Milton Friedman:

“What we call a deficit is simply a form of taxation; it’s hidden taxation.”

“If it is financed by printing money, it’s taxation in the form of inflation. If it is not financed by printing money, it’s an invisible tax on all property.”

Comment on $MU

Micron’s numbers are not just strong; they are almost implausibly good for a company that, until recently, was treated as a textbook commodity cyclicals story. Q3 revenue of $41.46B versus $35.59B expected and adjusted EPS of $25.11 against $20.60 would, on their own, justify a relief rally; pairing that with Q4 guidance for $50.0B in revenue versus a $42.92B consensus, adjusted EPS of $31.00 versus $25.50, and an 86% gross margin is an explicit challenge to anyone still modelling Micron as a mid‑cycle memory producer rather than an AI infrastructure utility.

The world is now structurally short compute, and in that world memory is not just a component but a form of “packaged intelligence”. Yet Micron still trades as if nothing has changed: the bears insist the cycle is already over, and the stock continues to command a massive discount to the broader market, much as it did in the pre‑AI era.

Either this upturn is fundamentally different , disciplined capacity, structurally higher HBM content, longer AI server replacement cycles, in which case that discount is a mispricing. Or it is not, and these are just the fattest margins of a familiar boom‑bust pattern that will again end with oversupply and crushed returns. The bears do not need to like this print. But if they still insist on fading it, they need a much better story.

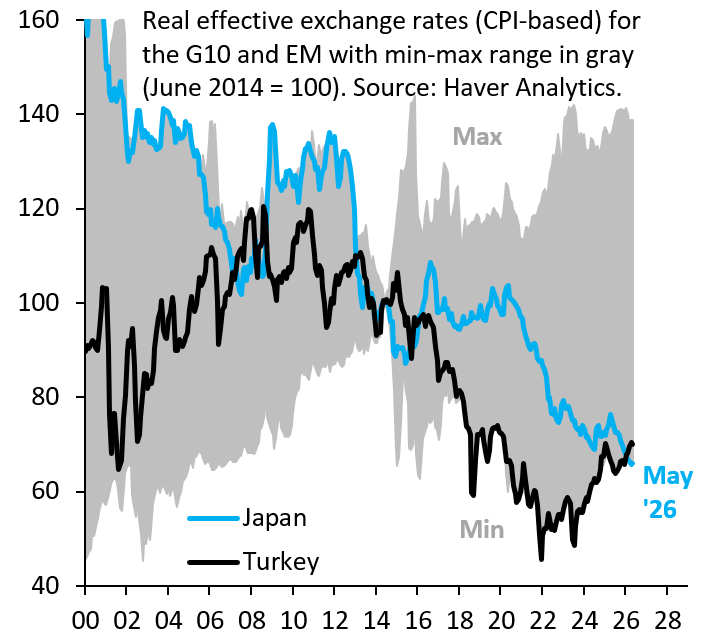

When is a crisis a crisis? The Japanese Yen is consolidating its fall below the Turkish Lira, making it the world's weakest currency. We're used to calling currency crises for Turkey, but we're reluctant to do the same for Japan. But Japan is in crisis...

https://t.co/c0kFK8YqeV

MICRON SEES AI-DRIVEN MEMORY SHORTAGE EXTENDING BEYOND 2027

• MICRON EXPECTS TIGHT MEMORY MARKET CONDITIONS TO PERSIST BEYOND CALENDAR 2027 DUE TO SURGING AI-DRIVEN DEMAND ACROSS ALL SEGMENTS

• COMPANY SAYS IT CURRENTLY HAS NO CLEAR VISIBILITY ON WHEN MEMORY SUPPLY WILL CATCH UP WITH GROWING DEMAND

• MICRON PROJECTS OPERATING EXPENSES TO INCREASE BY APPROXIMATELY $1 BILLION IN FISCAL 2027

• FISCAL Q4 CAPITAL EXPENDITURE EXPECTED TO REACH AROUND $10 BILLION

• FULL-YEAR FISCAL 2026 CAPITAL SPENDING FORECAST AT APPROXIMATELY $27 BILLION

• QUARTERLY CAPEX IN FISCAL 2027 EXPECTED TO EXCEED FISCAL Q4 2026 LEVELS

• COMPANY CONTINUES TO AGGRESSIVELY INVEST IN CAPACITY TO MEET AI-RELATED MEMORY DEMAND

• MICRON NOTES THAT POTENTIAL IMPACTS FROM TRADE POLICIES OR GEOPOLITICAL DEVELOPMENTS ARE NOT INCLUDED IN ITS GUIDANCE

• UNDER STRATEGIC CUSTOMER AGREEMENTS, MICRON EXPECTS TO RECEIVE APPROXIMATELY $22 BILLION IN CASH DEPOSITS AND RELATED FINANCIAL COMMITMENTS

• COMPANY PLANS TO INCREASE CAPITAL RETURNS TO SHAREHOLDERS

• MICRON STATES IT EXPECTS TO RETURN 100% OF EXCESS CASH TO SHAREHOLDERS OVER TIME

• COMMENTS REINFORCE THE VIEW THAT AI INFRASTRUCTURE DEMAND CONTINUES TO OUTSTRIP MEMORY SUPPLY, SUPPORTING A FAVORABLE PRICING ENVIRONMENT FOR DRAM AND HBM PRODUCERS

Last night’s speech by Treasury Secretary Scott Bessent signals the decisive shift in US economic doctrine: from efficiency to sovereignty.

Invoking Alexander Hamilton, Bessent framed industrial capacity not as a legacy asset, but as the foundation of national power in a contested world. The comparison is not casual. If carried through, it would make Bessent the most consequential Treasury secretary since Hamilton himself.

The message is clear. Globalisation optimised for cost has left the US exposed, to supply disruptions, geopolitical coercion and technological leakage. Dependence is no longer a benign feature of trade; it is a strategic vulnerability.

This is not autarky, but reprioritisation. Semiconductors, energy systems, advanced manufacturing and compute infrastructure are being recast as sovereign capabilities. Supply chains are judged less by efficiency than by their ability to withstand shocks and resist pressure from adversaries.

The economics are less comfortable. Resilience implies higher costs, sustained fiscal support and the risk of stickier inflation. But Washington appears willing to pay.

For markets, the shift is structural. Capital will follow policy into strategic sectors, while exposure to adversarial supply chains will command a growing discount. Hamilton’s logic has returned. This time, markets may have less choice but to follow.