Next Bridge Hydrocarbons Announces SEC Declares Effective its S-1 Registration Statement

Company prices and commences a public offering of 40 million shares

https://t.co/2hO7KuPeJJ

🚨Breaking news: 🦋

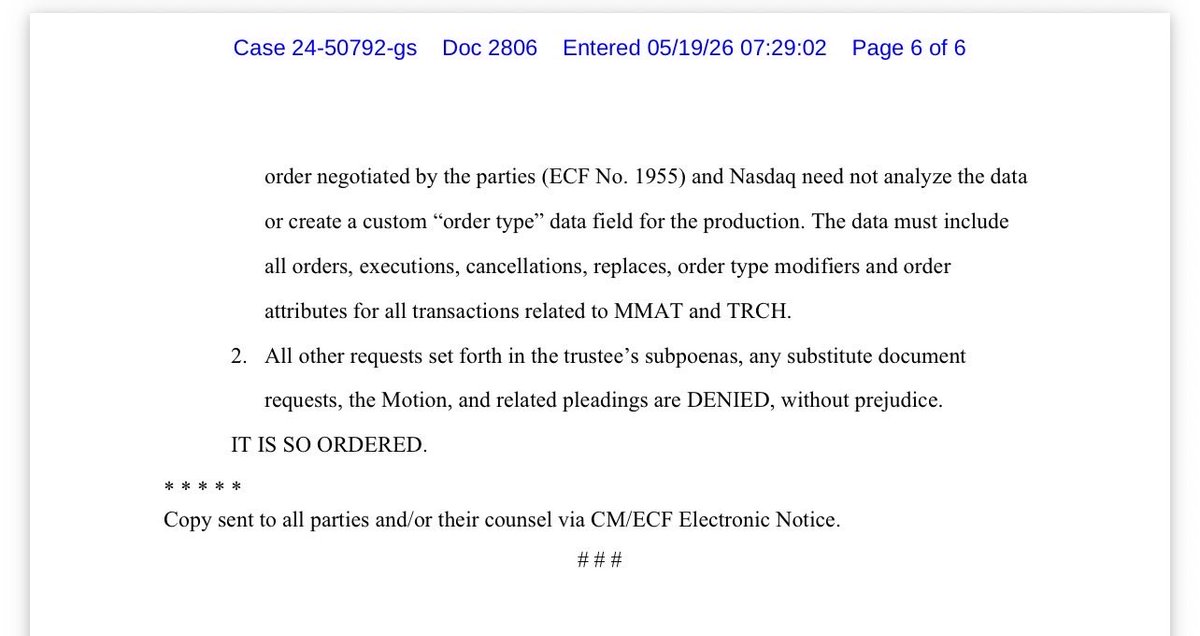

@Nasdaq just LOST its Motion to Quash.

Read that again s l o w l y . . .

The Bankruptcy Court in Nevada has now ordered Nasdaq to produce extensive $MMAT/TRCH trading data under Rule 2004, including RASH and CORE data, order attributes, cancellations, replaces, executions, and related transaction records covering nearly FOUR YEARS.

The Court was NOT persuaded by the ‘undue burden’ argument, noting that producing ~15GB of spreadsheet data is not exactly impossible for… Nasdaq. (One $10 usb stick)

Even more important, the Court explicitly recognized the Trustee’s AUTHORITY to investigate whether wrongdoing occurred on behalf of the estate, including potential claims tied to stock trading activity.

Translation:

This investigation is very much ALIVE.

For months, some people mocked and undermined the Trustee’s efforts, claimed discovery would never happen, and acted like every subpoena didn’t get served initially and that it would be crushed before daylight. Instead, the wall keeps cracking.

FINRA discovery.

Now Nasdaq discovery.

And the Court explicitly referenced separate pending motions involving Citadel, Virtu, and Anson.

Interesting times ahead.

Turns out Rule 2004 is not just a decorative suggestion.

To the Trustee and legal teams, incredible respect.

It takes courage to walk into rooms filled with institutions that have virtually unlimited resources and say:

‘Produce the data’

And to the echo chambers already warming up their spin machines tonight…

You may want to read the actual order first. 🤝

Blessings to all.

@Giftsonglass She literally had Massie by the balls... was a congressional staffer, and yet was the most quiet about mmtlp during that time. Odd... regardless it doesn't matter. It's all on Mccabe. Just shows congress really doesn't care...... not even hopeful on the executive action w Trump

@MakeAWish Be careful with interacting with these crypto folks and pumpfun in general. While it's nice the money is being donated to an awesome charity like MakeAWish, when the inevitable dump happens one day.... you will be caught in the bad pr being blamed.

@nikitabier Oh..... what a ridiculous take lol. Anyhow how about this gem....

https://t.co/ulEehcmUwE

Sounds like something a commie would say.... or even worse, a full blown dictator.

⏰🔥Breaking News:

I recently learned that Mrs Samantha Martin, who led the investigative side of the @johnbrda +me SEC case, is NO LONGER with the SEC Fort Worth...

Mr Chris Rogers, who worked under that structure, is also NO LONGER there, they left within weeks from eachother.

When key SEC investigators leave, how is continuity of understanding preserved?

No accusations, just facts

What remains is a trial team holding a file,

working from a record built by people who aren’t in the room anymore.

I am not a lawyer but from what i am told, in complex cases, especially ones involving emerging high-technology and market structure integrity (they called it a novel case), the difference between reading the file and understanding the case is everything.

When institutional knowledge walks out the door,

what remains is interpretation.

And interpretation… is where things get interesting.

What is our fearless CEO up to? Hmmmmmm…

I have my suspicions… But, we will save that for another day.

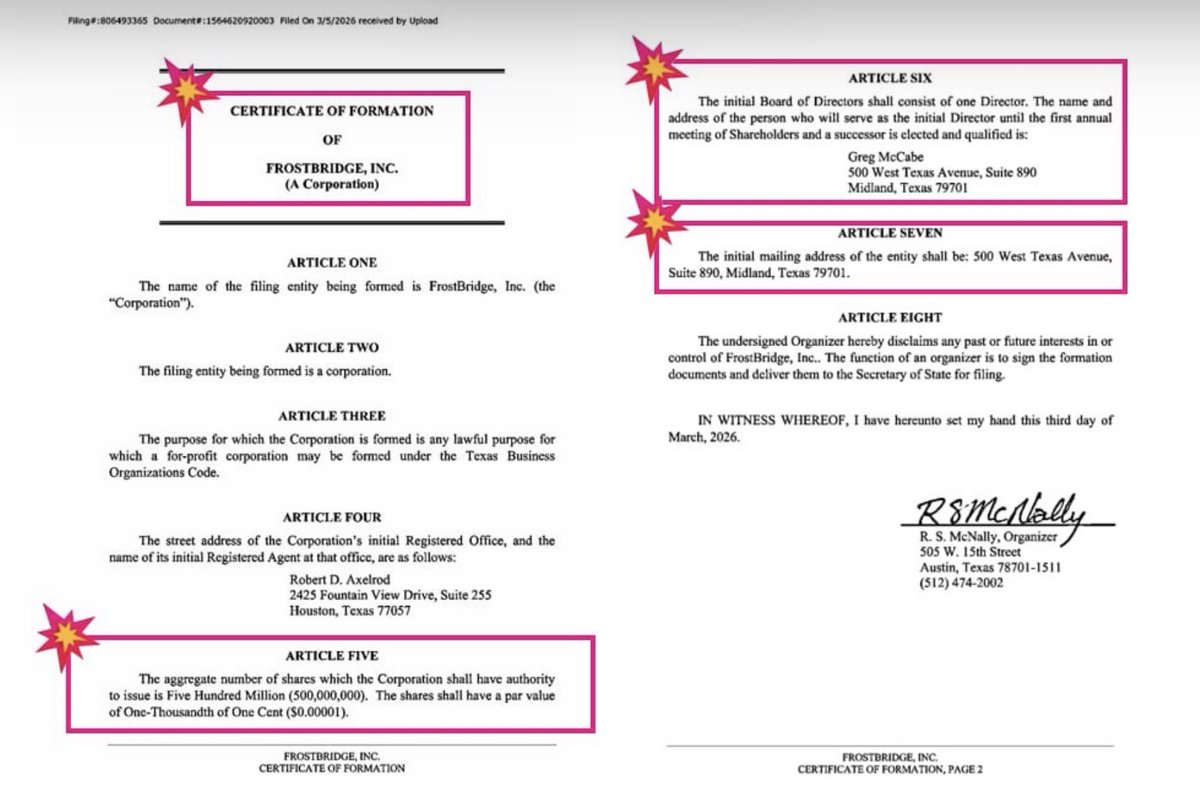

- Same director name ✅

- Same sole principal

on record ✅

- Same registered address ✅

- Same # of authorized shares ✅

If there’s anything we’ve learned in the #MMTLPfiasco, there are NO coincidences.😉

💥Bonus: FrostBridge, Inc. (FBI) LFGooooooo!!!

#MMTLParmy $MMTLP $MMAT #Relentless #FIF

1/ Dear @SECPaulSAtkins and Commissioner @HesterPeirce@SECGov

Regarding your posts earlier today I think there are important questions arising especially in context with a related FSB report.

I will be discussing below the Operational Classification vs. Legal Classification of #MMTLP, specifically:

The divergence between LEGAL classification and OPERATIONAL handling of MMTLP, and how this mismatch may have contributed to:

1. supervisory fragmentation,

2. regulatory blind spots, and

3. OTC’s ultimate settlement failure.

Key Findings:

While MMTLP was publicly characterized as an OTC equity preferred security, evidence indicates that at least one major broker-dealer (@Fidelity) processed buy-side activity through a fixed income desk, suggesting a MATERIAL divergence between legal classification and operational treatment.

This divergence is NOT merely administrative, it has direct implications for:

1. supervisory responsibility

2. compliance rule application

3. surveillance coverage and

4. settlement risk management

MMTLP wasn’t just an “equity” security that went wrong, it became a cross-system instrument processed through equity, derivatives, and “fixed-income” infrastructure simultaneously, and that fragmentation created a supervisory and settlement blind spot that no single regulator or broker fully controlled, in my opinion.

BREAKING… weather forecast for tomorrow:

it’s going to rain very hard. Stay inside, get some nice🥤 and buttery🍿 and watch the new blockbuster movie: “Silence of the 🦝” followed by the all time classic: “Apocalypse Now” #SunshineThroughTheFogOfWar#LFGB

OPEN LETTER TO @SECGov INSPECTOR GENERAL

Subject: Request for Review, FOIA Processing Integrity, MMTLP-Related Requests, Outcome and Delay Disparities

Dear Inspector General,

I am writing to request that the Office of Inspector General review FOIA processing practices affecting requests related to MMTLP and the December 9, 2022 U3 trading halt.

Based on FOIA log analysis and request tracking compiled by the public and community requesters, a large proportion of MMTLP-related FOIAs experience extended delays and procedural parking states, including “Referral Request” and “On Hold,” with some requests remaining pending for more than a year and, in certain categories, with median pending times exceeding two years.

Separately, the updated SEC-wide vs MMTLP roll-up indicates a large outcome disparity, where MMTLP-tagged requests receive full or partial disclosure at a substantially lower rate than SEC-wide FOIAs, while B7 exemption outcomes are substantially more prevalent in MMTLP-tagged requests. These patterns, taken together, raise process-integrity concerns that delay can become functional denial, particularly when information is time-sensitive for oversight, bankruptcy proceedings, or public accountability.

I respectfully request an OIG review focused on:

1.Time-in-status controls: Median and maximum duration in “Referral Request,” “On Hold,” and “Perfected” statuses, and whether escalation triggers exist.

2.Bundling practices: Criteria for bundling, notice to requesters, opt-out availability, and measurable impact of bundling on timeliness and outcomes.

3.Outcome disparity: Comparison of disclosure outcomes and exemption usage between MMTLP-tagged and baseline SEC FOIAs, controlling for request scope and subject matter.

4.Transparency of extensions: Whether the SEC logs and reports extension counts and delay events per request ID, and whether the current system understates delay frequency.

For convenience, I can provide the supporting spreadsheets and PDFs, including top longest-pending and most-delayed request IDs and category-level pending-day statistics.

Thank you for your consideration. I am available to provide the supporting materials, methodology, and any additional context your office may require, you have all my contact information on file.

Sincerely,

George Palikaras

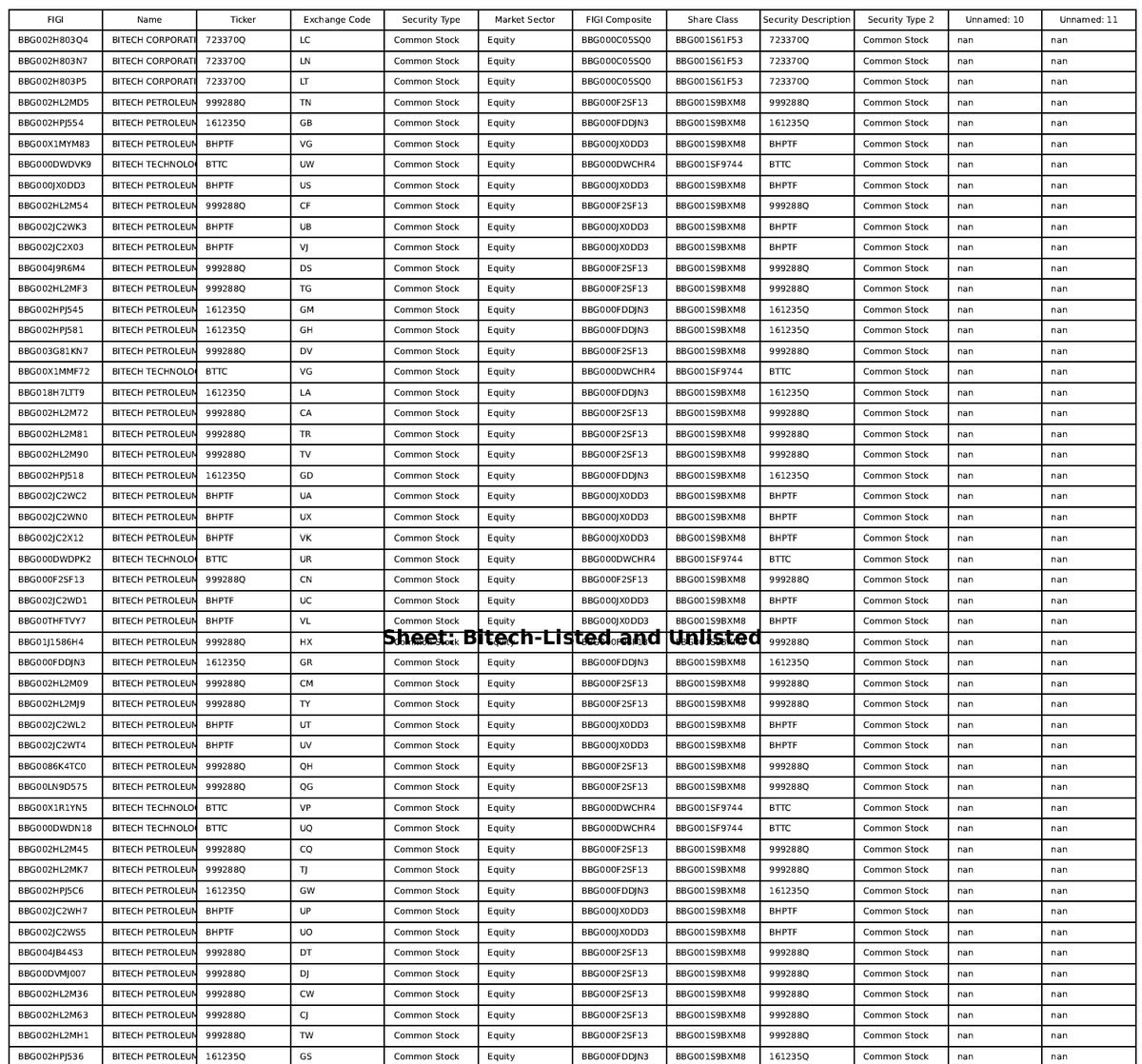

Thank you Kristen. We have been running a deep AI dive on $BESS market infrastructure presence...

So far, what I can say is our initial analysis shows at least 92 associated securities with unique identifiers, with 80% are UNLISTED and mostly in America...

(happy to share the list below image is about 1/3 for your information), confirming that these securities were deliberately created and maintained within market infrastructure systems.

However, there is extreme proliferation at the FIGI Composite level, with dozens of structurally distinct instruments referencing the same underlying economic security.

Many of these instruments do not participate in public price discovery, yet persist across jurisdictional and custodial systems, creating ambiguity around true exposure, settlement pathways, and disclosure obligations...

Given the "innocent" CUSIP recycling error in 2023-2024 by one of its shareholder and then separately by the company, that their leadership made we will be closely following this.

This is not financial advice. If I was a $BESS shareholder or $MMTLP participant (looking for some assurances that the two are not associated any more), I would submit some FOIA-style questions about the listed vs unlisted instruments, DTCC eligibility, margin treatment, lifecycle events, and who created or maintained the security master records.

Below is an example structure (for entertainment purposes), whether you’re sending to the SEC, FINRA, or (if applicable) any agency holding market-surveillance records.

Request scope (keep it narrow and mechanical):

example Timeframe: January 1, 2020 to present

example Subject: Security master, identifier creation, and instrument classification for $BESS-related issuer identifiers (list your issuer legal names and tickers)

exam[le Data types: CUSIP, FIGI, Exchange Code, Composite FIGI mapping, eligibility flags, lifecycle status, and associated correspondence

Format request:

“Produce in machine-readable format, including native exports where available, with all metadata fields.”

example Deconfliction request:

“If any portion is deemed overbroad, produce responsive records for the most recent 12 months first, and identify the additional custodians and repositories needed for the remaining period.”

example Expedited processing (optional, if you can justify for example due to the NYSE pending listing, etc):

“This request concerns potential systemic market integrity issues and public confidence, including inconsistencies in security master records and instrument classification that may affect investors.”

2. example FOIA-style questions that may offer useful information or not:

A. Identifier creation and provenance (who created what, when, and why)

For each security object tied to the issuer(s), produce a table containing:

-Identifier type (CUSIP, FIGI, etc.)

-Identifier value

-Security name

-Market / exchange code

-Share class / instrument type

-Date created

-Date modified

-Current status (active, inactive, cancelled)

-Reason code or free-text reason for creation, if maintained

Produce records showing who requested, approved, or initiated creation of each identifier or security master entry, including:

-Request tickets, emails, or internal forms

-System logs indicating user, department, or vendor source

Produce any security master change logs reflecting:

-Renames

-Reclassifications (listed to OTC, equity to other)

-Exchange code changes

-Corporate action mappings

B. FIGI Composite proliferation (why dozens map to the same economic security)

For each FIGI Composite associated with the issuer(s), produce:

-The list of all instrument-level FIGIs mapping to that composite

-The mapping rationale and rules used (documentation or runbook)

-Any flags indicating “primary listing,” “secondary listing,” “OTC,” “reference-only,” or similar

Produce any internal analyses, exception reports, or QA audits referencing:

“composite mapping anomalies”

“duplicate economic exposure”

“multiple instruments per composite”

“orphan FIGIs” or “stale instruments”

C. DTCC / NSCC / DTC eligibility (settlement plumbing)

For each identifier or instrument tied to the issuer(s), produce any fields indicating:

-DTC eligibility

-NSCC eligibility

-CNS eligibility

Any settlement restrictions or chills

Dates eligibility was granted, modified, or removed

The basis for eligibility status

Produce communications between the agency and any of the following regarding eligibility, settlement status, or instrument classification:

-DTCC

-DTC

-NSCC

(If they claim exemption, ask for an index of withheld items.)

D. OTC, grey market, and “non-price-discovery” status

Produce a list of all instruments tied to issuer(s) that were designated:

-OTC

-Grey market

“unlisted”

“reference-only”

“non-tradable”

“when-issued”

“restricted”

including the designation date and basis.

Produce any policy guidance, internal memos, or surveillance references defining how the agency classifies:

“exchange code present but not exchange-traded”

“reference venues”

“internal market codes”

and how those affect reporting and surveillance.

E. Margin, collateral, and netting treatment (where risk hides)

Produce any records showing whether any issuer-tied instruments were:

-Margin-eligible

-Collateral-eligible

-Eligible for netting sets or offsets

-Subject to special haircuts

Produce any communications or surveillance notes where margin, collateral, or netting concerns were raised due to:

-multiple instruments referencing the same underlying security

-unclear float / unclear exposure

-settlement fails or persistent fails

F. Lifecycle cleanup and corporate actions (did anyone ever close the loop)

Produce corporate action mapping records for the issuer(s), including:

-splits, mergers, name changes, cusip changes

-symbol changes

-cancellations / retirements / conversions

and all impacted identifiers.

Produce any exception logs where a corporate action could not be cleanly processed because:

-security master mismatch

-multiple identifiers for the same economic security

-cross-border share class conflicts

G. Cross-border anomalies (foreign ordinary share tied to U.S. issuer)

Produce records identifying any instruments tied to the issuer(s) that were classified as:

-foreign ordinary shares

-ADRs/GDRs

-depositary receipts

-offshore lines

including the rationale for classification.

Produce any communications discussing why a U.S.-centric issuer had a foreign ordinary share instrument in the security master.

H. Surveillance and internal flags (did the system itself complain)

Produce any surveillance alerts, internal flags, or exception reports referencing:

-abnormal number of identifiers for an issuer

-instrument proliferation

-inconsistent share class definitions

-exchange code inconsistency

-stale or orphaned instruments

Produce any internal discussions where personnel debated whether the inconsistency impaired:

-market surveillance

-consolidated audit trail correlation

-blue sheet reconstruction

-short interest computation

-fails-to-deliver analysis

I. Vendor and data-source responsibility (who fed the machine)

Identify the data sources used for security master ingestion for these issuer(s), including:

-vendor names

-internal feeds

-update frequency

-change-control governance

Produce contracts, SLAs, or governance documents (or excerpts) defining:

-responsibility for error correction

-time-to-correct requirements

-audit frequency for security master accuracy

(If contracts are exempt, request the policy/guidance documents and any QA audit summaries.)

in recent FOIAs we have observed how agencies love to block broad requests. The key would be to ask for structured exports and specific logs.

For example, i would use a tiered approach:

-Tier 1 (hard to deny, cheap to produce)

-The security master tables / exports for specific issuer(s)

-Change logs

-Composite mapping list

Tier 2 (if they push back) then i would:

Limit to “the 6 FIGI Composites identified”

Limit to “top 2 composites by instrument count”

Limit to “most recent 12 months”

Tier 3 (correspondence) i would seek:

Only emails/tickets containing:

“FIGI Composite”

“security master”

“CUSIP change”

“orphan”

“reference-only”

“grey market”

“eligibility”

“fails”

“CNS”

4. A short paragraph i would include in my FOIA would go something like this:

This request seeks objective security master and identifier governance records, including creation, modification, classification, eligibility, and lifecycle status fields, as well as mapping records between instrument-level identifiers and composite identifiers. These records should be maintained in structured databases and logs and can be produced as exports without discretionary narrative. If any portion is withheld, please provide a Vaughn-style index describing each withheld item, its date range, custodian, repository, and asserted exemption.

@AustinTobitt This is the exact same thing that happened with $MMTLP years ago before they u3 halted. It was a preferred share made tradeable by an unknown issuer, and began trading at around that price.

Whistleblower document found in #Epstein files details how "naked shorting which took place in $GME is a ROUNDING ERROR compared to the OTC market", citing one case where "37 BILLION shares of a pink sheet stock were printed from thin air and naked short sold"

Worse yet: "Virtu, Knight Capital Group, and Citadel run the show"

https://t.co/P4HtShdqAT