Ha Joon-Chang @the_hindu: "I am actually upset with people like Rajan Raghuram and, these days, Dani Rodrik, who mislead developing countries into believing that there is no future in manufacturing, and you can grow on the basis of services." https://t.co/GhHSQdGONQ

Ah yes, “global banks pulling cash out of Indonesia.” Terrifying. Except one of them left in 2023 and the other one is currently being fought over by three buyers. Some exodus.

Let’s be precise about what actually happened. Citi didn��t flee Prabowo. Citi sold its Indonesia consumer business to UOB and finished the migration in November 2023, part of a pre-planned retreat from consumer banking across 14 markets worldwide that was announced back in 2022, long before this administration existed. It walked away with about $1.1bn in regulatory capital benefit across the four ASEAN markets. The institutional business stayed.

HSBC is also the dane. It’s reviewing retail operations across Australia, Indonesia, Sri Lanka and more under a simplification plan announced October 2024, and is exploring a sale of the Indonesia retail unit, not bolting for the exit. DBS, SMFG and others are reportedly lining up for that book.

Funny kind of capital flight when there’s a bidding war for the asset. That same report notes foreign banks have been showing growing interest in Indonesia on the back of solid growth.

The real story is duller and more honest: profit repatriation timing. The corporate and institutional franchises stay put, which is the part that actually matters for capital markets. The remittance number and rupiah weakness are real. Pinning two pre-planned consumer exits on Prabowo is just reverse engineering a scary narrative from a soft currency chart.

Happy Monday to my fellow Indonesians who get bashed every Monday morning by Bloomberg 🤣

Salah satu analisa terbaik ttg arah policy ekonomi Indonesia ditulis oleh Anne Booth tahun 1998 yg sub- judulnya masih akurat sampe skr (abad 21) dan entah sampai kapan:

The Indonesian Economy in the Nineteenth and Twentieth Centuries: A History of Missed Opportunities

Selalu kehilangan kesempatan emas dan salah langkah sehingga kesusul.

Jadi WNI emang berat, warga Vietnam nggak bakal kuat. Kami aja

“If you haven't read hundreds of books, you are functionally illiterate, and you will be incompetent, because your personal experiences alone aren't broad enough to sustain you.”

— James N. Mattis

Baru baca jurnal peer-reviewed yg meneliti SOTO

Masuk dari tradisi kuliner Tionghoa lewat Semarang abad ke-19. Kala itu kolonial Belanda menganggap soto sebagai volksvoedsel (makanan jelata) yg ga higienis

Soto mana favoritmu dan kenapa? SOTO-in timeline yuk

This video from the Financial Times is just something else...

It's not as though Chinese officials kidnapped Western CEOs and CTOs during their clandestine visits to China, or strapped them to steel bolt-down chairs in secret warehouses just outside Beijing, before using modified cattleprods to force them to hand over their technological secrets.

Technological transfer to Chinese JV partners was simply part of the deal for profit-seeking Western corporations to be able to make direct investments - foreign direct investments - in China's burgeoning manufacturing ecosystem.

They did so of their own volition, for reasons of their own economic self-interest.

This is what the scriptwriters in the Communist Party like to refer to as a "win-win" situation.

This chart is one of the strongest pieces of evidence that China’s energy transition is already affecting the real economy, not just future plans.

The key takeaway is that 28 out of 31 Chinese provinces have seen thermal power utilization rates decline between 2023 and 2025. In simple terms, coal and gas plants are being used less frequently even though China continues to add electricity demand. That is an important distinction. Demand is still growing, but renewable generation is growing even faster.

Historically, rising electricity demand automatically translated into higher coal generation. That relationship is now breaking down. China is simultaneously building enormous amounts of solar, wind, hydro, nuclear, and battery capacity. As these resources enter the grid, they increasingly displace thermal generation during many hours of the day.

What is particularly striking is that the decline is broad-based. This is not confined to a few coastal provinces. From Guangxi and Qinghai to Guangdong and Inner Mongolia, utilization rates are falling across most of the country. That suggests a structural trend rather than a temporary economic slowdown.

For commodity investors, this has major implications. Many people still assume China’s power demand growth automatically means higher coal consumption. The data suggest otherwise. China may continue adding coal capacity for reliability and energy security, but the economic utilization of those assets is falling. Coal plants are increasingly becoming backup capacity rather than primary generation sources.

The second-order effect is even more important. Lower thermal utilization means weaker growth in coal demand, lower fuel imports, reduced exposure to volatile LNG markets, and a gradual decline in China’s energy intensity. Over time, this improves energy security while reducing marginal power costs.

For countries such as Indonesia and Australia, whose export sectors are heavily linked to thermal coal, this is a warning sign. China’s coal demand may not collapse, but the era when electricity growth automatically translated into ever-rising coal consumption appears to be ending.

The broader message is that the global energy transition is no longer theoretical. It is now visible in utilization data. China is still building coal plants, but increasingly it is building them as insurance. The growth engine of the power system is renewables.

Chart courtesy of @ember_energy

China is not trying to build a rival global order to the US, argues @patricia_m_kim.

“Beijing instead seeks global reach without entanglement, partnerships without binding obligations, and great-power status without the burdens of leadership.” https://t.co/Pb2xDIwz8J

Indonesia of all countries has found a way to exert leverage over Chinese firms.

Tsingshan, a Chinese private firm and world’s largest stainless steel producer, invested tens of billions of dollars in this Indonesian industrial park after Indonesia restricted raw nickel exports.

Ngomongin Buku Yah?! This 2 Beast of Papers Got Me Come Back Every Now and Then. Both more then Decade Old. Kraftwerk of Previous and Current Gandalf of Market Strategist at the World's top SellSide. Vintage Classics

this PhD student had 47 interviews and 4 offers before she was hired at OpenAI.

she practiced with her “notes on LLMs” and math and they’re a goldmine. super concise and organic and shared to everyone for free. you can use her notes or her topic list to study on your own.

The most interesting part of Danantara’s growing financial war chest is not the headline number itself. It is how that capital is being assembled.

At first glance, Danantara Investment Management (DIM) appears to have accumulated substantial firepower consisting of roughly US$7.4 billion of state equity, US$4.2 billion of domestic bond funding, US$10 billion of revolving credit facilities, and now an inaugural dual-tranche US dollar bond offering. By regional standards, that is a significant pool of capital capable of funding acquisitions, infrastructure projects, downstream investments, and strategic national initiatives.

However, investors should distinguish carefully between permanent capital and borrowed capital. Only around one-third of the reported funding comes from actual equity injections. The remainder consists of debt and credit facilities that ultimately need to be serviced, refinanced, and repaid. That distinction matters because the strongest sovereign wealth funds in the world were built primarily on accumulated savings and investment surpluses rather than increasing leverage.

The latest dollar bond issuance reinforces this point. Importantly, the reported 5.7% five-year and 6.3% ten-year yields are merely initial price guidance rather than final pricing. They represent what Danantara and its underwriting banks are offering investors, not necessarily where the bonds will ultimately clear once the order book is built.

The more important question is what level of compensation investors will ultimately demand. For reference, the US 10-year Treasury currently yields around 4.5%. If Danantara ultimately prices near the initial guidance, investors would be accepting a spread of roughly 180 basis points over the world’s benchmark risk-free rate to lend to a newly established institution with limited operating history, no long-term investment track record, and no explicit sovereign guarantee. That observation highlights why Danantara has attracted so much attention from investors, rating agencies, and policymakers.

Unlike the Indonesian government, Danantara is not a sovereign borrower. Unlike Singapore’s GIC or Abu Dhabi’s ADIA, it was not built from decades of accumulated fiscal surpluses and national savings. Yet the market appears willing to evaluate Danantara through a quasi-sovereign lens because of its strategic role and close relationship with the state.

This is why many investors increasingly view Danantara less as a traditional sovereign wealth fund and more as a quasi-fiscal vehicle operating alongside the government’s balance sheet.

When a state-owned investment platform raises domestic bonds, secures large revolving credit facilities, and accesses international debt markets, the debate naturally shifts from capital raising to liability ownership. Investors begin asking whether those obligations should be viewed as entirely separate from the sovereign or as contingent liabilities that could ultimately migrate back to the public balance sheet during periods of stress.

That is where the concept of shadow public debt emerges. Officially, Danantara’s liabilities belong to Danantara. In practice, however, markets may assume that government support would be forthcoming if the institution encountered serious financial difficulties. Whether that assumption is correct or not, it influences how investors price risk.

None of this means the strategy is inherently flawed. If Danantara successfully deploys capital into productive infrastructure, power generation, logistics, ports, digital infrastructure, industrial development, and other assets capable of generating durable cash flows above its cost of capital, leverage can become a powerful tool for accelerating economic growth and improving national competitiveness. 🧵

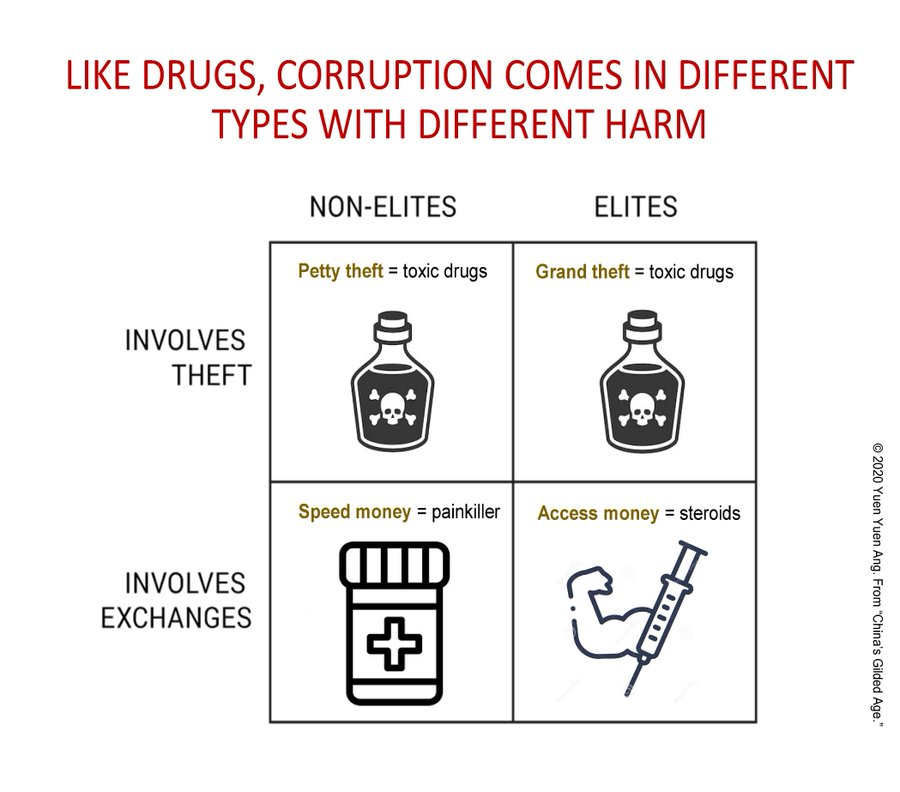

menurut Yuen Ang oligarki/korupsi bukan oli pembangunan tapi lebih seperti steroid di sport. bisa boost growth jangka pendek tapi merusak kesehatan ekonomi dan nggak sustainable.

dua kali saya posting pemikiran Yuen-Yuen Ang

https://t.co/eMU3AyDSW3

https://t.co/xMRaY82UM9