$NWBO

Other than the possibility that hedge funds and market makers somehow managed to corrupt thE @MHRAgovuk , I honestly do not see any reason why DCVax-L would not be approved. The data, safety profile, and unmet medical need all strongly support approval.

@wesstreeting@Siobhain_Mc@Keir_Starmer@zubirahmed

🧨 Short Circuit in Penny Stock Land: How $NWBO Built a Quiet Exit Ramp From the OTC Trap

Before anyone pins this story to a single day, the boundary gets drawn once and cleanly.

What is known is boring and checkable. NWBO has an existing London Stock Exchange line under ticker 0K95 with ISIN US66737P6007, and the LSE’s instrument page shows an issue date of 24 January 2018. On 19 January 2026, the UK’s new public offers and admissions regime takes effect, and the FCA’s final rules in PS25/9 raise the “further issuance” prospectus trigger for transferable securities already admitted to trading from 20% to 75%. NWBO’s SEC filings show two specific share-count snapshots: in its 10-Q, the company states that as of November 13, 2025, it had 1,540,682,082 common shares outstanding. In its DEF 14A, it states that as of the close of business on November 14, 2025, it had 1,528,682,082 common shares outstanding and 818,142 preferred shares outstanding. Shareholders approved increasing authorized common shares from 1.7 billion to 2.6 billion, and the company filed a Certificate of Amendment on December 30, 2025 to effect that increase. NWBO’s filings also set out the Series C conversion mechanics: 10,000,000 Series C shares authorized, and each Series C share convertible into 25 common shares once conditions are met—implying up to 250 million common-equivalent shares.

What is possible follows from those facts. NWBO now has more ways to compress the time between “plan” and “execution,” and that weakens the most profitable OTC short thesis—the thesis that lives on delays and visible countdowns.

There’s a financial weather system that forms over the OTC market. It isn’t about good companies versus bad companies. It’s about what happens when a stock trades in thin liquidity, where big institutional buyers rarely show up, where financing is survival, and where the people who do show up every day can learn to steer the tape.

Northwest Biotherapeutics has lived under that weather system for years. Some investors see a slow-motion breakthrough story. Others see a slow-motion implosion. But both camps often miss the real plot. On OTC, the most profitable trade is rarely “the science is fake.” It’s something simpler and more brutal.

It’s “they won’t finance cleanly in time.”

And if that’s the bet, the counter-bet isn’t an argument. It’s a clock hack.

This piece explains how NWBO can reduce the market’s ability to trade its deadlines—through lawful disclosure timing, regulatory tempo, institutional access, market plumbing, and one sleeper asset most traders ignored: the London Stock Exchange rail called 0K95.

⸻

🏚️ The OTC Isn’t a Lower Exchange. It’s a Different Machine.

The OTC market is often described like it’s just a cheaper, lower version of a major exchange. It isn’t. It’s a different machine.

A major exchange is a crowded city. Even when sentiment turns sour, there are still pedestrians. There’s depth. Big funds can enter and exit without detonating the price because enough participants absorb slow, steady flows. The market has mass.

OTC is a rural road at night. A few cars pass. Sometimes none. When one driver taps the brakes, the whole road reacts.

That difference isn’t cosmetic. It changes everything.

OTC tends to mean thinner displayed depth, wider spreads, fewer persistent buyers, and far less automatic demand from institutions and index flows. Thin marginal demand makes price easier to steer, and steerability is what turns a financing calendar into a trade.

That is the trap.

⸻

🧠 The Real Short Bet: Time, Not Truth.

Short selling is straightforward: borrow shares, sell them, hope to buy them back later lower, return them, keep the difference. The risk is unlimited on the upside, which is why successful shorts don’t just bet on direction. They bet on structure.

In OTC biotech, the durable bet isn’t “the drug won’t work.” It’s “the company won’t survive long enough for the drug to matter.”

That survival risk collapses into three variables:

Cash runway.

Financing timing.

Regulatory uncertainty.

So the thesis becomes temporal:

They can’t finance cleanly before the next deadline.

That’s why OTC stocks can behave in a way that drives long investors insane. Good news doesn’t re-rate the stock; it gets sold into. Because the market interprets good news as a financing window. If the company still looks like it needs money, a rally is treated as supply.

Not because the news was fake. Because the clock is still on the short seller’s side.

To beat a time trade, the company has to reduce the market’s ability to trade the countdown.

⸻

🧾 The Shares: The Math That Turns Time Into a Weapon — The One-Third Partner Slot

This is what the “Rule of Thirds” idea means in plain English. It isn’t a code. It’s a deal shape.

In biopharma, there is a common middle ground between “no partner” and “buy the whole company.” A large company takes a meaningful minority stake—large enough to align incentives and justify serious capital, small enough to avoid control. That ownership band often sits in the one-third neighborhood because it’s a natural balance point: big enough to matter, not big enough to become a takeover.

That’s the one-third partner slot.

Now the numbers that make this more than vibes:

• NWBO’s 10-Q states 1,540,682,082 common shares outstanding as of Nov 13, 2025.

• NWBO’s DEF 14A states 1,528,682,082 common shares outstanding as of the Nov 14, 2025 record date.

• Authorized common shares increased from 1.7B to 2.6B, effective via a Dec 30, 2025 Certificate of Amendment.

Authorized shares are not dilution. They are capacity—legal inventory.

Capacity matters because it reduces delay. Delay is the oxygen of the time-based short thesis.

Now add the instrument lane that sits quietly in filings: Series C Convertible Preferred. NWBO disclosures describe Series C shares being convertible into 25 common shares per Series C share, and the designation of 10,000,000 Series C shares implies up to 250 million common-equivalents.

Put the geometry together:

• a 900 million increase in authorized common capacity

• a preferred conversion lane of up to 250 million common-equivalents

• a common base around 1.53–1.54 billion outstanding at the time

This is why the one-third partner slot keeps showing up in serious thinking. The cap table now enables a large minority stake to be structured through a combination of preferred conversion capacity and common issuance headroom, without requiring an outright acquisition and without forcing the company into a slow, tradeable survival raise.

That doesn’t say a partner exists. It says the company is now built to take one.

⸻

🎛️ Path Control: How Thin Liquidity Turns Into a Price Narrative

In a deep market, repetition is expensive. In a thin market, small persistent pressure can shape the path.

The tape teaches this lesson through repetition: rallies stall early, key levels fail, quiet-day downdrafts land harder than they should, and bids vanish when volatility spikes. Buyers learn not to chase. Holders learn to sell sooner. Once that behavior takes hold, it becomes cheaper to keep it in place.

That’s why the company doesn’t merely need good news. It needs an execution architecture that interrupts what the market has learned—by collapsing the reaction window.

⸻

🏛️ Institutions: The Missing Demand Layer That Changes Everything

OTC suppresses institutional participation not because institutions are sentimental, but because they are constrained. Many funds can’t buy, won’t buy, or can’t size positions rationally in thin OTC names.

A second venue is not just a second price. It’s a second compliance reality.

Institutional capital doesn’t arrive because a company is interesting. It arrives because a company is financeable: clean enough, liquid enough, and executable enough to defend in committee.

That’s why the 0K95 rail matters even before it becomes liquid. It widens the battlefield. It creates a second place where price can print under a recognized exchange environment.

And it is thin today. That’s a description, not an insult. Some market data views show periods with no trades, while others show sporadic bursts of volume—either way, it is not a deep, continuously traded line. Thinness doesn’t negate it. Thinness is exactly why a credible external print can matter disproportionately if attention and demand arrive at the same time.

⸻

🕳️ Scenario Analysis: The Swapbook Amplifier

This section describes a general mechanism; there is no public data demonstrating a specific large swapbook in NWBO.

A total return swap is a contract that gives a fund economic exposure to a stock without owning it outright. The counterparty—usually a prime broker—hedges by buying or shorting the real shares into the market.

The world learned this in Archegos. The SEC’s complaint states Archegos used swaps “to limit the visibility” of its aggregate holdings and shifted from cash equity to synthetic exposure via swaps as it approached the 5% reporting threshold. Congressional research notes Archegos reportedly never filed a 13D despite large economic exposure via total return swaps.

The takeaway is structural: economic exposure can be larger than what is visible on a short-interest report, and dealer hedging can amplify moves when the tape flips.

In thin names, that amplification doesn’t glide. It stair-steps.

⸻

🤫 The Quiet Weapon: UK MAR Delayed Disclosure

Silence is not emptiness. In regulated markets, silence can be a tool.

UK MAR—the UK Market Abuse Regulation—is the UK’s market integrity and disclosure rulebook. It governs inside information: material nonpublic information that would likely move a stock if investors knew it.

UK MAR requires prompt disclosure in general. But it also recognizes that some processes are materially important but operationally incomplete. Disclose too early and negotiations can collapse, unfinished regulatory processes can be distorted, and the public can be misled into treating intermediate states as final.

So UK MAR includes a lawful mechanism for delayed disclosure under strict conditions:

Immediate disclosure would prejudice legitimate interests.

Delay would not be likely to mislead the public.

Confidentiality can be maintained.

In a time-based short regime, the effect is surgical. Delayed disclosure forces shorts to trade probabilities instead of timing.

Inside a lawful quiet window, a company can prepare contingent financing terms, align partners under nondisclosure agreements, stage documentation, and build execution capacity so the announcement is not a scramble.

That is how the reaction window collapses: preparation happens while the countdown is invisible, and execution happens when certainty arrives.

⸻

🌉 The Sleeper Rail in London: 0K95 and the January Turn

NWBO has a London Stock Exchange trading line under ticker 0K95, and the LSE’s own page lists an issue date of 24 January 2018 and ISIN US66737P6007.

The January shift is the real turn. The rail existed. What changes in January is the operating environment: the new UK public offers and admissions regime takes effect on 19 January 2026, replacing the inherited UK Prospectus Regulation with the FCA’s new rulebook-led framework.

Activation is not a press release. Activation is a market event. It happens when real order flow runs through the London line, when brokers and market makers quote it with intent, and when London becomes the first venue to establish a reference price during a window when the US tape is offline.

Once it’s used, path control becomes containment. Containment is more expensive.

⸻

🏦 Why SETSqx Matters: Auctions Can Jump Where Continuous Trading Drifts

The London Stock Exchange’s SETSqx model is built for less liquid securities. The LSE describes it as combining a periodic electronic auction book with quote-driven market making.

Continuous trading can bleed buying pressure gradually. Auctions can bunch demand and clear it at a single equilibrium price. When demand overwhelms supply at the clearing event, the price steps.

London doesn’t need to become the primary market. It only needs to print a credible reference price during a moment when demand is concentrated and supply is thin.

⸻

📜 POATRs and PS25/9: The January Rule Change That Cuts Time Taxes

January 2026 matters because the UK’s capital-markets framework changes in a real way. The new regime takes effect 19 January 2026, and the FCA’s policy statement PS25/9 spells out a key change: increasing the threshold at which a prospectus is required for a further issuance of transferable securities from 20% to 75% of those same securities already admitted to trading.

That does not guarantee a financing. It reduces the slow prospectus bottleneck that forces financings to telegraph themselves and creates a long pre-financing window that shorts can front-run.

Shorten the window and the time trade loses oxygen.

⸻

🧬 Big Pharma: The Nonlinear Catalyst that Makes the Setup Financeable

What follows is scenario analysis, not a description of any announced transaction.

Big Pharma doesn’t finance stories. Big Pharma finances systems.

A major partner can remove solvency fragility in one move. It can validate diligence. It can improve financing terms. It can change the pricing regime from survival to optionality.

And the minority-stake deal shape described earlier is not theoretical. In 2019, Gilead and Galapagos announced a collaboration that included warrants allowing Gilead to increase ownership up to 29.9%, alongside a 10-year standstill restricting Gilead from seeking to acquire Galapagos or increasing its stake beyond that level.

That’s the template: meaningful ownership without control, paired with deep strategic access.

⸻

🧹 The 8-K: Not the Hinge, the Housekeeping

The structural story is bigger than one filing. But the filing matters in the way boring things matter in capital markets: it trims an overhang.

NWBO’s January 15, 2026 Form 8-K states that the company entered into a settlement agreement regarding Delaware Court of Chancery litigation relating to 2020 option awards, and that under the terms of the settlement the company’s insurance carriers will pay $2.25 million to the company and 17% of the challenged 2020 options will be cancelled, among other terms.

That isn’t a London prerequisite. It is friction reduction.

⸻

⚙️ Settlement Discipline: The Strong Claim Without Fairy Tales

Settlement discipline is not a guaranteed squeeze button. The strong claim is simpler: settlement culture changes the cost curve.

For instance, stricter buy-in practices or tighter stock-loan terms can raise the ongoing cost of maintaining shorts—higher borrow rates, reduced availability, recalls, and less tolerance for settlement mess in the prime broker’s own book. None of this guarantees a squeeze. It raises cost and risk at the exact moment a time-based short thesis depends on cheap persistence.

⸻

🗓️ The Holiday Window: Asymmetry that Can Matter

The holiday window is a calendar asymmetry.

For example, when U.S. markets are closed for Martin Luther King Jr. Day while London is open, the U.S. tape can’t respond intraday, but London can still print. If a real catalyst coincides with that kind of window, first-mover price discovery can land in London before the U.S. market has a chance to shape the tape.

That asymmetry can break rhythm. In thin names, rhythm is half the trade.

⸻

⚠️ What Forces Shorts to Cover: Risk Systems, Not Theater

Short squeezes don’t happen because the internet gets angry. They happen because risk systems enforce limits.

Price rises.

Shorts take mark-to-market losses.

Margin requirements rise.

Some shorts cover.

Covering pushes price higher.

More shorts hit limits.

The loop reinforces.

⸻

🔚 The Master Synthesis: Tempo vs Time

The OTC regime makes time tradeable. Shorts bet on the clock.

NWBO’s escape architecture attacks that thesis by attacking its fuel:

• POATRs/PS25/9 reduces a key prospectus time-tax for further issuances from 20% to 75% in the relevant context, shrinking pre-financing windows.

• UK MAR delayed disclosure enables lawful preparation under strict conditions, so execution can be faster once certainty arrives.

• 0K95 provides a real London rail, even if thin today, operating under SETSqx auction mechanics that can print stepwise references.

• Share capacity + Series C terms make a serious strategic partner deal shape mechanically feasible.

• Big Pharma precedent shows the large minority-stake template is real, not exotic.

• Swaps explain how visible short interest can understate exposure and why reversals can amplify under dealer hedging.

• 8-K housekeeping trims friction and removes a governance overhang.

⚖️ Disclaimer: This is for informational and educational purposes only and is not investment advice.

$NWBO

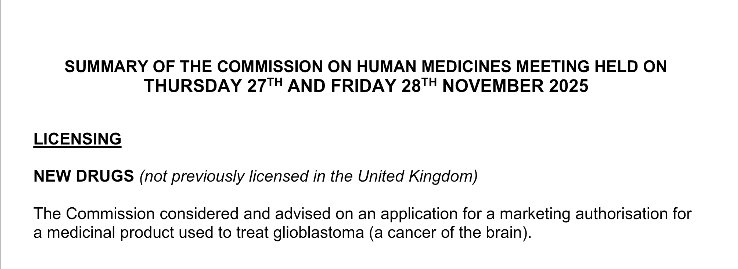

This is a good sign. While not 100% there is a lot of data showing that a regulatory decision usually happens within 3 months of a second CHM meeting.

https://t.co/YS38Sy9SIG

Thanks Lykiri

✅NWBO December 29, 2025 Annual Shareholder Meeting Recap

$NWBO

My notes below.

➡️Formal Portion of Meeting.

1⃣majority voted for reelection

2⃣majority voted in favor of ratification

3⃣majority voted in favor of increasing authorized shares

4⃣majority voted in favor of executive compensation

within 4 business days they will issue 8k with final voting results

➡️Questions submitted by shareholders (informal discussion with forward looking statements)

Four categories of questions: 1. MHRA process, other RA applications, 2. DCVax-Direct trials, Roswell trial plans, compassionate use, 3. Manufacturing related – Sawston, Pittsburgh, Flaskworks, 4. Business strategy – why raising authorized shares, partnering (?), succession planning

1⃣RA Applications & Commercial Readiness

MHRA – limited to what they can discuss. Enormous amounts of work put into DCVax-L application. Positive that MHRA is putting in so many resources to review the application. NWBO sees that as a positive. Going through cycles of RFIs. Don’t have a way to predict how much time it will take. NWBO isn’t the only one at 2+ years into application process. Attracted to the UK because of long positive history and supposed accelerated pathway. Want to submit to US and Canada as soon as the UK process is finished. Can’t do them at the same time b/c of manpower shortages and costs. Current spend is $12m/year in consultants.

Important developments in field moving in NWBO’s direction. In May the MHRA issued draft guidance giving permission for trials to use external controls. In early Fall they formalized this policy. Multiple regulators including the FDA recently came out with new and modernized policies embracing the use of real world data/evidence. NWBO has treated 100s of compassionate use patients.

Commercial Launch - Will proceed with reimbursement process as soon as they receive approval. Treatment of brain tumors is very concentrated. Vast majority of surgeries only happens in about 10 hospitals making it feasible to handle in house. C-Suite does not need to be completed prior to approval. Anticipating launching with 2 existing grade b suites.

Financing - Plan to focus on non-dilutive structures for funding. Royalty based or non-convertible debt based structures

2⃣DCVax-Direct & Roswell Park in-licensed technology

Manufacturing is ready to go.

Direct IND Package - CMC portion is written. Selected first phase 2 cancer, non brain cancer, lead institutions are onboard. Hesitating to move ahead because of costs.

Roswell/Pittsburgh trials temporary suspended enrollment as Dr. Kalinski moves offices. Ovarian cancer trial is first Kalinski/NWBO trial to proceed as company sponsored. Combo trial. Conditioning + dendritic cell + another component. Dendritic cells are polarized DC-1 cells. NWBO already did small pilot trial in ovarian with encouraging results. UPenn published those results.

Compassionate use program is ongoing. Expanding with additional doctors. In exploratory discussions with private hospital chain. Plan to offer compassionate use treatment to most types of solid tumor cancers. -L and -Direct planned to be offered for compassionate use.

3⃣Manufacturing

Working to maximize capacity of existing b suites. Hired additional staff. Streamlining procedures. Potential for two operating shifts.

Focus for future is c-suites. Going with simplified c-lab for cost reasons. Costs cut to less than half. Contractor has been selected, engaged and started prep work. Currently anticipate that physical construction get underway end of January and take 6 months. The simplified c-lab will have double the capacity of the two grade b labs.

Getting specialized equipment for c-labs can have 10-12 month lead time and be very costly. Advent found lightly used machines for about half the price of a new machine and already bought two of them.

Advent is a fully owned subsidiary of NWBO.

Pittsburgh, establishing a plant there. Pittsburgh will do Direct and L for compassionate use and clinical trials. Commercial production will take place at Sawston.

Flaskworks, the closed system, is designed as of 1+ year ago. Need to make a GMP version of it. Working on having Flaskworks prototype ready at same time simplified c-lab is complete.

4⃣Business Strategy

Why raise shares by 900m? Allow for flexibility. Anticipate negotiating significant financing, assuming positive approval decision. Need leverage in these negotiations. Burn rate was high last two years. It was low $50m. It is down significantly this year. If they kept up the higher burn rate it would still take years to burn those shares, but regardless, that isn’t the plan. They plan to focus on non-dilutive financing.

Partnering Always interesting in licensing or partnering for a region…latin America, the gulf, etc. Spent a lot of money to get patents throughout the world. $1.5m/year on patent costs. Already in exploratory discussion in regard to possibility of regional deal. Big pharma partnering? Always interested in that. Important avenue to that is combo trials, such as with checkpoint inhibitor drugs. Reaching stage where this might become possibility.

Expansion of management team and succession planning. Very high priority to expand management team. First wave is ready. They have senior managers already working 6months to 12 years as consultants. They will swap from consultants to full time if they get approval. Clinical medical, finance, and operations.

$nwbo @alphavestcap (Dr.Liau -Musella-Liau presentation -Q and A- 12/5/22) "when we give PD-1 inhibition neoadjuvant, before vaccination, you actually get a survival curve that’s better than giving PD-1 alone. But if you give the PD-1 inhibitor after dendritic cell vaccination, you can even boost that survival rate up to greater than 50%."

https://t.co/flNVNiRCdR

https://t.co/b3nwTZ0v42

https://t.co/PdJryzv8oo

After the filing of our $GNS lawsuit below, a message for our long-term shareholders:

(1) First, THANK YOU for your ongoing support through the darkest days (and for those who lost and left, know the Class Action seeks to recover your losses during the Class Period from April 2022 to May 2025 - all of them for everyone - and this period may very well extend).

(2) Second, this is just the FIRST MOVE. We are now going after the entire food chain, and we need your help:

We are putting on notice ANY and ALL BROKERS who have TAKEN AWAY THE BUY BUTTON on $GNS (while keeping the sell button). We consider this to be ILLEGAL MARKET MANIPULATION and demand they immediately reinstate the buy button and provide all our investors with a fair market.

We have had reports from our investors on the following brokers who have at some time or other taken away the buy button / forcing our $GNS investors to call in their buy orders while keeping the sell button, creating ongoing one-sided sell pressure of GNS shares:

Robinhood @RobinhoodApp

Schwab @CharlesSchwab

Fidelity @Fidelity

Vanguard @Vanguard_Group

Interactive Brokers @IBKR

If you are a client of one of these brokers (or others), could you please DROP A MESSAGE BELOW to let me know if - as of today - who your broker is and are you able to place a buy and sell order on $GNS with equal ease online? Or if you still have no buy button and find it much more difficult to buy vs sell your GNS shares?

I'm looking for both positive feedback for those brokers who are delivering a fair market, as well as negative feedback for those who are still providing an imbalanced (and obviously unfair) trading experience.

I've also copied in the X handles of the highlighted brokers above so the managers of those account have their own golden opportunity to drop a comment and give us good news you're responding to investors interests of a fair market.

I'll be reading every comment. And we will be taking IMMEDIATE action (ie. BEFORE THE END OF THIS WEEKEND) against any and all brokers where we receive feedback their buy buttons on $GNS are still off.

We will also give a thank you to each broker who has reconsidered / reinstated the buy button for $GNS.

Please give your honest feedback. Don't worry about your broker getting mad at you. There is ZERO reason for any broker to deliver an imbalanced trading experience on $GNS that leads to market manipulation, whatever their excuse. In fact, it's illegal.

Let's work together on this. Not just for you, or me, or Genius. Let's do this for a fair market - A clean, honest, transparent market. It's a long road. But together we can do this. Thank you!

📰Today's 8K

$NWBO

➡️10-31-25 Form 8K

https://t.co/j4BqlMyV9j

"On October 27, 2025, Northwest Biotherapeutics, Inc. (the “Company”) entered into a Commercial Loan Agreement and Note (collectively, the “Loan Agreement”) with Streeterville Capital, LLC (the “Holder”) in the amount of $5,505,000. The Loan Agreement has a maturity of 22 months. There are no repayments for the first 8 months. Repayments will begin June 26, 2026.

Following June 26, 2026, the Loan Agreement will be amortized in 14 equal monthly installments of principal at 110% of the pro rata amount, plus accrued interest. Interest on the Loan Agreement accrues at a rate of 8% per annum, and the Loan Agreement includes an original issue discount of ten percent. The Loan Agreement allows pre-payment at any time at the Company’s election. If the Company elects to pre-pay, the pre-payment would include a 10% charge. The Loan Agreement contains customary default provisions, including for potential acceleration.

The funds will be used for the Company’s ongoing business operations."

➡️5-2-24 Form 8K

This is $NWBO's prior loan with Streeterville Capital, LLC.

https://t.co/tm6r63jMhY

"On April 26, 2024, Northwest Biotherapeutics, Inc. (the “Company”) entered into a Commercial Loan Agreement and Note (collectively, the “Loan Agreement”) with Streeterville Capital, LLC (the “Holder”) in the amount of $11,005,000. The Loan Agreement has a maturity of 22 months. Repayments do not start until December 26, 2024.

Following December 26, 2024, the Loan Agreement will be amortized in 14 equal monthly installments of principal at 110% of the pro rata amount, plus accrued interest. Interest on the Loan Agreement accrues at a rate of 8% per annum, and the Loan Agreement includes an original issue discount of ten percent. The Loan Agreement allows pre-payment at any time at the Company’s election. If the Company elects to pre-pay, the pre-payment would include a 10% charge. The Loan Agreement contains customary default provisions, including for potential acceleration.

The funds will be used for the Company’s ongoing business operations, including beginning initial construction works for the first grade C lab in the Company’s Sawston, UK facility, ordering certain initial long lead-time equipment for the first grade C lab, and facility preparations for delivery of the initial GMP units of the Flaskworks system."

✅Thoughts

Exact same loan language.

This is encouraging if you're hoping for a positive DCVax-L approval decision. Why?

$NWBO faces an upcoming binary event that is highly likely to happen during the term of this loan. That binary event is the approval decision for DCVax-L. If the decision is 'yes approval' then $NWBO will have funds to pay back the loan. If the decision is 'no approval' then $NWBO could very possibly cease to exist as a company. In the later scenario, Streeterville does not get paid back. Thus, for Streeterville to give a loan to $NWBO at this point in time points to their impression that #DCVax-L is likely to receive a positive approval decision.

As a follow up, $NWBO has now closed the Advent acquisition

https://t.co/QtUl7QW55r

Since we're in Q4 we likely won't see Advent's Financials until the 10K.

As I stated prior, this oozes confidence that NWBO’s #DCVax-L will ultimately be approved as LP/Toucan would have had no incentive to hand over Advent for pennies prior to an approval decision.

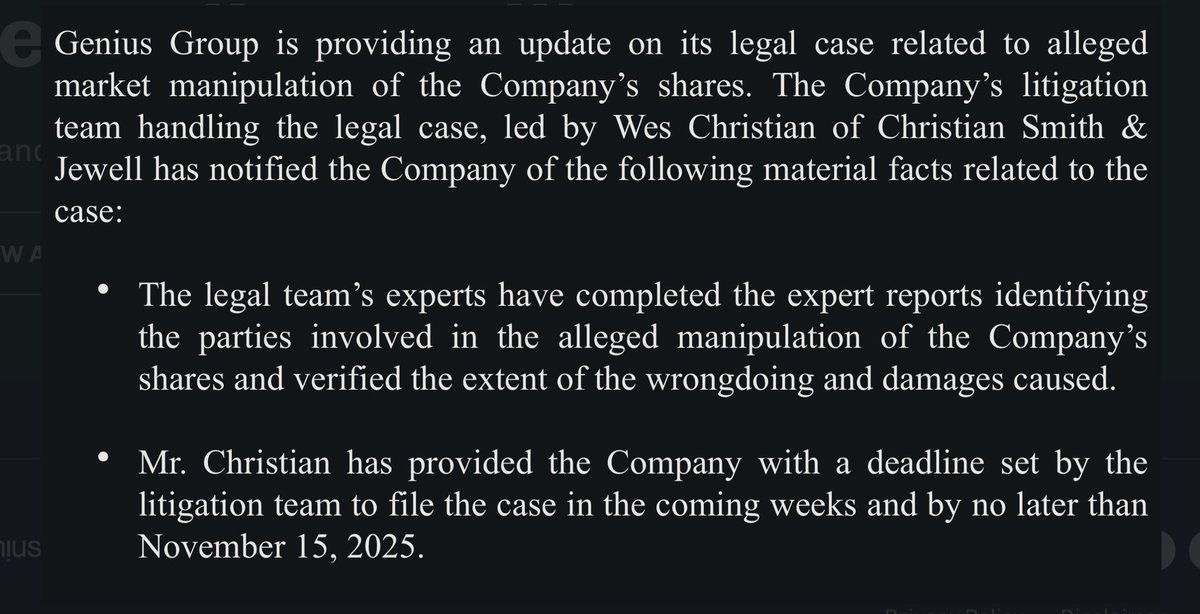

Latest $GNS news - Genius Group is providing an update on its legal case related to alleged market manipulation of the Company’s shares.

The Company’s litigation team handling the legal case, led by Wes Christian of Christian Smith & Jewell has notified the Company of the following material facts related to the case:

● The legal team’s experts have completed the expert reports identifying the parties involved in the alleged manipulation of the Company’s shares and verified the extent of the wrongdoing and damages caused.

● Mr. Christian has provided the Company with a deadline set by the litigation team to file the case in the coming weeks and by no later than November 15, 2025.

Genius Group will provide its next update with related to the case after the litigation team has filed the lawsuit.

#dcvax $nwbo #gbm

When 1 + 1 = 3

The Acquisition of Advent Bioservices Ltd. by NWBO Creates the World's First Vertically Integrated Dendritic Cell Vaccine Manufacturer

Yesterday Northwest Biotherapeutics (NWBO) announced their acquisition of Advent Bioservices Ltd. Advent was 100% owned by Linda Powers the CEO of NWBO who appears to have sold it to NWBO shareholders for a song. Though not detailing a specific price for the acquisition, the announcement of the deal states that it will be for £1.4 million ($1.9 million) and payment of the amount of net accounts payable (NAP) to Advent for work already performed. In the latest 10-Q for NWBO accounts payable to Advent totaled $8.0 million.

From the NWBO press release the company receives:

“all of Advent's fixed assets, including extensive cryostorage and other equipment purchased by Advent over the last several years. In addition, 19 million NWBio securities that were previously issued to Advent as payment for contract services will revert back to the Company (13.5 million shares and 5.5 million options). Certain intellectual property and other intangibles that Advent has acquired will also transfer to the Company.”

The shares alone are worth almost $2 million, and when you balance that against the $1.9 million payment to purchase Advent, it could be argued that Advent is paying Northwest Bio to acquire them. Yes, the acquisition does include NWBO also paying the outstanding NAP due Advent for past work, but that���s on NWBO books and Advent does have to be made whole for the work done. Still, that NAP is being rolled into the $1.9 million package (called “the consideration for the acquisition”), and payment can be paid in installments over two years, starting 90 days from the closure of the deal.

Putting the $1.9 million up against the returning shares and options looks to be a wash, leaving the NAP. After netting out the payables due Northwest, the remaining AP will likely be in the neighborhood of $5 million.

What Are the Benefits of NWBO Acquiring Advent Bioservices?

It Creates a Vertically Integrated Dendritic Cell Manufacturing Company

Advent Bioservices: A Good Manufacturing Practice (GMP) certified contract development and manufacturing organization (CDMO) that has proven ability and to make NWBO’s dendritic cell vaccines DCVax-L and DCVax-Direct. The former is used for cancer tumors that are resectable and the latter for ones that are inoperable. It has over 80 employees and is located in Sawston, UK, which is near Cambridge. Advent has licenses to import tumor samples and blood products needed to manufacture DCVax and to export the finished vaccines. It also has a lease on CL-2 lab and office space in South Cambridge.

Flaskworks: Acquired in 2020, this company developed and now manufacturers a closed system to automatically manufacture dendritic cell vaccines. With numerous worldwide patents, this first in-kind system allows for scalable and low-cost production. No other company possess this technology and that gives NWBO a tremendous lead over potential competition. The Flaskworks system enables onsite manufacturing in “C” suite cleanrooms which are far less expensive to build. Importantly, it provides NWBO the ability to quickly and cheaply scale production.

NWBO: Holds the intellectual property rights for dendritic cell vaccine technology. It holds over 70 patents for this technology in a number of countries throughout the world.

2. Remove Conflicts of Interest:

Linda Powers is CEO, CFO and Chair of the Board of NWBO and also owned 100% of Advent. NWBO relies 100% on Advent for the manufacturing of DCVax and other ancillary services. While NWBO has said that these services were provided at cost plus 15%, related party transactions are viewed with jaundiced eyes by many investors. Removing any potential conflict of interest and streamlining operations is good for NWBO shareholders.

3. NWBO Becomes a Revenue Generating Company

In the most recent public accounts for the year ending 2023, Advent posted revenue of £20,351,410 and net income £7,621,277. Assuming that the majority of this income was generated by DCVax production for the U.K. Specials Program (compassionate care) all this revenue will now accrues to NWBO. This will transform the company from a pre-revenue biotech to one with an income stream. With the consolidation and expansion of manufacturing capabilities, it is expected that by year-end NWBO will be able to produce enough DCVax to treat 1,500 patients per year. Assuming a cost for the treatment of $125,000, this means that if NWBO receives approval for DCVax-L, it has the potential to generate over $185 million in sales in 2026. This could prove to be on the low-side as additional production is added and an agreement with a U.S. manufacturing partner is reached.

4. Makes NWBO More Investable and Saleable

As noted, corporate structures where the listed company is fully dependent on a separate private company controlled by the CEO of the former is a major red flag for institutional investors. It is also a problem for a potential partner or buyer of NWBO. Selling Advent takes this issue off the table.

5. Lowers the Cost of Capital and Reduces Need For Continued Dilution

With $185 million or more in revenue NWBO, and especially if it has NICE approval for UK NHS reimbursement, the credit risk of the company will fall dramatically. This will allow Northwest to more easily borrow from the capital markets.

6. A Signal That MHRA Approval Will Likely Happen Soon

A currently cash strapped NWBO would not be able to afford to run Advent for any significant amount of time unless it expects to soon begin generating significant revenue. The only way that this happens is through an MHRA approval for DCVax-L.

7. Significant Cost Savings

Advent was charging NWBO cost + 15% for the work it performed. The consolidation of Advent will save NWBO millions per year, especially as production will ramp up on approval.

As mentioned above it, appears the acquisition cost will be in actuality zero, and the NAP is lessened by around $3 million, with the ability to pay that off in installments over a two-year period. As point of reference, Cognate Bioservices, which also had the ability to make DCVax-L and was once also controlled by Linda Powers, was sold to Charles River Labs for $860 million in 2021. Another comparison of the potential value of Advent can be made with Oxford Biomedica Plc which is a London listed CDMO with a market capitalization of almost $900 million. This unprofitable company trades at approximately 5 times sales. Applying this metric to Advent and assuming it had 2024 revenue of about $30 million yields a value of $150 million. If this comparison is right, then shareholders of NWBO have received and incredible windfall by acquiring Advent for a de minimis amount. Critics of the company argued that Ms. Powers was somehow using Advent to bilk NWBO. By effectively selling this valuable asset to NWBO for nothing she once again proves her critics wrong.

The NWBO takeover of Advent forms what looks to be a biotech powerhouse. With approval in the U.K. looming and approvals hopefully soon followed by other countries, NWBO’s potential looks soon to be realized. Adding manufacturing to create a vertically integrated company for next to nothing is a tremendous boon for NWBO shareholders. In this case, 1+1 really does equal 3.

https://t.co/z3ZotEcoMw