Historically, Bitcoin’s biggest bull runs began after the MVRV Z-Score dropped below 0 during bear markets.

If $BTC falls toward the $38K–$48K range, the indicator could enter that zone again, potentially setting up the next major bull run.

Gold volatility is now ~2.3x the S&P 500, a level last seen before 2008.

Historically, this shows stress in how risk is being priced across assets, not just strength in gold.

If this regime holds, equities carry a heavier load to keep broader risk assets supported.

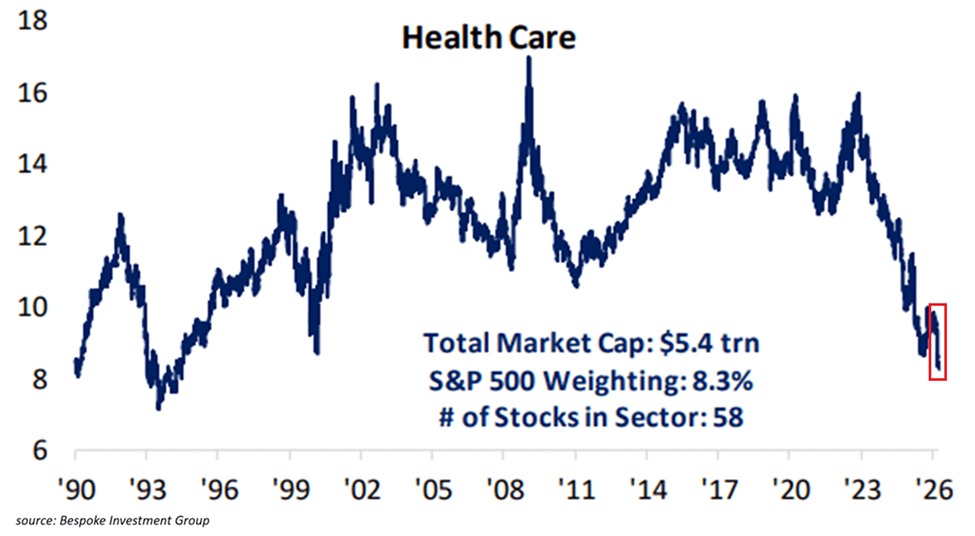

Defensive stocks have never been this disliked:

The healthcare sector now accounts for just 8.3% of the S&P 500’s market cap, the lowest percentage since 1994.

Their weight has fallen by -50% since the 2022 bear market.

By comparison, healthcare represented ~9.0% of the index’s value at the 2000 Dot-Com Bubble peak.

Furthermore, consumer staples, healthcare, and utilities collectively now account for just ~15% of the S&P 500’s market cap, the lowest since at least the 1970s.

Their weighting has dropped -12 percentage points since 2022, marking an even bigger drop than during the Dot-Com run.

Tech stocks have never been bigger.

If you invested $1000 in each asset at the beginning of 2025, this is your money now:

Silver — $2650

Gold — $1600

Copper — $1430

NVIDIA — $1400

NASDAQ — $1210

S&P 500 — $1140

Bitcoin — $950

Ethereum — $895

$XAGUSD $XAUUSD $XCUUSD $NVDA $NQ $BTC $ETH $SP

$Silver has a credible runway to the $58 - $61 range by end-2025, driven by rate-cut tailwinds, accelerating industrial demand (solar + EV), tight supply, sticky inflation, and persistent geopolitical risk.