As of today (May 28), all three memory giants crossed $1T market cap.

Mu : $1.05t

Skhynix(000660) : $1.08t

Nearly identical market caps.

But are they doing the same thing?

HBM Global Market Share:

SK Hynix: 53%

Micron: 11%

Why Korean Stocks Have More Room to Run

Reason 3: The Normalization of Korean Stock Market

Some say Korean stocks have risen too fast. But the real story is the opposite. they were suppressed for too long.

Korean markets lacked proper legal protections for shareholders. Duplicate listings, dilutive share issuances, and market manipulation were rampant.

That's changing now. Shareholder protection has been codified into law, and anti-market practices are being banned. The market is simply normalizing.

That normalization happened to coincide with the AI cycle, which accelerated the rally.

And yet, forward PE is still just 7~8x(at 7,800pt). This is not an overvalued market.

<That "South Korea wants to take AI profits from Samsung" headline? Misleading>

1. Here's what Kim actually write on his SNS :

- The "AI Citizen Dividend" draws from EXCESS TAX REVENUE — corporate taxes that surge as AI drives profits

- Kim himself clarified: he is NOT proposing to seize or redistribute company profits

2. The real argument is simpler and smarter:

- AI will generate a windfall of corporate tax revenue

- So let's have a serious conversation about how to use it well — for citizens

That's fiscal policy debate, not profit expropriation.

Why Korean Stocks Have More Room to Run

Reason 2: Korea Is a Full-Stack Manufacturing Superpower

People keep framing KOSPI as a "memory chip trade." That's missing the bigger picture. Yes, Samsung and SK Hynix are world-class.

But look at what else sits in this market:

- Shipbuilding #2 globally — with 65%+ of all LNG carrier orders (OECD, 2024).

- Transformers #1 in North America — right as the AI data center buildout is driving a once-in-a-generation grid upgrade supercycle.

- Defense #9 globally and rising fast — Europe is buying K2 tanks and K9 howitzers faster than Western suppliers can deliver.

- Automotive #4 — pivoting hard into EVs and software-defined vehicles.

- Cosmetics #3 — K-Beauty is becoming a genuine global consumer franchise.

- Nuclear Top 5 — as the world rediscovers that clean baseload power is not optional.

Each of these sectors is in a structural upcycle. AI infrastructure, energy transition — they're all tailwinds hitting Korean manufacturers at the same time.

The memory chip rally got there first. The rest of KOSPI is just starting to get priced in.

Image credit: @going_tothe_moon (Instagram) — Translation of original infographic

Why Korean Stocks Have More Room to Run

Reason 1: Korea's Great Money Move — From Real Estate to Equities

- Korea locks 64.5% of household wealth in real estate. US? 32%. Japan? 36.4%. The imbalance is extreme.

- The government just declared war on property hoarding. Multi-home bans. Mortgage crackdowns. Holding tax expansion. The rules of the game are changing.

- Korea's real estate market is ~$16T. If 20% rotates into equities = $3.2T of fresh demand. Into a stock market worth $3.9T today (KOSPI 6,930).

= Do the math. That's a rerating toward KOSPI 12,000+!!!

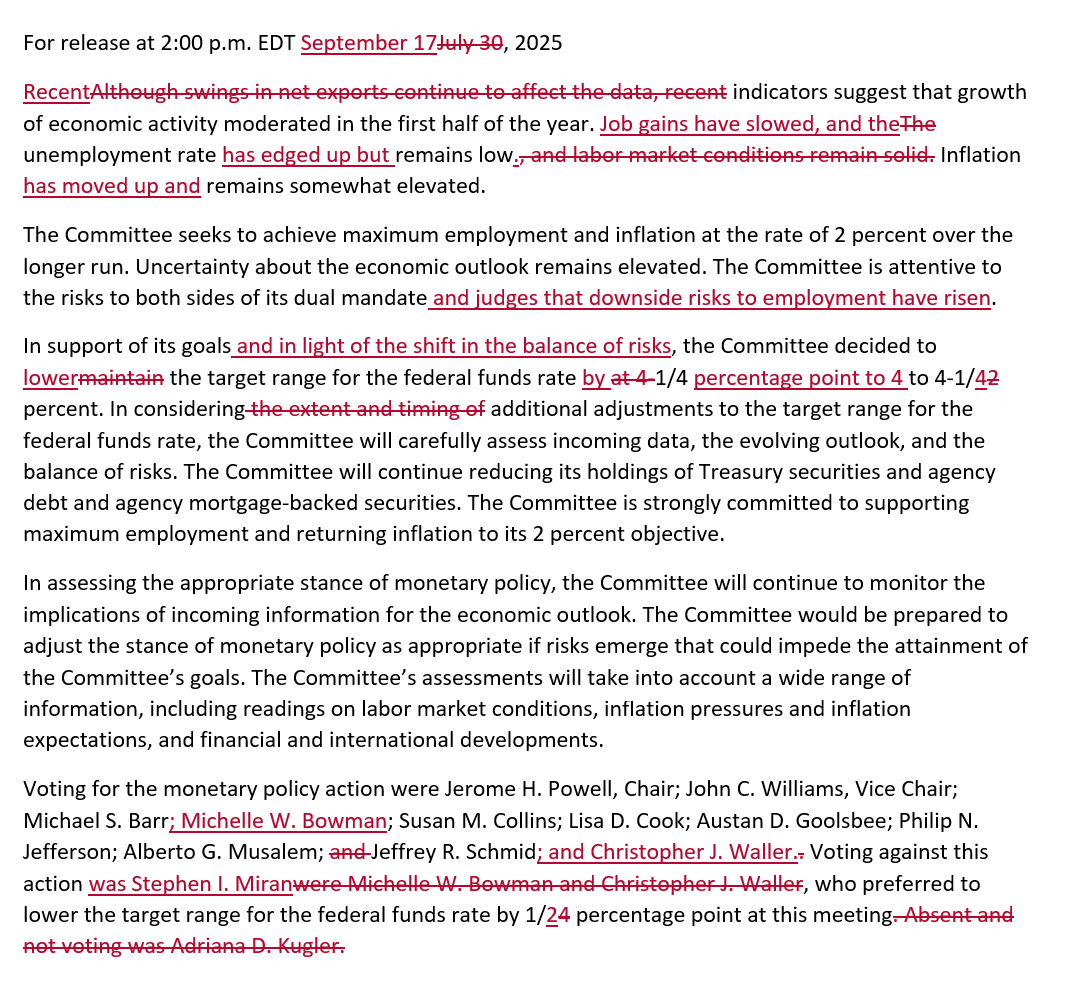

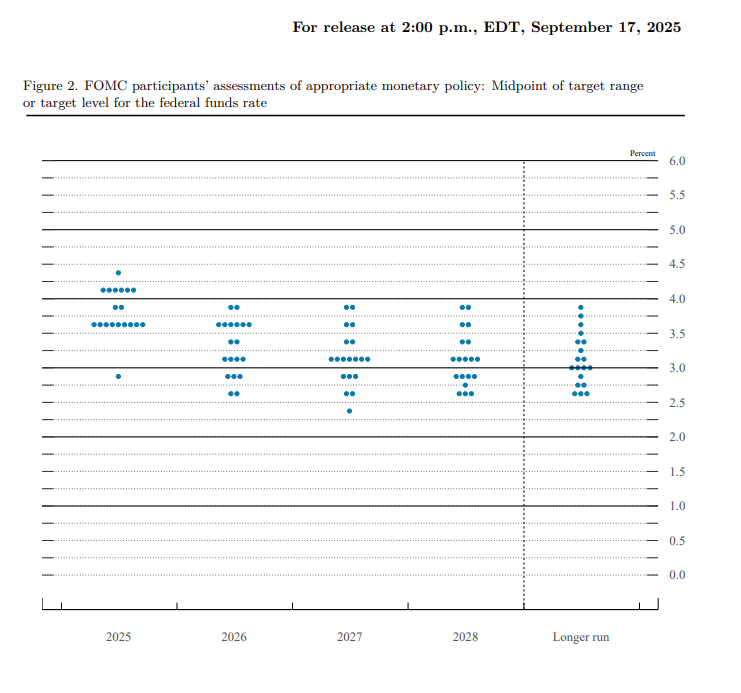

September FOMC

*The Fed cuts rates by 25 bps

*A narrow majority of officials pencil in a total of at least 3 cuts this year

*Statement changes are dovish

*Miran is the only dissent, for 50 bps

I think the Fed should cut by 50 bp. I feel we overanalyze each data point for what it means on timing & size of rate move rather than ask what *level* of rates is appropriate. I think it's obvious the right level is well below where we are now. My reasons ... https://t.co/IXOGnF9SH5

Headline CPI slowed to 2.5% in August, the lowest since February 2021.

The six-month annualized rate fell to 2%, which is the lowest since September 2020.