$NIM.V - Nicola Mining to Commence Gold Production at Dominion Gold Project

Nicola Mining announced it is finalizing preparations to start gold and silver extraction at the Dominion Gold Project in British Columbia, with mill feed expected to begin in July 2026.

The company has made a $251,000 reclamation bond payment, purchased equipment, and hired crews.

@NicolaMining

$PPTA.TO - Perpetua Resources Advances Construction of the Stibnite Gold Project

Perpetua Resources started construction on the Burntlog Route road after a federal court in Idaho denied a request from project opponents to stop work.

The court ruling removes an immediate legal barrier and lets the company keep to its construction schedule, which targets antimony production for U.S. defense by 2029.

Key points:

- Federal court denied opponents' motion for a preliminary injunction, allowing construction to continue.

- Company began construction of the Burntlog Route, a road upgrade for site access and environmental protection.

- Work is part of critical path activities to meet the 2029 operations target and supply antimony to the U.S. military.

- Construction follows early works started in October 2025 and includes worker housing and powerline upgrades.

$CCO.TO - Cameco Increases Ownership Stake in Cigar Lake Mine

Cameco agreed to buy an additional 2.871% stake in the Cigar Lake uranium mine for about $115.75 million, increasing its ownership to 57.418%.

Cameco is increasing its ownership in a high-quality uranium mine, a positive but expected strategic move.

Key points:

- Cameco's ownership in Cigar Lake increases to 57.418%

- Purchase price ~$115.75 million

- Transaction expected to close in Q3 2026

- Cigar Lake has proven and probable reserves of 172.4 million lbs U3O8

#uranium #U308

$USA.TO - Americas Gold and Silver released high-grade infill drill results from the Cosalá Complex, showing silver grades 2-5 times higher than the current modeled resource, including 599.8 g/t Ag over 14.0 meters.

Why it matters:

These results indicate potential to significantly upgrade the mineral resource grades and improve the economics of the future mine plan, as the intercepts are adjacent to existing infrastructure.

Key points:

- 14 drill results from three zones (San Rafael Upper, 120 Upper, 120 Lower) returned grades 2-5x above current resource grades.

- Highlight intercept: 14.0m at 599.8 g/t Ag and 0.8% Cu.

- All intercepts are adjacent to existing infrastructure and will be used to optimize the mine plan for H2 2026.

@americas_silver

The cost of developing #uranium mines has risen sharply due to:

🚨Inflation

🚨Labor shortages

🚨Higher fuel costs

🚨Supply-chain disruptions

🚨Increased regulatory complexity

🚨Rising capital costs

🔔Furthermore, feasibility studies often underestimate ultimate project costs

$EDV.TO - Endeavour Reports Fatal Accident at Lafigué Mine

A contractor died in a heavy mining equipment incident at Lafigué mine.

Contractor activities were temporarily paused; processing operations continued.

Endeavour is conducting a comprehensive investigation.

Relevant authorities have been informed.

Silver X Mining Corp. $AGX.V reported record financial results for the first quarter of 2026, with net income of $4.6 million, revenue of $13.4 million (up 155% year-over-year), and a cash balance of $53.8 million after closing a $50.3 million financing and acquiring the Pampas gold-silver project.

Why it matters:

The company has shifted from losses to profitability, strengthened its balance sheet significantly, and expanded its asset base in Peru. This suggests improved financial health and growth potential.

Key points:

Net income of $4.6 million vs. net loss of $0.3 million a year ago.

Revenue increased 155% to $13.4 million, with operating income up 791%.

Cash balance surged to $53.8 million from $10.1 million at year-end 2025.

Closed a $50.3 million senior secured convertible debenture financing.

Acquired the Pampas gold-silver project, becoming a multi-asset producer.

@Silver_X_Mining

Sitka Gold Corp. $SIG.NE reported assay results from the first drill hole of its 2026 program at the RC Gold Project in Yukon.

The hole intersected 94.0 metres of 1.79 g/t gold, including 19.3 metres of 5.04 g/t gold, within a broader interval of 273.8 metres of 1.10 g/t gold.

Why it matters:

These results extend the high-grade gold zone significantly below the current resource pit and suggest the potential for a future underground mining component at the Blackjack deposit.

What is still missing:

The release is based on only one drill hole, more drilling is needed to confirm the continuity and extent of the high-grade zone.

Key points

•First hole of 2026 program: 273.8 m of 1.10 g/t Au, including 94.0 m of 1.79 g/t Au and 19.3 m of 5.04 g/t Au.

•Deepest hole ever at RC Gold (1,093 m), extending mineralization 370 m below existing pit and 110 m along strike.

•Results support potential for high-grade underground mining at Blackjack.

•Approximately 13,000 m of a fully funded 60,000 m drill program completed.

@SitkaGoldCorp

GFG Resources Inc. $GFG.V discovers District-Scale Gold System at Nahanni with High-Grade Intercepts up to 11.20 g/t Au in First-Pass Drilling

These results suggest a new, district-scale gold system on the Goldarm Property, expanding exploration upside beyond the company's existing core targets.

Key points

•High-grade gold intercepts up to 11.20 g/t Au over 0.7 m at Nahanni East.

•Multiple drill holes returned broad zones of gold mineralization, e.g., 1.97 g/t Au over 6.2 m.

•10-hole program tested a 6 km segment of the Pipestone Deformation Zone, all three targets returned gold.

•Discovery validates GFG's greenfield targeting model and expands exploration potential beyond Aljo and Montclerg.

•Shallow depth of mineralization enhances potential for future development.

@gfgresources

Yes, mostly right, but there’s still upside beyond just dirt moved.

Copperstone is clearly derisked with a construction decision, funding path, and strong PFS economics, but the story still has room to grow through reserve conversion, underground expansion, and possible open-pit upside.

So I’d frame it as: no longer just optionality, but not fully priced on longer-term growth either.

Minera Alamos $MAI.V has decided to proceed with construction of the Copperstone underground gold mine in Arizona.

Minera Alamos released a pre-feasibility study for its Copperstone gold project in Arizona, showing strong economics with an after-tax NPV of $374M and IRR of 108% at a base case gold price of $3,500/oz.

The study supports a 6.3-year mine plan producing 291,000 ounces of gold, with initial production expected in mid-2027, which would more than double the company's current annual gold output.

Key points

•After-tax NPV5% of $374M and IRR of 108% at $3,500/oz gold

•Life-of-mine production of 291,000 oz gold over 6.3 years

•Initial production targeted for mid-2027

•All-in sustaining costs of $1,314/oz gold

•Full technical report to be filed within 45 days

@MineraAlamos

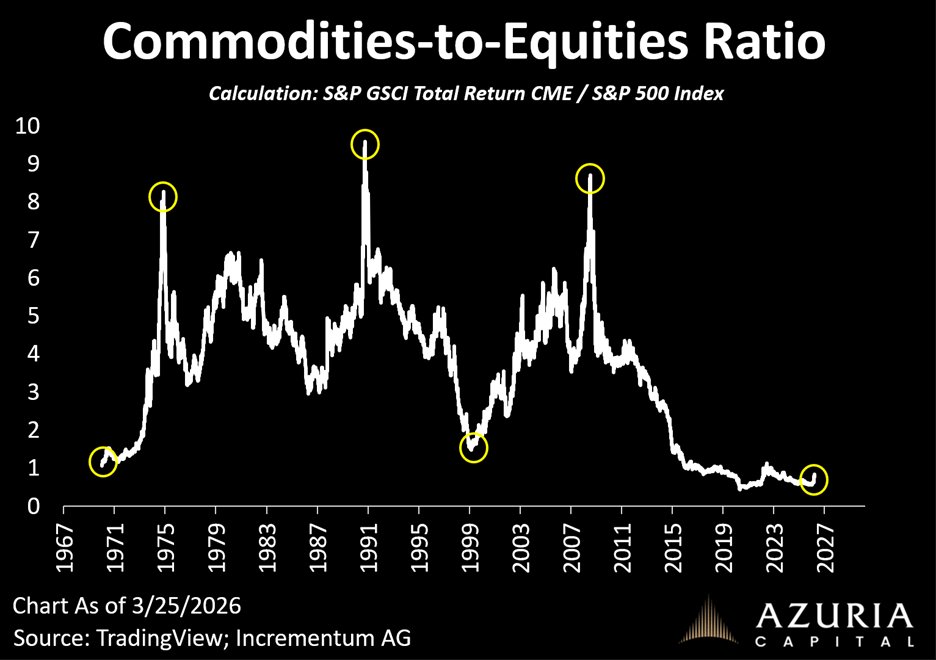

It’s only appropriate to revisit this chart after the recent move in markets.

And yes…

We’re still in the early innings of a regime shift from financial assets to hard assets.

The reality is simple:

Commodity markets play a critical role, yet their size still fails to match their importance.

Latest macro update with key technical and macro setups:

https://t.co/v2AJ7oh4sr

In recent interview on @INN_Resource, @TaviCosta shared his view on the market. Here are interesting takeaways:

Tavi's message is pretty clear: the next big move in commodities may be bigger than most people expect, and mining stocks still aren’t priced for it.

Mining: “The metal price moved… the stocks haven’t”

Tavi thinks we’re at a turning point for commodities. Gold has already broken out and held strong, but he believes the rest of the commodity space is still playing catch-up.

The part that really stands out is his view on mining equities: even with high gold and silver prices, many miners still trade like the good times won’t last.

His basic argument is simple: if the metals stay anywhere near these levels, miners are printing cash, yet the market still isn’t rewarding them the way it typically does later in a cycle.

Gold: not “too late,” still early

A lot of people look at gold and assume the move is over because the price already climbed so much.

Tavi doesn’t buy that.

He points to steady, structural buying from central banks and to how small the mining sector still is compared to the overall stock market.

In other words, the trade is getting attention, but he thinks we’re nowhere near the “everyone owns it” stage.

Silver: miners look mispriced

On silver, his view is basically: the market doesn’t believe the current silver price will hold, and that disbelief is showing up in silver mining stocks.

He’s focused on the simple math: if a miner can produce silver at roughly $15–$17 and sell it at much higher prices, that’s a massive margin.

His takeaway is that if silver stays elevated (even if it’s volatile), silver miners have room to rerate because their profitability is not being fully reflected.

Copper: could be the next “surprise” move

Tavi is especially excited about copper. He describes it as being near a “discovery phase”, the kind of moment when price can start moving fast and people scramble to reposition.

He’s not giving a neat price target, but he does suggest copper could have the kind of sharp upside move silver recently showed.

The bigger idea behind it: supply is tight, big discoveries have been rare, and it takes years to bring new mines online. If demand stays firm, copper doesn’t need a perfect story to move—it just needs a shortage.

Energy (oil & gas): under-owned and set up for a rebound

Tavi also likes energy, and he’s talking specifically about oil and gas.

Why? Because the sector is unpopular. He points out that ownership is low, drilling activity has dropped, and market positioning has been extremely bearish conditions that often show up near bottoms, not tops.

He expects energy stocks to “wake up” the way miners did after a long period of going nowhere.

Agriculture: the “lagger” that can catch fire

This is the sleeper part of his view. Tavi thinks agricultural commodities are lagging and laggers can become the best opportunities when the cycle turns.

He links agriculture to energy in a very practical way: when energy prices rise, costs tied to farming can rise too (like fertilizer inputs), and that can eventually push agricultural prices higher.

So he’s watching agriculture as a potential catch

up trade, not as a slow and boring corner of the market.

The thread that ties it together

Underneath all of this, Tavi keeps coming back to the same backdrop: if we move into a world of a weaker US dollar and falling interest rates, that tends to be friendly for hard assets, commodities, and resource equities.

His overall approach isn’t about predicting the exact top tick. It’s about noticing what isn’t happening yet, like the lack of exploration spending and the lack of major new discoveries, and using that to argue the commodity story still has runway.

If he’s right, the biggest opportunity may be owning the parts of the resource market that still feel ignored: miners that haven’t rerated, copper ahead of a potential squeeze, energy that’s under-owned, and agriculture that hasn’t joined the party yet.

Full interview here: https://t.co/SIMMvTqbhr

Here are the highlights worth watching:

Commodities may be at a turning point: gold has already moved, and the “catch up trade” is expected in copper, energy, and even agriculture.

Mining stocks still look cheap vs. metal prices: margins are strong, but many equities haven’t re-rated yet.

Exploration spending is still low (even with high prices): fewer discoveries today can mean tighter supply tomorrow.

Copper could be setting up for a big move: he sees it entering a potential “discovery phase” over the next 1–2 years.

Oil & gas are under-owned: he thinks the sector is set up for a rebound despite the “EVs killed oil” narrative.

Agriculture is a sleeper trade: he expects ag commodities to follow energy higher (fertilizer/input costs link them).

Thanks for sharing, lots to think about.

@DeItaone The decline, a roughly 70% reduction, stems from export disruptions via the Strait of Hormuz amid the ongoing Iran conflict, forcing production cuts due to storage limits

@OilandEnergy The decline, a roughly 70% reduction, stems from export disruptions via the Strait of Hormuz amid the ongoing Iran conflict, forcing production cuts due to storage limits

Everyone talks about Iranian oil in barrels.

Nobody talks about what’s inside them.

Iranian Light crude is the molecular sweet spot of global refining.

That’s why refineries quietly ran it through Dubai despite sanctions.

Everyone talks about Iranian oil in barrels. Nobody talks about what is inside them. That difference is why Western refineries have been running shadow networks through Dubai for twenty years to get it despite the sanctions.

Crude oil is not a uniform commodity. It is a spectrum of hydrocarbons with different molecular weights, and the composition of a given crude determines how easily it converts into the products refineries actually want to sell: gasoline, diesel, jet fuel, heating oil. The measurement that captures this is API gravity. Higher API gravity means lighter crude with shorter carbon chains, which means lower energy cost to crack, lower processing cost to refine, and higher yield of the light distillates that carry premium pricing. Lower API gravity means heavier crude requiring more energy, more processing steps, more capital equipment, and producing a higher share of lower-value residuals.

Iranian Light crude runs at 33 to 36 degrees API gravity with sulfur content between 1.36 and 1.5 percent. That is the refinery sweet spot. It is light enough to yield high fractions of gasoline and middle distillates without excessive processing costs, but heavy enough to produce the full range of products that complex refineries are designed to process. It is what petroleum engineers call an optimal blend crude.

Now compare the alternatives.

Venezuelan Merey heavy crude runs at approximately 16 degrees API gravity with sulfur between 3 and 5 percent. Refining it profitably requires a coking unit, a hydrocracker, and an extensive desulfurization train. The equipment exists. The economics work for refineries purpose-built around Venezuelan feedstock. It is not a substitute for Iranian crude. It is a different product requiring different industrial infrastructure.

US West Texas Intermediate runs at 39 to 40 degrees API with sulfur below 0.25 percent. In theory, the cleanest and easiest crude to process. In practice, it is so light that it does not yield the heavier middle distillates a complex refinery needs to run at full capacity. European and Asian refineries built around medium crudes cannot switch to WTI without blending it with heavier crudes to achieve the molecular weight distribution their process units require. WTI is not a drop-in replacement for Iranian medium.

Iranian oil fits where both US shale and Venezuelan heavy do not. It is the liquid that flows through the middle of the global refining system without requiring either the coking infrastructure for heavy crudes or the blending operations for ultra-light shale. That molecular fit is why it commands a persistent premium above comparable grades. It is why Indian refineries maintained Iranian crude purchases through every round of sanctions and negotiated the logistics to keep that flow moving. It is why the Dubai shadow banking and trading network that the UAE is now considering dismantling existed in the first place.

The Strait of Hormuz does not just carry oil. It carries the specific category of oil that the global refining system was built to process most efficiently. Closing it does not just reduce supply. It removes the grade of crude that the system runs best on and forces every refinery in the world to run less efficiently on whatever it can find as a substitute.

That is the premium embedded in the $82 oil price. Not just volume. Molecular weight.

https://t.co/ULBgEzZ3A8

We are two days away from war-risk coverage being terminated automatically if vessels enter the Persian Gulf. That has massive implications for traffic and the global energy market 🛢⤵️

The insurance pieces I have read is where the disruption we are seeing becomes self-reinforcing, because once insurance markets start pulling away, the Strait can seize up even without every vessel being physically blocked. Some Bloomberg reports that were part of the massive pile of paperwork on my desk noted that several major ship insurers, including Gard, Skuld, NorthStandard, the London P&I Club, and the American Club, have cancelled war-risk insurance coverage for vessels operating in Iranian waters, the Gulf, and surrounding areas, with the changes taking effect on March 5.

Bloomberg also separately reported that from midnight London time on March 5, as I noted at the start, war-risk cover will be terminated automatically if vessels enter the Persian Gulf, certain adjacent waters, or Iranian waters, and that this decision had already been taken by seven of the 12 members of the International Group of Protection and Indemnity Clubs, which collectively provide maritime cover for about 90% of the world’s ocean-going tonnage.

Reuters also confirmed that Japan’s MS&AD has suspended underwriting various war-risk policies in waters near Iran, Israel, and neighboring countries. Once that kind of insurance support is withdrawn, the cost of moving cargo rises sharply and, more importantly, a large share of the industry simply stops volunteering to take the voyage at all. This is one thing that most people don't think about or discuss, but it's an incredibly important part of the overal picture.

That is again why the distinction between “can ships physically pass” and “can the system function” is so important here. A handful of ships may still get through, especially smaller product tankers or operators willing to assume extraordinary operational and political risk, yet the systemic function of the lane is what matters for oil pricing and that function is already deeply compromised and we are feeling those effects right now.

Twenty million barrels of oil passed through the Strait of Hormuz yesterday.

Today the number may be zero.

Not because Iran mined the water. Not because a tanker was hit. Because Lloyd’s of London picked up the phone.

War risk underwriters began canceling policies for strait transits hours after Operation Epic Fury launched. The Financial Times confirmed premiums surging 50 percent. Baseline war risk sits at 0.25 percent of hull value. For a hundred million dollar tanker that is 250,000 dollars per voyage. At peak escalation rates, one million per transit. Vessels linked to American or Israeli interests are becoming uninsurable entirely. No price. No policy. No passage.

The KHK Empress was loaded with Omani crude heading for Basra when it executed a U-turn mid-strait and redirected to India. The Eagle Veracruz halted at the western approach carrying two million barrels of Saudi crude bound for China. The Front Shanghai stopped off Sharjah with Iraqi crude destined for Rotterdam. Nippon Yusen ordered its entire fleet to avoid Hormuz. Greece told its merchant armada to reassess passage. Hapag-Lloyd suspended all transits.

None of them were fired upon. Every one of them got the same call.

More than fifty million years ago the Arabian plate collided with the Eurasian plate and compressed the Persian Gulf into a basin that drains through a single geological bottleneck twenty one miles wide. Twenty one percent of global petroleum. Twenty percent of all seaborne LNG. One fifth of industrial civilization’s energy supply forced through a tectonic accident narrower than the English Channel, bordered on one side by the country whose supreme leader was killed yesterday morning.

The USS Abraham Lincoln carries enough Tomahawks to sink every IRGC patrol boat in 48 hours. Operation Praying Mantis crippled Iran’s operational naval forces in eight hours in 1988. The Fifth Fleet has rehearsed this scenario for decades.

None of that matters. Aircraft carriers cannot force an underwriter to rewrite a policy. Tomahawks cannot lower a premium. The most powerful navy in human history cannot make a Lloyd’s syndicate decide that a VLCC transiting Iranian coastal waters represents an acceptable risk on a Saturday afternoon when missiles are landing in Dubai.

Goldman Sachs estimates Brent could peak at 110 dollars per barrel. JP Morgan projects 120 to 130. At those levels every airline bleeds cash. Every central bank watches three years of inflation fighting reignite overnight. Bypass pipelines from Saudi Arabia and the UAE handle roughly three million barrels. Hormuz handles twenty million. The math does not close.

Iran figured out something the Pentagon still has not.

You do not need to close a strait. You just need to make it uninsurable.

https://t.co/BrzGRrU3VW