Imagine a company that just received or raised through IPO of Rs 6,000 crore in cash. And that entire amount is going into building a copper smelting plant and a fertilizer complex. Projects with Rs 40,000-45,000 crore revenue potential and Rs 3,000 crore PAT potential once operational. What should the valuation of that company be? Rs 10,000 crore? Rs 15,000 crore?

Now look at Kiri Industries. Market cap Rs 2,550 crore.

Here is what happened. Kiri owned 37.57% of DyStar, one of the world's largest dye companies based in Singapore. The majority shareholder, Longsheng Group, tried to squeeze them out. Kiri fought back. For 11 years. The Singapore International Commercial Court ruled in Kiri's favour and ordered a buyout at fair value. On 31st December 2025, Kiri received USD 689 million. That is Rs 6,195 crore. For a company that was trading at Rs 3,500 crore market cap at the time.

The stock jumped 20% on the news. And then fell 46% from its highs. Why? Management were not generous with the shareholders.

But here is where it gets interesting. Management is not sitting on the cash. They have announced a Rs 11,700 crore capex plan across two phases.

Phase 1: Rs 2,400 crore for a 2 lakh tonne copper smelting and refining facility in Gujarat. Expected to come online by FY28.

Phase 2: Rs 4,000-5,000 crore to expand copper capacity to 3 lakh tonnes and add a 9 lakh tonne fertilizer plant. Expected by FY29.

When fully operational, management is projecting Rs 40,000-45,000 crore in revenue and Rs 3,000 crore in PAT from these new ventures alone. Even if you discount those projections by 50%, you are looking at Rs 1,500 crore PAT from a company with Rs 2,550 crore market cap today.

Promoters clearly believe in the plan. They increased holding from 36.7% to 41.7% by subscribing to a preferential allotment at Rs 369 per share. When promoters are putting their own money in at current prices while sitting on Rs 6,000 crore cash, the signal is hard to ignore.

The risk is execution. Kiri has never built a copper plant before. They are a dye company pivoting into metals and fertilizers. That is a massive leap. The core dye business is bleeding at the operating level. And copper smelting is capital-intensive, power-intensive, and environmentally complex. If the copper project gets delayed or cost overruns happen, the market will punish this severely.

But the risk-reward is asymmetric. The downside is protected by cash that exceeds the market cap. The upside, if even one of these projects delivers, is a complete re-rating. You are essentially getting the entire dye business, the copper optionality, and the fertilizer optionality for free. The cash alone covers the current price.

That is what makes Kiri Industries one of the most interesting special situations in the Indian market right now.

Views are personal. For educational purposes only. Not investment advice

Vijay Kedia 🔥

It Took Him Nearly 37 Years To Grow His Capital From Just ₹35,000 To Over ₹1,200 Cr.

10 Years to grow from ₹35,000 to ₹1 Cr

13 More years to reach ₹100 Crore

14 Years of conviction to scale from ₹100 Cr to ₹1,200+ Cr

Real wealth explosion happened in the third phase through long-term holding of Quality

Compounders.

Patience truly wins!

Massive respect for the journey. 💯

I was trying to screen for companies below ₹10,000 Cr Market Cap in which BOTH FII and DII holdings increased over the last quarter, along with decent fundamentals.

Found some interesting names across sectors like pharma, defence, cables, heavy electricals, packaging, shipping, auto ancillaries, etc.

Sharing the list below for anyone tracking emerging mid/small-cap ideas

(Please do your own research before investing)

Also, if anyone wants the Screener query I used for this scan, DM me, and I’ll share it.

Some companies worth studying and tracking closely in the current market cycle:

▪ Syrma SGS

▪ Aimtron Electronics

▪ Alpex Solar

▪ Yash Highvoltage

▪ Quality Power

▪ Oriana Power

▪ TD Power

▪ Yatharth Hospital

▪ Apollo Micro Systems

▪ Sky Gold

▪ Pondy Oxides

▪ Lumax Auto

▪ Viviana Power

▪ Prizor Viztech

▪ Senores Pharma

▪ Pace Digitek

▪ Frontier Springs

▪ Fedbank Financial Services

▪ Atlanta Electricals

▪ Shilchar

▪ Jain Resource Recycling

▪ Sansera Engineering

▪ Minda Corporation

▪ Advait Energy

▪ Ashapura Minechem

▪ Pricol

▪ Belrise

▪ SJS Enterprise

▪ Vintage Coffee

▪ Krishna Defence

▪ Khazanchi Jewellers

▪ K.P. Energy

▪ L. T. Elevator

▪ Maxvolt Energy

▪ Freshara Agro

Power infrastructure, defence, electronics manufacturing, renewable energy, hospitals, recycling, AI infrastructure, and industrial manufacturing are some of the themes where strong momentum is clearly visible.

The next phase of the market may reward stock selection much more than blind investing.

Study businesses deeply.

Track earnings carefully.

Observe price action patiently.

That is where real wealth creation opportunities usually emerge.

Disclaimer:

For educational and study purposes only.

Not a buy/sell recommendation.

My friend Rahul bought an under-construction flat in Noida for ₹1 crore in 2020.

Last month, he sold it for ₹1.8 crore.

Everyone around him said:

“Wah! ₹80 lakh profit!”

But then we did the actual math...

GST paid at purchase (5%) = ₹5 lakh

Stamp duty & registration (~7%) = ₹7 lakh

₹12 lakh gone before he even got possession.

At the time of sale:

Capital gains tax = ~₹10 lakh

Brokerage (2%) = ₹3.6 lakh

Total costs: ₹25.6 lakh

So the real profit wasn’t ₹80 lakh.

It was closer to ₹54 lakh in 5 years.

That works out to roughly 9% CAGR.

For comparison:

1. FDs delivered ~7%

2. Mutual funds gave ~11%+

3. Some YEIDA land parcels appreciated 20-25% annually

Yet whenever someone buys a flat, people celebrate the sale price.

Almost nobody talks about GST, stamp duty, taxes, maintenance, brokerage, and the years of locked-in capital.

The question is:

Are people buying flats for returns, or just because real estate “feels” safer than other investments? 🤔

Would Rahul have been better off putting ₹1 crore somewhere else?

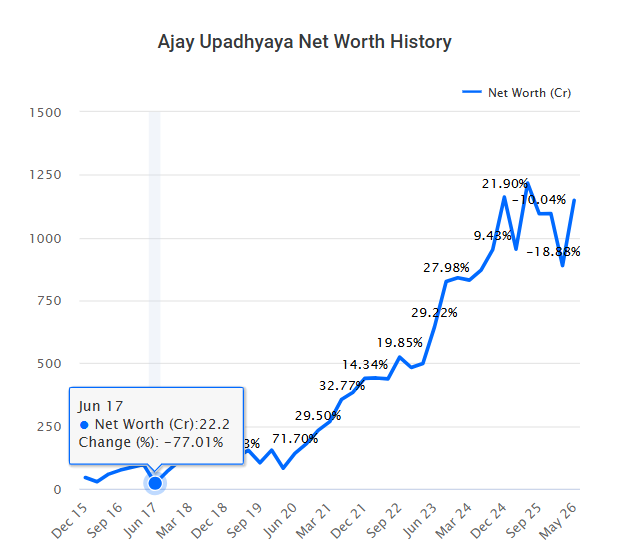

Ajay Upadhyaya 🔥

From A BITS Pilani Engineer to building a ₹1,100+ Cr listed equity portfolio.

Portfolio Growth:

Dec 2015: ₹45 Cr

Mar 2025: ₹973 Cr

Mar 2026: ₹1,164 Cr

Some remarkable wealth creators:

Invested ₹5 Cr in Navin Fluorine & Made ₹370 Cr

Invested ₹12 Cr in Genus Power & Made ₹125 Cr

Invested ₹11 Cr in Elecon Engineering & Made ₹204 Cr

Spots a macro tailwind (like the massive capex shift into engineering & chemicals), picks the clean managements, and sits tight.

Reiterating again 🙏🙏🙏

Dont miss this mega mega theme coming once in lifetime of capex cycle and our lifecycle 😁

Samajdar ko ishara hi kaafi hai 💡 ⚡

https://t.co/HPWwEhVtEr

📌𝐀𝐬𝐡𝐢𝐬𝐡 𝐊𝐚𝐜𝐡𝐨𝐥𝐢𝐚’𝐬 𝐖𝐞𝐚𝐥𝐭𝐡 𝐂𝐫𝐞𝐚𝐭𝐢𝐨𝐧 𝐉𝐨𝐮𝐫𝐧𝐞𝐲:

🔥𝟓 𝐋𝐚𝐤𝐡𝐬 𝐭𝐨 𝟑𝟎𝟎𝟎+ 𝐂𝐫𝐨𝐫𝐞𝐬

𝒀𝒆𝒂𝒓𝒘𝒊𝒔𝒆 𝑩𝒓𝒆𝒂𝒌𝒐𝒖𝒕:

✴️1993 → Started with ₹5–10 lakh

✴️2000 → Crossed ₹1–2 crore

👉 10X in 7 Years Is Easily Possible When Capital Is Low & You Get The Benefits of Compounding.

🟢CAGR - 32%

✴️2005 → Achieved ₹20–25 crore

✴️2007 → Captured Bull Run → ₹100 crore

👉100X in 7 Years Is Unbelievable, Though We Had A Great Bull Run 2003-2007.

🟢CAGR - 66%🔥

🔴2008 → Crashed ~₹30–40 crore

✴️2010 → Back above ₹100 crore

✴️2014 → Achieved ₹400 crore

✴️2017 → Crossed ₹1,000 crore

👉10X in 10 Years After Surviving Financial Crisis 2008.

🟢CAGR - 26%

✴️2020 Pandemic→ ~₹900 crore

✴️2021 Crazy Rally → ~₹1,500–1,800 crore

✴️2023 → ₹2,500 crore

✴️2024 → ₹3,000+ crore

𝐁𝐨𝐭𝐭𝐨𝐦 𝐋𝐢𝐧𝐞:

Building Wealth Takes Time and Needs Consistency.

Compounding Effect Is Beyond Your Imagination.

Source: @ChatGPTapp@LuckyInvest_ARK sir, is this information correct?✴️

My manager paid ₹1.5 crore for a 21th floor flat.

He sold it after 4 years.

Yesterday he told me everything. And he was ANGRY.

High-rise flat owners will NOT want to read this.

Reason 1 /13

They told me higher floors have no mosquitoes. Biggest scam ever.

From portfolio of ₹22 Cr in 2017 to making it ₹1200 Cr in 2026.

Ajay Upadhyaya has made it really big in investing.

Made over :

70x in Navine Flourine

18x in Elecon Engineering

10x in Genus Power

Bought a company in yesterday's bulk deal.

De Neers Tools.

A tiny company with a market cap of ₹200 crore has delivered excellent results.

Revenue: ₹1,780.3 million, up 23.0% YoY

EBITDA: ₹387.3 million, up 50.0% YoY

Margin expanded to 21.8% (from 17.8%)

PAT (Net Profit): ₹252.9 million, up 60.5% YoY

The company expanded its SKU portfolio to over 9,500, its dealer network to 352+, and strengthened its OEM ties.

It also announced a 51:49 JV for backward integration in tools manufacturing.

Disclosure: Holding.

You earn ₹2 lakh a month.

His first salary was ₹1000.

He built a villa. You can’t even rent one.

I sat with a 72 year old retired banker in Delhi last month. What he told me about the Indian rupee, no CA, no SIP advisor, no expert will ever say.

Especially the last part.

🔥 30 Dhurandhar Management Guidance Stocks

- Deep Industries – 30–35% growth for FY27 and FY28

- Zinka Logistics – 30%+ growth for next couple of years

Sky Gold & Diamonds – 30–35% growth for next 4 years

Sarda Energy – 20%+ growth for next 3 years

- Atlanta Electricals – 40%+ growth for next 2 years

- Gravita Ltd – 35% growth for next 4 years

Anand Rathi Wealth – 25% growth for next few years

- Zen Technologies – 50%+ growth for next 2 years

- Frontier Springs – 30%+ growth for next couple of years

- Genus Power – 33%+ growth for FY27

- Macfos Ltd – 40%+ growth for next 2–3 years

- Azad Engineering – 25–30% growth for next few years

- KEI Industries – 20%+ growth for next 3–5 years

- Va Tech Wabag – 20%+ growth for next 3–4 years

- Epack Prefab Tech – 20%+ growth for next couple of years

- Pondy Oxides & Chemicals – 20%+ growth for next 4 years

- Namo eWaste – 40–50% growth for next 2 years

- Baheti Recycling – 30–35% growth for next 2 years

- Sunlite Recycling – 20%+ growth for next 3–4 years

- Tinna Rubber & Infrastructure – 25%+ growth for next 2 years

- Antony Waste Handling Cell – 20%+ growth for next few years

- Shilchar Technologies – 20%+ growth for next 2–3 years

- Krishna Defence – 30–40% growth for next few years

- Airfloa Rail Technology – 50% growth for next 2 years

- Supreme Power Equipment – 50% growth for next 2 years

- Danish Power – 20–25% growth for next 3 years

- BLS International + – 20–25% growth for next 5 years

- TARIL– 40%+ growth for next 3 years

- Acutaas Chemicals – 25%+ growth for next 3 years

- Neogen Chemicals – 40%+ growth for next 3–4 years

Any on your radar?

Coal Gasification. India's largest import substitution plays since solar.

The Cabinet just approved a ₹37,500 crore scheme to back it. The headline number is not the real number.

The real number is ₹2.77 lakh crore. That's what India paid last year importing LNG, urea, ammonia, methanol and ammonium nitrate. Every product on that list can be made from coal.

Almost nobody is asking who is already building this.

So, I went and pulled the order book.

First, what coal gasification actually is.

It converts coal into syngas, a mix of carbon monoxide and hydrogen. Syngas then becomes methanol, ammonia, urea, ammonium nitrate, Synthetic Natural Gas, hydrogen and industrial fuels. So instead of paying foreign suppliers in dollars, India pays domestic miners in rupees.

The scheme:

🔹 Outlay: ₹37,500 crore

🔹 Target: gasify 75 MT of coal (national goal 100 MT by 2030)

🔹 Investment expected: ₹2.5 lakh crore to ₹3 lakh crore

🔹 Subsidy: up to 20% of plant and machinery cost

🔹 Cap per project: ₹5,000 crore

🔹 Cap per product (except SNG and urea): ₹9,000 crore

🔹 Cap per entity group: ₹12,000 crore

🔹 Coal linkage extended to 30 years

The 30-year linkage is the line most analysts will miss. Coal gasification plants are ₹10,000 crore plus capex. No board commits that without feedstock certainty for the full asset life. This is what de-risks the entire scheme.

The order book is not theoretical. The new ₹37,500 crore outlay builds on the ₹8,500 crore scheme from January 2024 under which 8 projects worth ₹6,233 crore are already in execution. The pipeline has been quietly building for 18 months.

The value chain has four layers. Here is who is already in.

👉Layer 1, coal owners:

🔹 Coal India: parent of BCGCL (JV with BHEL for coal-to-ammonium nitrate, ₹11,782 crore at Jharsuguda) and CGIL (JV with GAIL for coal-to-SNG at Sonepur Bazari, ₹13,052 crore). Plus, a standalone ₹12,214 crore coal-to-SNG project in Maharashtra. ₹1,350 crore incentive already received per project.

🔹 NLC India, NTPC: lignite and coal-linked optionality.

👉Layer 2, technology and EPC:

🔹 BHEL: 49% equity in BCGCL. Won LSTK-1 (gasification + air separation + steam) and LSTK-2 (raw gas purification) of the BCGCL project. Uses its own indigenous Pressurised Fluidised Bed Gasifier technology. The only Indian company with a commercial coal gasification tech stack.

🔹 Larsen & Toubro: won LSTK-3 (ammonia synthesis) and LSTK-4 (nitric acid + ammonium nitrate + prilling) of the same BCGCL project. Both booked as "large" orders by L&T Energy Hydrocarbon Onshore.

🔹 Thermax, ISGEC Heavy Engineering, Triveni Turbine: second-order exposure on boilers, steam systems, turbines and auxiliaries.

👉Layer 3, downstream chemicals and fertilisers:

🔹 GAIL: equity in Talcher Talcher Fertilizers Ltd and CGIL plus offtake economics on coal-to-SNG.

🔹 RCF, NFL, GNFC, GSFC, Chambal, Coromandel, Tata Chemicals: long-cycle demand and feedstock optionality.

👉Layer 4, ammonium nitrate, methanol and explosives users:

🔹 Deepak Fertilisers and Petrochemicals: 40% market share in Technical Ammonium Nitrate. 587 KTPA current capacity. Building 376 KTPA expansion at Gopalpur for Q1 FY27 that takes total past 1 MMTPA. Backward integrated via 500 KTPA ammonia plant at Taloja that cut India's ammonia imports by roughly 20%. Also, one of India's five major methanol producers.

🔹 Solar Industries: India's largest industrial explosives player. Heavy AN user. Margin sensitive to domestic AN economics.

🔹 GNFC: methanol, formic acid, acetic acid. Signed 50-50 JV with INEOS in November 2024 for a 600 KTPA acetic acid plant at Bharuch.

🔹 Petronet LNG, Gujarat Gas, IGL, MGL: substitution-risk angle over a decade as coal-to-SNG scales.

So, who makes money first?

Order book visibility is highest today for BHEL and L&T. Both have already converted BCGCL into hard orders. The ₹37,500 crore outlay expands the addressable pipeline by roughly 9x to 10x over the previous scheme. EPC and gasification equipment is the cleanest near-term play.

Coal India benefits two ways. Direct equity in three gasification projects with ₹1,350 crore per project already received. Indirect: 1.3 MT annual captive coal offtake into BCGCL alone is the kind of long-tail thermal coal demand that protects against the secular decline narrative.

Deepak Fertilisers benefits through market structure. BCGCL's 0.66 MMTPA eventually competes, but India today still imports ammonium nitrate from Russia. The near-term effect is domestic AN scaling without import dependence, lining up with Deepak's own 1 MMTPA expansion.

Most policy announcements fade in one news cycle.

This one looks like a 5–10 year industrial buildout.

India is trying to convert its largest domestic resource into a substitute for its biggest import vulnerabilities.

First-order winners: coal owners and EPC giants.

Second-order winners: chemicals, fertilisers and industrial explosives.

Long-term pressure point: gas-import-linked margins.

📌Disclaimer: For educational purposes only. Not a buy or sell recommendation.

Dear FM Madam @nsitharaman ji,

I have said it before. And I'll say it again. Loud & Clear.

LTCG of 12.5% on Equities is one of the Lowest in the World.

But there are a few issues:

1. LTCG was ZERO from 2004 to 2018. STT was introduced to offset the Loss in Revenue. It incentivised long term Investors to Hold on Patiently and enjoy Long Term Returns. I believe that Step was something Golden and rewards Long Term Thinking. FM Madam should reconsider this. Keep STT. Abolish LTCG.

2. STT is already taken for every transaction. This is a tax. Again putting Capital Gain, especially on Long Term Gains is not Ok. This is my Opinion. STT is borne by the investor irrespective of Profit or Loss.

3. We are not against Paying Taxes. In fact, we all Pay Income Tax, Capital Gains Tax, GST, Excise, VAT, Tax on Dividends and what not. The problem is the Freebies which are Distributed during the Elections. This is not at all ok. We don't want a single rupee of our Capital Gains to be used for Freebies. Please.

I humbly request the FM Madam to Abolish LTCG on Equities. Make the Long Term Period 24 months instead of 12 months. You will see Patient Capital 👍

For Indian Investors like me, the Pain is lesser. We will continue to Create Wealth. But what about our FII brothers & sisters. They also deserve to get minimum returns in Dollar Terms.

I feel for the FIIs who have suffered due to declining Rupee and they still have to pay LTCG on Rupee Terms. Something the FM Madam and team should revisit.

I think that it is a good time to implement this. FII no longer control our markets. Domestic Funds are consistent and plenty. If FIIs leave, let them Leave with Head Held High. That is our Responsibility.

India Structually is Brilliant. Let's make it Tax Friendly as well.

Patient Capital will Flow More & Stay, if these Steps are Taken.

A Proud Indian Investor,

#FI