Chief Economist @FirstAm. Father and dismal scientist. Runner, biker and beer maker. Views expressed here are personal and not the views of my employer.

Welcome to the fascinating world of industrial real estate! And there's more to it than just data centers. Listen to me "waxing on" about the absorption dynamics :-) with my colleagues @odetakushi and @XanderSnyderX in the REconomy Podcast™: https://t.co/EK1JbaYekF

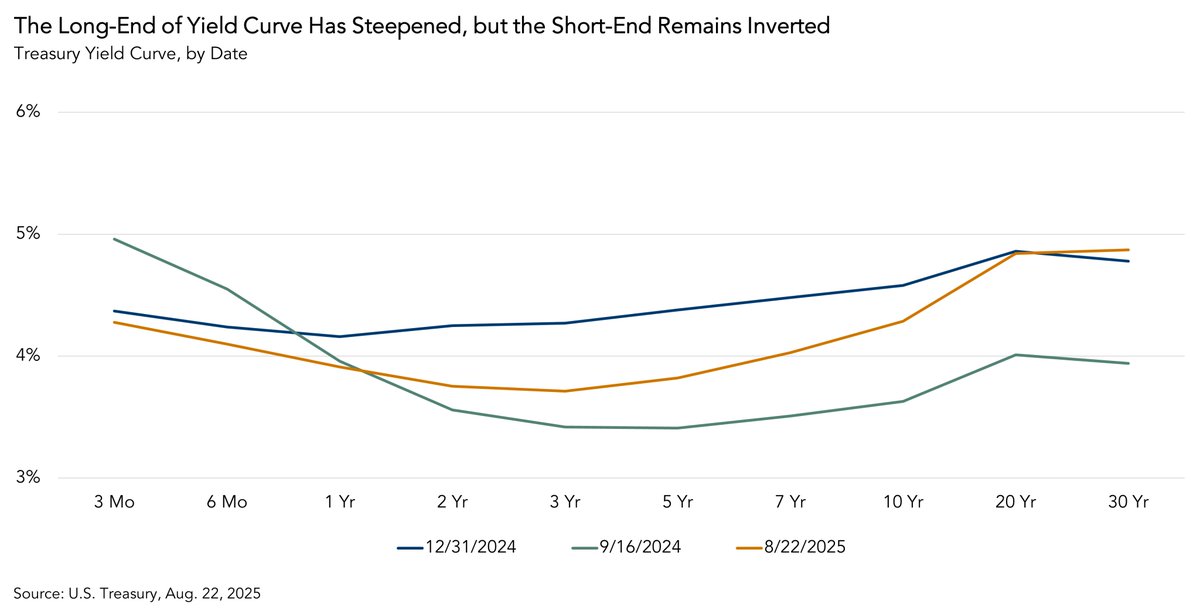

A great point made by @XanderSnyderX - even if the Fed cuts rates there is, unfortunately, no guarantee that "long-end" rates will follow. But, if done for the right reasons, rate cuts can't hurt!

The market has reacted jubilantly to Powell's comments at Jackson Hole today. Powell mentioned that the balance of risks between inflation and employment "appears to be shifting", suggesting that conditions "may warrant" interest rate cuts. He indicated that, though the economy remains resilient with a still-stable labor market, the downside risk to employment has grown.

These seem to be words that the CRE industry has been waiting to hear for several years. Finally, does this mean more rate cuts are at hand? It certainly seems more likely - data from CME shows that the market expectations of a quarter point rate cut in September has jumped to over 90%.

However, caution remains warranted. Remember - the Fed only directly sets short term interest rates. Variable rate commercial mortgages are typically priced based on a spread above SOFR, so Fed rate cuts would directly impact these mortgage rates. However, long term interest rates, like the 10-Year yield, are set by the market*, and it is the 10-Year Treasury yield that many fixed rate commercial mortgages are priced in relation to.

Why am I throwing just a touch of cold water on an otherwise positive rate story? Because it's plausible that short term rates decline while long term rates stay where they are. This would not provide nearly as much relief to commercial borrowers as the market seems to be expecting.

* The Fed can indirectly influence long-term interest rates by buying and selling bonds.

#JacksonHole #Fed #InterestRate #CommercialMortgages

And CME odds of 25bps is over 90% now compared to 75% yesterday. But pick your day and economic release as far as what the market thinks the Fed will do!

Powell cautiously tees up a cut: “The balance of risks appears to be shifting.”

While labor markets remain in balance, “it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers.”

“This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.”

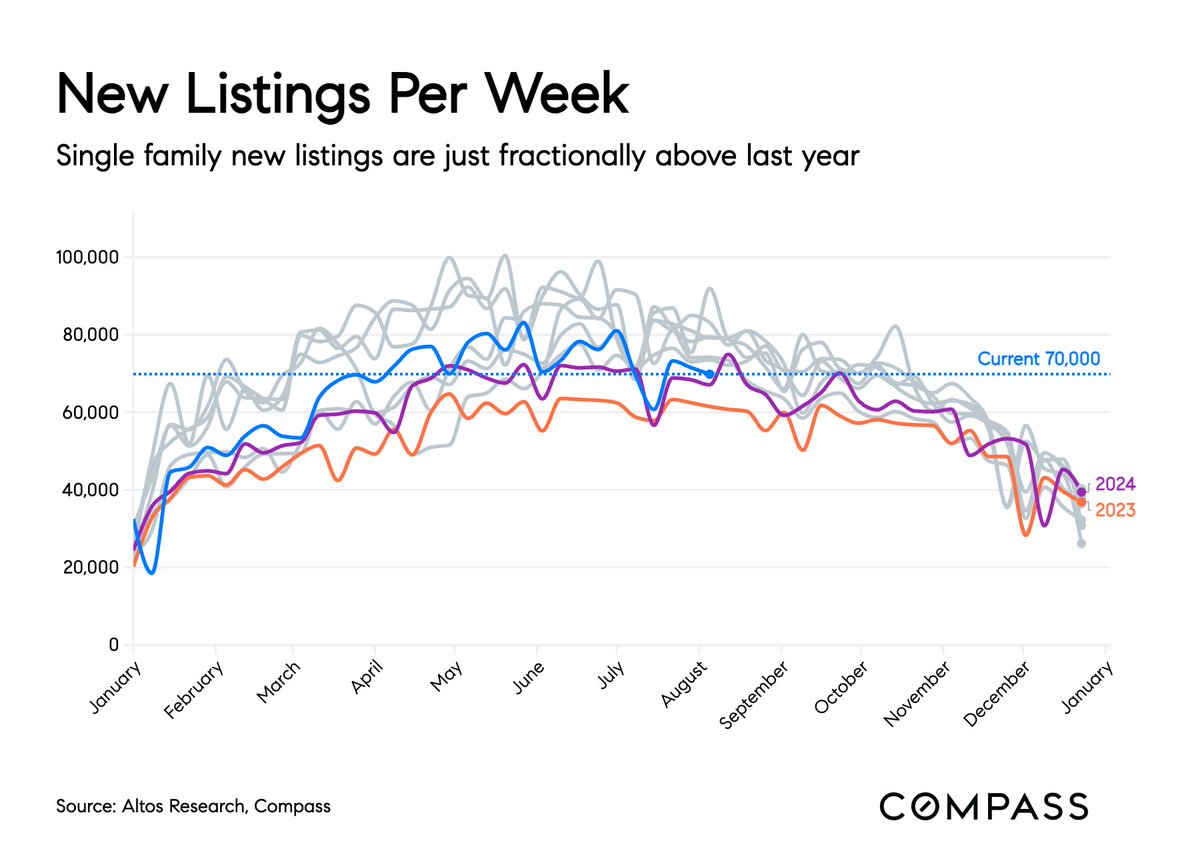

This week in @Compass Intelligence weekly housing market data:

Everyone knows that the price pressure is on. Did you know that have been gradually FEWER new listings each week?

Sellers are staying away.

That implies a cap on inventory growth for the rest of the year.

1/6

We are at the beginning of a new "more normal" housing market, but this time the reasons for growth will be different. Read on to find out more from @odetakushi : Housing Market Turning Point: Setting the Stage for a New Real Estate Cycle https://t.co/VB7EznatdP

If only we could build our way out of the housing shortage! In this episode of #REconomy summer school we look at potential solutions... and since its hip to be square.... one solution may be the old-school Sears and Roebuck way! https://t.co/E3C2o7rYqT

To rent or to own... the perennial question! But right now, if you are viewing this as a purely financial decision, its better to rent in many markets! See more and the details by market in the latest from my colleague @odetakushi#FirstAmEcon https://t.co/CfxgQ5VBHT

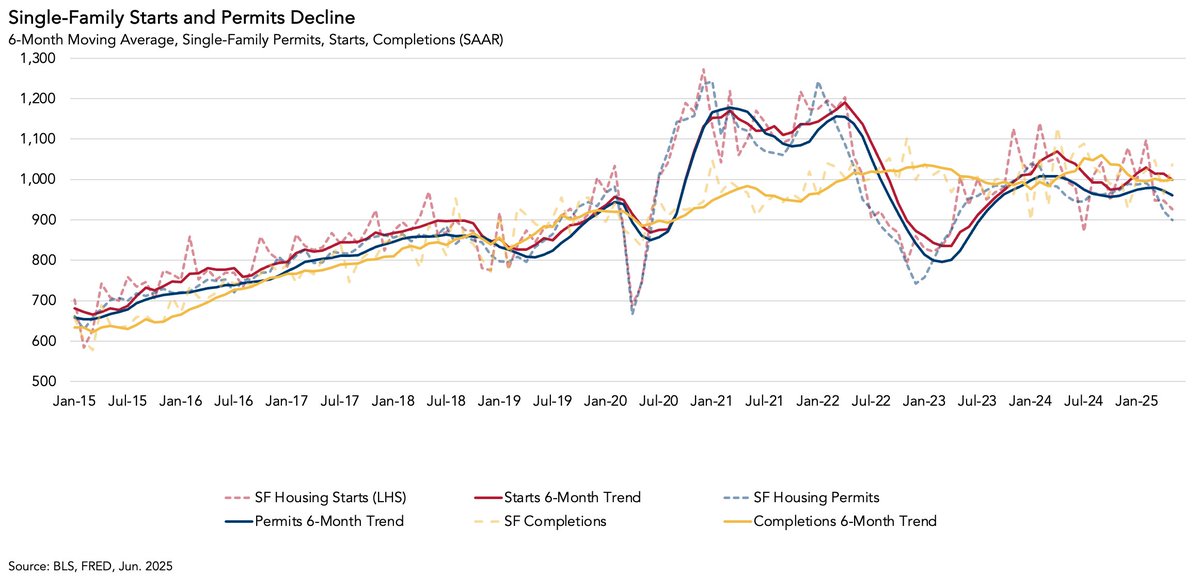

Housing starts rose slightly to a seasonally adjusted annual rate of 1.321 million, coming in just above the consensus expectation of 1.3 million. The 4.6% monthly increase was driven by a sharp 31% rise in the volatile multifamily sector, while single-family starts declined by 4.6%.

Permits, a leading indicator of future construction, came in at a seasonally adjusted annual rate of 1.397 million—also beating the consensus expectation of 1.387 million. The story was similar for permits: multifamily activity rose 8.1%, while single-family permits fell 3.7%. This marks the fourth consecutive monthly decline in single-family permitting. The pullback reflects ongoing affordability challenges, rising material costs and tariff-related uncertainties, elevated new home supply, and growing competition from the resale market. The continued decline in single-family permits, combined with weakened builder sentiment, points to a slowdown in future single-family construction.

Completions matter because they provide immediate relief to a supply-constrained market. Unfortunately, single-family completions fell 12.5% from last month and 15.5% from a year ago, further limiting additions to the housing stock.

In this episode of The REconomy Podcast™ Summer School series we take an in-depth look at the supply side of the housing market and the challenges limiting builders’ efforts to build more homes. https://t.co/ZoSGs5gAVf

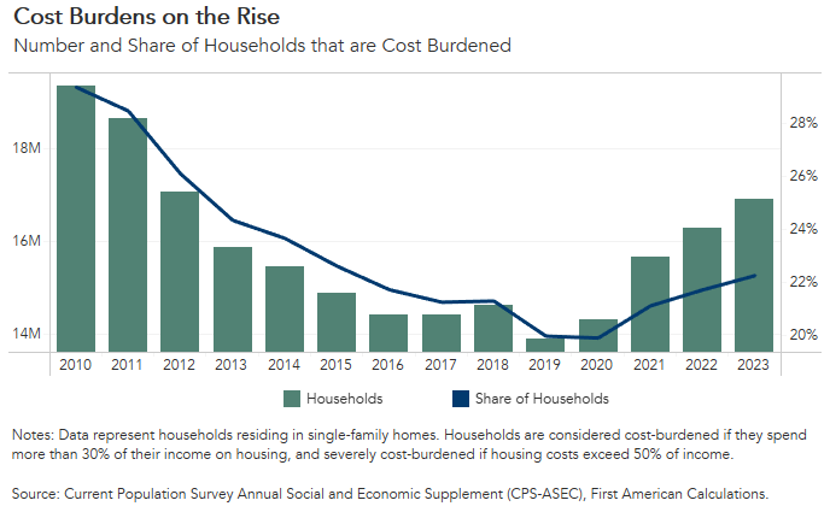

Since 2019, nearly nine in 10 newly cost-burdened homeowners have been either younger adults entering the market or seniors aging in place.

Read more about the rise in housing cost burden in our latest analysis. The analysis includes interactive dashboards, so that you can check out the number and share of households that are cost burdened in your market!

https://t.co/sTMLVGBYyL

Life happens! But that means home selling and buying does too (regardless of rates). In this summer school episode of #REconomy... we break it all down! - Why Life Events Still Drive Home-Buying Demand Despite Affordability Challenges. https://t.co/MbEhSN6JvQ

Inspired by Planet Money's summer school series, we are now doing our own, second year, of REconomy summer school. Ever wonder what a headship rate is? Why housing economics is often more about demographics? Aaaaaand, now you can "watch" the podcast too! https://t.co/xCIdyk7giC

I can 't resist a good Queen/Bowie reference. Check out the latest from @SWilliamsonEcon. Under Pressure: Rising Homeownership Costs Squeeze Housing Affordability https://t.co/L1mRd7AaQv

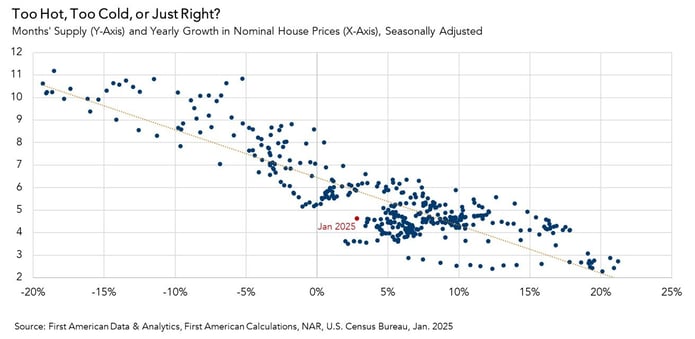

Housing affordability had a rough start to the year. However, affordability improved in February due to slower price growth, a decline in mortgage rates, and positive income growth. Inventory is expected to rise in 2025, which should continue to cool price growth and improve affordability.

In this latest research, @mflemingecon lays out three scenarios for 2025 depending on how months' supply changes and impacts price growth:

1) If price appreciation stabilizes near where it currently is, affordability will improve by 3.5 percent by year's end

2) If months' supply increases to 6 months, which would indicate a more balanced market, price appreciation would slow and affordability would increase by 4 percent by year's end.

3) If sales outpace inventory growth, prices would re-accelerate. If months' supply falls to levels comparable to spring 2024, then affordability would end the year a little worse than compared to the end of 2024.

#Housing #Economics #SpringHomeBuying #FirstAmEcon

While builders benefit from a chronic housing shortage made worse by the “seller’s strike”, they still face supply-side challenges making it difficult to scale up construction to just keep up with growing shelter demand let alone reduce the overall housing stock supply debt.

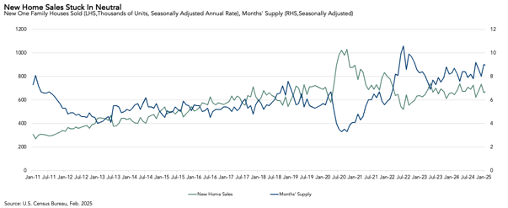

New home sales are improving but well below what’s needed, increasing 1.8% on a monthly basis to 676,000, slightly below the consensus estimate which was predicated on the fact that mortgage rates were declining in February, which is usually a boost to new-home sales.

then new-home sales is down to the same levels as the early 1990s, about 0.5%, and well below the long-run average of 0.7%. If new-home sales were tracking at the long-run average percentage of total households, then the pace of new-home sales would be almost 950,000!