NO white person alive today owned slaves. Teach your kids that.

NO black person alive today was born a slave. Teach your kids that.

Not all white people owned slaves back then. Teach your kids that.

Millions of white people fought and died to end slavery. Teach your kids that.

People should not inherit guilt from their ancestors. Teach your kids that.

People should not inherit victimhood from their ancestors. Teach your kids that.

You are responsible for your own actions, not the actions of people who lived 200 years ago. Teach your kids that.

America is not perfect, but it is not uniquely evil. Teach your kids that.

The West is responsible for some of humanity's greatest advances in freedom, science, medicine, and prosperity. Teach your kids that.

Loving your country is not racism. Teach your kids that.

Wanting secure borders is not racism. Teach your kids that.

Wanting safe communities is not racism. Teach your kids that.

Wanting merit over quotas is not racism. Teach your kids that.

Questioning political narratives is not racism. Teach your kids that.

People should be judged by their character, not their skin color. Teach your kids that.

History should be taught honestly, not used as a weapon. Teach your kids that.

A nation that teaches its children to hate their heritage will not survive. Teach your kids that.

Your country is your home. Protecting it is not something to be ashamed of. Teach your kids that.

You do not owe an apology for being born. Teach your kids that.

Never let fear of being called names stop you from speaking the truth as you see it. Teach your kids that.

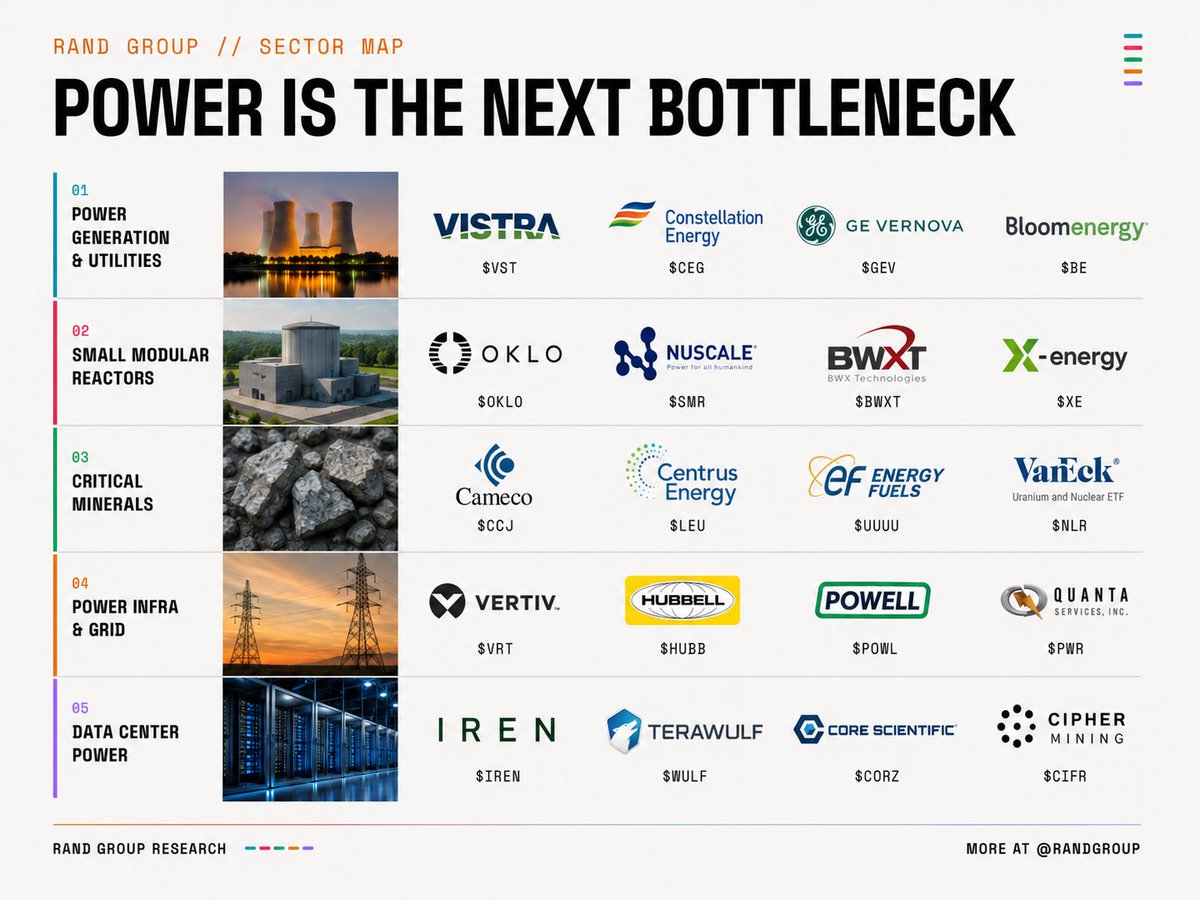

Every hedge fund I respect is suddenly talking about the same thing, and... it is not the chips.

It is the one bottleneck that breaks the entire AI story if it is not solved. Around 20 public companies sit on it. I put them all in one map across 5 layers.

Let's dive into it 🧵

Here is the thing nobody priced in two years ago. We spent a decade with flat electricity demand in this country. Utilities planned around it. Then AI showed up asking for gigawatts at a time.

The Electric Power Research Institute now thinks data centers could eat 9% to 17% of all US electricity by 2030, up from roughly 4% in 2023. Former Google CEO Eric Schmidt told Congress the sector may need 67 more gigawatts by the end of the decade. That is not a tweak to the demand curve. That is a new industrial revolution landing on a grid built for a different century. Every company below sits somewhere between a power plant and a server rack. This is the map.

🔌 POWER GENERATION & UTILITIES

Start at the source. These are the companies that actually make the electrons. For years this was the most boring corner of the market: regulated returns, slow growth, dividend investors only. Then the hyperscalers started signing power contracts directly with generators, and the whole category repriced.

$VST Vistra

This is the one I watch most closely in the group. Vistra signed Meta to a power purchase agreement for roughly 2,600 megawatts at its PJM nuclear sites, which tells you everything about where this is going: tech giants are now buying nuclear output directly. Q1 2026 adjusted EBITDA hit a record for a first quarter at $1.494 billion. They have hedged almost all of their 2026 generation, and they have bought back about 30% of the company since late 2021. A generator that trades like a buyback machine with an AI tailwind bolted on.

$CEG Constellation Energy

The largest nuclear fleet in the country, and the company that put nuclear back on the front page when it agreed to restart Three Mile Island for Microsoft. In January it closed the $21.8 billion Calpine acquisition, adding around 23 gigawatts of mostly gas and renewable capacity, and Q1 2026 revenue more than doubled the year before to $11.1 billion. The thesis is simple: when an AI company wants carbon free baseload power tomorrow, there are very few phone numbers to call, and this is one of them.

$GEV GE Vernova

If you only own one name in this entire map, my honest take is that it should probably be this one. GE Vernova makes the gas turbines and the grid equipment, the literal picks and shovels of the buildout. In a single quarter its Electrification segment booked $2.4 billion in data center equipment orders, more than it booked in all of 2025. Total backlog sits around $163 billion and management pulled forward its $200 billion target to 2027. The gas turbine backlog jumped from 83 to 100 gigawatts in one quarter, and they are raising prices into that demand. This is the cleanest expression of the trade.

$BEPC Brookfield Renewable

Note the ticker: this is Brookfield Renewable, $BEPC, not the $BE on most charts (that is Bloom Energy). Brookfield operates about 47 gigawatts and is developing a pipeline north of 200. It signed a framework with Microsoft to deliver over 10 gigawatts, roughly eight times the size of the largest single corporate power deal ever signed before it, plus a multi gigawatt hydro deal with Google. It also owns about half of Westinghouse alongside Cameco. The patient, contracted, dividend paying way to play the same wave.

⚛️ SMALL MODULAR REACTORS

Now the speculative end. The promise here is clean, firm baseload power in a compact box you can site right beside a data center. The catch: almost none of these are producing commercial power at scale yet, so you are buying a timeline as much as a company. Price that carefully.

$OKLO Oklo

The most exciting and the most expensive name in the room. In May the NRC approved the principal design criteria for Oklo's Aurora powerhouse in under half the usual review time, a real regulatory step forward. The customer pipeline is around 14 gigawatts, anchored by a 12 gigawatt agreement with Switch and a 500 megawatt deal with Equinix, and it added a research partnership with NVIDIA and Los Alamos. Just remember Oklo plans to build, own and operate its reactors and has essentially no revenue yet. This is a call option on a 2028 plus story.

$SMR NuScale Power

The one with the regulatory lead. NuScale has NRC design approval for both its 50 and 77 megawatt modules, which genuinely derisks deployment. It is sitting on about $1.2 billion in liquidity and is working toward a definitive power agreement with TVA through its ENTRA1 partner, with its first project tied to RoPower in Romania. Revenue was a rounding error last quarter because the licensing work wrapped up, so this is still a story about getting the first units in the ground.

$BWXT BWX Technologies

The adult in the room, and the name I would own if I wanted nuclear exposure without buying a lottery ticket. BWXT actually makes money: Q1 2026 revenue of $860 million and net income of $91 million, and it raised full year guidance. It builds reactors for the US Navy, produces medical isotopes, and just acquired Precision Components Group to push into commercial nuclear manufacturing. While the SMR startups sell the future, this one sells into it today.

$XE X-energy

Brand new to the public market. X-energy IPO'd on April 24 at $23 a share, raised about $1.02 billion, and came out around a $12 billion valuation with Amazon as its anchor backer holding nearly a third of the company before the listing. It pairs an 80 megawatt reactor design with its own proprietary TRISO fuel, and its order book already tops 11 gigawatts including Amazon's commitment to as much as 5 gigawatts by 2039, plus Dow and Centrica. Reality check: it lost about $390 million on $109 million of revenue in 2025, and first deployments are not expected until the early 2030s.

⛏️ CRITICAL MINERALS

You can build every reactor on the list above and they are paperweights without fuel. This is the front end of the cycle: mining, enrichment, conversion, and the magnet metals the whole grid runs on. Quick note: I swapped the misfiled Northland slot for Energy Fuels here, which is a genuine US critical minerals producer.

$CCJ Cameco

The blue chip of the uranium world. Q1 2026 net earnings jumped 87% and adjusted EBITDA rose 44% to $509 million on stronger prices and volumes. The kicker is Westinghouse: Cameco owns roughly half of it alongside Brookfield, so it captures both the fuel and the reactor technology side of the renaissance. When people want uranium exposure without a science project, they buy this.

$LEU Centrus Energy

The reshoring play, and a fascinating one. Centrus is the only production ready uranium enricher in America, sitting on a $2.3 billion enrichment backlog, a $900 million HALEU award from the Department of Energy, and a notice from the NNSA that it intends to sole source enrichment work to them. It is pouring over $560 million into its Oak Ridge centrifuge factory and is even exploring a fuel joint venture with Oklo. This is a national security story wearing a stock ticker.

$UUUU Energy Fuels

This is what $UUUU actually is. Energy Fuels runs White Mesa, the only conventional uranium mill operating in the United States, and it is the rare company licensed to produce both uranium and separated rare earth oxides under one roof. Its 2026 uranium guidance implies growth of 50% to 150%, and it is now turning out the dysprosium, terbium and magnet metals that everything from EV motors to grid hardware depends on. Uranium and rare earths, the two supply chains Washington is most desperate to pull back from China, in one company.

$NLR VanEck Uranium and Nuclear ETF

If you would rather own the whole theme in one line instead of picking a winner, this is the basket. $NLR holds the nuclear value chain end to end: reactors, enrichers, miners and the utilities running the plants. A lot of this very map sits inside it, with Constellation, Cameco, Centrus, BWXT and Energy Fuels all among its largest positions. The lazy way to be right about the sector even if you pick the wrong individual stock.

🔧 POWER INFRA & GRID

Between the power plant and the server rack is the least glamorous and maybe most investable layer of all. Transformers, switchgear, cooling, and the crews who build it. The dirty secret of the AI buildout is that the grid itself is the bottleneck. Interconnection queues run years, and the equipment to connect anything is on backorder.

$VRT Vertiv

The purest grid adjacent winner so far. Q1 2026 sales rose 30% to $2.65 billion, with the Americas up 44% on data center demand, earnings per share up triple digits, and guidance raised twice in two quarters. Vertiv makes the power and thermal systems that keep a data center alive, and it just joined the S&P 500. When the chip names sneeze, this one catches it, but the order book keeps validating the story.

$HUBB Hubbell

Boring on purpose, and that is the point. Hubbell makes the electrical and utility hardware, the transformers, metering and grid components, that every new data center and every grid upgrade quietly requires. It will never 10x in a year, but it sells into both the AI buildout and the broader grid replacement cycle at the same time. This is the ballast in the basket.

$POWL Powell Industries

My favorite quiet story in this section. Powell makes custom electrical equipment for utilities, energy and now data centers, and the demand signal is screaming: orders up 97% last quarter, a record $1.8 billion backlog, and right after the quarter closed it landed a single data center order worth more than $400 million, the largest in its history. It did a three for one split this spring and carries no debt. A small cap industrial running into a structural tailwind.

$PWR Quanta Services

The labor. Quanta physically builds and upgrades the grid, the part of this problem that no software fixes. Q1 2026 revenue rose 26% to $7.87 billion and its backlog hit a record $48.5 billion. If all of the generation and transmission above actually gets built, a meaningful slice of it gets built by crews like these. The pick and shovel play on the wires themselves.

🖥️ DATA CENTER POWER

The wild card, and the highest beta corner of the map. These started as bitcoin miners, which means they already owned the one thing everyone now wants: large blocks of interconnected power and the land around it. They pivoted to hosting AI compute, signing leases with the hyperscalers and the neoclouds. Enormous growth, real execution, and serious single customer risk. Size accordingly.

$IREN IREN

The furthest along. Formerly Iris Energy, IREN has a Microsoft AI cloud partnership worth billions, a power pipeline around 4.5 gigawatts, and high performance computing on track to make up the majority of its revenue by the end of the year. It already trades like an infrastructure company rather than a miner, because increasingly that is what it is.

$WULF TeraWulf

TeraWulf describes itself as a power company that happens to build digital infrastructure, which I think is exactly the right framing for this whole row. It has locked in over $12.8 billion of contracted compute revenue through long term leases with the Google backed Fluidstack and Core42, anchored by its Lake Mariner site and scaling toward a gigawatt of power. Its leasing revenue more than doubled year over year. Controlled power, leased to AI, on a multiyear contract.

$CORZ Core Scientific

The contrarian one. CoreWeave tried to buy Core Scientific in an all stock deal, and in a rare moment of shareholder backbone, the holders voted it down in late 2025. So it stays public, and it kept the prize: roughly $10 billion or more of contracted revenue with CoreWeave across about 590 megawatts, while converting its old mining sites into AI colocation. You are betting the company creates more value alone than the buyout offered.

$CIFR Cipher Mining

The earliest stage of the pivot, rebranding toward AI as it goes. Cipher signed a hosting deal backed by Google's Fluidstack, with Google taking around a 5% stake, plus a 300 megawatt arrangement tied to AWS, building toward a contracted compute backlog around $9 billion. Highest risk, least proven, most torque if the leases convert to cash on schedule.

⚡️FINAL THOUGHTS

Step back from the tickers and a pattern jumps out. The market is paying up for the same insight at five different points on the same wire.

The stability lives at the bottom and the middle. Cameco, Hubbell, Quanta Services and BWX Technologies make money today and sell into a buildout that is contracted for years. They will not triple overnight, but they do not need a single thing to go right that has not already happened.

The growth lives at the edges. GE Vernova is the rare name that has both, scale and acceleration, which is why I keep coming back to it. The reactor startups and the former miners are where the imagination is, and also where the disappointment will be when timelines slip, because timelines always slip in nuclear and in construction.

The clearest read of all is that the AI story quietly handed the baton from the chip layer to the power layer, and most people are still watching the wrong race. You cannot run the model without the electrons, and the electrons are the scarce thing now.

I will say the obvious part out loud: this is a map, not advice. I am pointing at where the money is moving, not telling you what to buy. Do your own work on every one of these, especially the speculative names where a single contract or a single regulator can move the whole thesis.

If this saved you a week of research, do me a favor and bookmark it, then send it to the person in your group chat who only owns Nvidia. The power bottleneck is the second half of that trade.

Not one, not two, but three S&P 500 sectors are testing either Dot-Com or GFC extremes. Relative to the rest of the market, Healthcare is back to March 2000 specifically. Consumer Staples = Dec. 1999. The S&P 500 Financials sector just broke March 6, 2009.

I took a little position in $CRWV today

700 shares

+ those debit spreads

Jan27 $150C bto

Jan27 $220C sto

I don't love the debt this company carries, but I think if $NBIS is gonna run the way it is, $CRWV deserves some love considering Jensen and Leopold just increased their stake

Basically same thesis as $IREN. These guys own a massive amount of compute.

Few notes

$CRWV has more actual AI compute live today

$IREN has the raw power footprint

$NBIS has the future contracted capacity story

- Jensen basically put a backstop on this company a few quarters ago and said that if they ever can't sell their compute, NVIDIA will buy it 🤣

- News today: $Dell Delivers World's First Nvidia Vera Rubin NVL72 Server Rack To CoreWeave

Again, I don't LOVE the company to hold forever but i think with the AI buildout lasting much longer than most expect, capex increasing everywhere, this has the same recipe to make a move like $ARM IMO.

I see too much arguing over $NBIS vs $IREN vs $CRWV

when in reality I think theyre all going to be winners over the next few years.

How to lose a country and it’s culture…

The % of white population in America:

1970: 88%

1990: 80%

2000: 75%

2010: 72%

2020: 62%

2025: 57%

The % of immigrant households on government benefits:

1970: 6%

1990: 9%

2000: 18%

2010: 51%

2020: 59%

2025: 61%

All by design.

Insane.

🚨 HUGE DEVELOPMENT: Sec. Markwayne Mullin announces DHS is drawing up plans to BLOCK ALL international flights into sanctuary cities by ending Customs screening there

This would DEVASTATE those cities.

Mullin is doing it as a direct result of sanctuaries refusing to cooperate

GOOD! We need consequences where it hurts!

"Why are we processing international flights into the airport there? And we are currently, which we're not issuing it yet, but we're currently drawing up plans to say, listen — in these sanctuary cities where the local radical left Democrats aren't allowing us to do our job and enforce federal laws, then we shouldn't be processing international flights into their cities either, because they don't want us to enforce immigration, but they want us to process immigration at their facilities!"

🚨 NOW: EVERY SINGLE DEMOCRAT state Attorney General has REFUSED to show up for JD Vance's anti-fraud roundtable at the White House

Republicans showed up, but Vance specifically sent out an olive branch and invited Dems.

THEY SAID NO.

They're pro-fraud.

Nearly 2 dozen Democrat AGs cited time constraints as the reason they can't show up. Yeah, sure.

Democrats = PARTY OF FRAUD

🚨The Minnesota fraud empire is falling:

Yesterday 15 fraudsters were charged and $90 million was busted. The MSM tried to cover for the fraudsters. @GovTimWalz called it "white supremacy" to expose it and @IlhanMN is completely SILENT.

Independent journalism defeated an entire fraud network upheld by billions of dollars with support from corrupt politicians who allowed this fraud and the MSM who failed to report it.

Major win for America and hardworking law-abiding taxpaying citizens. This is just the beginning.

Arrest them all.

Those who listen will become MILLIONAIRES.

Once the AI hardware rotation slows down…

power will still need to grow exponentially.

Here’s the AI Power Super cycle that RETIRES you:

1. Layer 1 Fuel & Natural Gas Supply

(the energy feeding the AI boom)

• $EQT - largest U.S. natural gas producer

• $KMI - gas pipelines + infrastructure

• $WMB - natural gas transport + LNG

• $ET - massive U.S. energy network

2. Layer 2 Onsite / Fast Deploy Power

(the real near-term bottleneck solution)

• $BE - Bloom Energy fuel cells

• $GEV - gas turbines + power systems

• $CAT - backup generators

• $CMI - power generation systems

• $KGS - gas compression + mobile power

• $TE - solar + microgrid exposure

3. Layer 3 Grid & Electrical Infrastructure

(the hidden AI winners)

• $ETN - electrical systems

• $PWR - grid buildout

• $VRT - cooling + power management

• $HUBB - transformers + grid equipment

• $NVT - electrical infrastructure

• $EMR - industrial power systems

4. Layer 4 Nuclear & Long-Term Baseload

(the future AI power source)

• $OKLO - advanced nuclear

• $SMR - small modular reactors

• $NNE - portable microreactors

• $CEG - largest U.S. nuclear fleet

• $VST - nuclear + power generation

• $BWXT - reactor components + services

Here is how it breaks down.

AI models get larger. Data centers get bigger.

Energy demand keeps accelerating.

CBS News said there was no evidence of fraud.

The NYT said the Somali community was being targeted

CNN said there was "little evidence."

Tim Walz said it was “white supremacy” to expose fraud

Today: $90M busted and 15 charged.

IT WAS ALL FRAUD AND THEY KNEW.

Chicago woman mocks Democrats by speaking in a squeaky, high-pitched voice, who say black people's voting rights are in danger.

The woman also called out the commissioners one by one to their faces.

"I'm 63 years old. I've been voting since I was 18. I have never had a problem voting..."

"So now you're all gonna drag black people in here, definitely some senior citizens, and gonna have them come up here and talk about how they're scared to vote... all that junk, when you know it's not true."

🚨 BREAKING: Google Gemini can now analyze any stock like a Wall Street analyst (for free).

Here are 10 insane Gemini prompts that replace $4,000/month Bloomberg terminals:

(Save this 🔖 you’ll need it later)

California gave ONE nonprofit $1 BILLION.

To put solar panels on poor people's roofs.

You know how much solar they actually installed?

$72 million.

That's it.

So where the FUCK is the other $928 MILLION?

I'll tell you exactly where.

The same nonprofit that WROTE the law that gave them the money ALSO got the contract to run "community outreach."

Same guy runs the nonprofit AND the program. Chris Walker. Two paychecks. Look it up.

And their SISTER organization — same building, same staff, same donors — is a 501(c)(4) that endorses Democrat candidates and runs door-knocking operations in the EXACT SAME NEIGHBORHOODS.

Connect the dots, idiot.

You pay $7.50 a gallon for gas.

Cap-and-trade takes a cut at the pump.

That money flows to "climate justice nonprofits."

Those nonprofits funnel it into Democrat get-out-the-vote machines.

You. Are. Funding. The. People. Who. Are. Robbing. You.

Every time you fill up your fucking tank, you're paying for a Democrat campaign volunteer to knock on a stranger's door and tell them how amazing Gavin Newsom is.

$928 MILLION.

GONE.

And not one journalist in this state asked a single question until @jennyraeca and CAL DOGE pulled the receipts.

You think this is the only one?

There's a hundred more like it.

This is how California works now.

This is how a "blue state" stays blue when only 48% of the voters are Democrats.

Wake the fuck up.

@patrickbetdavid@VincentOshana@FoxNews@WallStreetApes @CalDOGEgov @elonmusk@libsoftiktok

We're standing in front of the building right now.

https://t.co/bYQD11T69M

A psychologist at the University of North Carolina spent 20 years proving that a single 20-second hug rewires the human cardiovascular system, and the experiment she ran is so simple you can replicate it tonight at home.

Her name is Karen Grewen.

She works inside the UNC School of Medicine's Department of Psychiatry. The paper that made her famous was published in 2003, and almost nobody outside her field has read it.

Here is what she actually did.

She recruited 183 healthy adults living with a long-term partner. She split them into two groups. The warm contact group sat together for 10 minutes holding hands while watching a romantic video. Then they stood up and hugged each other for exactly 20 seconds.

The control group sat alone in a separate room for the same amount of time doing nothing.

Then she made every single one of them give a public speech in front of a panel.

Public speaking is one of the cleanest stressors in psychology. Heart rate spikes. Blood pressure climbs. Cortisol floods the system within minutes. It is the laboratory version of every stressful moment you have ever had at work.

The people who had been hugged for 20 seconds before walking into that room had measurably lower blood pressure responses to the stress. Lower systolic. Lower diastolic. Lower heart rate increases. Everything was the same.. the speech, the panel, and fear. But this time completely different physiological response.

The hug had not made the stress disappear. It had changed how the body was allowed to respond to it.

Two years later Grewen ran the follow-up study that explained why. She drew blood from 38 couples before and after the same warm contact protocol and measured what was actually changing inside them. The answer was a hormone called oxytocin.

Oxytocin is the chemical your body releases during childbirth, breastfeeding, and orgasm. It is the same molecule that makes a mother feel calm holding her newborn.

Grewen's data showed that 20 seconds of physical contact with a trusted partner triggered a measurable spike in plasma oxytocin in both men and women, and the size of that spike directly predicted how much their blood pressure dropped.

The mechanism turned out to be older than recorded history. Oxytocin binds to receptors in your heart, your blood vessels, and the part of your brainstem that controls how aggressively your nervous system reacts to threat.

When the hormone shows up, the entire fight-or-flight machine downshifts. Your blood vessels widen. Your heart slows. Your cortisol production gets suppressed.

This is not a feeling. This is a chemical instruction your body sends to itself that you can measure with a blood pressure cuff.

The detail Grewen kept emphasizing in her interviews was the duration. Three seconds is the average length of a hug between two humans. It is too short.

The hormonal cascade does not have time to start. 20 seconds is the threshold where the oxytocin actually crosses into the bloodstream in a quantity large enough to do something measurable.

A follow-up study tracked 59 premenopausal women over time and found that the ones who hugged their partners most frequently had lower resting blood pressure and higher baseline oxytocin levels than the ones who did not. The effect compounded. Daily hugs produced a permanent shift in the cardiovascular baseline.

A separate review of long-term partner contact research found that married adults with frequent affectionate touch had significantly lower rates of heart disease and all-cause mortality than equally healthy adults without it.

The American Heart Association now cites this body of research when explaining why social isolation is treated as a cardiovascular risk factor on the same level as smoking.

The most haunting line in Grewen's research is one she said in an interview after publishing the second paper. She pointed out that the average American touches another human being less than they did 50 years ago. Phones replaced eye contact. Texts replaced visits. Hugs at the door got shorter.

The thing that used to regulate our cardiovascular system multiple times a day quietly disappeared from most adult lives.

Your body still expects it. The hormone receptors are still there waiting. The system was designed to be reset by physical contact with people who feel safe, and the reset takes 20 seconds.

You can run the experiment yourself tonight. Hug someone you love for 20 full seconds. Count it out. The first 10 will feel awkward. Around 15 something shifts. By 20 the shoulders drop, the breathing slows, the chest opens.

That is not in your head. That is your bloodstream changing.

⚡️Higher education is entering its liquidation phase as a mass middle-class belief system.

The demographic cliff is only the visible trigger. The deeper break is that the entire college model was built on three assumptions: there would always be more students, families would always treat college as mandatory, and employers would always reward the credential enough to justify the cost. All three are now weakening at the same time.

That is why this matters.

A fertility decline from 2007 shows up in college admissions with an 18-year delay, but the enrollment shock lands inside a system already overbuilt. Colleges expanded staff, facilities, administrative layers, debt loads, athletic budgets, student-life amenities, DEI bureaucracies, marketing machines, and low-ROI programs during an era when the college-going population was bigger and the credential premium felt unquestioned. Now the customer base is shrinking while the product is being repriced.

That creates a financial vise.

The elite tier survives because it sells scarcity, network, status, marriage markets, recruiting access, and proximity to power. A Harvard or Stanford degree is not mainly a classroom product. It is a social-routing asset. Those schools can keep demand even if people lose faith in “college” broadly.

The practical tier survives because it has obvious economic utility. Engineering, nursing, accounting, skilled health fields, hard technical programs, logistics, applied AI, defense-adjacent disciplines, and high-placement public universities can still justify themselves. Cheap public options also survive because affordability becomes a weapon.

The exposed layer is the bloated middle: expensive private colleges without elite status, regional schools with weak draw, generic master’s programs, low-placement liberal arts degrees, weak online MBAs, tuition-dependent institutions, and universities that confuse branding with value. Those schools are going to face the hardest truth: students were not loyal to them. Students were loyal to the belief that the system required them.

That belief is cracking.

AI makes the break sharper because it attacks the bottom rung of the white-collar ladder. College made sense when the degree bought access to entry-level knowledge work. If entry-level knowledge work gets compressed by AI, the bridge weakens. Families will not pay unlimited tuition for a credential that leads into a shrinking first rung. They will ask harder questions: what job, what network, what income, what debt, what skill, what proof?

The cultural layer is even bigger. College used to be the default coming-of-age institution for the American middle class. It replaced church, apprenticeship, local adulthood, early marriage, and family formation as the official bridge from youth into adult status. Now that bridge is expensive, delayed, ideologically contested, economically uncertain, and increasingly detached from real capability.

So the enrollment cliff is really a legitimacy cliff.

The schools will respond by discounting tuition, poaching students, merging departments, cutting humanities programs, chasing international enrollment, adding AI buzzwords, expanding career services, begging donors, leaning harder into athletics, and selling “community” because the economic case is weaker. Some will survive. Many will shrink. Some will close. The sector will consolidate because the old demand curve is not coming back.

The brutal truth: higher education became a credential factory priced like a luxury good, staffed like a bureaucracy, and justified by an employment ladder AI is now destabilizing.

Demography lit the fuse.

AI removes the escape route.

The next decade is going to separate institutions that actually create human capital from institutions that merely certify participation in a fading social ritual.

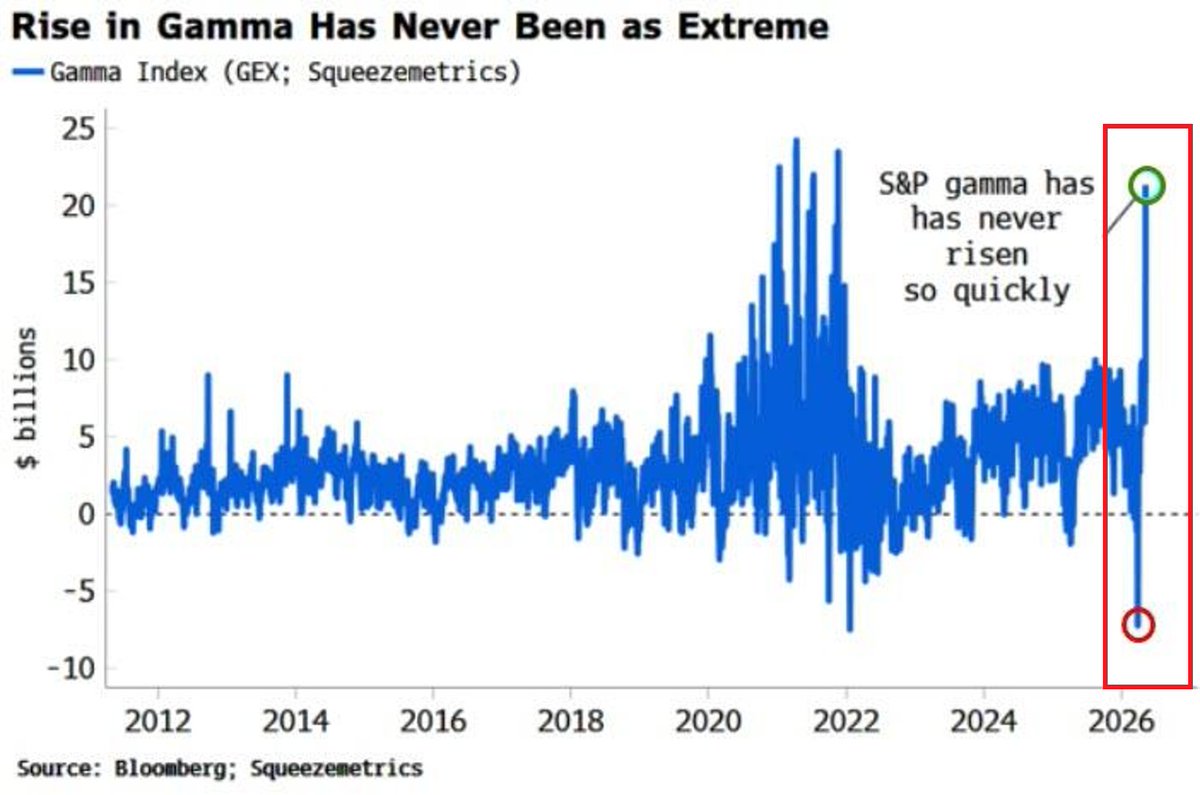

⚠️THIS IS UNPRECEDENTED:

The S&P 500 Gamma has surged from deeply negative levels at the end of March to the highest since 2021, the fastest surge EVER.

The only comparable episode was late 2021, when a similarly extreme gamma setup preceded a market top by just 1-2 months.

Gamma measures how much market makers must buy or sell in stock futures to hedge their options positions.

When gamma is positive and rising, market makers act as a stabilizing force, buying dips and selling rallies.

When it swings this violently from negative to positive, it signals an extraordinarily unstable market structure underneath a calm surface.

This has been driven by extreme speculation, particularly in the semiconductor stocks.

When a market reversal comes, it will be sharp and severe.