A big pivot from Ken Griffin on AI:

“Number one is, in the last few months, there has been a step change in the productivity of the AI toolkit. It is profoundly more powerful than it was just nine months ago.

And for us at Citadel, that has allowed us to unleash a much broader array of use cases for AI. And it has been really interesting to watch, to be blunt, work that we would usually do with people with masters and PhDs in finance over the course of weeks or months being done by AI agents over the course of hours or days.

These are not these are not mid-tier white collar jobs. These are like extraordinarily high skilled jobs being, I'm going to pick a word, automated by agentic AI. And I gotta tell you, I went home one Friday actually fairly depressed by this because you could just see how this was going to have such a dramatic impact on society.

When you witness it in your own four walls, when you see work that used to be man years of work being done in days or weeks, it's like, wow, like that's the first time I've seen real impact in our four walls.”

This echoes my own experience with agents and the conversations I am having with students, friends & clients. The toolkit has dramatically transformed and it feels like in finance, for the first time, AI is real.

Isn’t it shameful how these unions always seem to hold travelers and employers/visitors hostage at the worst possible times? First the LIRR strike threat ahead of Memorial Day, and now the hotel union threatening a strike ahead of the World Cup, just as tens of thousands of international visitors are expected in NYC.

https://t.co/2bsZLWCUL4

Thousands of high paying highly taxed jobs - money the city sorely needs. And don’t forget the income the city’s now going to miss out on from all the knock-on/adjacent spending (real estate taxes, dining, entertaining etc etc etc). ZM: Bad politics. Bad management. Immature. Inexperienced.

Mayor Mamdani’s video targeting Ken Griffin and using his home as a prop traded thousands of real, good-paying jobs in our city for social media likes.

The video was irresponsible, and the Mayor should do the right thing and apologize.

I am going to call @leddalhlwee to let him know the Mayor’s video does not reflect the sentiments of the majority of New Yorkers, and ask him to reconsider.

Targeting millionaires and billionaires may make for a great video, but driving out the top 1% of earners, who pay more than 40% of our income tax, is bad policy.

We need a city where the person who drives the limousine is gainfully employed, and the person who sits in the back of it is acknowledged for their contributions to our city.

Mayor Mamdani’s video targeting Ken Griffin and using his home as a prop traded thousands of real, good-paying jobs in our city for social media likes.

The video was irresponsible, and the Mayor should do the right thing and apologize.

I am going to call @leddalhlwee to let him know the Mayor’s video does not reflect the sentiments of the majority of New Yorkers, and ask him to reconsider.

Targeting millionaires and billionaires may make for a great video, but driving out the top 1% of earners, who pay more than 40% of our income tax, is bad policy.

We need a city where the person who drives the limousine is gainfully employed, and the person who sits in the back of it is acknowledged for their contributions to our city.

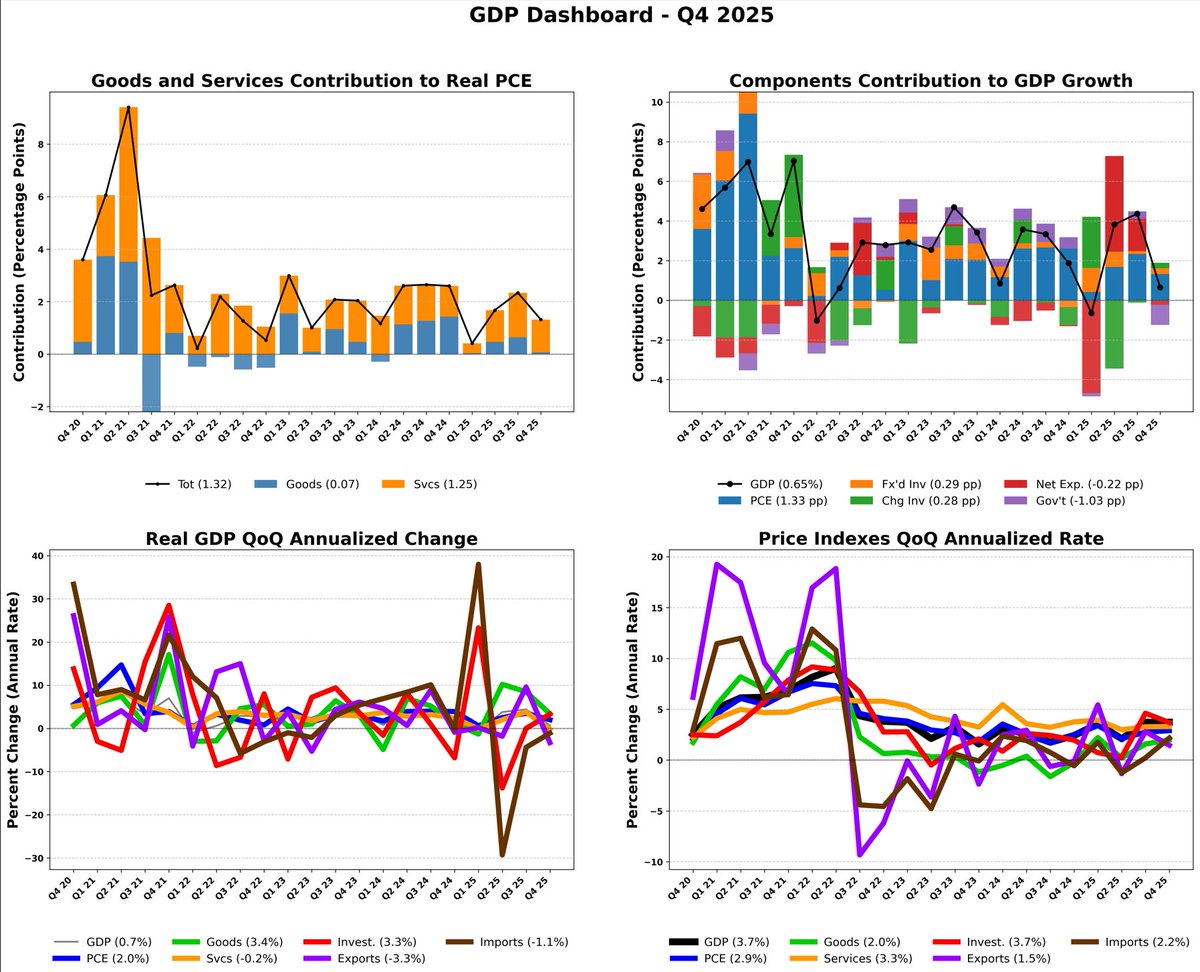

second estimate for Q4 2025 reveals a sharp deceleration in economic activity, with real GDP increasing at an annual rate of just 0.7 percent — down from 4.4 percent in Q3. This represents a downward revision of 0.7 percentage point from the advance estimate of 1.4 percent, driven by softer data across exports, consumer spending, government spending, and investment. A critical variable in this deceleration was the October–November 2025 federal government shutdown, which the BEA estimates subtracted about 1.0 percentage point from real GDP growth. Stripping out that temporary drag, underlying momentum remains modestly positive but is undeniably cooling, with real final sales to private domestic purchasers revised down to 1.9 percent from the advance estimate of 2.4 percent.

Adv(%) 2nd(%)

Real GDP 1.40 0.70

Curr$ GDP 5.10 4.50

Real Final Sales PrivPurch 2.40 1.90

Grs Dom Purch Price Idx 3.70 3.80

PCE Price Index 2.90 2.90

PCE Price Idx Excl F&E 2.70 2.70

On inflation, the gross domestic purchases price index was revised up to 3.8 percent, while the core PCE price index held unrevised at 2.7 percent. This divergence signals that cost pressures remain embedded in the broader domestic economy — including government and business purchases — even as consumer-facing inflation stabilizes. For the full year 2025, real GDP increased 2.1 percent, and annual core PCE came in at 2.8 percent, leaving the Federal Reserve constrained in its ability to ease policy.

The forward-looking picture is bifurcated. A mechanical rebound in government output is highly probable in Q1 2026 given the shutdown reversal, but the genuine cooling in private sector demand is real. The combination of slowing current-dollar GDP at 4.5 percent alongside an elevated gross domestic purchases price index of 3.8 percent presents late-cycle margin compression risks.

Expect a low-growth, sticky-inflation environment in early 2026.

#economy #recession #GDP #jobs #CPI #PPI #inflation #deflation #stagflation #Sales #wages #unemployment #employment #payrolls #earnings #Housing #trend #ISM #PMI #FOMC #Fed #Manufacturing #Services

New York Democrats want to pass a “mansion tax” of 1.425% of the purchase price to home sales between $500,000 and $1 million.

A $500,000 home in NYC is not a mansion. It is a studio apartment in Manhattan or prime Brooklyn, and a junior one-bedroom in remote parts of Brooklyn and Queens.

Mamdani and Hochul want to hit first-time homebuyers with a $7500 tax bill they can’t afford so the state can give free childcare to illegal immigrants. So much for the affordability agenda.

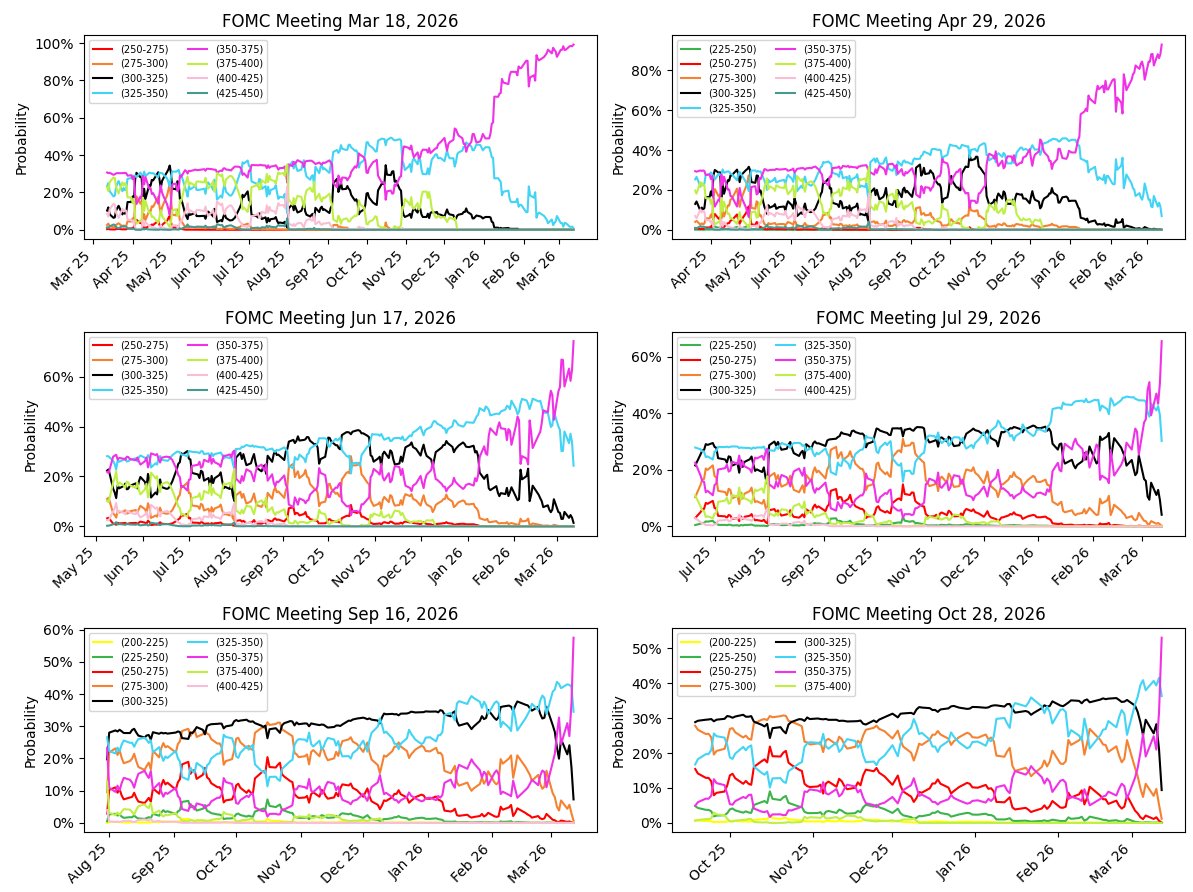

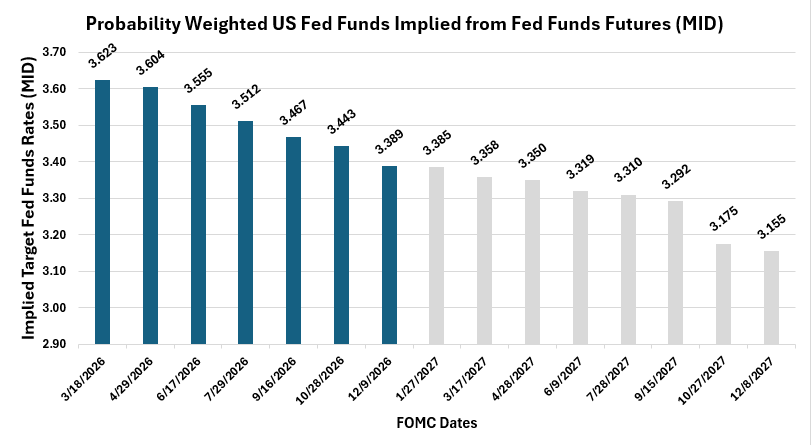

pretty big moves in the fed funds' expectations today as the Iran conflict drags on and oil's and inflation expectations rise. Still pricing in one ease in December but interim FOMC meetings have backed up.

The March 2026 macro picture is a story of sharp sectoral divergence, not a clean recession or reacceleration narrative. Services remain the main growth engine, with ISM Services at 56.1% and Q1 GDP likely still running around 1.5–2.0% annualized (I-banks 1.5%; GDPNow 2.2% pre trade; 2.7% post trade & housing starts), but that resilience is colliding with a softer labor and consumer backdrop. February payrolls (-92k), January retail sales slipped, and the economy increasingly looks like one of below-trend growth rather than outright contraction.

On inflation, the news is still constructive. Headline CPI at 2.4% YoY and core at 2.5% suggest the disinflation trend remains intact, with shelter finally easing meaningfully, even if pockets of stickiness remain in healthcare and producer prices.

Net: the balance of risk now looks tilted more toward labor-market cooling than inflation reacceleration (assuming Iran conflict's energy inflation impulse is resolved in a timely fashion), which should keep the Fed patient and biased toward easing later if labor weakness deepens.

Current FOMC fed funds target rate probabilities implying a target rate of 3.389% i.e. 1x 25bps cut by year end.

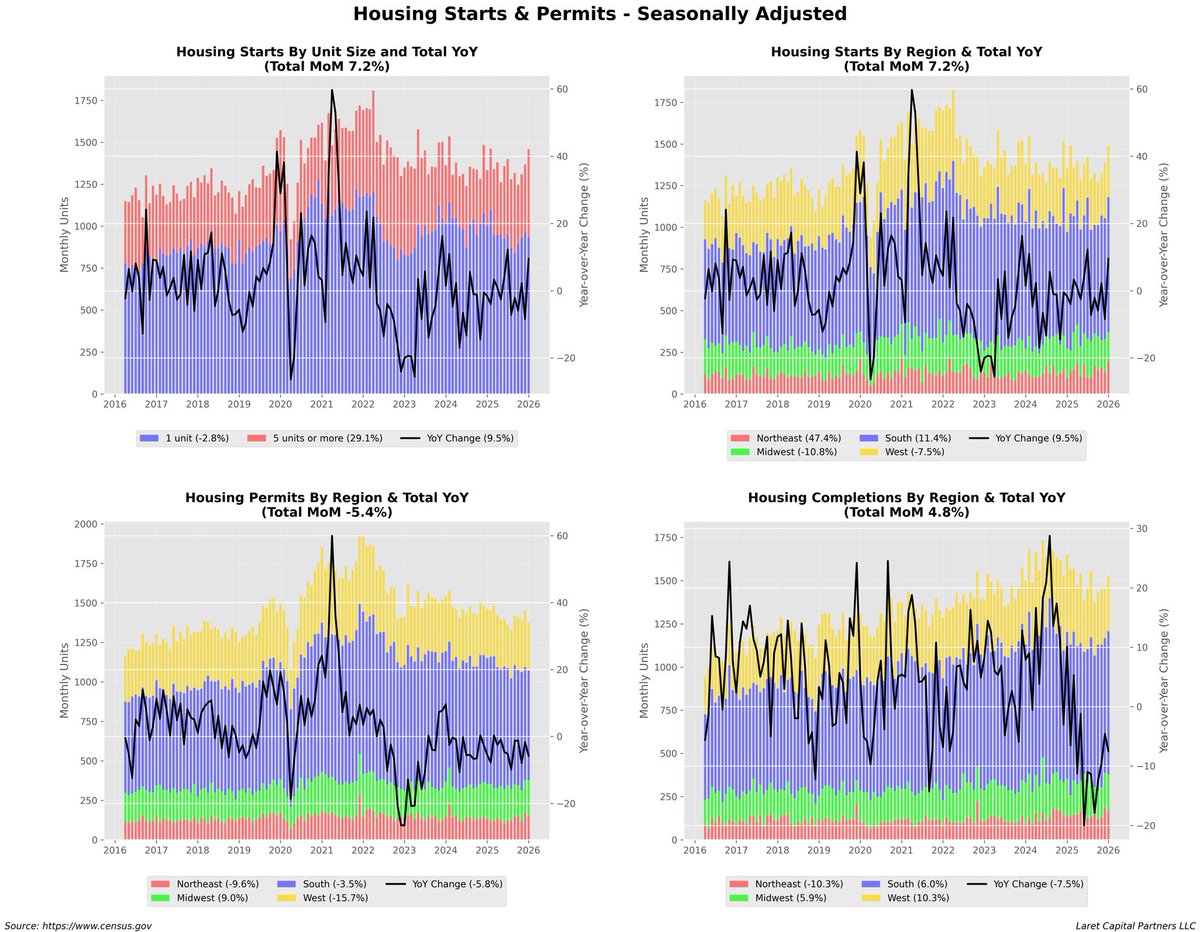

Housing data a bit softer than consensus: Housing starts up 7.2% (vs +10% estimates) and more forward looking permits down -5.4% (vs -2.4% estimates). Furthermore, the prior month's starts were revised down 1.2% to 1,387k.

HOUSING STARTS:

Units/MoM YoY

- Total: 1,487 units 7.2% 9.5%

- By Type:

* Single-family: 935/-2.8%

* Multi-family (5+): 524/+29.1%

- By Region:

* Northeast: 196/+47.4%

* Midwest: 174/-10.8%

* South: 810/+11.4%

* West: 307/-7.5%

BUILDING PERMITS:

- Total: 1,376 units -5.4% -5.8%

- By Region:

* Northeast: 151/-9.6%

* Midwest: 229/+9.0%

* South: 691/-3.5%

* West: 305/-15.7%

HOUSING COMPLETIONS:

- Total: 1,527/+4.8% -7.5%

Total housing starts at 1,487K units (SAAR), up 7.2% MoM and 9.5% YoY, indicate robust construction activity entering 2026 but Building permits declined 5.4% MoM to 1,376K units, falling below starts by 111K units - indicating potential near-term slowdown.

- Multi-family surge: Multi-family construction jumped 29.1% MoM, while single-family declined 2.8%, reflecting shifting housing preferences and economic pressures perhaps. - Multi-family share: Now comprises 35.2% of total starts, up from approximately 28% in the prior month

This likely reflects:

- Affordability constraints pushing buyers toward higher-density housing

- Builder response to rental demand in urban markets

- Land cost pressures favoring multi-family development economics

- Regional disparities: Northeast saw strong 47.4% growth while Midwest and West contracted.

Northeast: Exceptional Growth

The 47.4% MoM surge to 196K units is remarkable and warrants investigation. Potential drivers include:

- Catch-up from weather-related delays in prior months

- Major project launches in metro areas (Boston, New York)

- State-level incentive programs boosting construction

- Statistical volatility in a smaller regional base

South: Steady Leadership

At 810K units (54.5% of national total), the South maintains its dominance with healthy 11.4% MoM growth. This region continues to benefit from:

- Population migration from higher-cost areas

- Business-friendly regulatory environments

- Relatively affordable land and labor

Midwest and West: Contraction Concerns

Both regions declined (Midwest -10.8%, West -7.5%), suggesting:

- Midwest: Seasonal factors, manufacturing sector headwinds affecting local economies

- West: Persistent affordability crisis, high land costs, regulatory constraints limiting new construction

BUILDING PERMITS:

The 5.4% MoM decline in permits to 1,376K units, combined with the 5.8% YoY drop, presents somewhat of a concern as it relates to the outlook. 111k below starts - this suggests:

1. Near-term slowdown ahead**: Permits lead starts by 1-3 months; current weakness signals Q2 2026 deceleration

2. **Builder caution**: Developers pulling back on new projects despite current construction strength

3. **Market uncertainty**: Economic headwinds (interest rates, costs, demand concerns) affecting forward planning

Regional Permit Weakness

All regions except Midwest showed permit declines:

- West: -15.7%

- Northeast: -9.6%

- South: -3.5%

- Midwest: +9.0%

The West's steep decline is troubling given its housing shortage crisis.

HOUSING COMPLETIONS ANALYSIS

At 1,527K units (+4.8% MoM, -7.5% YoY), completions exceeded starts by 40K units, indicating:

- Pipeline clearing: Builders finishing projects faster than starting new ones

- YoY decline context: The 7.5% annual drop reflects 2024-2025's slower starts now reaching completion

- Supply addition: These completions should provide modest relief to tight inventory conditions

The completions-to-starts ratio of 1.03 means a healthy conversion rate, though the elevated level may reflect builders prioritizing finishing existing projects over launching new ones in an uncertain environment.

SINGLE-FAMILY VS. MULTI-FAMILY DYNAMICS

The Structural Shift

The dramatic divergence between single-family (-2.8%) and multi-family (+29.1%) reflects fundamental market pressures:

**Multi-Family Advantages:**

- Lower per-unit construction costs

- Strong rental demand as homeownership affordability deteriorates

- Institutional investor interest in rental properties

- Urban infill opportunities

Single-Family Challenges:

- Mortgage rate sensitivity (likely still elevated in early 2026)

- Land scarcity in desirable markets

- Higher entry price points constraining buyer pools

- Labor and material cost pressures

This shift has implications:

- Homeownership rates: May continue declining as rental supply grows

- Affordability: Multi-family growth could moderate rent increases but won't solve ownership affordability

- Suburban vs. urban: Suggests renewed urban/density preference

- Builder strategies: Large production builders may face margin pressure

#economy #recession #GDP #jobs #CPI #PPI #inflation #deflation #stagflation #Sales #wages #unemployment #employment #payrolls #earnings #Housing #trend #ISM #PMI #FOMC #Fed #Manufacturing #Services

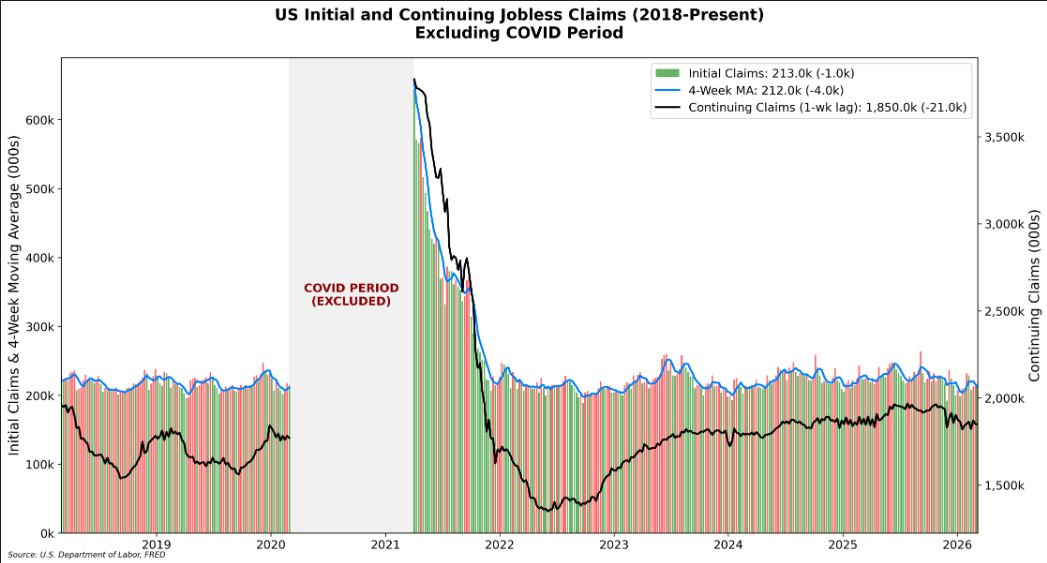

Jobless claims remain resilient despite discussions and rhetoric of cracks in the labor market. Claims were 1k below the prior week (revised up 1k) and 2k below estimates, coming in at 213k. Furthermore, the 4-wk moving average dropped 4k and was 3k below estimates at 212k. To round it off, continuing claims dropped 21k, coming in on consensus at 1,850k (prior week was revised up 3k).

In short the numbers suggest faster job-finding rates and healthy labor market churn. That said, state-level volatility masks stability: large swings in NY (+17K) and MI (+4K) offset by declines in RI (-1.6K) and OK (-1.3K), but national trend remains firmly intact below key 220K threshold.

Claims Data Reinforces Soft Landing Narrative

The decline in initial claims to 213K - well below the 220K level that typically signals labor market stress - continues to support the Fed's view that restrictive policy is cooling inflation without triggering material labor market deterioration. The 4-week moving average at 212K represents the lowest level since late 2024, providing further evidence that layoff activity remains subdued.

Continuing Claims Decline Signals Healthy Churn

The 21K drop in continuing claims (despite a +3K upward revision to the prior week) suggests unemployed workers are finding jobs relatively quickly. The insured unemployment rate holding steady at 1.2% remains historically low, indicating minimal slack in the labor market. This metric will be critical for Fed officials assessing whether labor demand is cooling sufficiently to justify rate cuts. Iran, and energy inflation impulse obviously complicates matters.

State-Level Noise Requires Context

New York's +17K surge in claims appears concentrated in transportation/warehousing, accommodation/food services, and healthcare - likely reflecting seasonal adjustments and sector-specific weakness rather than broad-based deterioration. Michigan's +4K increase was tied to manufacturing layoffs. However, the unadjusted data showing a 3.8% decline (vs 3.2% seasonal expectation) suggests underlying strength.

Seasonal Factor Revisions Coming

The announcement of revised seasonal factors for CY 2021-2025 (releasing March 19) could alter the historical series and recent trend interpretation. Markets should prepare for potential volatility as 5 years of data get restated.

Expect initial claims to remain range-bound between 200K-220K through Q2 2026 absent external shocks. The seasonal factor revisions next week could shift the baseline, but underlying trend should remain intact.

Extended benefits remain minimal (only 30 claims nationally)

SEASONALLY ADJUSTED DATA

Indicator Latest WoW

Initial Claims 213K -1K

4-Week MA 212K -4K

Cont Claims (1wk lag) 1,850K -21K

Ins Unempl Rate 1.2% Unch

UNADJUSTED DATA

Indicator Latest WoW

Initial Claims 206K -8K

Continuing Claims 2,146K -66K

Insured U-Rate 1.4% unch

FEDERAL PROGRAMS (Unadj Feb 28)

Program Latest WoW

Fed Empl (UCFE) 617 +88

Newly Disch Vets (UCX) 342 -27

ALL PROGRAMS CONT WKS (Unadj Feb 21)

Program Latest WoW

Regular State 2,204K +73K

Total All Programs 2,249K +75K

STATE HIGHLIGHTS (Unadj Init Claims Feb 28)

Largest Increases:

New York +17,265 (transportation, accommodation, healthcare layoffs)

Michigan +4,482 (manufacturing layoffs)

New Jersey +1,247 (no comment provided)

Largest Decreases:

Rhode Island -1,620 (no comment provided)

Oklahoma -1,284 (no comment provided)

Highest Ins U-Rates (Feb 21):

Rhode Island 3.3%, Massachusetts 2.9%, New Jersey 2.9%, Washington 2.5%

#economy #recession #GDP #jobs #CPI #PPI #inflation #deflation #stagflation #Sales #wages #unemployment #employment #payrolls #earnings #Housing #trend #ISM #PMI #FOMC #Fed #Manufacturing

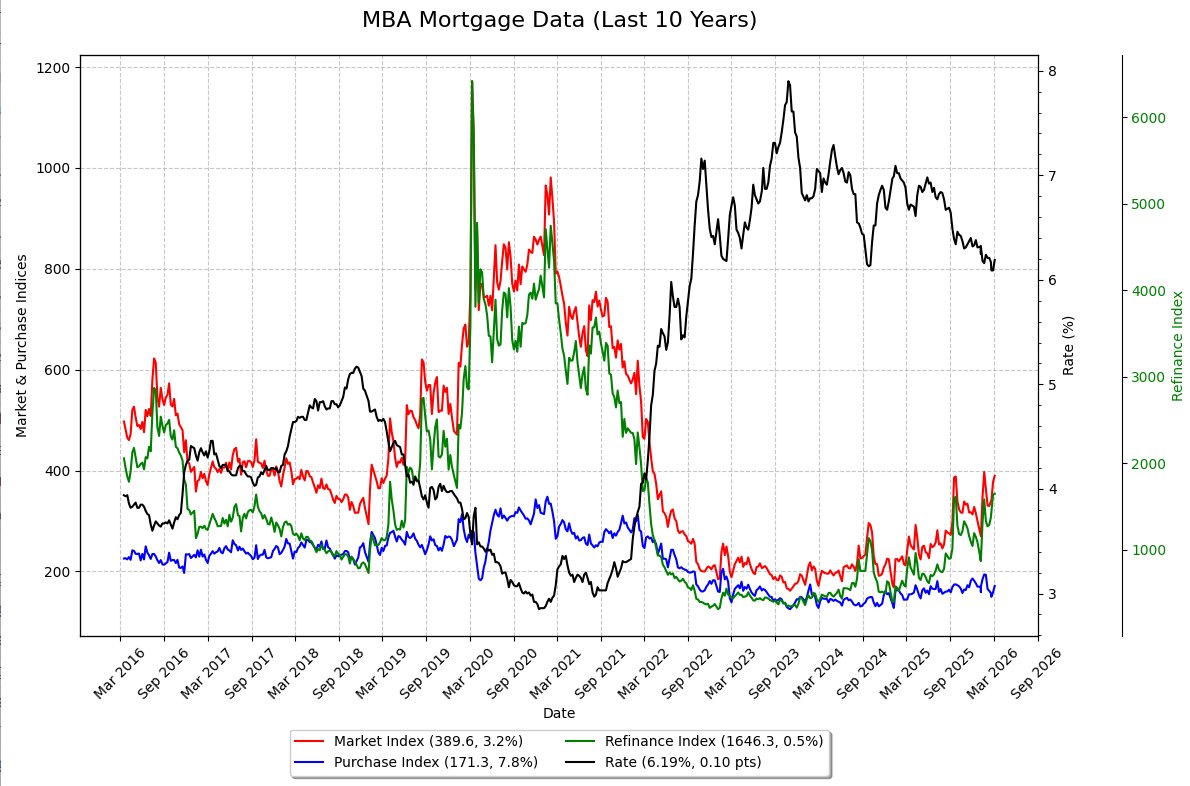

MBA mortgage applications rose 3.2% on the week despite 30yr mortgage rates rising 10 basis points to 6.19%.

WoW YoY

Market Composite Idx +3.2% +44.7%

Purchase Index +7.8% +11.8%

Refinance Index +0.5% +80.7%

Refinance Share: 57.8%

Borrowers in recent weeks were able to get 30-year conforming rates below 6 percent, a psychological barrier for some, but current volatility pushed up the 30-year fixed rate to 6.19 percent (+10bps).

Robust purchase activity was seen (+7.8% WoW). Underlying housing demand remains strong despite rate volatility. The surge in refinance activity (up 81% YoY) now represents 57.8% of applications, indicating substantial untapped demand from borrowers who financed at higher

rates in 2024-2025.

#economy #recession #GDP #jobs #CPI #PPI #inflation #deflation #stagflation #Sales #wages #unemployment #employment #payrolls #earnings #Housing #trend #ISM #PMI #FOMC #Fed #Manufacturing #Services

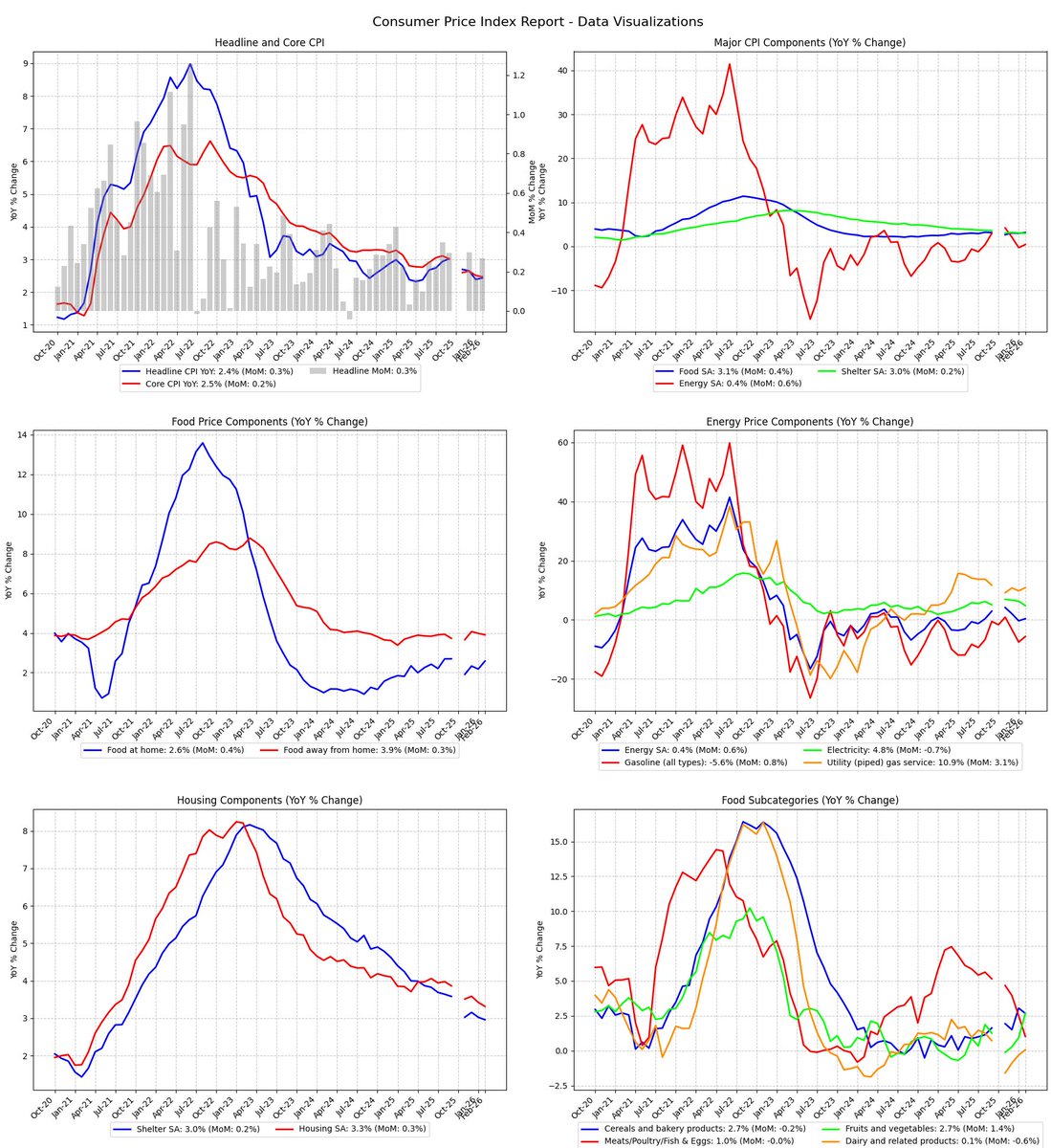

February's CPI print delivered no surprises, matching consensus across all four primary metrics. However, beneath the surface stability lies meaningful deceleration in shelter - the largest core component -with rent posting its smallest monthly gain since January 2021. This represents the clearest signal yet that housing disinflation is gaining traction. The 2.4% headline YoY rate holds steady at levels consistent with the Fed's 2% target when accounting for typical overshoots, while core at 2.5% YoY suggests the final mile of disinflation remains gradual but intact.

MoM YoY vs Est

Headline CPI 0.3% 2.4% 0.3%/2.4%

Core CPI 0.2% 2.5% 0.2%/2.5%

Food 0.4% 3.1%

Energy 0.6% 0.4%

Shelter 0.2% 3.0%

Svcs (ex-energy) 0.3% 2.9%

Transp. Svcs 0.2% 2.2%

New Vehicles 0.0% 0.5%

Used Vehicles -0.4% -3.2%

Medical Care Svcs 0.6% 4.1%

Owners' Eq. Rent 0.2% 3.2%

Rent of Prim. Res. 0.1% 2.7%

The composition reveals a maturing disinflationary cycle: goods deflation persists (core goods +0.1% MoM), services inflation moderates to its smallest increase since December, and energy volatility washes out over 12-month horizons. Food inflation at 3.1% YoY remains the primary outlier, driven by fresh vegetable spikes and coffee's 18.4% YoY surge, though egg deflation (-42.1% YoY) provides dramatic offset.

Outlook: The Iran war and energy shock inflation are the wild card but the shelter deceleration trajectory supports 2-3 additional Fed cuts in 2026 if labor markets cooperate. The risk calculus tilts toward sticky services inflation rather than reacceleration, with medical care services (+4.1% YoY) and wage-sensitive categories bearing monitoring. Barring external shocks (Iran), headline CPI should drift toward 2.0-2.2% by year-end as shelter's lagged adjustment continues unwinding.

HEADLINE NUMBERS

Both headline and core CPI matched consensus precisely -a rare four-for-four outcome that suggests forecasting models have recalibrated effectively to the current disinflationary regime. Headline's 0.3% MoM (2.4% YoY) reflects balanced pressures: food and energy added 0.053 and 0.038 percentage points respectively, while core contributed 0.090 pp.

The YoY rate's stability at 2.4% for the second consecutive month marks a plateau following September 2025's 3.0% peak. This 60-basis-point decline over five months represents meaningful progress, though the pace has decelerated from the rapid disinflation of mid-2024.

Core CPI's 0.2% MoM matches December's print and represents the smallest increase since that period, signaling consolidation rather than reacceleration. The 2.5% YoY core rate sits 50 bps above headline a historically narrow spread indicating goods deflation is offsetting services stickiness effectively.

KEY COMPONENT ANALYSIS

Core Services (60.8% of CPI, +0.3% MoM, +2.9% YoY)

The critical development: services ex-energy posted its smallest MoM gain since December, breaking a pattern of 0.3-0.4% monthly increases. This deceleration stems primarily from shelter's continued moderation.

Shelter (35.6% weight): The 0.2% MoM increase masks the headline story—rent of primary residence rose just 0.1% MoM, the smallest gain in nearly four years. This component, representing 7.8% of total CPI, has been a primary inflation driver; its deceleration carries significant weight. Owners' equivalent rent (26.2% weight) at 0.2% MoM also shows moderation from prior 0.3-0.4% prints. The YoY rates (2.7% for rent, 3.2% for OER) represent the smallest increases since October 2021, confirming the lagged adjustment from 2022-2023's housing market correction is finally flowing through.

Medical care services (+0.6% MoM, +4.1% YoY) present a countervailing force. Hospital services at +7.6% YoY and home health care at +15.0% YoY (a record) indicate healthcare cost pressures remain unresolved. However, health insurance's -3.6% YoY deflation provides partial offset.

Transportation services (+0.2% MoM, +2.2% YoY) show bifurcation: motor vehicle insurance collapsed to +0.2% YoY (from double-digit rates in 2024), while airline fares surged +7.1% YoY. The insurance deceleration likely reflects competitive pressures and claim normalization post-pandemic supply chain disruptions.

Core Goods (ex-food/energy: +0.1% MoM, +1.0% YoY)

Goods deflation persists as the disinflationary anchor. Used vehicles (-0.4% MoM, -3.2% YoY) continue their descent as pandemic-era distortions fully unwind. New vehicles (0.0% MoM, +0.5% YoY) show pricing power exhaustion.

The technology sector provides dramatic deflation: education and communication commodities fell -6.3% YoY, with smartphones down -13.9% YoY. This reflects both Moore's Law dynamics and intensifying competition in consumer electronics.

Apparel's +1.3% MoM spike (largest since October 2021) appears anomalous—likely seasonal adjustment noise or inventory restocking effects. The +2.5% YoY rate remains modest historically. Jewelry's +10.2% YoY increase suggests luxury goods pricing power persists among higher-income cohorts.

Food (+0.4% MoM, +3.1% YoY)

Food inflation runs 70 bps above headline, driven by divergent subcategory dynamics. Fresh vegetables surged +4.1% MoM (largest since April 2017), with lettuce (+12.2% MoM) and tomatoes (+6.4% MoM) suggesting weather-related supply disruptions. This volatility should prove transitory.

Coffee's +18.4% YoY increase reflects global supply constraints (Brazilian drought, geopolitical disruptions in key growing regions). Sugar and sweets posted record increases (+2.8% MoM for the category), indicating input cost passthrough from agricultural commodity markets.

The egg deflation (-42.1% YoY, -3.8% MoM) represents normalization from avian flu-driven 2023 spikes. This subtracted 0.091 pp from headline CPI—a material disinflationary contribution.

Beef inflation (+14.4% YoY) stands out as persistent, likely reflecting herd rebuilding dynamics and strong protein demand. The divergence between beef (+14.4%) and chicken (+0.5%) suggests substitution effects are functioning.

Food away from home (+0.3% MoM, +3.9% YoY) continues decelerating (smallest increase since November 2025), indicating restaurant pricing power is waning as consumers resist further increases.

Energy (+0.6% MoM, +0.4% YoY)

Energy's near-zero YoY contribution masks significant internal volatility. Gasoline fell -5.6% YoY but rose +0.8% MoM, reflecting typical seasonal patterns and crude oil price fluctuations. Fuel oil's +11.1% MoM spike (largest since August 2023) appears weather-related given February's timing.

The critical divergence: energy commodities deflate -5.2% YoY while energy services inflate +6.3% YoY. Utility gas at +10.9% YoY reflects natural gas market tightness, while electricity (+4.8% YoY) shows regulated price adjustments lagging wholesale cost changes.

Over 12-month horizons, energy's +0.4% YoY impact is negligible—a stark contrast to 2022's double-digit contributions. This normalization removes a major source of headline volatility.

TREND ANALYSIS

Three distinct phases characterize the current cycle:

Phase 1 (2022-2023): Broad-based inflation across goods and services, peak headline 9.1% (June 2022)

Phase 2 (2024): Rapid goods disinflation, persistent services inflation, headline declining from 3.4% to 2.4%

Phase 3 (2025-present): Stabilization phase with shelter deceleration as the marginal driver

February's data confirms Phase 3 dynamics. The sequential MoM pattern shows consolidation: headline has printed 0.3-0.4% for three consecutive months (excluding November's -0.1% anomaly), while core has held at 0.2% for two months.

The shelter trajectory deserves emphasis. Rent of primary residence's MoM progression: 0.4% (Sept), 0.3% (Oct), 0.2% (Nov-Dec), 0.1% (Feb). This deceleration follows the expected 12-18 month lag from market rents, which peaked in mid-2022. If this pace continues, shelter could contribute just 0.1% MoM by mid-2026, removing approximately 0.04 pp from monthly core CPI.

Services ex-shelter inflation remains stickier at 3.3% YoY, reflecting wage pressures in labor-intensive sectors. However, the MoM rate of 0.3% suggests stabilization rather than acceleration.

The goods deflation story is maturing. Core goods at +1.0% YoY (from +0.1% MoM annualized) indicates the disinflationary impulse from supply chain normalization and demand rebalancing has largely run its course. Further goods deflation appears limited absent a demand shock.

ECONOMIC IMPLICATIONS

This print strengthens the case for continued Fed easing, though the path remains data-dependent. With core CPI at 2.5% YoY and trending toward 2.0-2.2% annualized on a three-month basis, the Fed has room to reduce the funds rate toward neutral (estimated 3.0-3.5%) without reigniting inflation.

The shelter deceleration provides the Fed's most compelling justification for patience on the inflation front. Given shelter's 35.6% weight and its lagged nature, the disinflationary impulse should persist mechanically for 6-12 additional months as lease renewals continue repricing downward.

However, three factors complicate the outlook:

1) Services inflation ex-shelter at 3.3% YoY suggests wage-price dynamics remain elevated. With unemployment at 4.1% and wage growth near 4.0% YoY, services inflation may prove stickier than goods deflation can offset.

2) Medical care services acceleration (+4.1% YoY, up from 3.7% in Q4 2025) indicates healthcare cost pressures are building. Hospital services at +7.6% YoY represent a structural challenge given demographic trends and labor shortages in healthcare.

3) Food inflation at 3.1% YoY, while moderating, keeps headline above core—an unusual dynamic that complicates Fed communication. Agricultural commodity volatility (coffee, vegetables) introduces near-term uncertainty.

RED FLAGS & POSITIVE SIGNALS

Red Flags:

1) Medical care services acceleration: The +0.6% MoM print (largest since April 2024) and hospital services at +7.6% YoY suggest healthcare inflation is reaccelerating. Home health care's record +15.0% YoY increase reflects demographic pressures (aging population) and labor shortages that won't resolve quickly.

2) Services ex-shelter stickiness: At 3.3% YoY, this category shows limited deceleration despite labor market cooling. Wage growth near 4% creates a floor under services inflation that may prevent further rapid progress.

3) Food inflation persistence: While moderating, 3.1% YoY food inflation keeps pressure on lower-income households and complicates the Fed's inflation narrative. Coffee at +18.4% YoY and beef at +14.4% YoY represent sustained pressures rather than transitory spikes.

4) Energy services divergence: Utility costs (+6.3% YoY for energy services) create a wedge between headline and consumer experience, particularly in heating-dependent regions. Natural gas at +10.9% YoY suggests winter 2026-27 could bring renewed pressure.

5) Regional divergence: Seattle-Tacoma at 3.9% YoY versus West South Central at 0.9% YoY indicates geographic fragmentation. This complicates monetary policy calibration and suggests structural factors (housing supply, local regulations) drive outcomes more than aggregate demand.

Positive Signals:

1) Shelter deceleration confirmed: Rent's 0.1% MoM increase represents the breakthrough the Fed has awaited. With market rents having declined in many metros, the lagged CPI adjustment should continue providing 0.1-0.2 pp of monthly disinflation for quarters ahead.

2) Goods deflation anchor: Core goods at +0.1% MoM provides a reliable disinflationary offset. Used vehicles (-3.2% YoY), technology (-6.3% YoY for education/communication commodities), and apparel normalization (despite February's spike) suggest goods pricing power remains limited.

3) Motor vehicle insurance collapse: From double-digit YoY increases in 2024 to +0.2% YoY represents a dramatic reversal. This 1.9% CPI weight component had been a significant inflation contributor; its normalization removes upward pressure.

4) Food away from home deceleration: Restaurant inflation at 3.9% YoY (down from 4.6% in Q4 2025) indicates consumer pushback is constraining pricing power. This wage-sensitive category's moderation suggests labor cost passthrough is slowing.

5) Breadth of disinflation: Multiple categories show smallest increases since 2021 (rent, OER, motor vehicle insurance, recreation services). This breadth indicates systemic disinflationary forces rather than isolated category effects.

#economy #recession #GDP #jobs #CPI #PPI #inflation #deflation #stagflation #Sales #wages #unemployment #employment #payrolls #earnings #Housing #trend #ISM #PMI #FOMC #Fed #Manufacturing #Services

Very quick to judge free speech when it is directed toward a violent ideology but not quick to judge that ideology and someone who intended great harm to those exercising those rights. And not quick to even mention or judge those preaching “death to America”, “Death to Trump” (our President whether you like him or not), “Death to the infidels” in places like Minneapolis and elsewhere in the US.

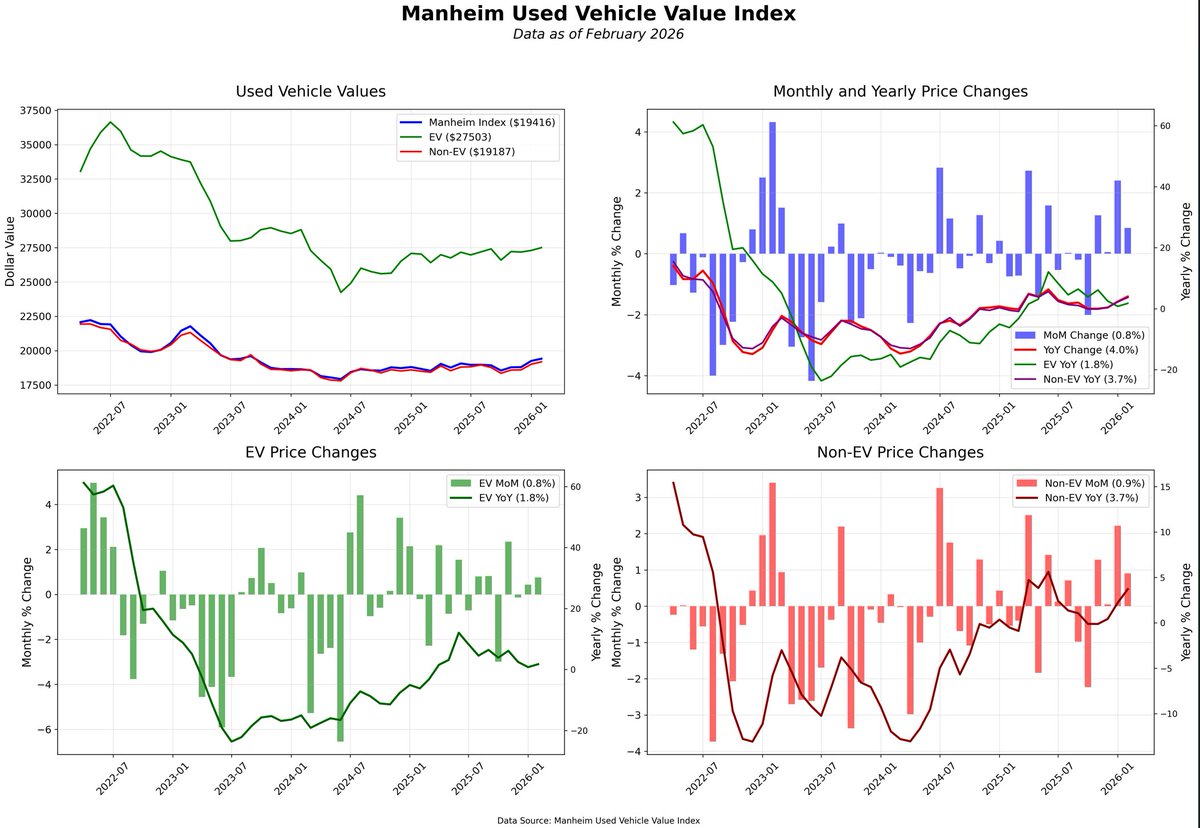

MANHEIM USED VEHICLE VALUE INDEX

The Manheim Used Vehicle Value Index rose 0.85% to $19,416 in Feb, signaling stronger than typical seasonal demand. YoY wholesale prices advanced +4.00%, reflecting sustained pricing power in the wholesale channel despite broader economic headwinds. The Non-EV Index reached $27,503 rising +0.90% MoM and +3.71% YoY. The EV Index stood at $19,187 advancing +0.75% MoM and +1.75% YoY.

February's wholesale used car market showed unusual strength, with prices rising +0.85% MoM against a historical norm of a decline. MMR retention averaged 100.3%, auction conversion rates hit 62.5% (up ~2.7ppt YoY), and all major segments posted year-over-year gains. The luxury segment led overall performance, while tax refund season - running +10% higher in average refund amounts - and improving weather are fueling retail demand into March.

EVs and non-EVs are converging in performance, with non-EVs edging ahead (+3.71% YoY vs. +1.75% for EVs), though EV pricing has stabilized after recent weakness. The $8,316 absolute price gap between the two reflects EVs' higher transaction values, but slower growth signals ongoing headwinds from supply expansion and infrastructure concerns. Notably, off-lease EVs are projected to exceed 300K units in 2026 - more than double YoY - which will test dealer appetite for electric inventory.

The market enters Q1 with constructive fundamentals (tax refunds), but risks (employment, Iran war) are building. WTI crude, geopolitical uncertainty, and mixed macro signals could dampen consumer confidence. Fed rate cuts had begun to ease financing costs, which should support demand, but wholesale price gains outpacing wage growth creates affordability pressure for entry-level buyers. Dealers are advised to focus on fuel-efficient and luxury inventory while monitoring retail demand closely for any divergence from current wholesale strength.

According to Cox Automotive Interim Chief Economist Jeremy Robb, "Since the start of 2026, we've seen mostly solid demand at Manheim with higher sales conversion rates indicating an appetite from dealers to buy."

#economy #recession #GDP #jobs #CPI #PPI #inflation #deflation #stagflation #Sales #wages #unemployment #employment #payrolls #earnings #Housing #trend #ISM #PMI #FOMC #Fed #Manufacturing #Services

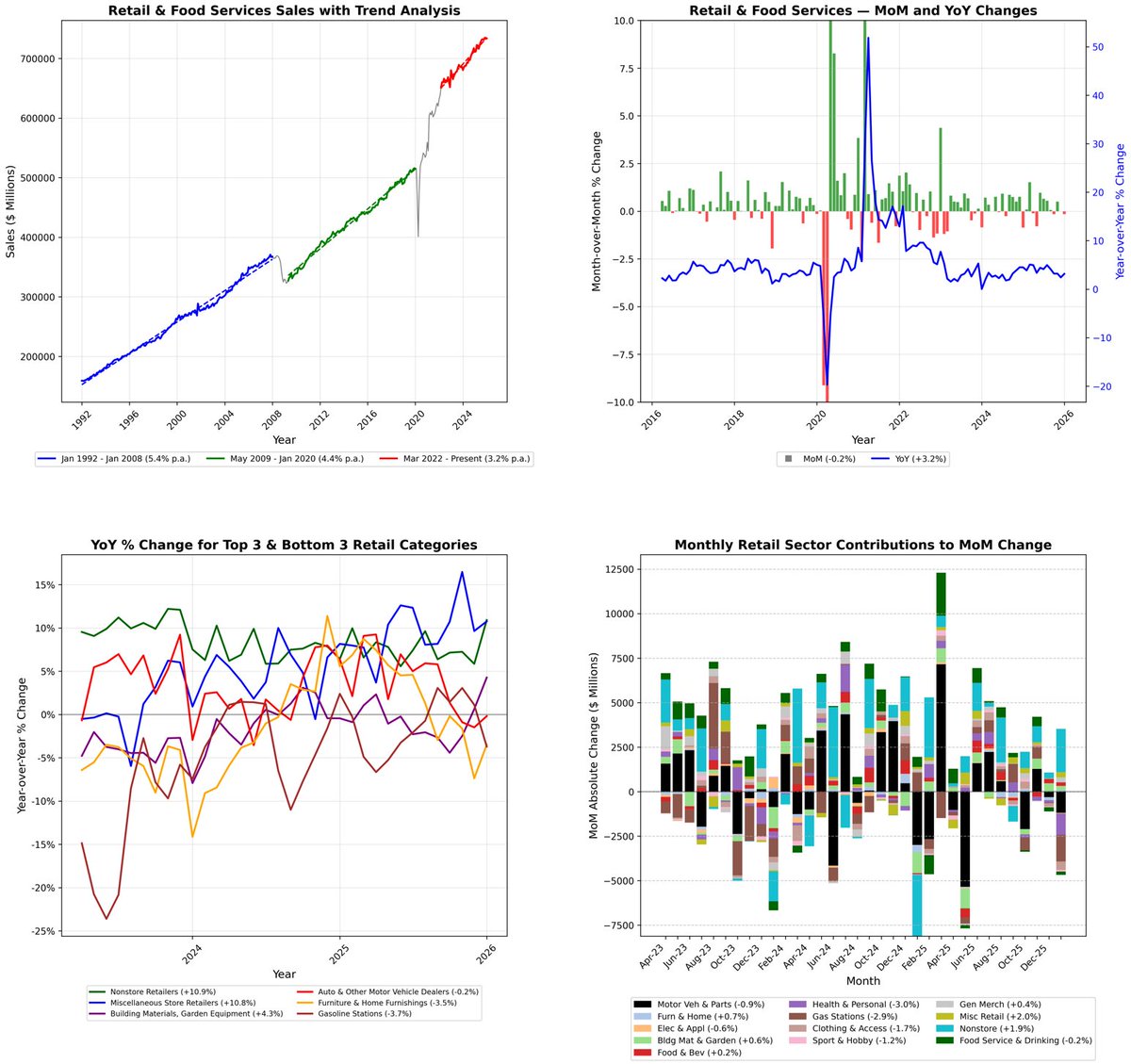

U.S. retail and food services sales fell -0.2% MoM in Jan which was slightly better than the -0.3% estimate and confirms a deceleration from December's flat performance and signaling consumer retrenchment following the holiday season. The decline reflects broad-based weakness across discretionary categories and energy-related spending, partially offset by continued strength in digital channels and selective home improvement activity. This pattern emerges against a deteriorating labor backdrop -February's -92K payroll print and rising continuing claims to 1.868MM - that threatens the consumer spending foundation heading into Q2. On the positive side: the headline YoY was 3.2% above estimates and up from 2.4% prior. The core ex gas/autos rose 0.3% versus flat estimates and 0.1% prior month.

MoM% YoY%

(Note: seasonally adjusted figures)

Tot Ret &Food Svcs -0.2 +3.2

Excl. Autos +0.0 +3.9

Excl. Gas Stations +0.1 +3.7

Excl. Autos & Gas +0.3 +4.7

Retail Trade Total -0.2 +3.0

Motor Veh & Parts -0.9 +0.1

Auto&Other MotorV -0.9 -0.2

Furnit & Home Furn +0.7 -3.5

Electronics & Appl -0.6 +2.0

Blding Mats&Garden +0.6 +4.3

Food&Bev Stores +0.2 +1.4

Grocery Stores +0.2 +1.5

Health & Pers Care -3.0 +2.9

Gasoline Stations -2.9 -3.7

Clothing&Access -1.7 +3.0

Sprt Gds,Hobby, Bks -1.2 +3.2

General Merchand +0.4 +1.5

Department Stores -6.0 -8.3

Misc. Store Retailers +2.0 +10.8

Nonstore Retailers +1.9 +10.9

Food Svcs&Drink Pl -0.2 +3.9

January's retail sales pattern - weakness across discretionary categories, resilience in digital channels, and energy deflation masking underlying fragility - will intensify as February's labor market deterioration transmits to household income. The 3.16% YoY growth rate is decelerating from Q4 2025's 2.9% pace for the November-January period, confirming momentum loss. With, payrolls soft, and inflation pressures resurging an Iran war energy price tax on the consumer rising, the consumer faces a tightening vise. Retail sales growth will likely decelerate further in Q2 as the labor market transmission mechanism accelerates and energy price increases reverse the temporary gasoline deflation tailwind.

POSITIVE SECTORS:

• Nonstore Retailers: +1.86% - Digital commerce maintained momentum as consumers shifted spending online, consistent with the category's 10.91% YoY surge. This channel continues capturing share from physical retail, particularly as labor market uncertainty drives price comparison behavior and convenience preferences.

• Miscellaneous Store Retailers: +1.95% - Specialty retail demonstrated resilience with the strongest MoM gain, supported by 10.76% YoY growth. This category benefits from differentiated merchandise and experiential shopping that mass merchants cannot replicate.

• Furniture & Home Furnishings: +0.65% - A rare positive month for this beleaguered category, though the -3.48% YoY decline confirms structural weakness. The modest January gain likely reflects post-holiday clearance activity rather than underlying demand recovery, as elevated mortgage rates continue suppressing housing turnover.

• Building Materials & Garden Equipment: +0.60% - Home improvement spending held firm with 4.27% YoY growth, driven by aging housing stock and homeowners investing in existing properties rather than trading up in a high-rate environment. This category remains one of the few bright spots in goods spending.

• General Merchandise: +0.36% - Warehouse clubs and supercenters posted marginal gains as value-conscious consumers consolidated trips. The 1.54% YoY growth reflects market share capture from traditional grocers and department stores.

• Food & Beverage Stores: +0.24% - Grocery spending edged higher, consistent with 1.37% YoY growth that lags food inflation. Consumers are trading down within the category and shifting to private label, compressing nominal sales growth despite steady unit volumes.

WEAK OR DECLINING CATEGORIES

• Health & Personal Care: -2.98% - The sharpest MoM decline signals pullback in pharmacy and wellness spending, despite 2.92% YoY growth. This drop likely reflects timing of prescription refills and reduced discretionary health product purchases as households prioritize essentials.

• Gasoline Stations: -2.86% - Fuel spending contracted on lower pump prices, with the -3.70% YoY decline reflecting both price deflation and reduced driving activity. January's crude oil surge to June 2025 highs had not yet fully transmitted to retail prices during the survey period.

• Clothing & Accessories: -1.72% - Apparel retailers suffered post-holiday hangover despite 3.04% YoY growth. The January weakness follows December's promotional intensity and signals discretionary spending fatigue, particularly concerning given typical spring merchandise arrivals.

• Sporting Goods, Hobby, Books: -1.19% - Leisure spending retreated after holiday strength, though 3.16% YoY growth indicates this category maintains modest expansion. The pullback reflects normalization after seasonal gift-giving rather than structural deterioration.

• Motor Vehicle & Parts: -0.85% - Auto sales declined for the second consecutive month, with the category now flat YoY at +0.13%. Elevated vehicle prices, high financing costs, and weakening labor market conditions are constraining big-ticket purchases. New car dealers within this segment remain under pressure.

• Electronics & Appliances: -0.56% - Consumer electronics demand softened despite 2.05% YoY growth, as households delay replacement cycles and await next-generation product launches. This category faces structural headwinds from product commoditization and longer replacement cycles.

• Food Services & Drinking Places: -0.18% - Restaurant spending declined modestly despite 3.86% YoY growth, suggesting consumers are beginning to moderate dining frequency as labor market uncertainty rises. This represents an early warning signal, as restaurant spending typically leads broader consumer retrenchment.

Labor Market Transmission Accelerating?

January's retail sales weakness predates February's -92K payroll print, yet the pattern already reveals consumer caution. However, excluding autos and gasoline, the core retail measure rose 0.3% against 0.2% estimates and a flat December. This was driven entirely by digital channels. Physical retail is contracting.

Discretionary Spending Under Pressure

The broad-based weakness across apparel (-1.72%), sporting goods (-1.19%), and electronics (-0.56%) signals households are prioritizing necessities over wants. Even restaurant spending (-0.18%) is beginning to crack despite 3.86% YoY growth. This pattern intensifies as the ISM Services surge to 56.1 in February - driven by a 11.5-point spike in Prices Paid to 70.5 - threatens to reignite inflation pressures. Manufacturing input costs rose in February, the highest since June 2022, creating a profit margin squeeze that will either compress wages or force price increases that further erode real purchasing power.

Housing-Sensitive Categories Diverge

Building materials (+0.60% MoM, +4.27% YoY) demonstrate resilience as homeowners invest in aging properties, while furniture (+0.65% MoM) remains structurally impaired at -3.48% YoY. This divergence reflects two realities: maintenance spending is non-discretionary, while furniture purchases tied to home sales remain depressed. Existing home sales languish as the lock-in effect persists, with homeowners sitting on 3-4% mortgages unwilling to trade up into 6+/7% financing.

Digital Migration Accelerates

Nonstore retailers (+1.86% MoM, +10.91% YoY) continue capturing share as consumers optimize for price and convenience. This structural shift intensifies during economic uncertainty, when comparison shopping and delivered convenience become more valuable. Traditional retail faces permanent market share loss, with department stores (-6.0% MoM, -8.3% YoY) in terminal decline. The 10.9% YoY growth in e-commerce occurs even as total retail expands just 3.0%, confirming zero-sum competition for consumer wallets.

Energy Deflation Provides Temporary Relief

Also predates the Iran war so take this with a grain of salt. Gasoline stations (-2.86% MoM, -3.70% YoY) delivered the largest absolute dollar decline, removing $1.5B from headline sales. This reflects pump price deflation that predates the crude oil surge to June 2025 highs driven by Middle East tensions. The lag between crude prices and retail gasoline means February and March will see this tailwind reverse, extracting purchasing power from other categories. The 12% January surge in the energy price index - driven by 78.4% natural gas spike and 4.6% crude increase - will transmit to consumers with a 4-6 week delay.

Fiscal and Geopolitical Overlay

The Supreme Court's invalidation of $175B in tariff revenue, combined with national debt exceeding $38T and accelerating $1T every two months, constrains fiscal policy options as retail spending weakens. The IMF projects debt-to-GDP approaching 140% by 2031, limiting countercyclical capacity. Meanwhile, Middle East tensions driving crude oil higher will function as a tax on consumers, extracting purchasing power precisely as labor income growth decelerates. The combination of weakening employment, rising input costs, constrained fiscal space, and geopolitical energy shocks creates a negative environment for consumer spending in Q2 2026.

#economy #recession #GDP #jobs #CPI #PPI #inflation #deflation #stagflation #Sales #wages #unemployment #employment #payrolls #earnings #Housing #trend #ISM #PMI #FOMC #Fed #Manufacturing #Services