The $META premium AI subscription angle is WILD.

Meta has 3.5B+ daily users across its family of apps.

If just 1% convert to a $19.99/month AI subscription…

That’s 35M+ subscribers.

35M x $19.99 x 12 = ~$8.5B in annual subscription revenue.

Meta’s current dividend burden annualizes around ~$5.4B.

So at ONLY 1% conversion, a premium AI tier could theoretically generate enough revenue to cover the ENTIRE dividend…

And still have billions left over...

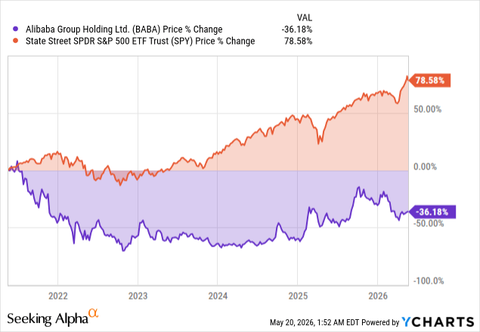

$BABA has massively underperformed the S&P 500 $SPY for years, and anyone pretending this is an easy hold is fooling themselves.

But that’s also why I’m interested around ~$110.

$BABA is a bet. I won’t pretend otherwise.

At ~$110 I think the risk/reward is interesting enough that I’m considering adding again for the first time in almost 2 years.

My last buy was late 2024 around $80. Watched it run to ~$190, now back near ~$110.

Not a clean thesis: China risk, weak FCF, AI capex, margin pressure, e-commerce competition.

But if Cloud/Qwen/AI becomes a real earnings driver, the market may still be underpricing that optionality.

Not my highest conviction idea, but potentially worth topping up the position.

$SOFI CEO Anthony Noto just bought another ~$250K of stock at $18/share.

He has now purchased ~$2.3M worth of shares in 2026 across five separate buys.

Sentiment is so bad right now that the contrarian in me wants to buy more $BABA and $JD. Check out the comments on posts about China 🇨🇳 in the last few weeks.

@Dividend_P That's the real test to your conviction and thesis, when it's moving slower than expected, awful sentiment, and another part of the market is printing money.

Peter Lynch had a great line:

“The typical big winner… generally takes three to ten years or more to play out.”