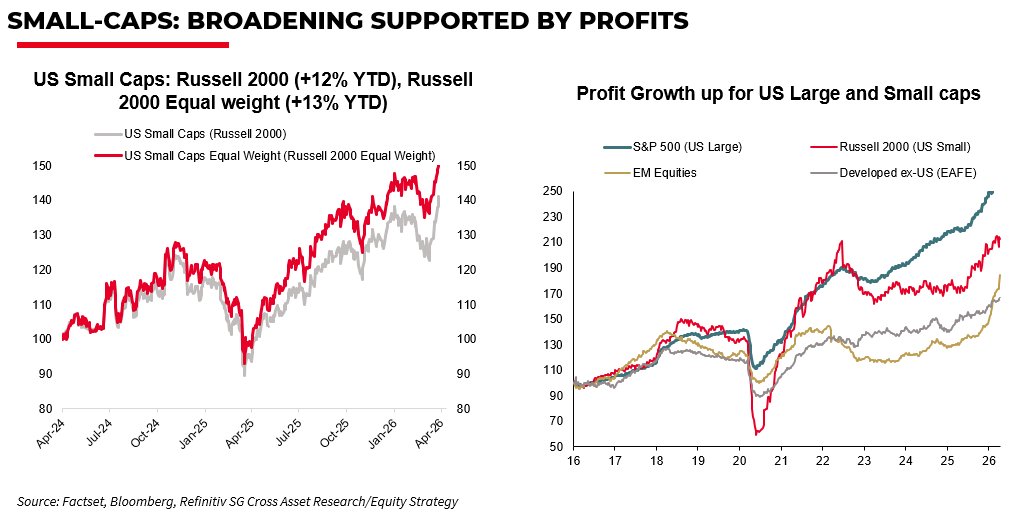

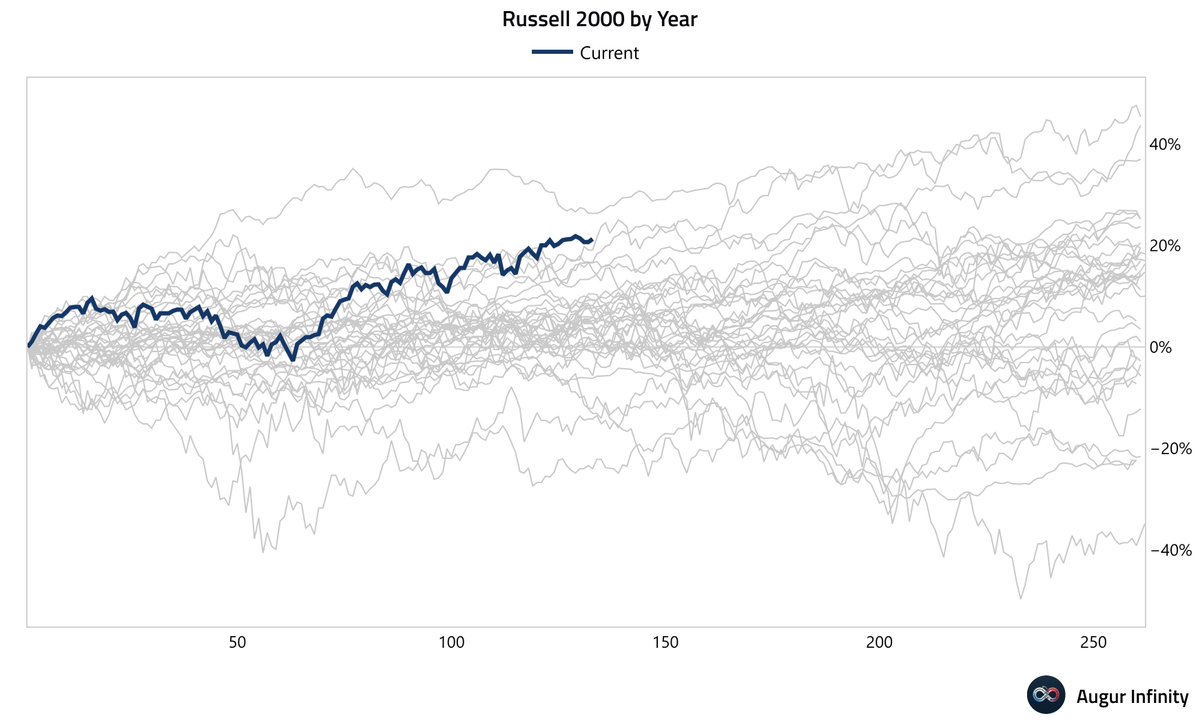

"One of the better places for broadening surprisingly is the US Small caps. Russell 2000 up ~12% YTD and equal‑weight small caps up ~13% YTD. Broadening has been visible since the profit cycle for small firms bottomed in early’25."

-SocGen Kabra

BofA FMS shows investors fully positioned for a 2026 profit boom—PMI and EPS acceleration powered by rate, tax, and tariff cuts.

But: …no Fed QE, no weaker oil, no affordability boost = CPI, yields, and the USD squeeze real returns.

Eurozone May PPI:

m/m +0.2% (est +0.2%, last +0.7% from +0.6%)

y/y +5.9% (est +5.8%, last +5.0% from +4.9%)

The PPI came in in line with consensus in May. Meanwhile, the Global Supply Chain Pressure Index edged lower last month, suggesting that price pressures have likely peaked

The rotation in markets has been violent but encouraging for some equity investors. While traders sold tech stocks last week, they bought everything else, with the equal-weighted S&P outperforming the market-cap index by the most since 2020. h/t @DRBCurtis

Morgan Stanley’s message is nuanced. They are not turning bearish on AI. They are arguing that the memory trade is transitioning from its explosive first phase into a more normal phase of the cycle.

The key question investors are debating is whether hyperscalers, particularly the largest AI infrastructure buyers, are beginning to accumulate excess compute capacity. If some AI infrastructure is no longer fully utilized and starts being resold or leased to third parties, pricing power for GPUs and memory could moderate. Morgan Stanley refers to this as “chipflation,” where competition and excess capacity gradually reduce hardware pricing.

Memory remains one of the strongest beneficiaries of AI because HBM and DRAM demand continues to outstrip supply. However, Morgan Stanley notes that several leading indicators are approaching peak momentum. Memory pricing growth is slowing, inventory conditions have normalized considerably, and earnings revisions have already been overwhelmingly positive. Historically, this combination often marks the point where share prices consolidate even though fundamentals remain healthy.

Importantly, they distinguish between a peak in the rate of change and a peak in the cycle. Those are very different. Investors frequently confuse slowing growth with declining growth. Semiconductor stocks often begin correcting once earnings momentum becomes “less good,” even while profits continue reaching record highs.

Another concern is positioning. Memory has become one of the most crowded trades globally, with investors heavily concentrated in names such as Samsung, SK Hynix, and Micron. When positioning becomes this crowded, even minor disappointments during earnings season can trigger sharp pullbacks as investors take profits.

What Morgan Stanley will be watching most closely is not memory companies themselves, but the AI hyperscalers. If companies such as Microsoft, Amazon, Meta, Alphabet, or OpenAI begin signaling slower infrastructure spending, weaker token economics, or more disciplined capital allocation, investors may question how sustainable the current pace of memory demand will remain. The focus is shifting from hardware suppliers toward the spending intentions of the customers.

The long-term thesis, however, remains intact. Morgan Stanley still expects AI-related earnings growth of roughly 35% to 40% in 2027 and continues to view agentic AI as a structural investment theme. Their message is that the AI infrastructure build-out is unlikely to end, but the market may be entering a period where expectations become more realistic and valuation expansion gives way to earnings-driven returns.

In other words, this looks less like the end of the AI memory supercycle and more like the transition from Phase One, characterized by explosive hardware deployment, to Phase Two, where investors become increasingly focused on utilization, monetization, and return on capital.

We broadly share that view. Markets often correct when expectations become overly optimistic, even while fundamentals remain strong. AI infrastructure spending is unlikely to follow a straight line, but the long-term demand for high-performance memory continues to strengthen as model sizes grow and inference workloads expand. We view the current pullback as an opportunity to selectively add exposure to high-quality memory names rather than a reason to abandon the sector. In our view, this is a correction to buy, not the beginning of a structural downturn.

At this point, implied correlations only rise 1 of 2 ways.

Either single-name vol compresses hard, which is unlikely given the concentration in semis, or $SPX vol catches up.

And if the whole signal is just $SPX vol catching up, you might as well just watch $SPX vol directly.

The services demand pulse cooled, but it did not break.

ISM Services PMI slipped to 54.0 from 54.5. New Orders slipped to 55.1 from 57.3.

Both are still above 50, so this is expansion at a slower rate rather than outright contraction. The next question is whether market cyclicals and earnings confirm the survey.

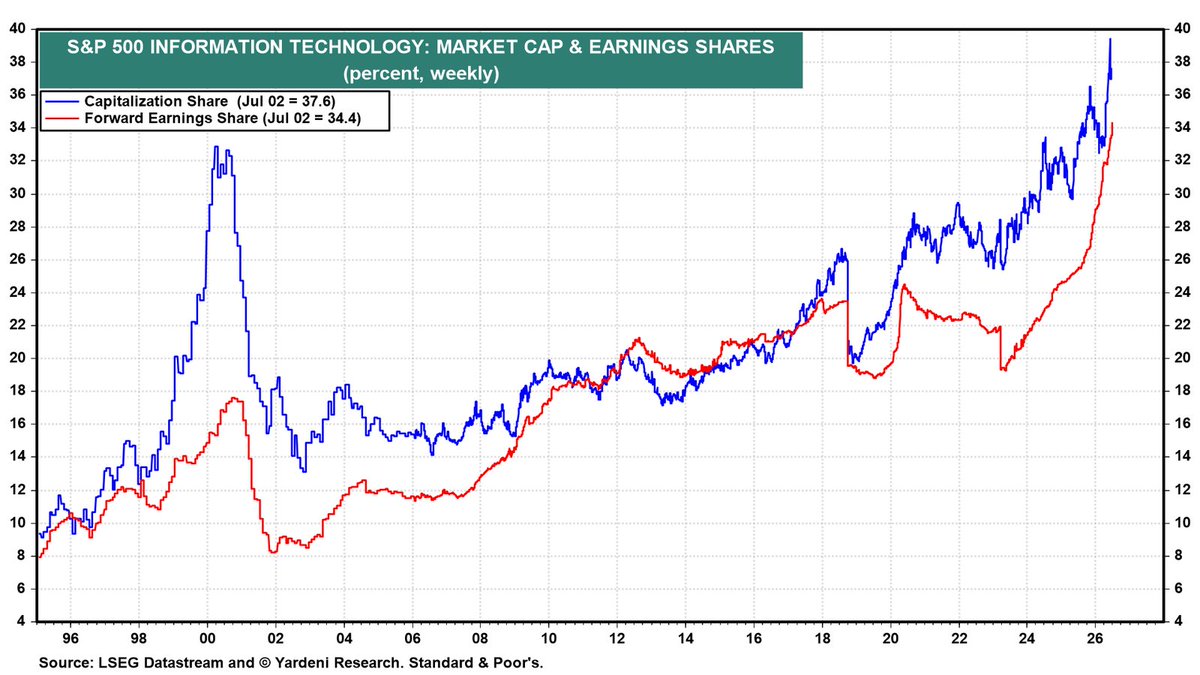

Yardeni Research Chart of the Day (July 6, 2026)

Then vs. now: the 1990s tech meltup was FOMO-fueled speculation. Today's S&P 500 IT sector re-rating reflects FEMO — fabulous earnings momentum. Sentiment drove the last peak. Fundamentals are driving this one. Can earnings keep delivering?

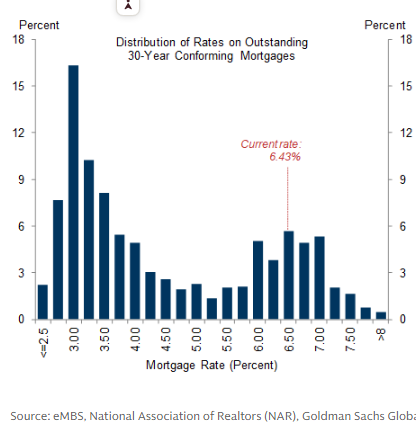

GS: Almost 80% of Borrowers Have Mortgage Rates Below Current Market Rates...We Expect Existing Home Sales to Rebound Only Modestly Over the Next Couple of Years

Crack spreads (the per-barrel spread between crude and products) hit a new all-time high today, indicating massive margins for refiners.

per @bespokeinvest

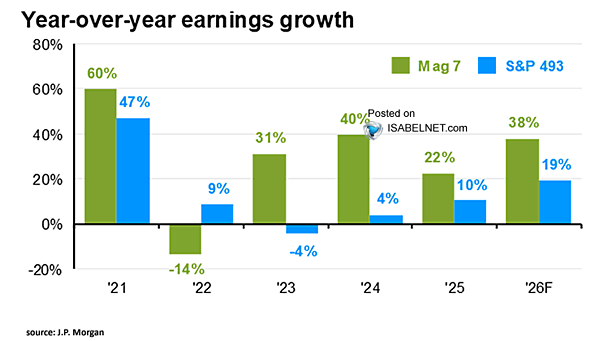

The Mag 7 is Losing?

"Nothing outperforms forever. Expectations change. Investor flows go to where there is value or momentum. The winners never win forever. Even the biggest, best corporations in the world underperform sometimes."

https://t.co/UuexrMpmth

by @awealthofcs

Companies beat earnings expectations every quarter for many years at this point. They are good at guiding and then beating.

Expectations are highest for this quarter since 2021. If they beat here, we may see perma-bears capitulate ("estimates are too high!").