A daily reminder for me to never get too comfortable. A daily reminder to keep stretching myself beyond what I think is possible. A daily reminder to keep engaging in activities that challenge me to become better. A daily reminder to always have fun while aiming for the moon.

Mark Zuckerberg wanted to cure, prevent, and manage all diseases by the end of the century.

He and Priscilla then had a series of meetings where Nobel Prize-winning scientists laughed at them.

Now Zuckerberg says, "I thought that by the end of the century was a stretch. Now I think it's too conservative."

Full episode linked in replies.

The two principal schools of investing:

Value investors, who, out of conviction, buy stocks in the belief that the current value (i.e., fair value) is high relative to the current price (e.g., Intenegins, TIP, etc.).

Growth investors buy stocks even when the fair value is low relative to their current price, because they believe the value will grow fast enough in the future to produce substantial appreciation (e.g., NAHCO, Presco, Nascon, etc.).

The choice really is between value today and value tomorrow. Growth investing represents a bet on a company’s performance that may or may not materialise in the future, while value investing is based on analysis of a coy’s current worth.

Ultimately, both approaches still require an opinion regarding the future (assessing a coy’s worth today still means you need an opinion about the future – and you can be wrong with either).

We spent months building a stock investing product. Apparently, people liked it. 🙂↕️

Cowrywise just won Trading Platform of the Year.

A huge thank you to every customer who trusted us with their first share purchase, first portfolio, and first step into investing.

We're just getting started. 🥳

This has quietly been a miracle month in medicine.

In the last 5 weeks we’ve got news on:

- retatrutide, the triple agonist GLP-1 from Lilly, basically melting fat and body-wide inflammation at record levels

- RevMed’s new pancreatic cancer drug showing unprecedented abilities to extend life

- small trial of a one-and-done PCSK9 gene editing therapy for slashing LDL cholesterol

- Mayo’s AI-assisted radiology showing vastly improved cancer detection

- this new therapy for metastatic solid tumors

This stuff is at varying levels of evidence. Retatrutide is ~100% on its way, other stuff needs more clinical trial data. But put it together and we’re maybe on the verge of majorly reducing the mortality of heart disease and cancer, the two leading causes of death in America.

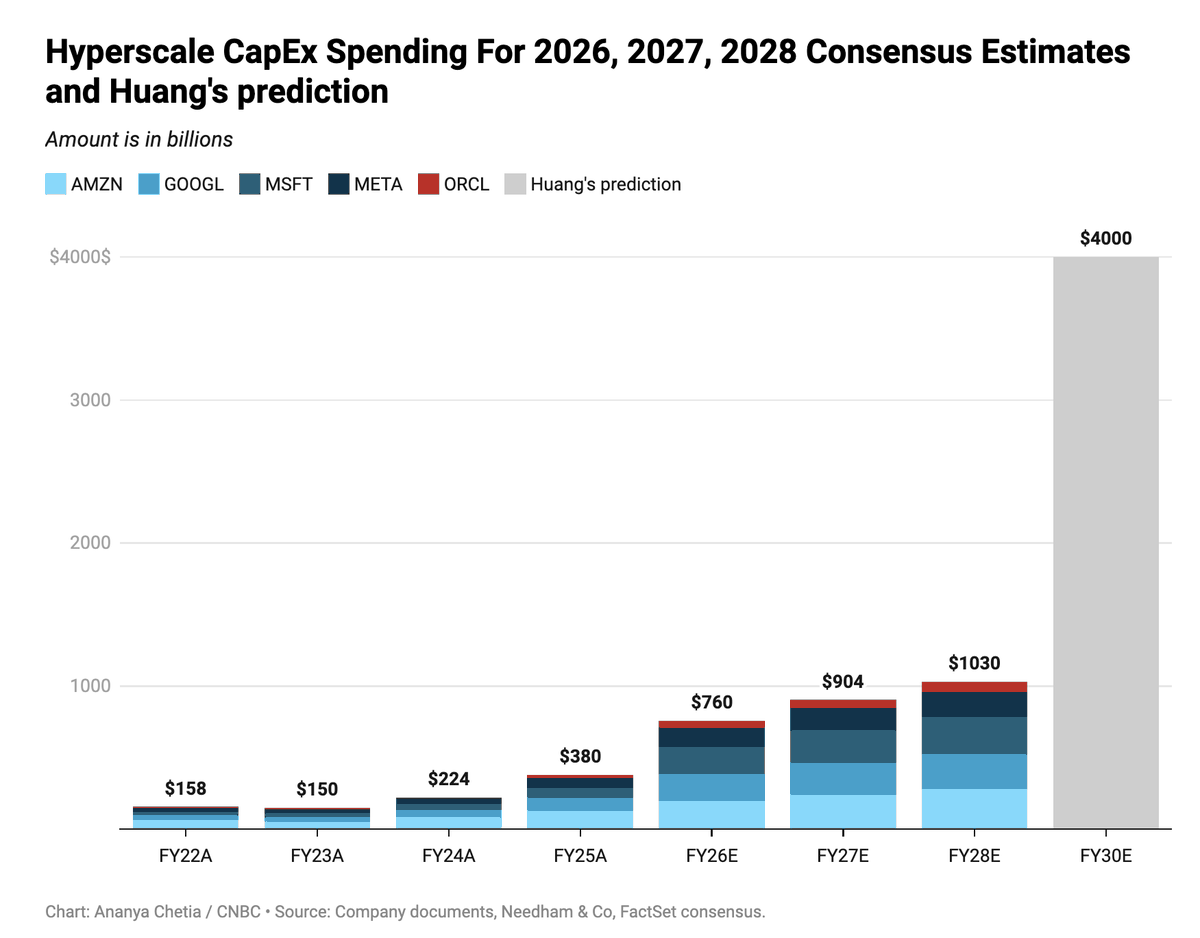

AI capex spend is expected to go to "$3 to $4 trillion annually" by 2030 from $NVDA Jensen Huang projections.

You're not bullish enough.

And it might be a good idea to stay exposed + own the keys of the AI Kingdom:

-> $AXTI controls the materials buildout with photonics.

-> $SOI controls the AI buildout with silicon photonics.

-> $SIVE controls laser chokepoints for CPO.

-> $IQE controls Western epiwafer supply chains for photonics.

All these started off as tiny companies, yet the trillions of projected capex gradually upward to them.

There's many more in other industries as well.

-> AI Capex flows to Neoclouds like $NBIS.

-> AI Capex flows to memory like $MU and $SNDK.

And many of the "commodity" materials or "science projects" for the past 20 years now a sudden shift in exponential TAM expansion.

We're witnessing the next industrial revolution with Artificial Intelligence + Physical AI.

I’ve spent the past couple of weeks building Looters: a public archive of Nigerian political corruption since the 1990s.

Governors, ministers, shell companies, Swiss accounts, the Jersey trusts, — one searchable graph.

You too can connect the dots: https://t.co/faIfzWfAIp

A Guide by Serenity:

How to Cripple the Western Hyperscaler buildout with just $170m.

Just take over Nippon Chemical (4092) with $169m!

For InP substrates, you need: Indium and High Purity Phosphorus.

Thought $AXTI was a bottleneck? NCI is the bottleneck of the bottleneck.

NCI is actually the leader of the high purity red phosphorus chokepoint holding 26-27% of the market share (Rasa has less share, then the rest is China).

And they export to $AXTI, Sumitomo, JX that need it to make InP substrates.

So… if you have $160m to spend to acquire NCI (plus Rasa as smaller capacity), you can remove the leading Western world’s production of 6N/7N red phosphorus needed to make InP substrates!

And without InP substrates: no photonics.

Fun fact: China’s tech companies would get pretty disrupted with it too by NCI.

For $AXTI, the mapping/reliance is actually pretty interesting:

- AXT's Tongmei outlined its structural reliance on importing high-purity precursor materials from Japan on their STAR Market listing

- WITS data showing ~$460/kg high-purity phosphorus flowing from Japan into China

So they secretly do depend on NCI.

China does have capacity like Wylton Chemical, Qin Xi New Materials, Jinding Electronics, and Chuxiong Chuanzhi, Guizhou Wylton Jinglin Electronic Materials as well.

However, they’re all smaller players so can’t make up for high purity red phosphorus capacity provided by NCI for InP substrate production at scale.

$LITE CEO already said inp substrates keeps him up at night.

So now with NCI, you can give the guy permanent insomnia?

For just $169M.

So here's what the supply chain looks like:

-> DGC phosphate rock mine and ships it to NCI

-> NCI refines Yellow Phosphorus into High Purity Red Phosphorus

-> Sumitomo / JX / AXT melt the Red Phosphorus with Indium to grow InP Substrates

-> $COHR / $LITE fab InP substrates into Lasers

-> Innolight/Fabrinet package them into 800G/1.6T transceivers

-> $NVDA / $GOOGL use them for ASIC/GPU clusters.

And basically, the entire West depends on NCI to make InP substrates for photonics.

I hold some very small positions, just for fun. However, Japan is not well known for price hiking.

So you’d probably run into regulatory problems eg. FEFTA if you bought the company and hiked prices 15000% (like government seizing back the company once they realize)…

Maybe 30-50% hikes is possible to compress fwd p/e? But very likely wont end up like $AXTI.

Regardless, this company is a massive, massive national security risk priced at ~$160m.

As for fundamentals, they’re trading at .54 book value and a forward P/E of 11.4 so it’s probably undervalued anyway.

TLDR:

-> Is it the next $AXTI? No.

-> Is it an unknown structural bottleneck + critical vulnerability of the Western hyperscaler buildout with photonics? Yes.

-> Is there still room for re-rating?

Just reverting to Book Value of 1 is immediate 80-85% upside. Maybe more if you give it multiples past 11 fwd p/e.

Regardless, it’s fun to find a major point of failure in the hyperscaler supply chains for $169m.