Why I call the below the most important story in markets / geopolitics?

1) without China importing far less, oil would be way, way above $100

2) Fed would be forced to hike rates, crashing Wall Street

3) President Trump would be against the clock in negotiations with Iran

Rule changes for the SpaceX $SPCX IPO:

Index providers waived the profitability requirement and cut the seasoning window from 90 days to 5.

This forces over $30 trillion in passive 401k and retirement money to buy SpaceX at IPO valuations.

Bloomberg Intelligence estimates S&P 500 funds must absorb 19% of SpaceX's float within 6 months.

Russell 1000 and Nasdaq 100 funds will absorb 24%.

The rules built to protect passive investors:

1. S&P 500 has required 12 months of trading and 4 quarters of GAAP profitability since 2002. Both waived.

2. Nasdaq cut its inclusion window from 90 trading days to 15.

3. FTSE Russell cut its to 5.

All three benchmarks are now structured to buy SpaceX at IPO pricing.

The Soho Society is objecting to *every* new bar/restaurant licence in what is supposed to be the centre of London’s nightlife. More planning/licensing insanity.

I asked them to come on my Sunday LBC show: "We will absolutely not be taking questions from journalists". Of course not.

https://t.co/0UfHJs9Klg

What's happening to oil exports around Hormuz?

• Oman is winning: same barrels at a higher price

• Saudi & UAE: higher prices more than cover volume losses

• Iran: US blockade cut exports by 2/3

• Bahrain, Iraq, Kuwait, Qatar: minimal exports

Analysis on @TheTerminal

Corporate America enters its AI reckoning phase as IT bills keep rising and consumer sentiment nosedives.

My latest, which includes an account from a CFO fretting over a half a *billion* dollar accidental AI bill: https://t.co/EQhgn0v8DI

How Socialist French banker Matthieu Pigasse won a leading role in Venezuela’s massive debt restructuring after strongman Nicolás Maduro’s ouster https://t.co/H4Im2KUwTr

FT exclusive: Saudi Arabia has stopped issuing new contracts for western consultancies working in the kingdom and delayed some payments as the government manages a widening deficit and the fallout of the Iran war https://t.co/1IlM3RyjDO

🚨 Quelles mesures les Français sont-ils prêts à accepter pour réduire le déficit public ? J'analyse les résultats d'une enquête inédite menée en 2026 sur un échantillon représentatif de 1 000 Français.

🧵Voici les 5 résultats qui m'ont le plus surpris :

Returning to something I have been ringing the alarm bell about, here are five things to note about the move in UK yields since the start of the Middle East War (please see the CNBC chart below):

The magnitude is significant: The move is now approaching a full percentage point—a staggering shift in such a short window.

"High Beta" turbocharged: The surge has significantly outpaced movements in other advanced economies, reflecting the UK’s structural "high-beta" characteristics and recent domestic political developments.

Highly eroded buffers: This volatility comes at a time of not only limited policy flexibility but also a thinning of other economic shock absorbers.

"Main Street" as much as Treasury: These yields will not only feed into higher government interest payments but also into mortgage rates and corporate borrowing costs, as well as weaker growth dynamics, placing further pressure on an already strained fiscal situation and the household sector.

Multidimensional fallout: The consequences will likely extend far beyond economics, with ripples across financial, political, and social spheres.

#economy #UK #gilts #growth #markets

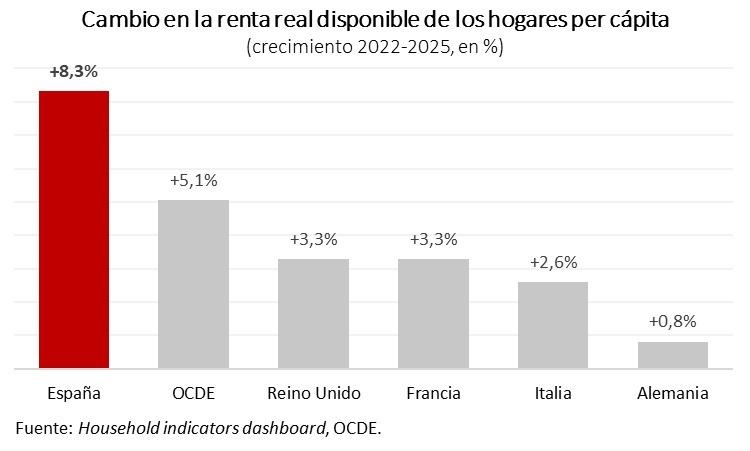

La OCDE acaba de publicar sus datos. Desde el fin de la pandemia, la renta real disponible de los hogares españoles ha crecido un 8,3%. Más del doble que en Francia. El triple que en Italia. Diez veces más que en Alemania.

Solo en el último año, la renta real creció en nuestro país casi el doble que la del promedio de la OCDE.

No partimos desde el mismo punto. Aún queda muchísimo por hacer. Pero la dirección que llevamos es la correcta.

SEGUIMOS 💪🏻

THE CASE FOR MANCHESTERISM by @DantonsHead

Ask someone in Wythenshawe or Rochdale whether the buses are better than they were three years ago and they will say yes. Greater Manchester’s Bee Network is the most instructive public transport experiment in Britain not because it is radical in design but because it works. Since franchising began under Andy Burnham’s leadership, passenger numbers have risen for the first time in a generation. Routes have expanded into communities that private operators had abandoned as insufficiently profitable. Fares are capped at levels the deregulated system could not deliver.

The model is now spreading. A public operator optimising for coverage and frequency rather than fare recovery serves a social need that private calculation screens out, while reducing system costs through public coordination.

Manchesterism works. Public control of essentials reduces the cost of provision by eliminating the privatisation premium and lowering coordination frictions, which in turn reduces the fiscal transfers required to make essentials accessible – progressively deflating the upward pressure on public spending that currently exposes the country to the harsh judgement of bond markets. Rebuilding public provision is not the alternative to fiscal prudence. It is fiscal prudence.

What has been done for buses can be done with similar ambition for energy, water, housing, and care. The architecture operates at multiple scales simultaneously: national corporations for network infrastructure like energy and water, regional and municipal authorities for transport and housing, municipal providers for care and local services. The institutional template is already being built, sector by sector, in the places that have chosen to reclaim public control.

That is why this is an argument for Manchesterism rather than a blueprint for Whitehall – its political character is decentralised, plural and democratically accountable. The question is whether national politics has the ambition to match it.

A sobering statistic from the BLS highlights another dimension of the Main Street/Wall Street divide:

The US labor share of output fell to 54.1% in Q1 2026, the lowest level since this data series began in 1947.

Put another way, labor is consistently capturing a declining share of the value created by productivity gains, with the benefits increasingly accruing to the owners of capital.

#economy #markets #labor #productivity

🔴 Reform UK Treasurer and Donors Share London Address with Sanctioned Russian Oligarchs

Reform UK’s Treasurer and three other donors have handed £1.55 million to Nigel Farage from Britain’s most expensive apartment block which is home to sanctioned Russian oligarchs and massive post-Soviet wealth

https://t.co/VhsrLeqwwK