🚨 Tax specialists have uncovered a sleeper clause in the federal budget bill designed to quietly inflate investor tax bills — and it's a rort. The bill which passed the lower house yesterday, introduces a mandatory "loss-ordering" mechanism for the first time in Australian tax history. Instead of cherry-picking how losses offset gains, investors will now be forced to burn through their oldest gains first — stripping away the 50% CGT discount and leaving newer gains fully exposed to the punishing new cost-base indexation regime from July 1, 2027.

Say you bought shares in 2018 and again in 2024. You sell both at a gain, but you also have losses to offset. Previously, you'd apply those losses to your 2018 gains first — which already qualify for the 50% CGT discount, meaning less of them are taxable anyway. Under the new rules, you're forced to do exactly that — exhausting the discounted gains first and leaving your 2024 gains fully exposed to the new, harsher indexation rules.

You end up paying more. This isn't an oversight. It's a deliberate revenue grab buried in fine print

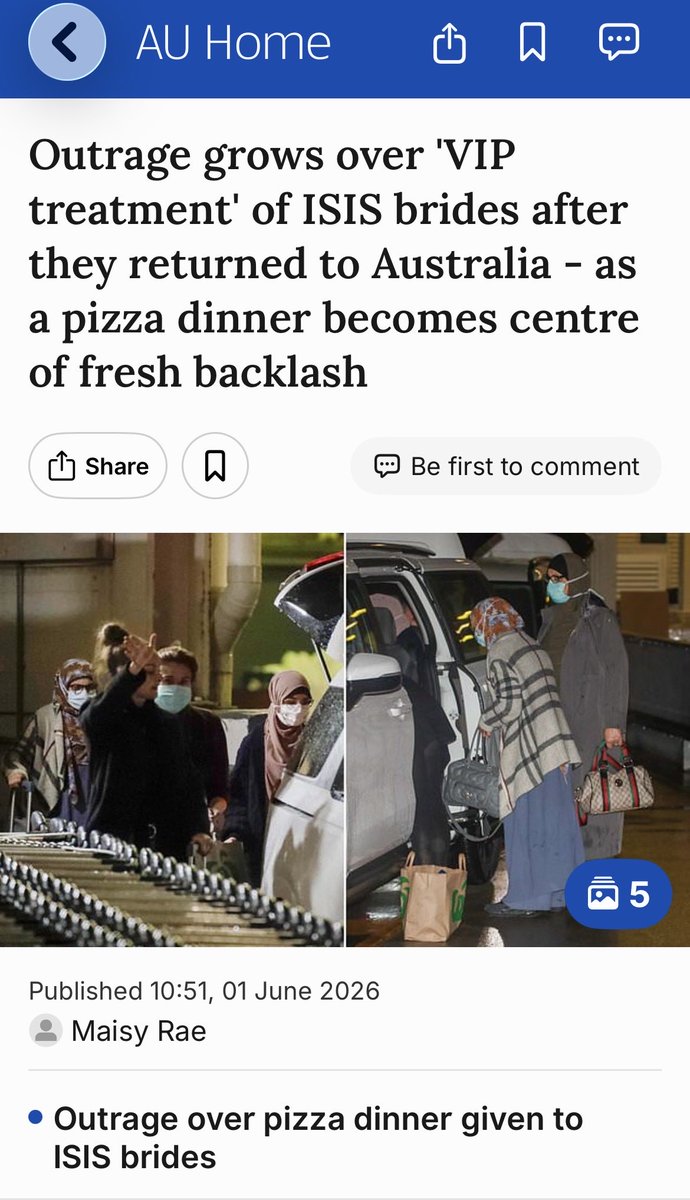

The NSW and Albanese governments have been urged to come clean over who paid for a pizza dinner for the ISIS brides and their children after they returned to Sydney, as outrage grows over their 'VIP treatment'.

The cohort of four women and six children arrived at Sydney Airport on May 26 and were greeted by officials from the NSW Department of Communities and Justice.

Officials are believed to have conducted an almost three-hour health assessment on the group before police assisted them to a line of waiting cars.

AFP officers were then seen shielding the women and children from cameras by forming a line in front of the vehicles.

Media later spotted the women at a nearby hotel, where pizza boxes were delivered to reception as riot police stood guard outside.

A federal government source told the Daily Telegraph it was 'ridiculous' the group had received 'VIP treatment' on their arrival.

'It sets a precedent that you can willingly travel to and come back with a red carpet rolled out for you from a side exit,' they said.

Speaking on claims the ISIS-linked cohort were fed pizza, a police source said they 'got fed and we didn't'.

Pressure is mounting for the NSW and federal governments to disclose who paid for the pizza dinner.

Federal Opposition home affairs spokesman Jonno Duniam demanded answers from Prime Minister Anthony Albanese and his government.

'The federal government still tries to argue that it has done nothing to help these women and children,' he said.

'As if passports, consular assistance, identity checks, transport, police arrangements, health checks, accommodation and other special privileges – including upon their arrival in Australia – have somehow all materialised by magic.

From a reader...

Dear Sir

Under current legislation, all trusts (not just discretionary trusts) are taxed on accumulated income to which no beneficiary is presently entitled. Such income tax is assessed to the trustee under section 99A of the Income Tax Assessment Act, 1936 (“the Act”). The tax rate assessed to the trustee is at the highest marginal rate, plus Medicare. That imposition amounts to 47% of the accumulated income. The Commissioner retains a discretion to assess such income under section 99 of the Act, (which applies personal rates of taxation) but that discretion is exercised sparingly and only in limited cases, such as deceased estates and bankruptcies.

Again, under current legislation, a share of trust income – to which a minor or a non-resident beneficiary is presently entitled to – is assessed to the trustee under section 98 of the Act and assessed again to the beneficiary with a full credit given to the beneficiary for the tax assessed to the trustee.

The 2026 Federal Budget proposals change the concept of the taxation of beneficiaries of trust estates that has applied since the Federal Government introduced income tax. That is done by treating the trustee as a separate taxpayer on income to which beneficiaries of a discretionary trust are presently entitled to. Now, a beneficiary is said to be presently entitled only on the after-tax net income of a discretionary trust estate. Any credit for tax paid by the trustee, under these new proposals:

is not fully credited to the beneficiary if it produces a cash tax refund to the beneficiary, and

in the case of a corporate beneficiary the tax paid by the trustee is not credited at all.

With all due respect to Treasury officials and the Treasurer, who devised this new arrangement, there is a complete misconception on who is being assessed on income to which a beneficiary is presently entitled to. Unlike companies, where the taxable income of a company is legally and beneficially derived by the company, in the case of trusts, including discretionary trusts, any net income of a trust estate to which a beneficiary is presently entitled to is income of the beneficiary, not the trustee. By taxing the trustee on income to which the trustee is not beneficially entitled to, and not passing the tax paid by the trustee to the beneficiary who is entitled to that income from the trust estate is not a tax, but – in my opinion – an illegal penal confiscation. Allow me to explain:

The Core Problem:

When a trustee is assessed on income to which a beneficiary is already beneficially entitled, without any credit (or a full credit) being passed to the beneficiary, two (2) serious legal problems arise with regard to the Constitutional validity of the legislation purporting to assess:

1. Section 51(ii) — Is it a Valid "Tax" or a Penalty/Forfeiture?

The High Court in Matthews v Chicory Marketing Board (Vic) (1938) 60 CLR 263 confirmed that a tax is "a compulsory exaction of money by a public authority for public purposes, enforceable by law, and... not a payment for services rendered." A "tax" – in the constitutional sense – requires it to be imposed for revenue-raising purposes, not as a punishment or confiscation. See Woodhams v Deputy Commissioner of Taxation of the Commonwealth of Australia (1997) VSC 59 on what constitutes a penalty (and not a tax).

The key issue is whether imposing the full tax burden on a trustee — without any (full) credit mechanism for the beneficial owner — crosses the line from taxation into something more like a forfeiture or a penalty. In these circumstances, I submit the trustee’s right to exoneration and indemnity are in jeopardy and a beneficiary would be entitled to restrain the trustee from using trust funds to discharge a personal obligation, that is not a fiduciary obligation, even if the obligation was imposed by flawed legislation.

2. Section 51(xxxi) — Acquisition on Just Terms

If the Commonwealth imposes a liability on a trustee with respect to property or income beneficially owned by another, and the trustee cannot recover that tax from the trust estate or beneficiary through the tax legislation itself or under the terms of the relevant trust deed, this could constitute an acquisition of property (money) from the trustee without just terms, contrary to s 51(xxxi) of the Commonwealth Constitution.

The High Court has ruled in Minister of State for the Army v Dalziel (1944) 68 CLR 261 and most recently in Government of the Russian Federation v Commonwealth of Australia [2025] HCA 44 that section 51(xxxi) of the Constitution will protect a party whose property is assumed by the Commonwealth without compensation. The term “property” is widely characterised to give the affected party full constitutional protection.

In my view, the proposed arrangements don’t fall into the unintended consequences camp, as is often claimed when some controversy is later discovered after a proper and considered analysis. In this case, the proposed arrangements are fundamental misconceptions, that fail to recognise basic constitutional protections.

North-west Queensland farmers are still reeling after devastating floods wiped out tens of thousands of cattle.

The Queensland Government stepped up and proposed a $94 million jointly funded package to help these hard-working families restock their herds and get back on their feet.

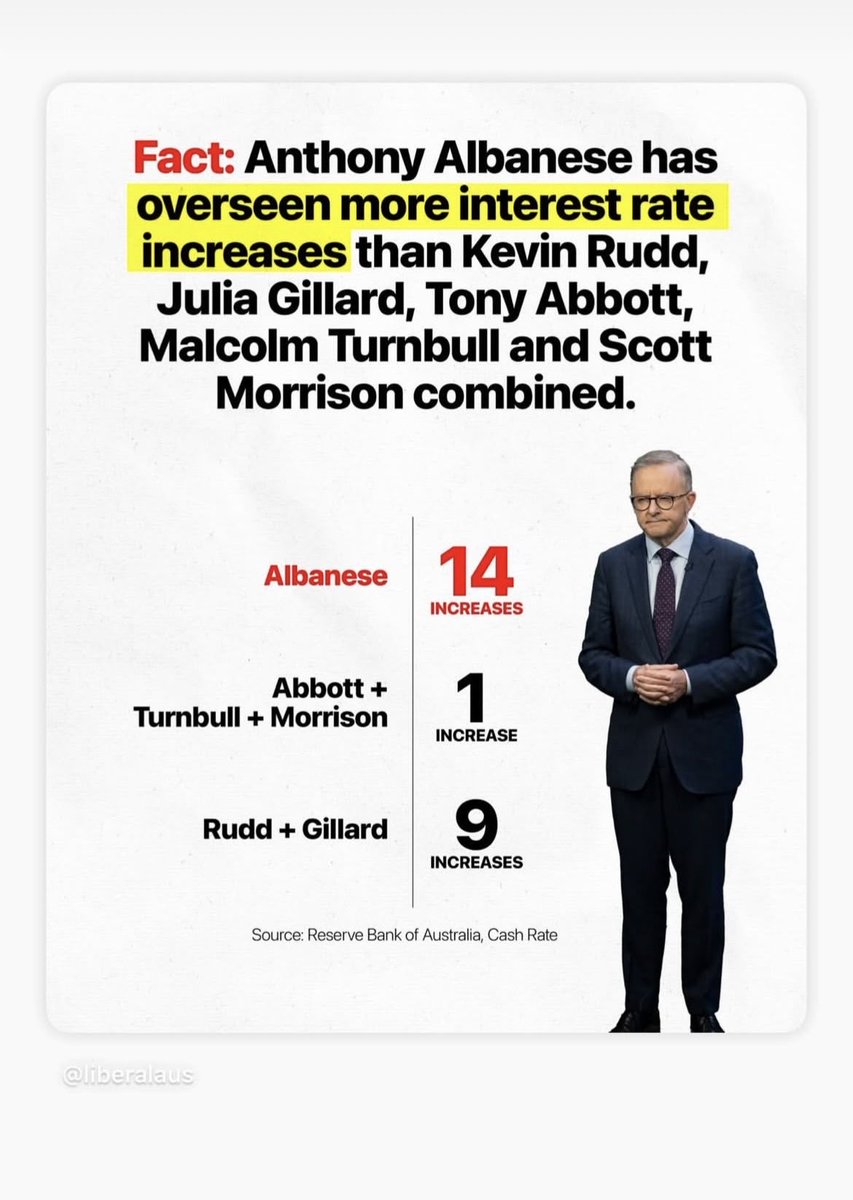

Prime Minister Anthony Albanese’s response?

“No. You pay for it yourself.”

While Aussie farmers — the backbone who feed our nation — battle to survive one of the worst disasters in years, Labor washes its hands and walks away.

This is absolutely disgraceful.

These are the same farmers keeping our supermarkets stocked and our rural communities alive. When they need real support after a natural disaster, Albanese says “not our problem.”

Enough of this out-of-touch neglect!

Farmers First. Australians First.

Are you furious at Albanese for abandoning our farmers? Drop a massive YES or 🔥 below if you stand with Aussie farmers 👇

#AustraliansFirst #FarmersFirst #FloodedFarmers #AlbaneseFailed #QLDFloods #SupportOurFarmers #LaborNeglect #RuralAustralia #PutAussiesFirst #AustraliaFirst #WakeUpAustralia #OneNationRising #FarmersMatter

@Tedthekelpie@hasselljpb@NationalFarmers I don't get it. They want us to take a risk in business. Tax us to set it up with stamp duty, tax along the way PAYG, income tax etc, then when we get out CGT up to 47%. Why would you do anything? We need Tommy Robinson.

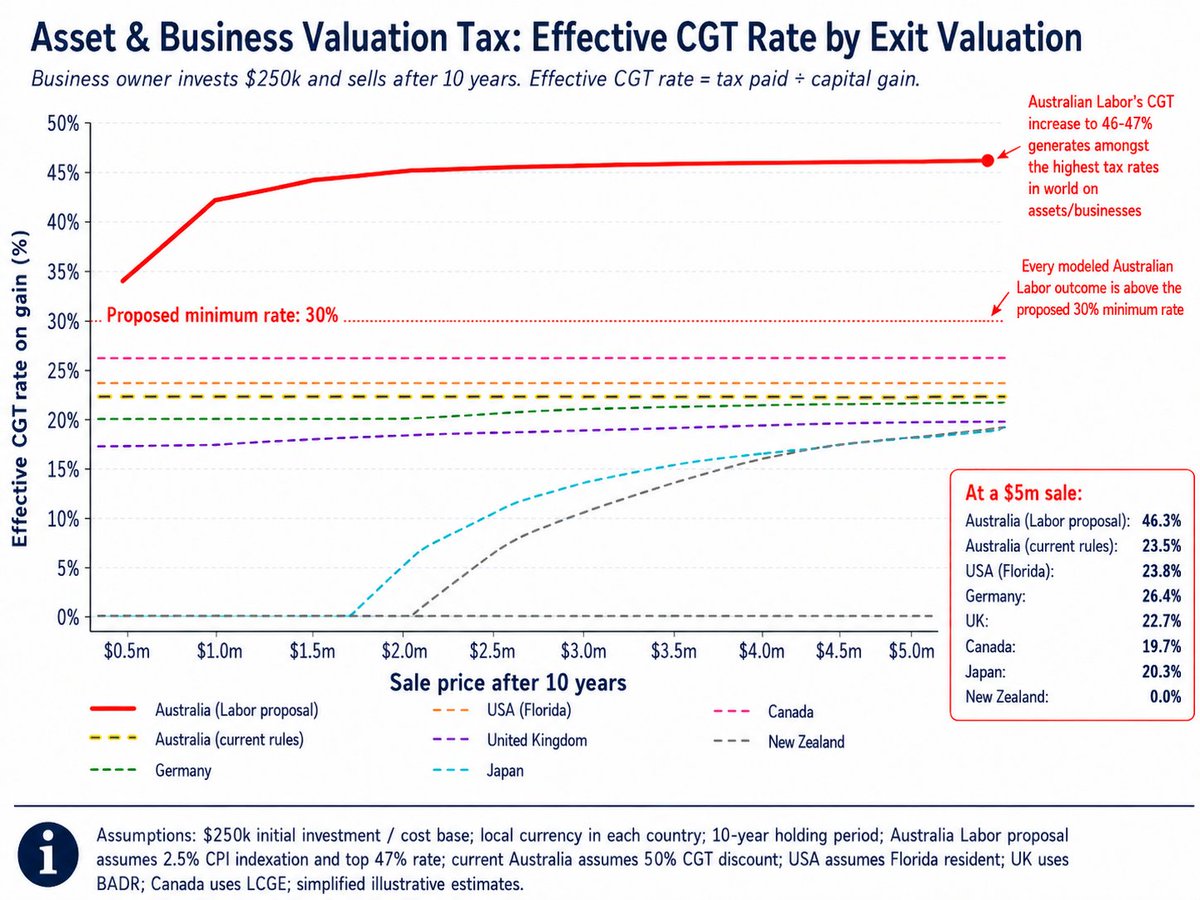

The chart below shows the effective capital gains tax rate facing a business owner who invests $250,000 upfront, holds for 10 years, and then exits at different valuations. The result is striking: under Labor’s proposed CGT changes, Australian founders and investors would face an effective tax rate of up to 46% — roughly double the burden faced in most comparable markets, including the US, UK, Canada, Germany, Japan and New Zealand. And this is not just a founder problem. The same logic applies across all small, medium and large businesses, and any asset, including listed equities, property, private equity, venture capital and crypto. If these changes proceed, Australia will become one of the least attractive places in the developed world to build, invest, take risk and realise gains. The one major asset still sitting outside this tax net is the owner-occupied home, which remains CGT-exempt. That creates a powerful distortion. If investment properties, businesses, shares, commercial property and other assets are hit with materially higher effective CGT rates, capital will rationally look for shelter in the family home. The likely result: less capital for startups and productive enterprise, lower productivity, more pressure on rents as investors retreat from housing, higher inflation and interest rates, weaker demand for risk assets, and even more money being recycled into owner-occupied property — the last great tax haven in Australia. In short: this is not just a profound increase in the tax burden, with zero consultation in the name of giving imprudent politicians more money to waste. It is a major repricing of risk-taking in Australia. It is not reform: it is highly regressive, as it seeks to punish entrepreneurial success, which is the key driver of long-term jobs, incomes, growth and prosperity. It does not boost productivity: it destroys it by actively discouraging innovation and business creation. It will not lower the cost of living: it will lift it by boosting rents and making us much more inefficient. It will not reduce interest rates: alongside rampant and reckless government spending and record migration, it will pressure the RBA to raise our mortgage repayments. What is perhaps most shocking is that only 12 months ago this government was elected on the basis promising to never make these changes...

Excuse my shitous video but this captures the essence I’m in the sprayer ahead of the autonomous sowing tractor. 2 machines operating with one operator. It’s great when the pieces fit together. Had a successful sowing with Ornata last paddock.

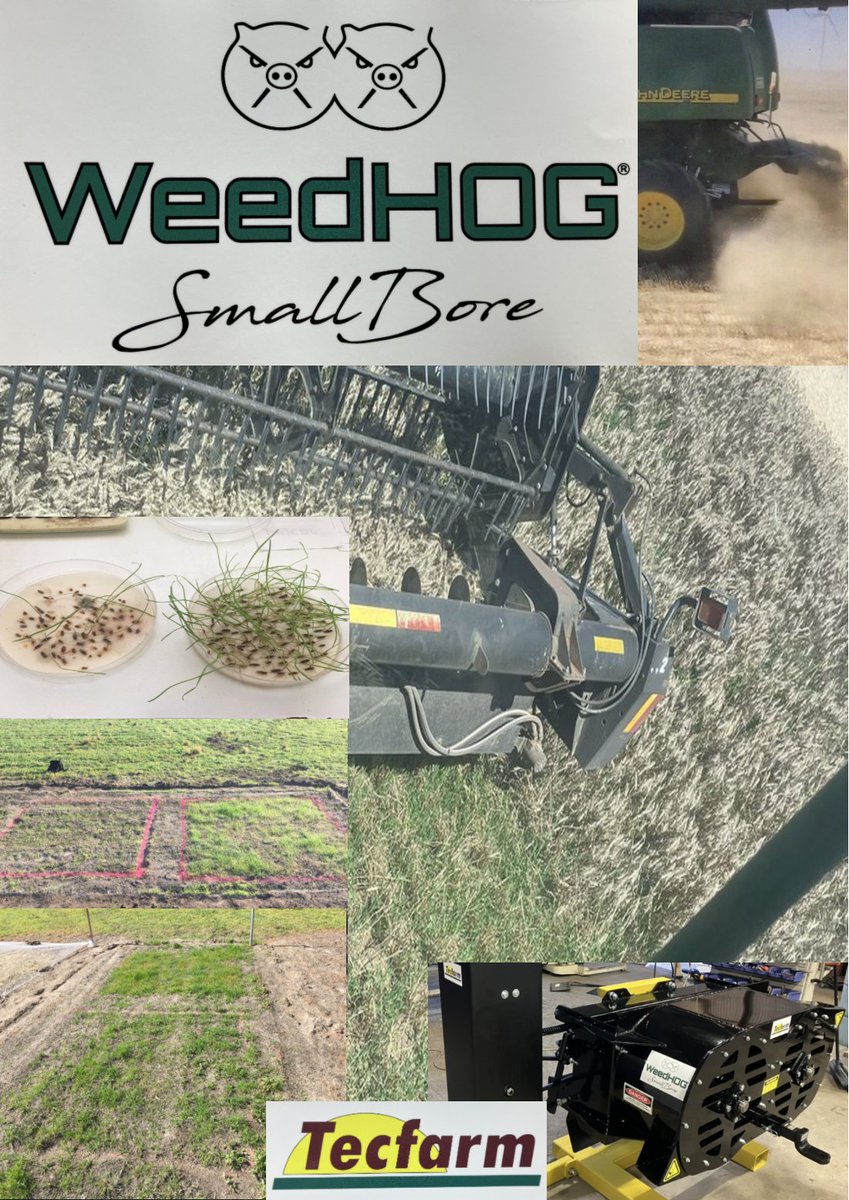

WeedHOG: Royalties only!

The aim is simply to make this unique tool available where other options for harvest weed seed control don't fit.

So a "royalties only" arrangement is available to an ag engineering business willing to do a small amount of further R and D, basically just fitment of the proven unit to more harvester makes.

WeedHOG is different: the method sits alone in its field, having competitive advantages that are hard to match.

WeedHOG's totally unique REVERSED INERTIA mode of action (simply, the "bug on the windscreen effect") is an exciting advance in seed mill design.

WeedHOG offers game changing advances in the field of harvest Weed Seed Control worldwide.

WeedHOG has the Big 4++++'s.

+1. Innovative multiple action seed kill.

+2. Lowest power draw of any mill.

+3. Excellent ability in damp conditions.

+4. Low dust output.

They're all a Big +

WeedHOG's simplicity makes HWSC possible for all combines, even the smallest machines and in damp harvest conditions. This is indeed unique.

Much has been achieved by a small farm based team in Western Australia using only private resources.

So now it's an opportunity for a business with capacity and vision, who's focus is Ag Engineering. Big or smaller, no matter where located.

The ROYALTIES ONLY LICENSE ARRANGEMENT MINIMISES ANY DOWNSIDE!

Strong multi region IP protection is in place. All working drawings are included. The maths look very good.

DM here for more.

The mouse population in parts of wa is out of hand @APVMA seems to not have an interest in doing anything about an emergency permit for us. All knowing full well that 25 g active mouse bait is not effective. The numbers we have are the worst I’ve seen.

@michaelsnape@HallRaelene You forget that the likes of Perth might have a million vehicles. They all get topped up 50l. That is your strategic reserve gone. 50 million litres. Herd mentality.

This is a monumental crisis for Australian agriculture, and I urge politicians and authorities to act urgently. No more round-tables, take control now. You are elected by the Australians to make hard decisions. This is it, now is your time.

Please read and repost Brad Jones in The Australian today. Also posted by OKA Australia.

#fuelcrisis @RogerCookMLA@AlboMP