I think this is a misconception. CEO hasn’t sold a single share since IPO. The two other founders haven’t sold shares since I think May 2025 (it has been a long time) and the rest of mngt that has sold; it has always been for taxes which is a very reasonable thing to do. The only person that has sold more than just for taxes is Tami Rosen and I hope it’s bc she’s on her way out. I have never heard anything positive about her people skills. She was “promoted” to a board role only.

$PGY: “Pagaya has built a differentiated, institutional-grade platform for accessing consumer credit. We’re excited to partner with Pagaya to support the continued growth of its point-of-sale strategy, while offering our investors consistent exposure to short-duration assets with highly attractive risk-adjusted returns and durable income,” said Philip Bartow, Head of Specialty Finance and Fintech Lending & Portfolio Manager at Sound Point.

That is a compelling statement from their new partner

From what I could tell, this is a large deal for Sound Point. It sounds like conviction.

@PatientInv618ng 110m. My own calc trying to pull things together. Just the 160 convert is 11m+. So, if they redeem in cash. that drops my figure below 100m. I would go back thru 10k/q's for footnote detail. OR, just ask Chat/Claude to give you a good ballpark figure (using these sources)

It's been fully diluted above 100m for a long time (think 2024 convertible preferred). If the company was reaching valuation extremes then I'd worry but it's not. If cash flow comes in then I think Pagaya is likely to redeem in cash and not shares which brings down the "fully diluted" number.

$PGY: Some thoughts on this new debt structure. Announced $350 (really much larger) debt deal with 26 North and others.

A few things that might go unnoticed here:

The "hybrid" structure is doing a lot of work.

This appears to be a Reg D private placement throughout. That matters because Reg D deals are exempt from Dodd-Frank's 5% risk retention requirement. Pagaya = ZERO in this deal. No risk retention like Forward Flow deals.

And even if retention was required, the revolving feature is a great mechanism. $350M deal size supports ~$700M in throughput over 24 months. Retention would likely be calculated on the initial $350M, not the cumulative volume. Capital efficiency on top of capital efficiency.

From a risk retention angle, this acts like a forward flow deal. But it's better:

Forward flow:

- Single counterparty

- Servicing may transfer

- Need new commitments to reinvest

Revolving ABS:

- Can syndicate to many in Phase 2

- Pagaya likely retains servicing fees

- Reinvestment built in for 24 months

Capital efficiency of forward flow. Syndication optionality and servicing economics of ABS. Best of both.

And this is just the 1st one.

Gal has said PGY is targeting 3-4 of these structures in 2026. If each looks like this deal, that's $1B+ in deal capacity supporting $2-3B in throughput. All with zero or minimal retention. Scale the model, not the balance sheet.

The timing tells a story.

PAID 2025-REV1. Announced January 16, 2026. PGY names deals by year of issuance. A 2025 deal that just made it out. Infrastructure in place. Fully loaded heading into 2026.

The partners matter.

26North is one of the initial investors. Josh Harris's firm. Co-founder of Apollo, $32B platform.

Blue Owl. Castlelake. Now 26North and others. Pagaya is building a network of sophisticated capital partners who want access to their origination engine. Forward flow for those who want whole loans. Revolving ABS for those who want securities. Same engine feeding both.

I'll be interested what they highlight on the call in a couple weeks.

$PGY: Pagaya keeps on executing = secures $350M of 2-Year funding that can flex up to $700M

Pagaya Launches A Revolving Asset-Backed Funding Structure Backed by Personal Loans with Investment from 26North

Pagaya expands its Personal Loan PAID ABS platform through an innovative, hybrid Public/Private revolving ABS structure

Inaugural $350 million PAID 2025-REV1 transaction provides Pagaya with an additional form of long-term funding capacity over a two-year revolving period tailored to insurance capital and asset managers

Transaction establishes up to $700 million in flexible funding capacity, creating a new scalable, long-term source of capital for Pagaya

NEW YORK--(BUSINESS WIRE)--Jan. 16, 2026-- Pagaya Technologies LTD. (NASDAQ: PGY) (“Pagaya” or “the Company”), a global technology company delivering AI-driven product solutions for the financial ecosystem, today announced the closing of PAID 2025-REV1, a $350 million asset-backed securitization (ABS) backed by consumer loans originated on the Pagaya network.

This transaction is the first of its kind for Pagaya’s personal loan business and establishes another form of long-term capital supplementing Pagaya’s market-leading public ABS platform. This initial revolving structure was completed in partnership with affiliates of 26 North Partners LP.

This new revolving Personal Loan ABS product, structured by Pagaya’s Capital Markets team, is designed for insurance capital and asset managers. The revolving nature of the deal structure enables Pagaya to reinvest capital as loans are repaid over a 2-year period, further diversifying Pagaya’s asset funding platform. The inaugural $350 million PAID 2025-REV1 transaction features a 24-month revolving period, effectively doubling the total transaction funding capacity to up to ~$700 million over the life of the deal.

“We designed this structure in a liquid security format with a 24-month revolving period for insurance capital and asset managers seeking access to consumer credit with attractive carry and reinvestment potential,” said Sahil Chandiramani, Pagaya’s Head of Capital Markets. “We focus on bringing market-ready structures that are built for our investors and provide sustainable funding to enable our Lending Partners to grow. We are excited to partner with 26North on this new format and build a longstanding relationship.”

Pagaya is expected to onboard several new lending partners in 2026 across its Personal Loan, Auto Loan, and Point of Sale Loan segments. This structure, which is similar to the Point of Sale ABS structures previously launched in 2025, will create efficient and sustainable funding for Pagaya’s expected expansion of their personal loan market.

“In a market of persisting uncertainty, we continue to drive product innovation as a leader in consumer credit structuring and we’re kicking off the year focused on highly disciplined growth,” said Evangelos Perros, Chief Financial Officer of Pagaya. “We will continue to diversify our funding and our lending partner network through innovative structures and products. We are thrilled to partner with 26North, an alternatives-focused platform strategically aligned with Pagaya.”

Original PR: https://t.co/20jx3Hl1CY

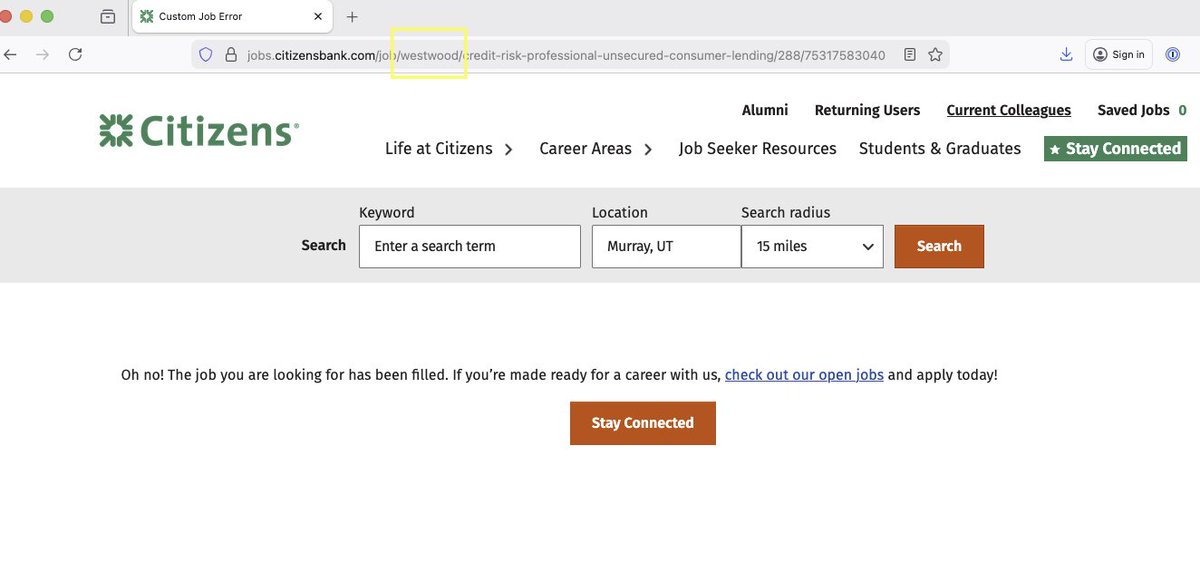

$PGY CFG is building out a team. Look at this job I found that has been filled as well. In the URL you can see that it says location is "Westwood" which is in Massachusetts. It was for a "Credit Risk Professional" in "unsecured consumer lending".

The First Link Senior Risk position I shared in Oct also listed Westwood as a location for the position.

Westwood, MA Campus (200 Station Dr.):

Houses: Operations, Consumer Banking, Wealth Management, Technology, Data & Analytics, Enterprise Marketing

- The Credit Risk Professional for Unsecured Consumer Lending was specifically slotted for Westwood

- This is where the Consumer Lending Strategy & Business Analytics team appears to be based (per the Manager - Business Insights role which is also in Westwood)

$PGY - CFG released earnings today. Nothing related to Pagaya BUT the job posting shows filled. You can see that the specific url points to the job I posted about and Citizens returned a webpage saying the job has been filled.

$PGY: Citizens Bank may be the “top-20 U.S. bank” Pagaya referenced as relaunching its personal-loan business.

From Pagaya’s Q2 2025 Shareholder Letter:

“…we are currently in the onboarding stage with a top-20 U.S. bank by assets, to help in the re-launch of their personal-loans business…”

Citizens Bank ($220 B in assets) fits the description perfectly:

➡️Previously offered personal loans, later exited

➡️Currently not offering new personal loans

➡️Operates as a large regional across New England, NYC, and the Midwest.

And here’s the kicker:

Last week, Citizens participated in expanding Pagaya’s loan facility alongside Wells Fargo

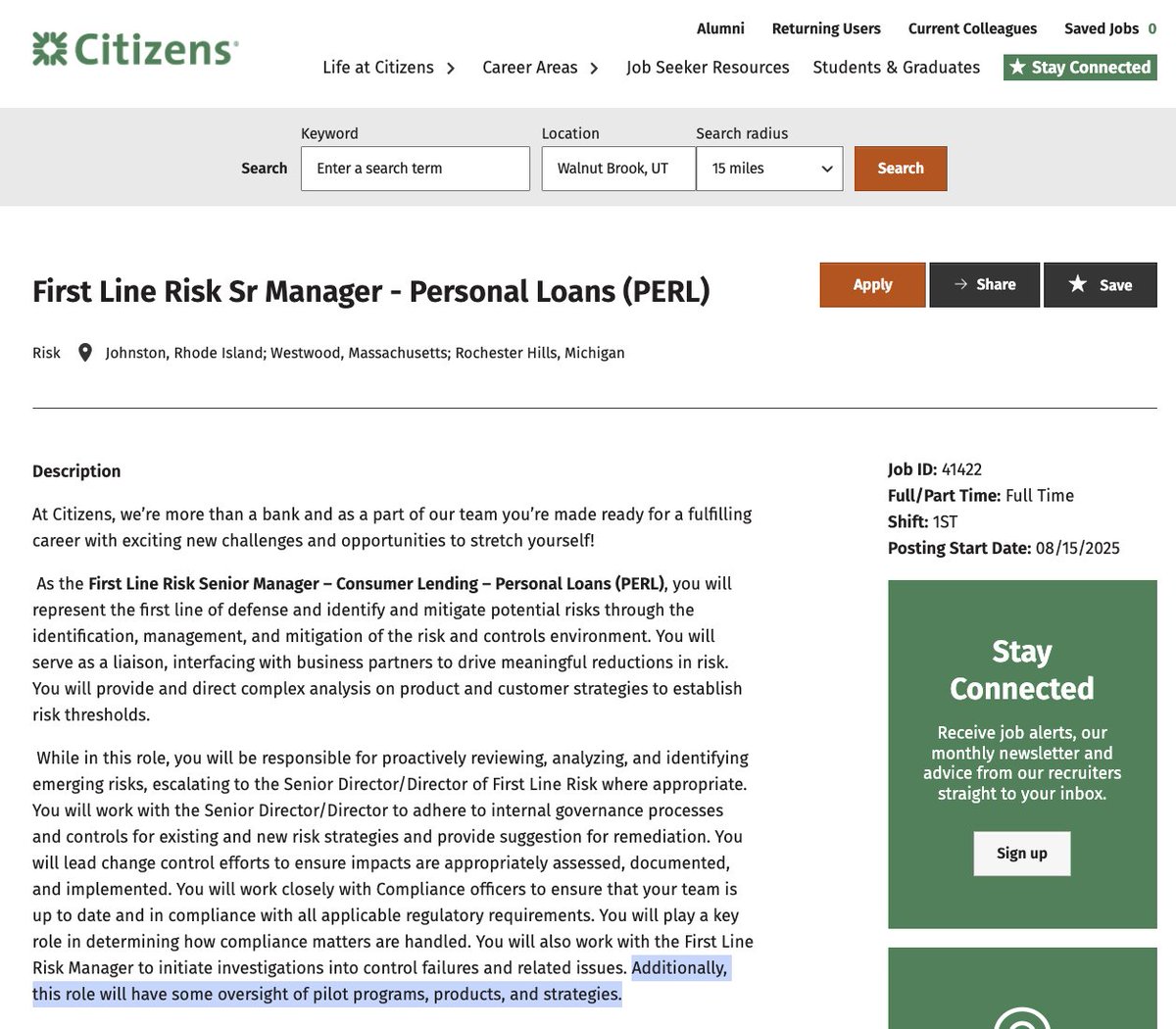

Still don't believe me? Even more interesting, a new Citizens job posting references a “pilot program” for personal loans. I think that's pretty compelling, don't you? 👇

🔗 https://t.co/YPx2nepCva

I believe Citizens is one of several large banks that Pagaya is working with. This could potentially mark the start of a major second wave of institutional adoption.

@BDbayc Nothing that I can see. Did you notice anything in footnotes or listen to the call? But, I did go back to the job posting by CFG and it now says "filled". Seems positive.

$PGY: Citizens Bank may be the “top-20 U.S. bank” Pagaya referenced as relaunching its personal-loan business.

From Pagaya’s Q2 2025 Shareholder Letter:

“…we are currently in the onboarding stage with a top-20 U.S. bank by assets, to help in the re-launch of their personal-loans business…”

Citizens Bank ($220 B in assets) fits the description perfectly:

➡️Previously offered personal loans, later exited

➡️Currently not offering new personal loans

➡️Operates as a large regional across New England, NYC, and the Midwest.

And here’s the kicker:

Last week, Citizens participated in expanding Pagaya’s loan facility alongside Wells Fargo

Still don't believe me? Even more interesting, a new Citizens job posting references a “pilot program” for personal loans. I think that's pretty compelling, don't you? 👇

🔗 https://t.co/YPx2nepCva

I believe Citizens is one of several large banks that Pagaya is working with. This could potentially mark the start of a major second wave of institutional adoption.

$PGY: Two years ago, Pagaya quietly mentioned a new product that caught my attention.

Buried on page 15 of their Q3 2023 shareholder letter: they had tested "data-driven advisory services to optimize the loan life-cycle." It had generated just over $1 million in EBITDA with potential to scale to $10 million+ annually.

I've been waiting to hear more ever since.

Pagaya's core business is volume-based. They earn fees when loans get funded. Advisory services would be different. Pure technology and fee-based revenue, decoupled from whether a loan actually gets booked. That's meaningful diversification.

Then the product disappeared from the narrative.

Fast forward to today. Pagaya's President, Sanjiv Das, just published a LinkedIn article asking: Why does credit still feel fragile when banks have more data than ever?

His diagnosis cuts to a real problem. Each bank only sees its own portfolio. Bureau data is backward looking. When uncertainty rises, lenders lack the visibility to make surgical adjustments. So they tighten broadly, cutting off creditworthy borrowers along with risky ones.

Das argues lenders need network level signals, real-time feedback loops, and cross product visibility.

Think about what that means for a bank. Instead of waiting months for delinquency trends to surface in their own book, they'd see stress emerging across a network of 31 lenders in real time. They'd understand how their borrowers behave across auto, POS, and personal loans. Not just the single product they originate. They could run challenger models against their own underwriting to find where they're leaving money on the table.

For a lender trying to grow through volatility, that visibility is a competitive advantage.

Pagaya is one of the few companies positioned to deliver it. They sit at the center of 31 lending partners and 150+ institutional investors, processing billions in application flow quarterly across multiple asset classes. They have the system level view Das is describing - the one individual lenders lack.

Same data asset they already have. New revenue stream! Stickier partner relationships!

Is Das laying groundwork for something bigger?

Earnings are a few weeks out. I'll be listening for it.

@EverosPatrikos He proposed capping credit card rates. Pagaya won't have a cap. But, I think this is a moot issue. If credit card companies pull back access (b/c 10% cap on interest) to credit via credit cards then the US economy contracts. Trump doesn't want that.

@NapkinMath Grabbed an analyst estimate from May 2025. Not a surprise.

Can go back to 2024 and show the AVG weight for 2025 was 87m. If 93m in Q4 then average is going to be 85.2m. So it has trended down since 2024.

$PGY: Bullish.

Earnings are being reported earlier than in prior years; 4 days earlier than 2025 & 12 days earlier than 2024. The release is scheduled for a Monday.

Last year, the Q4 earnings date was announced on Jan 23. This year, Jan 7 (today).

Companies generally do not move earnings timelines forward or accelerate disclosure unless they are comfortable with both results and outlook.

You do ZERO of this if things aren’t good. I’m expecting a solid Q4 and strong 2026 outlook.

https://t.co/WiD6wL2UDN