@paramonoww is 100% right. Reading his article, I realize: this is exactly what we in VC constantly talk about behind closed doors, but publicly everyone pretends the problem doesn't exist.

As an analyst at https://t.co/tLfvswQbFW, I review dozens of projects every month, and you know what?

Over the past couple of months, we've shifted to a classic venture approach for analyzing web3 projects:

▫️ Technology: how big is the market, what are you building, what problem are you solving

▫️ Business model: revenue, growth, unit economics

▫️ GTM: launch strategy, team, founder exits

▫️ Token (last)

And that's where it gets interesting 👨💻

About 80% of pitches end in rejection specifically on the token. Not because the team is weak or the product is bad.

But because the token simply isn't connected to the product at all. It exists in a parallel reality, glued on the side because "that's what you're supposed to do".

What's even worse: you talk to founders and can feel that they themselves don't understand why they need this token.

⚙️ You look at the deck: governance, staking, utility written beautifully on slides.

You ask for specifics - why would anyone need your token, what value does it bring? They can't give a clear answer. That's why equity is much more honest now.

When you enter as an LP or buy a company stake at any stage (Pre-seed, Seed), we know the founder will think about:

✅ Revenue

✅ User retention

✅ Building a business

Not about creating visual noise to successfully list the token.

📍The market will change when VCs and founders understand: a product can generate stable revenue without a token.

Build a quality business, and it will return more than the endless grind of projects with TGE dumps.

DeFi yield remains fragmented across protocols where users must track borrow rates, liquidity, and pegs simultaneously. @syntropia_ai internalizes that complexity into a single portfolio of strategies divided by risk tranche, allowing capital to allocate based on preference rather than constant monitoring.

The architecture removes the lending intermediary. Capital from the senior tranche is virtually lent to the junior tranche inside the system, creating internal leverage at a target 5x while keeping 100 % utilization.

Yield comes from an RFQ market making book that quotes intent flow on @NEARProtocol Intents and partner venues, with every fill hedged on Hyperliquid to stay near delta neutral. Returns therefore reflect captured spread, not token incentives.

Early numbers show the structure is attracting the right capital mix. Total value locked stands at $4.17 million, with the conservative senior tranche holding the majority at $2.3 million. Cumulative hedge volume has reached $200 million since the strategy went live in January.

That distribution indicates institutional and conservative liquidity providers are supplying the base while risk-tolerant users take the leveraged side.

The real test is durability

When external lending rates spike or liquidity fragments, internal tranching can absorb shocks that would otherwise force negative yields on leveraged positions. Whether this approach becomes standard infrastructure depends on how consistently the circuit breakers and scoped permissions protect capital through volatile periods.

The model replaces user-level complexity with manager-level execution, which is the shift required for larger pools to enter DeFi without building their own risk teams.

The figures accurately reflect the current institutional trend. The growth of the active lending portfolio to nineteen billion dollars proves the formation of a real blockchain based credit market rather than familiar speculation. The initiative to update HASH tokenomics is an absolutely logical and necessary step to synchronize protocol capitalization with its actual economic activity.

May Pulse Check Provenance Ecosystem

Six weeks ago we highlighted how the @provenancefdn architecture is reshaping the private credit sector. Today fresh data from Artemis confirms that institutional capital migration onchain is happening even faster than anticipated.

Core Growth Metrics

The network TVL experienced a massive (+92.0%) surge over the last 14 months hitting an absolute peak of $25.75B. In just the last month alone the network added $1.34B in total value.

Simultaneously the lending portfolio broke all historical records. Daily active lending loans reached $19.18B. We are seeing a clear trend acceleration of (+20.6%) over the past 4 months with $945M added to the loan balance in May alone.

This capital growth is matched by user adoption as the network now hosts over 77K participants generating upwards of $316K in monthly chain fees.

Strategic Roadmap

These figures represent real economic activity rather than speculative volume. To sustain this momentum the project is focused on executing a three step plan

1. Reworking HASH tokenomics to capture economic value more efficiently

2. Creating deeper utility mechanisms for asset holders 3. Actively attracting third party participation and developers to the platform

Such fundamental dynamics prove that the real integration of traditional finance and blockchain has already begun. We continue to closely monitor the progress of infrastructure solutions in this segment.

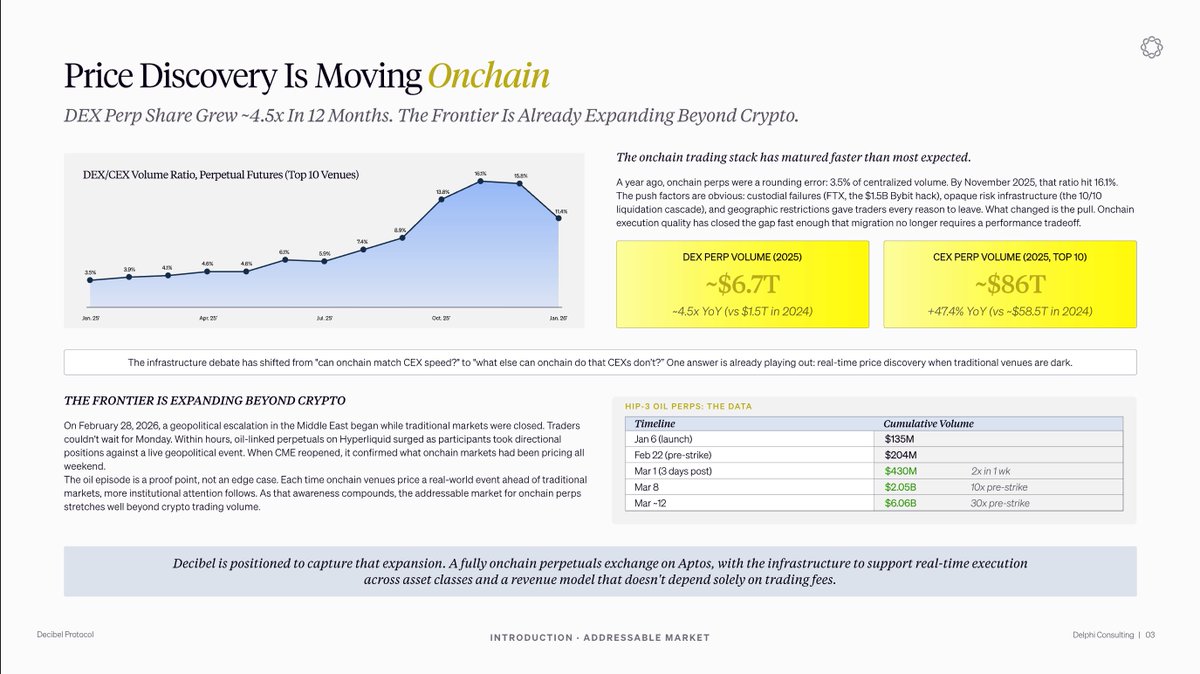

Onchain perps are matching CEX execution on event flows and beginning to pull measurable share.

> @DecibelTrade average daily volume: $142M in November, +340% from Q3

> Median trade latency: 180ms during volatility spikes

> Slippage on $1M BTC perp: 4.2bps vs 3.8bps on top CEX

> Share of onchain perp volume: 12% and rising

Fully onchain venues now compete on the metrics that matter for tactical flows. This is what share migration looks like.

The @HyperliquidX architecture systematically absorbs adjacent verticals through the zero-cost conversion of its existing active trader base.

Sustaining this expansion rate over a six-month horizon mathematically guarantees the protocol will capture the dominant share of prediction markets without incurring external capital acquisition costs.

We're excited to announce our collaboration with @raikucom on our first-ever Solana Revenue Report, covering Q1 2026.

• Protocol-Level Revenue

• Infrastructure Revenue: MEV, Jito, Invisible Layer

• Who Earned the Most in Q1

• Established Players & New Ones

Enjoy the read!

Thanks to the teams at @raikucom and @hazeflow_xyz

for publishing the Q1 2026 Solana Revenue Report.

The core insight of the research lies not in peak fees but in a fundamental shift in user demographics. February marked the first time the blockchain recorded systemic infrastructure payments originating directly from autonomous algorithms.

Machines are now paying customers:

Providers Helius and QuickNode integrated programmatic API billing directly in USDC. Algorithms currently purchase their own computational capacity.

A new liquidity model:

Protocols DFlow and Claw Credit opened credit lines specifically for AI. Simultaneously BankrBot manages Raydium pools with complete autonomy.

The optimal execution environment:

Algorithms require high transaction frequency and near zero costs. Block finality under 50 milliseconds makes this architecture the default layer for machine micropayments.

Blockchain revenues have historically relied on retail emotion and speculative cycles. The integration of autonomous agents breaks this paradigm. Machines establish a persistent base load on the network.

They do not panic and they completely ignore price trends. For smart capital the scaling of this sector represents the emergence of the first truly predictable revenue stream in Web3.

Chasing the highest APY is a fool’s errand for institutional treasuries.

Today, DAOs and corporate funds are manually hopping between @ethereum , @base , and @avax . They burn margin on gas, slippage, and bridge fees just to squeeze out an extra 20 basis points. But once you factor in the operational overhead and the exponential smart contract risk of managing positions across four networks, that 3.89% on @aave quickly evaporates.

The answer isn’t bloating your internal treasury team. That’s not how TradFi scales, and it’s not what Web3 should be doing either.

Grove skips the noise via algorithmic capital routing. The protocol doesn’t compete for "degen" yields. At 3.65%, it establishes a definitive, risk-adjusted benchmark. By batching transactions, dynamically balancing tokenized RWAs with decentralized lending pools, and removing cross-chain friction, @grovedotfinance collapses fragmented liquidity into a single, unified yield curve.

Composability risk is the industry’s biggest hurdle, but Grove solves it through network-isolated vaults and asynchronous circuit breakers. A blowout on Avalanche won’t drain the vaults on Base.

With $8.3B in TVL generating over $72M in annualized fees, the value accrual is undeniable. Revenue flows directly back into the ecosystem via Real Yield and liquidity bribes, turning the token into a cash-generating asset rather than just a governance proxy.

By next year, I expect automated RWA-to-DeFi routing to be the standard primitive for every major on-chain entity. This is how crypto balance sheets finally mature.

Did anyone actually track @grovedotfinance and understand its core architecture?

The protocol launched in June 2025 as a capital allocation layer within the Sky (formerly MakerDAO) ecosystem.

The platform automatically deploys capital into tokenized RWA assets, Aave lending, Morpho vaults, and Curve LP positions.

This infrastructure operates across Ethereum, Base, Avalanche, and Plume.

Let us review the actual metrics:

• Grove Savings TVL has reached $5.7 billion.

• Core protocol TVL stands at $2.67 billion.

• Annualized fees exceed $72.6 million.

• The $SKY Savings Rate offers a 3.65% APY. This rate competes tightly with $AAVE at 3.89% and $MORPHO Prime at 3.75%.

The fundamental value of Grove lies in algorithmic capital routing. The protocol bridges fragmented liquidity across multiple networks and forms a unified yield curve for stablecoins.

Dynamic balancing between tokenized RWAs and lending pools establishes the baseline risk free rate for the sector.

The project operates as a comprehensive treasury primitive. It automates corporate asset management and drastically cuts portfolio rebalancing costs.

When a chain @solana actively supports its projects, it creates a powerful symbiosis: the growth in quality of individual applications directly boosts the overall revenue and user metrics of the entire ecosystem.

We have moved from "infrastructure for infrastructure’s sake" to a phase where the success of a network is measured by the success of the products launched within it.

This shift evidenced by the surge to 29.9K weekly deployers and 50.5K new contracts is the leading indicator that promises a major wave of high-impact application projects in the near future.

AI is shifting from the discovery stage to the ROI stage, and the market now demands infrastructure over hype.

Key points:

1) Early AI was focused on testing capabilities and building broad applications.

2) The focus is now shifting toward sustainable economics and solving real-world problems.

3) Vertical AI solutions in logistics or fintech are becoming drivers of margin expansion.

4) The next decade will be built by infrastructure solutions, not standalone features.

Capital is gradually flowing toward cash-flow-generating, industry-specific products.

Great read below.

Y Combinator’s RFS for Summer 2026 confirms a market shift we’ve been acting on at Funders VC : the AI industry is moving from the "discovery" phase to the "ROI" phase.

The first wave of LLM adoption naturally focused on testing capabilities and accessible applications. Now, the market demands foundational infrastructure and sustainable unit economics. The hype cycle is over; the execution cycle has begun.

At @FundersVC , we aren’t looking for broad horizontal platforms. Our current thesis is built around "real solutions for real problems." We are hunting for AI-infra and Vertical AI deeply embedded in narrow industries such as logistics, construction, manufacturing, QA or B2B fintech.

We back founders who are building the backbone of the next decade by:

• Delivering margin expansion

• Solving complex legacy enterprise workflows rather than building superficial features.

• Demonstrating clear paths to revenue and capital-efficient growth from day one.

Every VC makes a bet on what the world will look like in 10 years. Our bet is on founders turning technological shifts into scalable, cash-generating businesses.

Great observation. To build on this, the most interesting part lies in the math of their capital and their long-term hedging strategy.

Tether is currently operating on a model that no classic VC fund can replicate. By leveraging zero-cost liabilities (users don't earn yield for holding solana:Es9vMFrzaCERmJfrF4H2FYD4KCoNkY11McCe8BenwNYB ) and massive cash flows from US Treasuries, they are funding complex, capital-intensive deep tech with essentially free money.

Their pivot away from pure crypto infrastructure toward brain-computer interfaces, robotics, and alternative communication networks looks like a highly pragmatic macro hedge. The core stablecoin business will inevitably hit a ceiling either due to strict institutional regulation or competition from banking products and CBDCs.

By acquiring physical hardware, media platforms, and independent data transmission channels, Tether is preemptively building an autonomous conglomerate. If the crypto market stagnates or gets squeezed by compliance, they will still hold the foundational infrastructure of the next technological cycle on their balance sheet.

We are essentially witnessing the evolution from a token issuer to a Berkshire Hathaway-style tech holding company.

A closer look at Tether’s venture arm shows a portfolio moving far beyond standard crypto infrastructure.

Stakes in Blackrock Neurotech, Neura Robotics, and Generative Bionics indicate a clear focus on deep tech and human-computer interfaces.

Meanwhile, investments in platforms like Rumble and Holepunch show an active interest in alternative media and P2P communication networks.

This isn't just basic diversification. Tether is essentially using its massive financial float to buy into the physical and digital hardware of the next decade.

The market still treats onchain privacy as a regulatory gray area, but the institutional reality tells a different story.

A fully transparent public ledger is structurally incompatible with enterprise adoption. No business can operate when its supply chain, margins, and vendor payments are broadcasted to competitors in real time.

What this architecture demonstrates is a fundamental repricing of trust. Legacy finance relies on heavy identity verification (KYC) to mitigate default risk. It is a slow, expensive, and data-heavy patch for an inherently inefficient system. By replacing identity with collateralized mathematics, the system shifts from trust-based settlement to deterministic settlement.

Bottom line: Privacy is not a consumer luxury; it is a strict institutional mandate. Collateral-as-identity is the ultimate architectural moat that will finally bridge traditional commerce with decentralized rails.

The traditional banking premium is structurally obsolete.

Fighting for paid deposits yields diminishing returns when a parallel entity captures global liquidity for free and relentlessly compounds the spread into hard assets and proprietary networks.

For capital allocators, the ultimate moat is no longer regulatory licensing. It is zero-cost liabilities paired with vertically integrated infrastructure. We are adjusting our macro thesis accordingly.

The Tether model: From Stablecoin to permanent capital

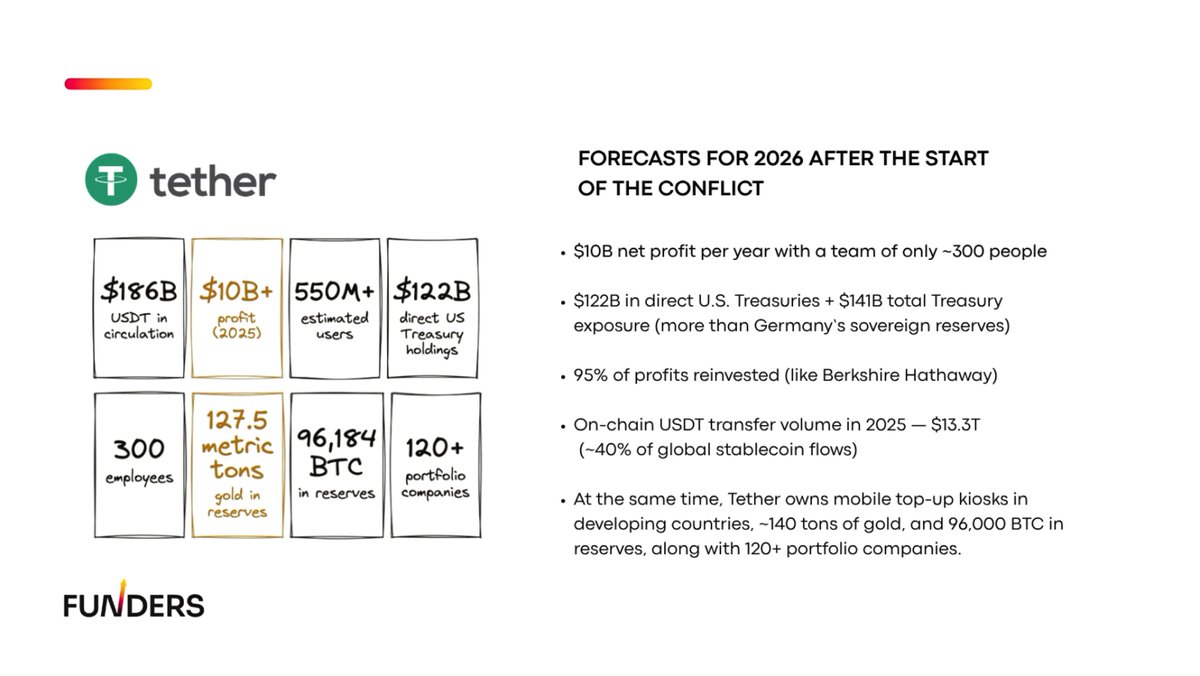

Tether generates roughly $10 billion in annual net profit with a team of around 300 people. Its operational leverage is driven by exposure to $141 billion in U.S. Treasuries. The liability base carries effectively zero cost.

95% of profits are deployed directly into a portfolio of hard assets. This includes 96,184 bitcoin:native, 140 tons of physical gold, bitcoin mining infrastructure, and stakes in more than 120 private companies. In 2025, solana:Es9vMFrzaCERmJfrF4H2FYD4KCoNkY11McCe8BenwNYB on-chain transfer volume reached $13.3 trillion, accounting for roughly 40% of global stablecoin flows.

Structurally, @tether occupies a position with no real equivalent in traditional finance. Banks pay for deposits. Insurance companies absorb underwriting risk.

Tether acquires liquidity for free, allocates it into Treasuries yielding 5%, and reinvests the spread into assets with effectively unlimited duration. The cost of liabilities is fixed at zero, while the value of assets compounds over time.

The next layer is control consolidation. Direct access to 40% of global stablecoin flows positions Tether as an operator of settlement infrastructure. The launch of its own blockchain, @Plasma, with zero fees and restrictions on speculative assets, removes dependency on external networks. Mining farms in Uruguay, Paraguay, and El Salvador add a physical base for asset generation.

The regulatory track forms the second pillar. In January 2026, ethereum:0x07041776f5007aca2a54844f50503a18a72a8b68 was launched under the GENIUS Act framework. The issuer is Anchorage Digital Bank, reserve custodian is Cantor Fitzgerald, and the CEO is Bo Hines, former head of the White House Crypto Council. Separate perimeter, separate product, separate audience. A sanctioned access layer running in parallel to the core structure.

Bottom line: the market is still debating reserve transparency while the structure already operates like a vertically integrated holding company. Short-term float is being arbitraged into long-term control over settlement infrastructure, energy production, and hard assets.

$DUST (dedust) has 64% of TON's DEX volume, routes 79% of all bot trading via dtrade, and runs sTONks.pump which is TON's version of https://t.co/31ZmEI0BSv. estimated $23m annualized fee revenue on a $3m market cap. that's a 0.13x price to fees ratio. uniswap trades at 3.5x. pancakeswap at 2.8x. the token accrual mechanism is still unclear which is why the market prices it like a throwaway. if they announce a fee switch or buyback, this re-rates 20-40x overnight. own the casino not the chips

A recent report by @galaxyhq exposes a core vulnerability in algorithmic finance.

The market has long known that underlying blockchain infrastructure was built exclusively for humans. The value of this research lies elsewhere.

Analysts have identified the exact structural bottlenecks currently preventing the transition to autonomous capital management.

Here are 4 barriers to machine autonomy:

1. The Semantic

Barrier Blockchains guarantee code execution, not economic meaning. Without interfaces, algorithms are incapable of interpreting raw smart contract data.

2. Identity Deficit

Token authenticity is established socially. Without institutional registries, machines are forced to guess the correct asset among hundreds of clones, risking capital.

3. Data Fragmentation

The absence of shared standards requires multiple disjointed queries to evaluate the market. This carries critical latency risks during high volatility.

4. The Control Problem

Eliminating the manual signature nullifies risk management. Sending a transaction is easy, but programmatically verifying its outcome in an adversarial environment is nearly impossible.

The infrastructure landscape has officially split into two categories: interfaces for humans and middleware for machines. The era of decentralized finance built around convenient design has reached its limit.

The next major venture capital rotation will fund the semantic layers necessary for algorithms to manage liquidity autonomously.

Source: https://t.co/tUVJxfoNdA