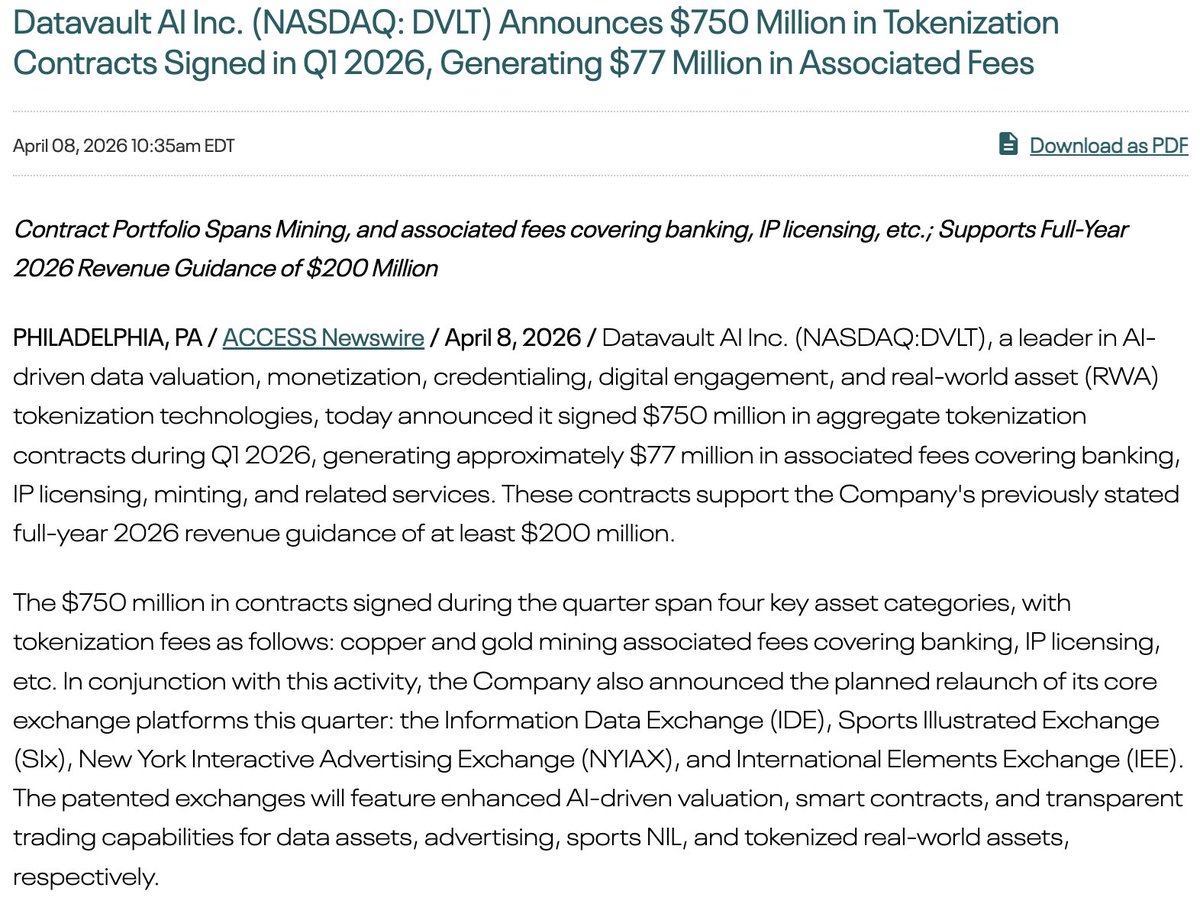

BREAKING NEWS:

I think the fee math here is what wakes people up on Datavault AI Inc $DVLT.

Q1 2026:

$750M aggregate tokenization contracts

$77M associated fees

That implies roughly a 10.3% fee layer on the announced contract base.

Then compare it to the old business:

FY2025 revenue = $39.1M

Q1 fee pool = $77M

That means:

nearly 2x full-year 2025 revenue

about $37.9M more than the entire FY2025 revenue base

Then the next checkpoint:

May 12, 2026 earnings

Revenue estimate = $20.4M

3 analysts

Price target = $4.00

Then execution:

4 asset categories

4 exchanges relaunching this quarter

IDE

SIx

NYIAX

IEE

That is why I think this can keep pushing a much wider revaluation story.

$FLY looks to be the next asymmetric space stock 🪰

He's too humble but this savage @AlmaCap114204 went big into $ASTS at single digits.

He found $KRKNF long before me, and got filthy multi-bagger returns.

Now he's calling $FLY. I suggest you study his work.

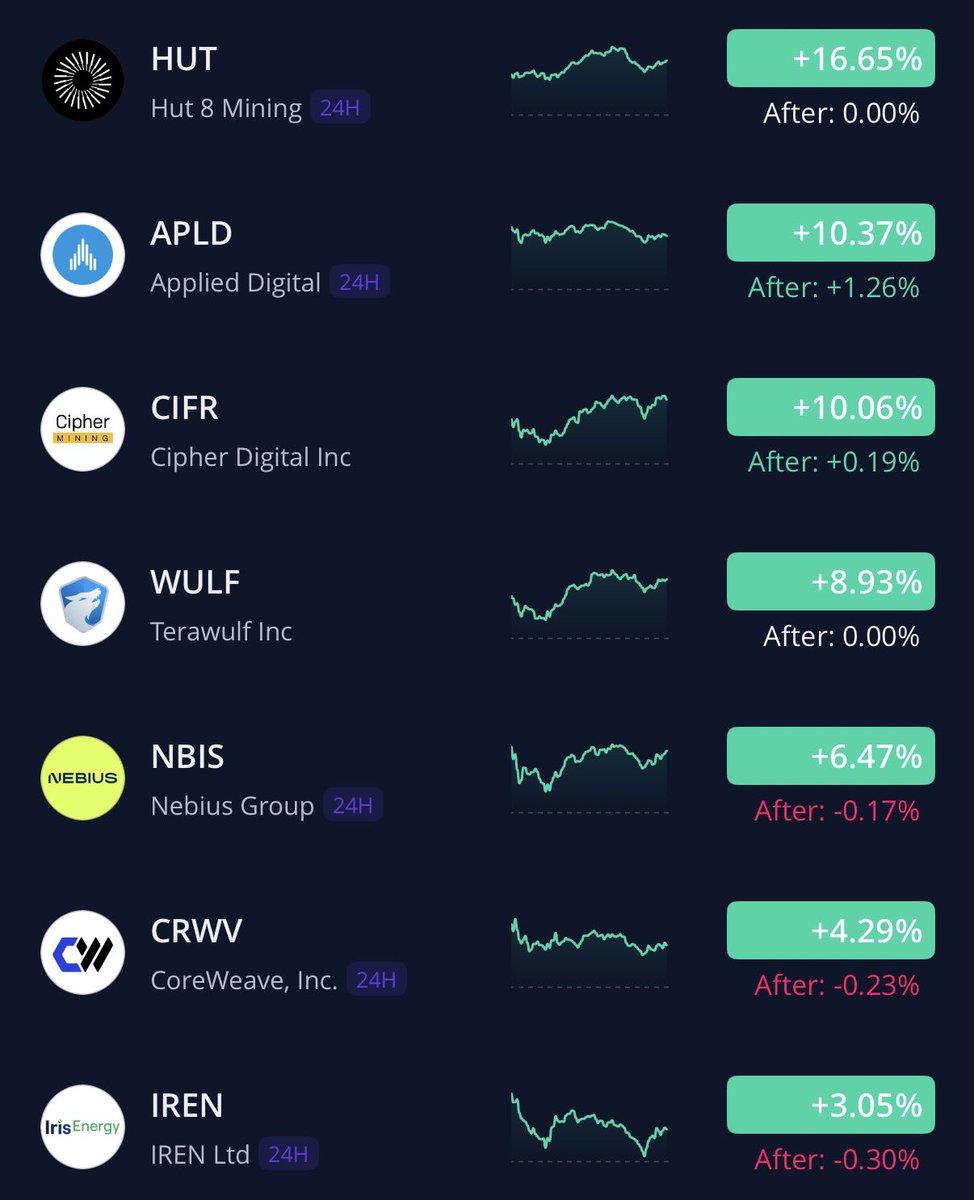

$WULF went from a 52-week low of $2.06 to ~$19 today!!! 📈📈📈

That's nearly a ~9x run in under a year...

@TeraWulfInc is ditching Bitcoin mining and pivoting to AI data centers and HPC leasing.

The market is starting to believe it... 🐺🐺🐺

What a day for data centers with $HUT $APLD & $CIFR leading the pack

$IREN is likely dealing with near term ATM overhang as the rest of the sector has outperformed lately

Long term remains accretive

$AEHR keeps making ATHs today and is in price discovery territory.

The price target I set at the beginning of the year? $70. We're almost there. When I set the price, I mentioned it wasn't my ultra bull scenario, which seems to be playing out.

I'm thankful as a long-term investor I don't have to try and guess short-term movements.

BREAKING NEWS:

I think the reason this Datavault AI Inc $DVLT update feels bigger than a normal small-cap headline is because now the timeline is getting crowded with numbers.

You have the release:

$750M in Q1 2026 tokenization contracts

$77M in associated fees

$200M+ 2026 guidance supported

You have the old base:

$39.1M FY2025 revenue

So the fee pool alone comes in at about 1.97x the entire prior-year revenue.

Then you have the next checkpoint:

May 12, 2026 earnings

Q1 / 2026

EPS estimate: -$0.07

Revenue estimate: $20.4M

Revenue Q2Q: 3,143.24%

EPS Q2Q: 60.33%

3 analysts

Then you still have:

4 asset categories

4 exchanges relaunching this quarter

IDE

SIx

NYIAX

IEE

That is why I keep landing on the same conclusion:

this still looks like the beginning of a wider revaluation story.

$RKLB trades at roughly 45x 2026 revenue estimates.

$FLY guides for $420 to $450 million this year and trades at about 13x that. The market cap gap between them is 7 to 1.

But $RKLB is a launch and spacecraft company. $FLY is a launch company, a lunar lander company, a defense software company already inside the Pentagon's Golden Dome contracting framework, and an orbital transfer vehicle company. Firefly and SciTec were onboarded to the MDA's Golden Dome vehicle earlier this year. The ceiling on that contract is $151 billion. Imagine if SciTec gets 1% of this.

SciTec is also the first new prime contractor for U.S. missile warning ground systems in 50 years. That position exists inside $FLY at a 7x valuation discount to its closest public comp.

Miranda has crossed 100 hot fires. Eclipse first flight is 2027. Four Alpha launches guided this year with potential for 6 to 8 with Block II debuting on Flight 8.

$FLY $RKLB $LUNR

$HUT

Bull flag on the daily chart breaking out today

This has held this range since the new year

We can see some serious expansion over $67

Another data center name pushing