The Top 10 investments across Robinhood just got updated for June.

All 10 of the top held assets are the same except for one...

$AMD.

AMD replaces $NFLX (which was in the top 10 for the past few months) as one of the top 10 held stocks across the platform on $HOOD Robinhood.

$AMD is up 118% YTD and has been a massive winner for retail investors that bet on Lisa Su over the past few years.

The other 9 most held on Robinhood:

$META $GOOGL $AMZN $MSFT $NVDA $PLTR $F $MSFT $TSLA

US PREMARKET MOVERS – JUNE 5, 2026

S&P 500 Index futures are down 0.5% at 7:51 a.m. in New York, as the AI trade continues to weaken. Nasdaq 100 futures fall 1.1%, while Dow Jones Industrial Average futures edge up 0.2%. The MSCI World Index is little changed.

Magnificent Seven

$NVDA -1.3% | $MSFT +0.4% | $TSLA +0.1% | $AAPL -0.1% | $GOOGL -0.4% | $AMZN -0.2% | $META -0.2%

Biggest Premarket Movers:Winners

• $MRLN +29% – Defense tech company surges after successful critical design review for its C-130J autonomy program with US Special Operations Command.

• $TTAN +15% – Software firm jumps on strong first-quarter revenue beat.

• $AGX +11% – Power-plant builder rallies after Q1 revenue topped analyst expectations.

• $GIII +8% – Apparel group gains on raised full-year EPS guidance.

• $COO +6% – Lens maker rises after Q2 sales and profit exceeded estimates.

• $CMG +2% – Chipotle climbs following JPMorgan upgrade to overweight, citing a “rare valuation opportunity.”

Losers

• $GWRE -12% – Software company drops after Q4 subscription revenue guidance missed estimates.

• $LULU -10% – Lululemon slides following a lowered annual forecast due to weak North America performance.

• $DOCU -4% – Docusign falls after in-line Q2 revenue outlook; investors await progress on its AI-powered contract platform.

• $IOT -2% – Samsara slips after reporting first-quarter results.

Overall sentiment remains cautious with AI-related stocks under pressure.

The Market Is Wrong About AI Software and Bitcoin

The early take on AI was simple: if agents replace workers, and workers use software, then software demand falls. Clean logic. Completely wrong.

We have seen this mistake before. When the internet arrived, the consensus was that paper would disappear. Instead, paper usage rose for years because the internet made it easier to create, copy and distribute information. Demand expanded, it did not shrink.

AI is doing the same thing to software.

Agents do not replace software. They consume it, constantly. An AI agent is not just a chatbot. It reads information, makes decisions and calls tools to execute tasks. Databases, spreadsheets, CRMs, code engines, each step triggers another action, another request, another loop.

A human uses software during the workday. An agent uses it 24 hours a day, seven days a week, without pause. Software activity is already exploding, with a growing share driven by AI agents rather than people. What looks like automation is actually a surge in usage.

When usage rises, spending follows. Companies deploying agents are not shrinking their software budgets they are expanding them. The model is shifting from paying per seat to paying for consumption. The market, as usual, is misreading the shift.

Don’t even get me started on AI and the labor force.

Capital is crowding into a narrow set of semiconductor names, as if every company in the space shares the same economics and exposure. They do not. Memory is not logic. And not every Semi stock needs to be re-rated.

Cyclicality is not scarcity. Use that. The stupidity of the market is an opportunity. While FOMO traders chase anything tied to AI and assume every semiconductor stock looks like Micron, the real differentiation is in who actually captures sustained demand.

The same analytical error is now showing up in Bitcoin.

Whether the Clarity Act passes or not, or whether stablecoins offer yield or not, does not matter to Bitcoin. Those debates are distractions. They do not change its role, its design or its long-term demand.

In both cases, the mistake is identical: confusing what changes at the edges with what drives the system.

In AI software and in Bitcoin, the edge trade is noisy, the base trade is obvious, and that is where the real money is made.

The most important thing to internalize as an investor right now:

Demand for intelligence is infinite.

As long as there are problems to solve, there will be demand for the intelligence to solve them.

The demand scales with the click of a button...

But the supply is constrained by the physical world (chips, energy, grid, etc.)

So demand will outstrip supply for a long time.

Once you understand this,

You just buy and hold the companies that will have way more demand than supply for the foreseeable future.

Give your capital to the teams that understood this early and have been treating shareholders well.

And benefit from a once in a lifetime transition from a human intelligence economy to a machine intelligence economy.

Hoist your sails and let the generational tailwinds compound your capital.

It won't be smooth sailing the whole way.

But we're never going back to humans doing all the mental labor.

AI will continue to proliferate.

It will enter the physical world via robots, autonomous vehicles, and smart sensors.

Understand this and it's easy to build long-term conviction in certain assets.

For me $NBIS and $OUST have become high-conviction holds.

Nebius is becoming a leading supplier of intelligence for the new economy. They're selling intelligence 2-4x cheaper than OpenAI and Anthropic. Demand is off the charts and margins are expanding.

Ouster is building the vision hardware and software that helps robots, autonomous vehicles, and sensors make sense of the real world.

Easy theses.

And they work for me.

But the most important thing is to own SOME piece of this revolution.

I like a barbell approach:

AI revolution bets on one side, and investing in real world maxxing on the other side.

The faster my capital compounds, the more focused I become on squeezing every bit of life out of my finite time here.

This is ultimately the promise of this revolution.

Let the machines crunch the numbers and click the buttons.

And free us up to become more human.

Next post will be about real-world maxxing.

Which is arguably the harder thing to nail.

🇨🇦 ROBINHOOD LAUNCHES INTO CANADA WITH CRYPTO TAKEOVER

Robinhood has completed its $180M purchase of WonderFi, officially expanding into Canada through crypto platforms Bitbuy and Coinsquare.

The deal takes Robinhood past 1 MILLION international funded customers.

Let’s be honest

The AI Earnings Super‑Cycle Has Arrived

First Dell and now HPE are telling investors the same thing: the AI earnings super‑cycle is no longer theoretical, it has arrived, and S&P 500 numbers are still too low. HPE is now guiding fiscal 2026 non‑GAAP EPS to roughly 3.35–3.45 dollars and free cash flow to at least 3.5 billion dollars—levels it had previously targeted for 2028—on the back of nearly 30–plus percent revenue growth and more than 70 percent networking growth this year. Dell, meanwhile, has turned into an AI systems pure play, with AI‑optimized server revenue exploding, a multi‑year backlog measured in tens of billions, and management now talking about AI server revenue running toward 50 billion dollars as data‑center capex accelerates rather than fades.

This is what an earnings super‑cycle looks like in practice: the core infrastructure providers are pulling multi‑year profit curves forward because AI demand is compounding from a high base, not rolling over. Scarcity in GPUs, power, networking, and physical capacity means the constraint is supply, not demand, and that in turn is forcing customers into larger, longer‑dated contracts to secure AI infrastructure years out. Ignore the noise about quarterly “AI capex deceleration.” First Dell, now HPE: the message is that the AI build‑out is accelerating, hardening into long‑term commitments, and dragging index‑level earnings power higher and faster than the current S&P 500 forecasts are willing to admit.

$Dell $HPE $NVDA

THE AUTONOMY LAYER OF THE DEFENSE BUILDOUT

President Trump is pursuing funding deals with drone companies to boost domestic production & the market is starting to reprice unmanned systems as a core layer of modern warfare.

The bottleneck is shifting to autonomy, attritable mass & secure communications where the systems that let hundreds of low-cost drones operate like one coordinated force are driving dollar-content expansion across the stack:

1. $ONDS building autonomous systems layer for modern defense through drones, counter-UAS, ISR & mission-ready robotics with backlog jumping to $457M & a new $PLTR partnership bringing AIP & its Sky Weaver AI intelligence layer into the stack.

2. $KTOS one of the cleaner defense autonomy plays sitting across tactical drones, target drones, hypersonics & battlefield systems with Q1 delivering a record $2B backlog, a 1.6x book-to-bill & $14B opportunity pipeline.

3. $AVAV established drone warfare leader with loitering munitions, counter-drone systems & tactical UAS exposure that directly benefits as the Pentagon shifts toward attritable mass with $4.6B in YTD awards anchored by a $186M Army order for next-gen Switchblade munitions.

4. $AVEX higher-risk emerging supplier in the basket tied to the market’s search for smaller defense drone names that can scale into domestic unmanned systems demand thats backed by recent Air Force awards for one-way-attack autonomous aircraft & UAS engineering services.

5. $UMAC U.S. drone supply-chain play focused on rebuilding the domestic hardware layer from components to FPV drone systems as the government tries to reduce reliance on foreign-made drone parts while partner Powerus advanced to Phase II of the Pentagon’s $1B Drone Dominance Program.

6. $RCAT positioned around low-cost military drones & battlefield reconnaissance with Black Widow selected by Japan’s Ministry of Defense for 173 systems plus adoption from a NATO ally and the Australian Army.

7. $DPRO most speculative autonomy name in the basket with exposure to public safety, defense & emergency response plus a U.S. Air Force Special Operations FPV drone award & validated SwarmOS swarm-autonomy integration with Palladyne AI.

$IGV

Okay, let’s talk about software…

Here’s my question: are software stocks actually ready to breakout or is this move legit?

If it is legit, then it may be time to buy the breakout.

Software stocks I bought during the SaaSpocalypse:

$PLTR, $ZETA, $RDDT, $SHOP, $ORCL.

I bought a very small amount of $MSFT at $413, my bigger DCA on the Mag 7s has been $META over $MSFT. I believe $META is a fantastic risk/reward right now but they still have narrative issues to revolve. However, given the new chip news with Microsoft/Nvidia/ARM, it seems like Microsoft could have a breakout.

Buying that name into strength is NOT scary given it’s…Microsoft. If they actually start selling chips to Anthropic, they may completely get rerated.

But, what about everything else? Are the rest of these software names scary to buy into a breakout after their run?

I know this chip names have done amazing, but take a look at the performance of these SaaS names since the lows…

$DDOG +152%

$SNOW +116%

$RDDT +45%

$ZETA +59%

$NOW +53%

$PLTR +28%

$SHOP +26%

$ORCL +62%

$CRWD +107%

$PANW +91%

Last week, people were saying Shopify would be vibecoded away. ServiceNow would be going out of business. I mean just absurd commentary on incredibly important companies.

If the software narrative being destroyed is gone, why wouldn’t these names be buys into the breakout? Assuming no broader macro drawdown, is the risk reward not still very strong for these names?

Many of them are still DOWN year to date. If token spend is going to normalize (as per Anthropic not raising costs for Opus 4.8) and the market finally realizing that all this token demand is actually coming from the SOFTWARE companies processing and orchestrating it…then it feels like the SaaS breakout could be just beginning and even if you missed the drawdown, buying these names into strength wouldn’t be scary given their multiples are still compressed but their growth rates continue to match some of the best chip names.

Did you buy SaaS during the drawdown? Are you buying more software names into strength?

$RDDT should be leaving the station and moving much higher if the SaaS sentiment continues to improve.

30% CAGR for the next 4 years on EPS probably doesn’t deserve the fwd multiple they are trading at.

The entire company is in serious growth mode and also has the one thing that matters in AI: real, curated human content.

$PLTR

The biggest concern around Palantir over the past 2 years has been its valuation.

That concern should not be that relevant anymore.

If we are looking at other companies in Software, $SNOW and $CRWD are trading at HIGHER multiples on a NTM EV/EBITDA yet they are growing 2x LESS than Palantir and at 2x WORSE margins, as shown in the chart below by Arny.

You want to know what’s even worse?

The TTM GAAP profits for all 3:

Palantir did $2.28B in GAAP net income, actual profit coming down to the bottom line.

Snowflake LOST $1.33B and Crowdstrike LOST $162M!

$SNOW and $CRWD can’t produce a GAAP profit, have significantly worse margins and have significantly less growth but are getting a HIGHER multiple.

This is not to say that Snowflake or Crowdstrike are overvalued or don’t deserve the premium they are getting, but it is to say there is a massive valuation disconnect and anyone screaming that Palantir is expensive cannot make that argument relative to every other company in SaaS.

Better margins, faster growth, profitable…and basically guided to 100% topline growth next year.

This is obvious.

If the market is willing to continue giving these premiums to software companies as the “AI destroying software” narrative goes away, Palantir should continue to gain momentum.

Since this post a week ago:

1. $WYFI +47.25%

2. $RIOT +26.79%

3. $CORZ +24.62%

4. $IREN +37.69%

5. $TE +80.57%

6. $PUMP -11.18%

7. $SHAZ +41.32%

8. $SEI -2.80%

9. $BTDR +49.59%

10. $CLSK +45.69%

11. $HIVE +39.14%

12. $PSIX +12.12%

Ten positions up, two down. Average return of +32.57% in under two weeks. See for yourself.

Next list dropping soon.

Turn on notifications so you don’t miss the next set.

$DELL just posted record earnings - $43.8B in revenue, up 88% YoY, and beat estimates by $8.4B.

AI server revenue hit $16.1B. Up 757% year over year. $24.4B in AI orders in a single quarter.

Here are 5 companies that are direct beneficiaries you should keep on your watchlist:

1. $SMCI - Super Micro Computer

Direct AI server competitor riding the same demand cycle. Q3 revenue $10.2B, up 123% YoY. $13B+ Blackwell order backlog. They hold 70-80% market share in direct liquid cooling - which becomes mandatory as AI racks get denser. If Dell is shipping this much, SMCI is shipping right behind them.

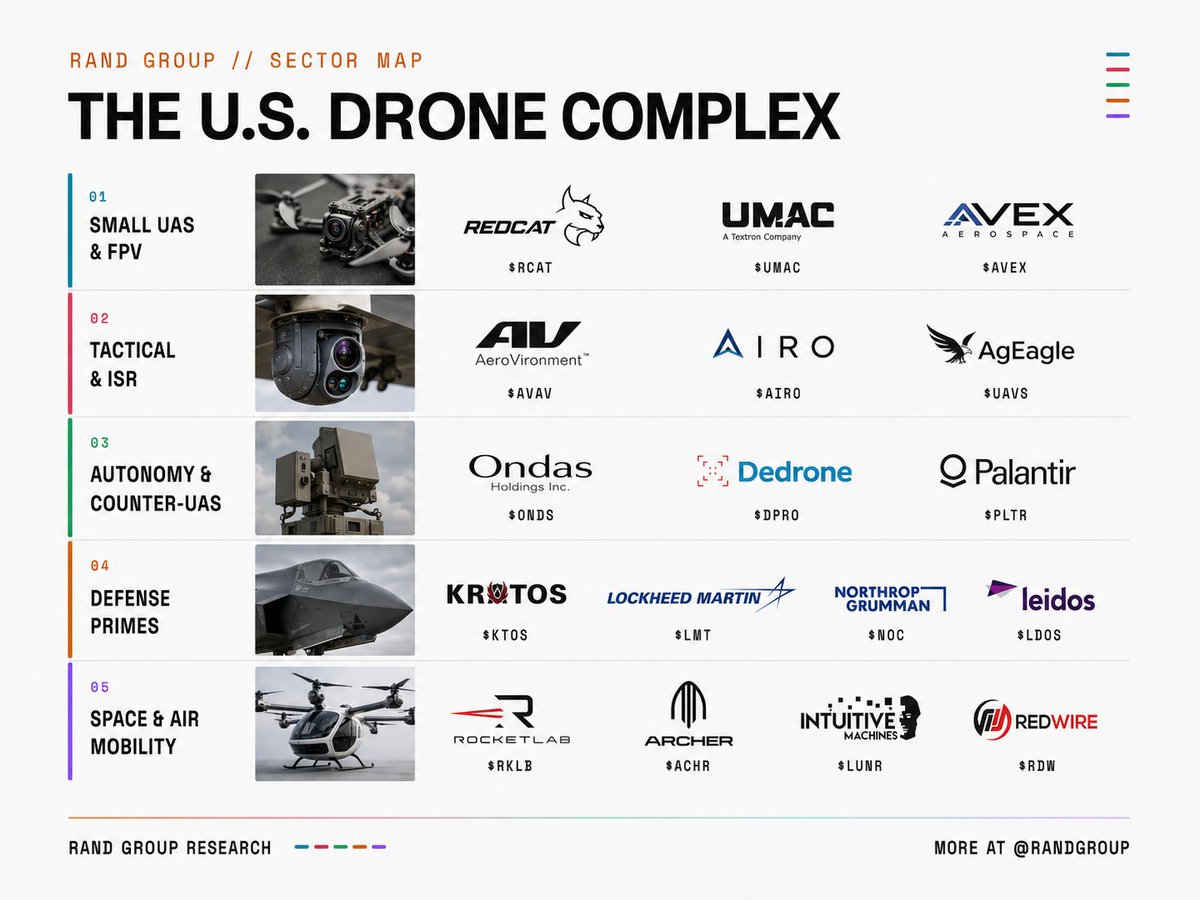

🇺🇸 The Pentagon is reportedly negotiating to take direct equity stakes in US drone companies. Not contracts. Actual government ownership.

I researched 16 public companies that will directly benefit from this massive move, so you don’t have to.

Bookmark it and let's dive in 🧵

🕹️ SMALL UAS & FPV

The frontline layer. Small, cheap, expendable drones that changed the way wars are fought. Ukraine proved the concept. Now every military on Earth is scrambling to buy them.

$RCAT Red Cat Holdings

This might be the most explosive growth story in the entire drone sector right now. Revenue grew 849% year over year in Q1 2026. Secured a $35M U.S. Army contract for its Black Widow reconnaissance drone. Just won a competitive deal to deliver 173 systems to Japan's Ground Self Defense Force. Also shipping to NATO allies and multiple Asia Pacific partners. Participating in the $1B Drone Dominance Program. Expanding beyond air into unmanned surface vessels through its Blue Ops unit. The contract velocity here tells you something real is happening.

$UMAC Unusual Machines

Consumer and military FPV drones and components. Makes Fat Shark goggles and FPV flight controllers. Jumped 57% in a single day on the Pentagon equity stakes news. The hype is real but so is the caution: this is still an $11M revenue company trading on narrative momentum. Supplies components to Red Cat's FANG drone program. If the government truly starts taking ownership stakes in American drone makers, UMAC is exactly the kind of small pure play that gets swept up in the wave. High risk, high potential.

$AVEX Aevex Aerospace

IPO'd April 2026 and nearly doubled from its $20 offer price within days. Backed by private equity. Goldman Sachs initiated at buy. Strong profit margins and cash flow, which is rare in this space. Focused on ISR drone services for defense customers. One of the few profitable drone companies going public right now.

🎯 TACTICAL & ISR

Bigger, more sophisticated systems. Loitering munitions. Battlefield intelligence. These are the drones that militaries actually deploy at scale.

$AVAV AeroVironment

The institutional grade drone stock. After the BlueHalo acquisition, trailing revenue surpassed $1.6B. Funded backlog at $1.1B. Makes the Switchblade family of loitering munitions that became famous in Ukraine. The 300 handles personnel, the 600 destroys armor. This is the name that real money flows into when it rotates into the drone theme. When UMAC jumped 57% on the Pentagon news, AVAV only moved 8%. That gap is where the institutional opportunity lives. The boring choice in defense investing usually wins.

$AIRO Airobotics

Focused on autonomous drone operations for defense and security applications. Part of the broader push toward fully autonomous ISR platforms that don't require a human operator in the loop. Secured a $20M order for autonomous border security. Early but the autonomous angle is the direction the entire sector is heading.

$UAVS AgEagle Aerial Systems

Drone solutions spanning hardware, software, and sensors for commercial and government applications. Provides imaging and analytics capabilities. Smaller player in a sector that's consolidating fast, which could make it an acquisition target as the primes look to bolt on capabilities.

🤖 AUTONOMY & COUNTER UAS

The software and AI layer. Autonomous flight, swarm coordination, and the increasingly critical mission of shooting down enemy drones. Counter UAS is becoming as important as the drones themselves.

$ONDS Ondas Holdings

Dual business: private wireless networks and autonomous drone systems. The OAS unit (Airobotics, Iron Drone, Apeiro Motion) is the growth engine. Just completed a $196.6M acquisition of Omnisys to add AI battlefield software on top of the hardware stack. Iron Drone Raider is their counter UAS platform. Sentrycs subsidiary won counter drone security contracts for the FIFA World Cup. Q1 revenue hit $50.1M with a $457M backlog. Also just partnered with Palantir to build AI powered autonomous systems. That partnership tells you where this is going.

$DPRO Draganfly

Canadian company developing interoperable, modular drone platforms for military, public safety, and commercial use. NDAA compliant across 5+ systems, which matters as the U.S. bans Chinese drones from critical infrastructure. Recently acquired Skip Dynamix for electronic warfare resilient autonomous systems and partnered with Palladyne AI for SwarmOS integration. Sitting on C$147M cash with minimal debt. The thesis is that future military operations need fleets of interoperable drones, not isolated platforms. Draganfly is building for that world.

$PLTR Palantir

Not a drone company but increasingly the software brain behind them. Their AI and data analytics platform is becoming the operating system for autonomous defense systems. The Ondas partnership is just one example. When military drones need to make real time decisions, coordinate swarms, and process battlefield data, Palantir's platform is in the stack. The picks and shovels play for the entire autonomy layer.

🛡️ DEFENSE PRIMES

The companies with the budgets, the contracts, and the manufacturing scale to produce drones by the thousands.

$KTOS Kratos Defense

Makes the XQ 58A Valkyrie, a jet powered drone designed to fly alongside manned fighter jets as an autonomous wingman. Marine Corps selected Valkyrie for its Collaborative Combat Aircraft program with an initial contract of $231.5M. Also secured an OTA worth up to $446.8M for ground systems work. This is the name that bridges the gap between startup innovation and defense prime scale. Institutional enough for real money, innovative enough for growth investors.

$LMT Lockheed Martin

The largest defense contractor on Earth. Building autonomous systems, hypersonic platforms, and integrating drone capabilities across its programs. When the Pentagon writes the biggest checks for unmanned systems, Lockheed is on the receiving end.

$NOC Northrop Grumman

Partnered with Kratos on the Valkyrie program. Developing next gen autonomous combat aircraft and integrating unmanned systems into its broader defense portfolio. Deep government relationships and decades of contract visibility.

$LDOS Leidos

IT services, cybersecurity, and mission systems for defense. Provides the data infrastructure, communications networks, and analytics platforms that drone programs depend on. Not a drone maker per se, but deeply embedded in the software and systems layer that makes autonomous operations possible.

🚁 SPACE & AIR MOBILITY

The companies expanding the definition of what "drone" means. From orbital platforms to electric air taxis to space based autonomous systems.

$RKLB Rocket Lab

Already covered in the space map but relevant here too. The infrastructure layer for anything that operates above the atmosphere. As autonomous systems extend into orbital and suborbital domains, Rocket Lab's launch and satellite capabilities become part of the drone complex supply chain.

$ACHR Archer Aviation

The eVTOL play. Completed Phase 3 of FAA certification for its Midnight aircraft. Still very early with ~$1.6M in Q1 revenue but sitting on $1.78B cash. This is a bet on urban air mobility becoming real. If electric air taxis happen, Archer is one of the best positioned companies to deliver them. Big if, but the capital is there to try.

$LUNR Intuitive Machines

Covered in the space breakdown. Relevant here because their autonomous systems capabilities extend from lunar operations to orbital data processing. The autonomy stack they're building for space has direct applications in the broader drone and robotics ecosystem.

$RDW Redwire

Space infrastructure and on orbit manufacturing. Developing autonomous systems for orbital operations. As drones move beyond the atmosphere, Redwire's capabilities in autonomous space robotics put them at the intersection of the drone complex and the space economy.

🧠 FINAL THOUGHTS

The U.S. drone sector is at a turning point. The Pentagon is allocating over $74B to unmanned systems. The government is reportedly preparing to take equity stakes in American drone companies. Ukraine proved that cheap, autonomous drones change the calculus of modern warfare. And every military on Earth is now racing to build or buy them.

What stands out to me:

AeroVironment is the institutional anchor of this sector. Billions in revenue, massive backlog, the Switchblade franchise. When large allocators rotate into drones, this is the first name they buy.

Red Cat is the high growth pure play. Revenue up 849% and contracts stacking across the U.S., NATO, Japan, and Asia Pacific. If they execute on manufacturing scale, this could be a very different sized company in 18 months.

Kratos bridges the gap between startup innovation and defense prime scale. Valkyrie is potentially the most important autonomous combat aircraft program in the U.S. military.

And Palantir quietly sits behind all of it, building the AI operating system that autonomous drones will run on.

The drone sector is no longer speculative. It's becoming a core pillar of national defense spending. The companies on this map are the ones building that future. Map it now.