We can see how buy-side institutions are hedging by looking at sector transaction volume flows; e.g., over the last 6 months, real estate sector risk has been (i) sold to purchase UST risk, and (ii) bought by selling consumer / healthcare sector risks and foreign equity risks:

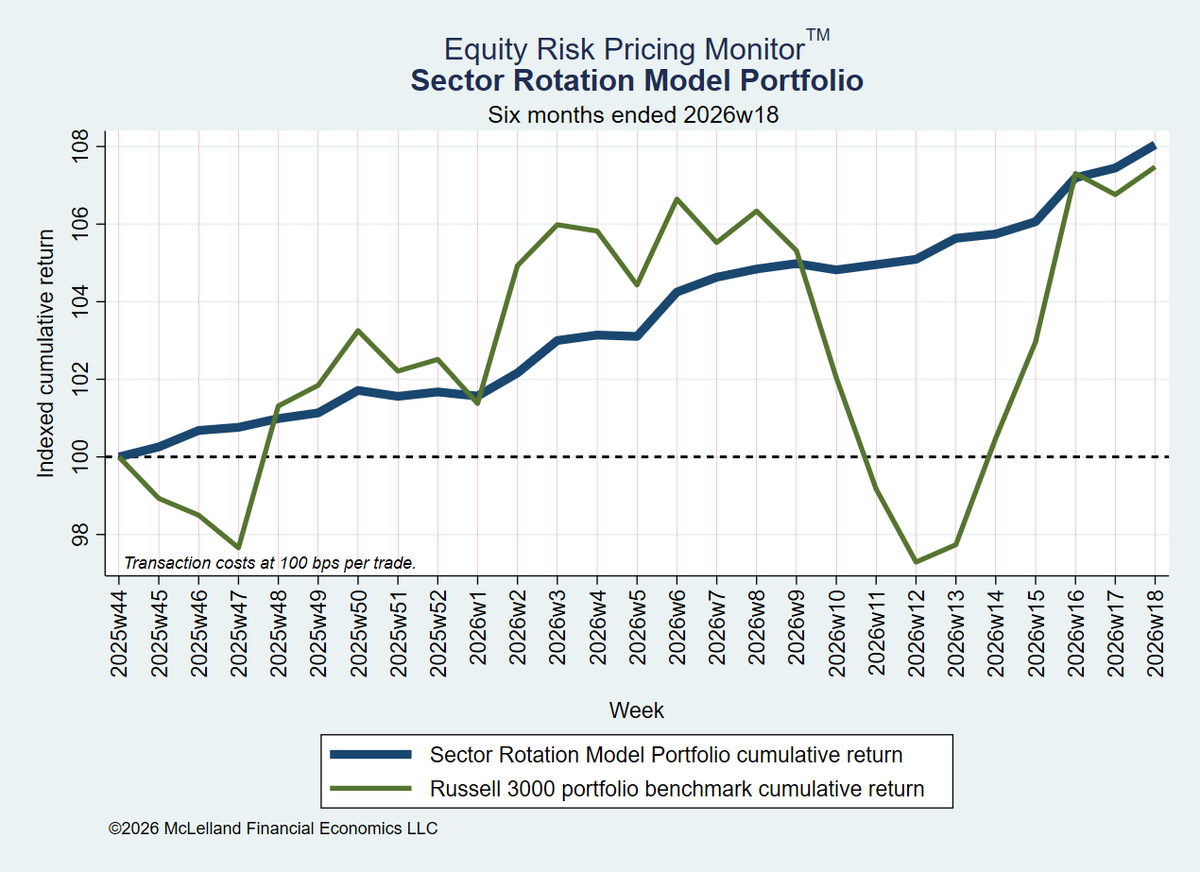

How do buy-side institution portfolios (BlackRock et al.) perform relative to overall market indices and why? Slightly-but-noticeably-better return with low volatility by low cost hedging via *trading risks* in the most liquid symbols. Consider a buy-side-replicating portfolio:

@MarketWatch The question above is actually a false dichotomy, but it's always important to think about what risk has and hasn't already been priced into equities.

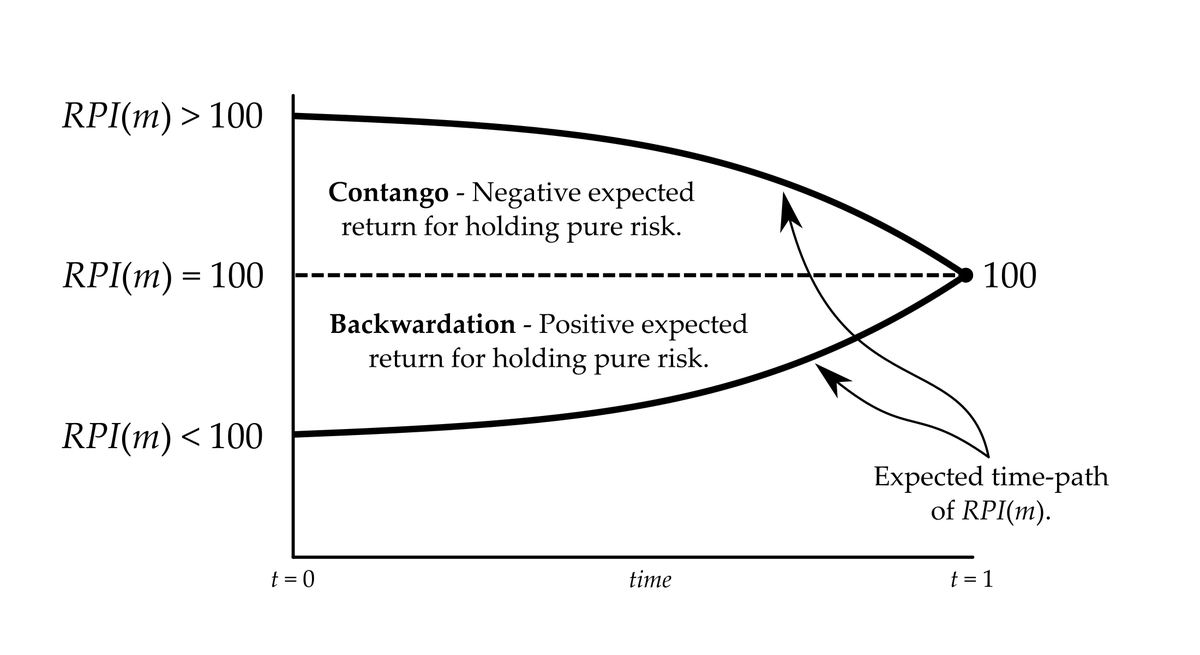

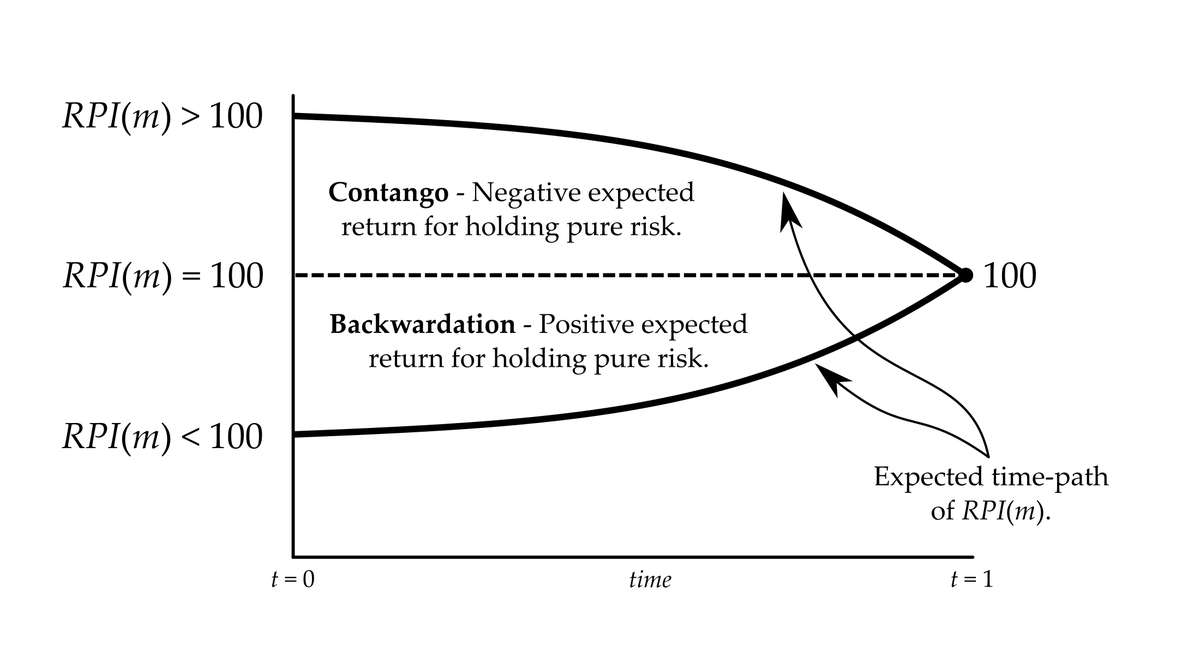

Although abstract, #risk_contango is precisely this condition; i.e., as sensitivity to (any) risk increases, expected capital asset returns decrease, which implies a negative expected return to holding the risk:

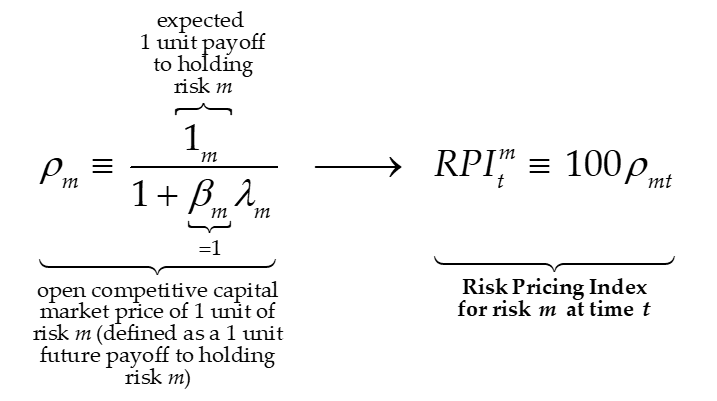

What is a 'risk price index' (for a pure risk)? In simple terms, it is a risk-adjusted present value factor for an expected cash flow resulting from holding a pure risk multiplied by 100 (constructed from the no-arbitrage expected rate of return for a pure risk): #arbitrage#risk

What is a 'risk price index' for a capital asset? Most simply, it is a risk-adjusted PV factor based on risk factors relevant to the asset multiplied by 100; i.e., the expected PV of a 100 monetary unit payoff to holding the asset based on its sensitivities to the risk factors:

@EdKrassen Free speech issues aside--and I do think Congressman Green has the right to be heard--repeatedly yelling (?) “You have no mandate to cut Medicaid!” hardly constitutes meaningful speech or criticism of the new administration. I think we should all aspire to rise above idiocracy.

@chamath Yep, this time is different: As Mr. Palihapitiya has suggested elsewhere (e.g., on CNBC), in pathological feedback cycles *things get progressively worse* ... at least until the cycles fail. Sadly, this might take some time: https://t.co/IHxopJ3U59