appeal to me, who wasn't even my type!"

"I think you have tactical wokeness in service of statecraft." This is an important exchange I had with @ggreenwald tonight on USAID. I went over Wokeness vs Blobness, and why **the Republican** wing of NED funds transgender dance festivals, ethnic identity events and rap groups

>Be Nissan, ticker 7201.

>It’s the year 2000 and you’re about to go bankrupt.

>Year 2001 name your foreign COO as CEO to promote being a global company but keeping a mostly Japanese board to exercise the real control.

>The foreign CEO is actually excellent, a working machine, cuts costs dramatically, not only saves but turns the company around and creates one of the best global automobile alliances to date in two years!

>The foreign CEO becomes an international celebrity and corporate hero.

>Nissan is Japanese, and Japanese management don’t like that.

>Decide to get rid of the foreign CEO who’s taking the spotlight from the Japanese management.

>CEO won’t leave, actually gets stronger. Finally forced to step down in 2017.

>Nissan decide to accuse him of serious crime and get him jailed in 2019, just to be on the safe side.

>Foreign CEO who saved Nissan escapes inside a musical instrument box, becomes an international criminal and a refugee in his own country thanks to your strategy to get rid of him.

>It’s the year 2024 and you’re still Nissan, and you’re about to go bankrupt…

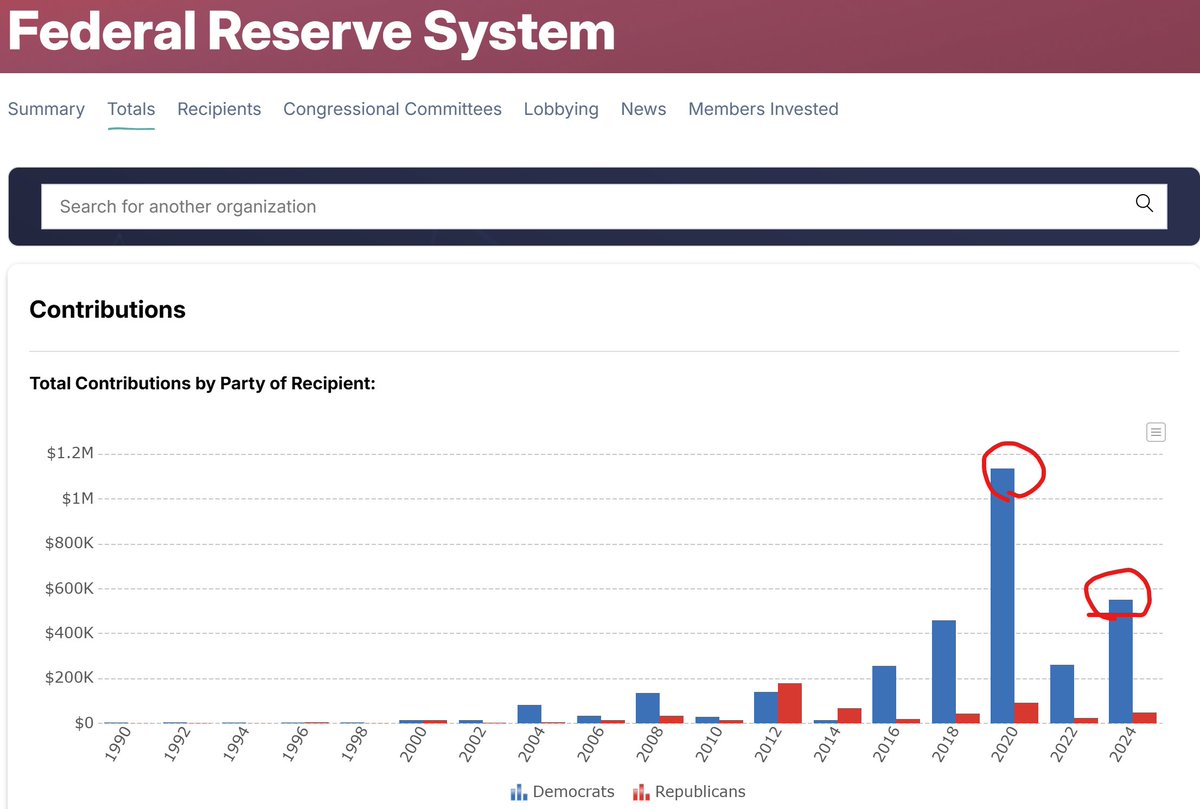

All this pearl clutching about Fed independence is nonsense. Fed is not independent, it is basically a branch of the Democratic party. You can see this in many ways.

1) Political donations by Fed employees overwhelming go to the Democrats.

2) Former FRBNY president is comfortable writing columns suggesting Fed conduct policy against Trump.

3) Former Fed Chair and Fed Vice Chair just sliding into senior roles in the Biden White House.

4) Fed Chair happily supporting Biden fiscal policy, then feigns ignorance afterwards.

5) Fed making moves on political issues like climate regulations for banks.

6) Fed staff pumping research on climate change and DEI stuff that just aren't in their mission.

I think the Fed would better serve the public if it were more politically balanced.