Safety + Income

Selective Convex Extraction

Within a barbell allocation, the strategy sits in the cautious 90% — the long-term capital-growth engine.

Its self-hedging income stream is what lets that safe base hold its ground against inflation, freeing the aggressive 10% to take convex risk without jeopardizing the whole.

Profits lead, hiring follows

US corporate profit growth remains exceptional - and it typically leads labour demand, not the other way round. With corporate spending still running hot, the outlook for the rest of the year is bright.

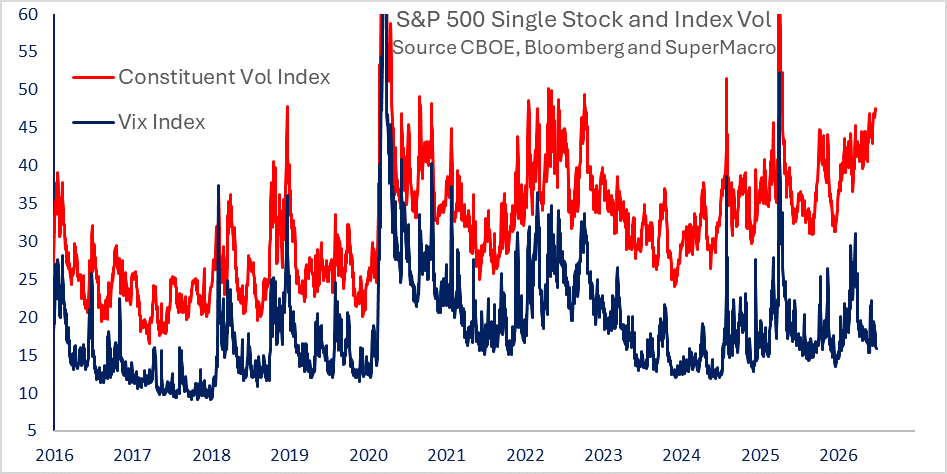

Correlation is the only thing holding the Vix down

Single-stock implied vol in the S&P 500 is extremely high, yet the Vix keeps drifting lower. The spread between the two hit a new high last week. Only low correlation is holding the index down - and if it turns, the Vix moves sharply. Our weekend note explains this in depth.

(Bloomberg ) -- The Federal Reserve could break decades of precedent and buy equity ETFs during the next major bear market.

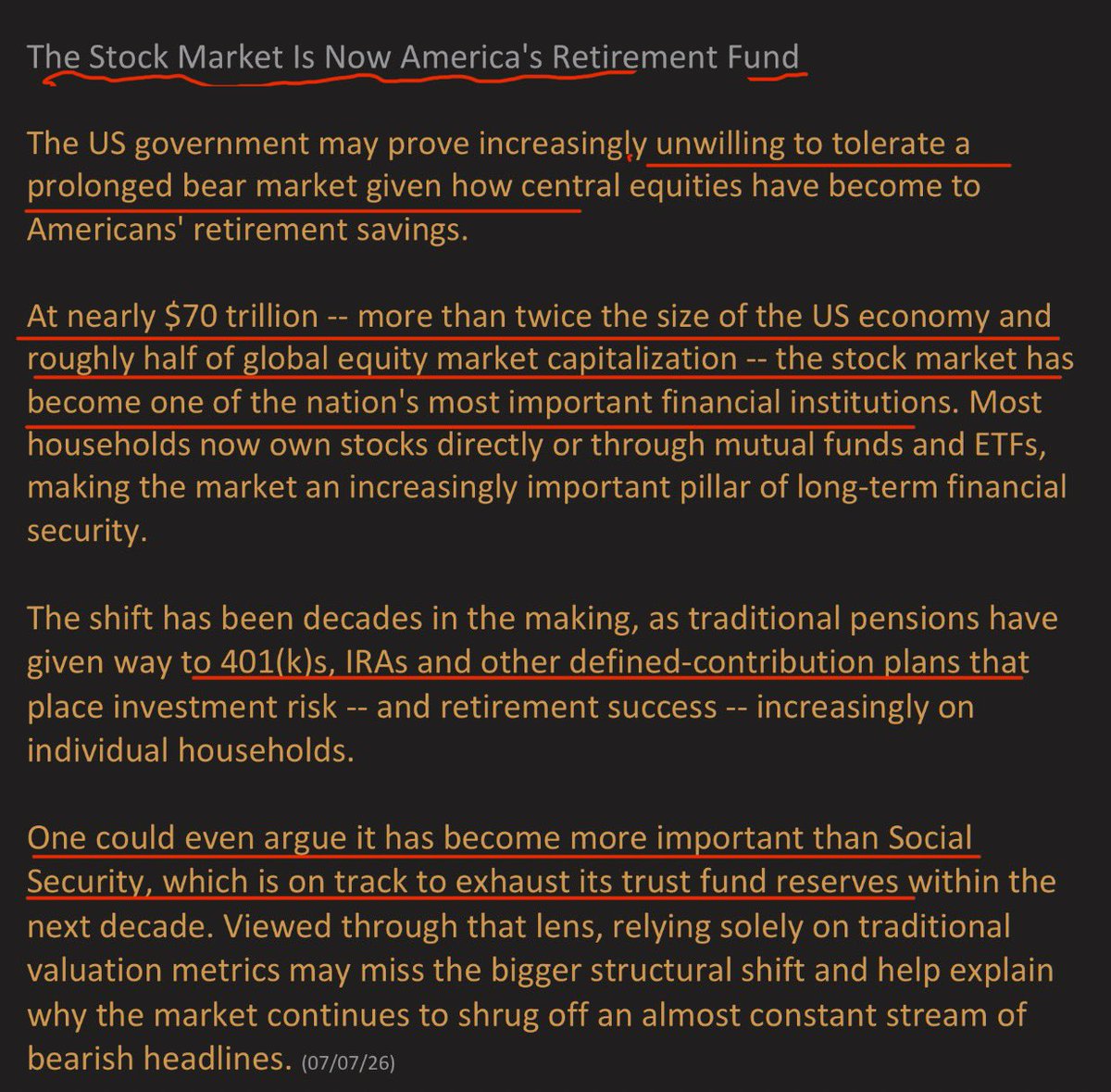

Is the US Stock Market Too Big to Fail?

At nearly $70 trillion -- more than twice the size of the US economy and roughly half of global equity market capitalization -- the stock market has become one of the nation's most important financial institutions

Markets No Longer Expect Aggressive Fed Cuts

Fed futures have undergone a dramatic repricing. Early in 2026, markets expected April 2027 policy rates to sit well below the effective Fed Funds Rate. Today, implied rates have risen to roughly 4.1%, while October 2026 expectations approach 3.9%. The spread between future contracts has shifted from negative territory to roughly +0.2 percentage points, reflecting expectations that policy will remain restrictive for longer. Investors who anticipated a rapid easing cycle have been forced to adjust. Stronger U.S. data, resilient employment, and persistent economic momentum have significantly reduced expectations for aggressive Fed rate cuts over the coming year.

In the top stocks the buyside is actually short gamma (dealers long) on net. That gives dealers positive gamma (blue)

The skew is an artifact of the right tail risk from these stocks going up 🍌s % for the last 90 days

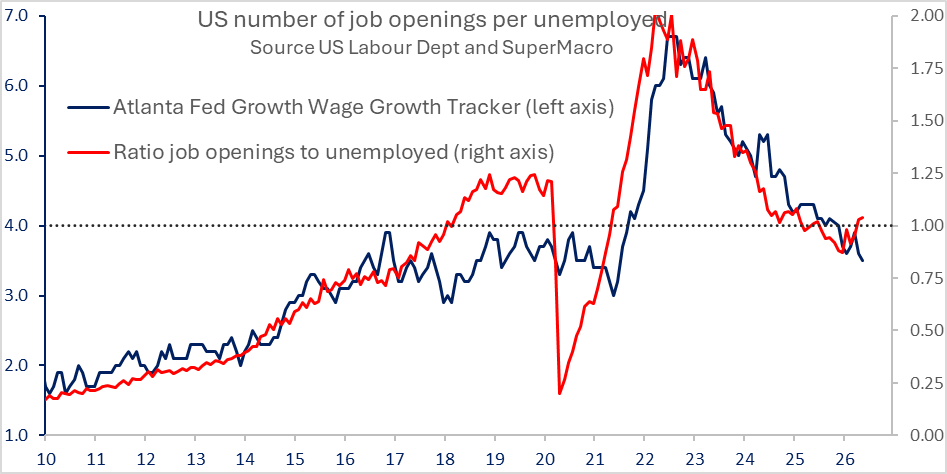

Bargaining power is shifting back to workers

JOLTS beat expectations and the number of openings per unemployed was above 1 for a second straight month. The survey is lagging and imperfect - but the message is clear: demand for workers is rising into restricted supply. Our weekend note discusses the implications

When oil and yields stop moving together, it signals the Fed's problem has shifted from headline to core... cheaper oil alone won't open the door to cuts

-Torsten at Apollo

Went under the radar a tad y'day, but Korean exports were down 3.4% for June...Recall a chart from old of the correlation with the US ISM manufacturing (out 2 July) - the market expects 55.8, the Korean exports suggest downside here

That suggest downside for SPX EPS

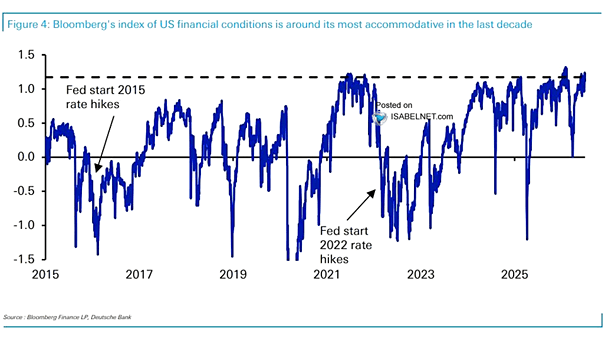

The Bloomberg U.S. Financial Conditions Index is at one of its most accommodative levels in years, which is helping to support the bullish undertone of the market, at least for now.

h/t @ISABELNET_SA

Maturity is a leverage slider for options.

On a short time frame, the option return ≈ spot return x Ω.

Ω = Δ·S / C, i.e. delta x spot divided by premium, aka 'omega'.

As the chart shows:

• Ω amplifies the spot move

• Ω is higher for short maturities

Explanation.

For an ATM option, premium scales roughly with σ√T while delta sits near 0.5, so cutting maturity shrinks the denominator without shrinking the numerator. The second factor is gamma: for short-dated options, the delta changes more for a given price move. Therefore, short-dated options are more convex.

The challenge is that, empirically, front-end implied vol tends to be more overpriced. You usually pay too much in theta for the gamma you get.

That said, the simple fact remains that if you're right on direction and timing, short-dated options give higher returns. Delta is king. It dominates vega and gamma-theta. And the option does not charge you for delta, only for vol.

Hownership base of government bonds is changing. With less QE, holdings of central banks are decresing, with increasing weights of foreign holders.

In Eurozone we can see that hedge funds volumes in trading increased in last years.

OIL

Managed Money short positions >40% (third highest reading in 15 years + Record crack spreads = recipe for a solid bottom.

The question is how big will the bounce be?

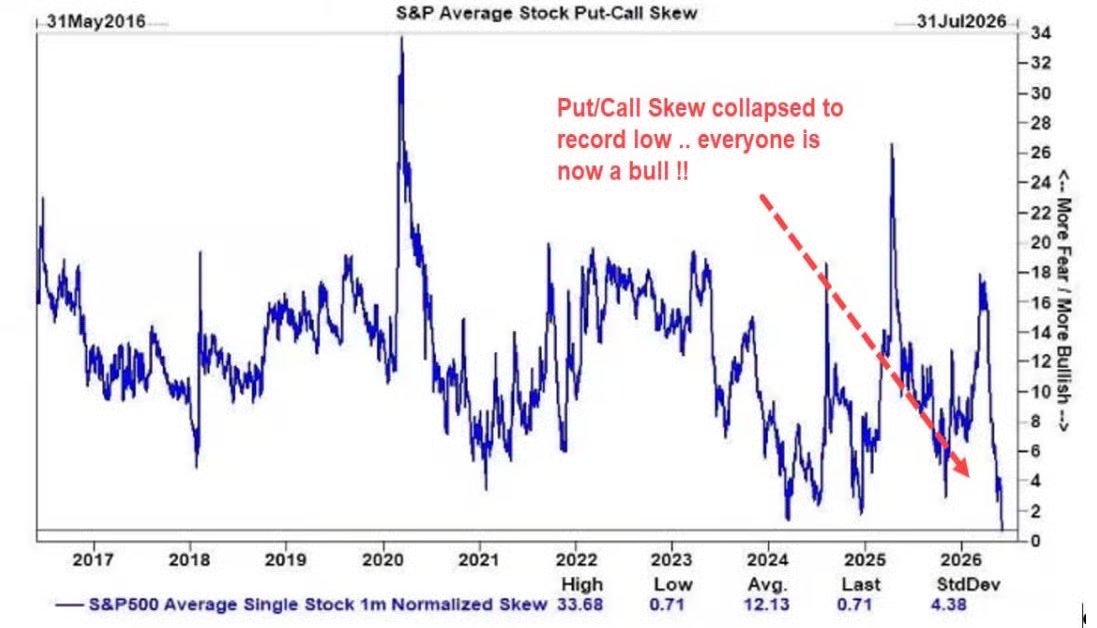

"The S&P put/call skew just collapsed to 0.71. Not a low. The lowest reading on record ... crash protection is essentially free. Nobody wants it."

Goldman Sachs via @ThierryBorgeat

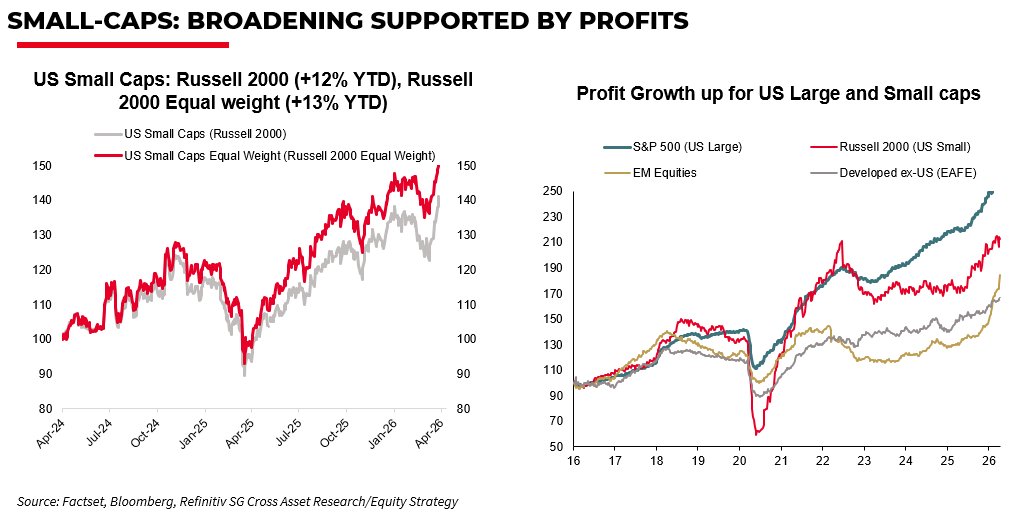

"One of the better places for broadening surprisingly is the US Small caps. Russell 2000 up ~12% YTD and equal‑weight small caps up ~13% YTD. Broadening has been visible since the profit cycle for small firms bottomed in early’25."

-SocGen Kabra

BofA FMS shows investors fully positioned for a 2026 profit boom—PMI and EPS acceleration powered by rate, tax, and tariff cuts.

But: …no Fed QE, no weaker oil, no affordability boost = CPI, yields, and the USD squeeze real returns.

Eurozone May PPI:

m/m +0.2% (est +0.2%, last +0.7% from +0.6%)

y/y +5.9% (est +5.8%, last +5.0% from +4.9%)

The PPI came in in line with consensus in May. Meanwhile, the Global Supply Chain Pressure Index edged lower last month, suggesting that price pressures have likely peaked