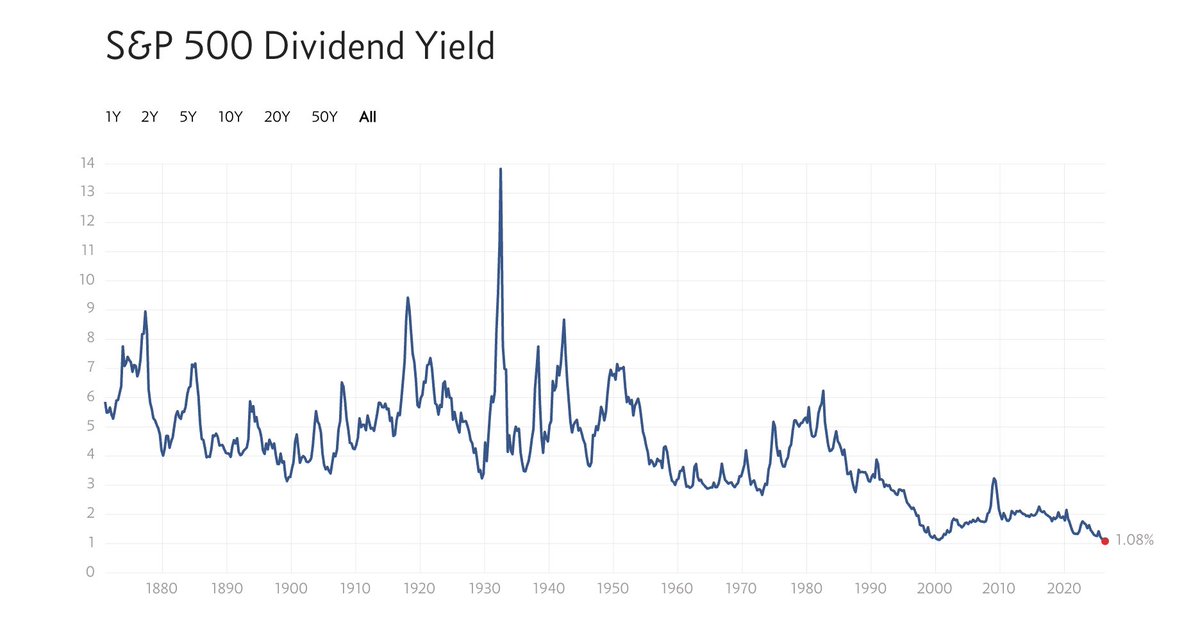

The S&P 500 dividend yield just hit an all-time low of 1.08%, going back to the 1800s. The prior low was 1.1% in 2000.

There are now "dividend" mutual funds with negative yields (their expense ratios are higher than their dividend yields).

Stock buybacks have exceeded dividends since the late 1990s.

And yet, nearly all stock funds still focus solely on dividends, which is crazy. (And it's not just about the buybacks, but also the share issuance!) Buffett's been talking about this more than anyone for decades...

We wrote a book on the topic 13 years ago, and the 2nd edition is free online.

As you tune into the Berkshire meeting, and gasp at the $400 billion in cash on their balance sheet, understand why they consistently choose buybacks over dividends...

https://t.co/rohyv8nzt0

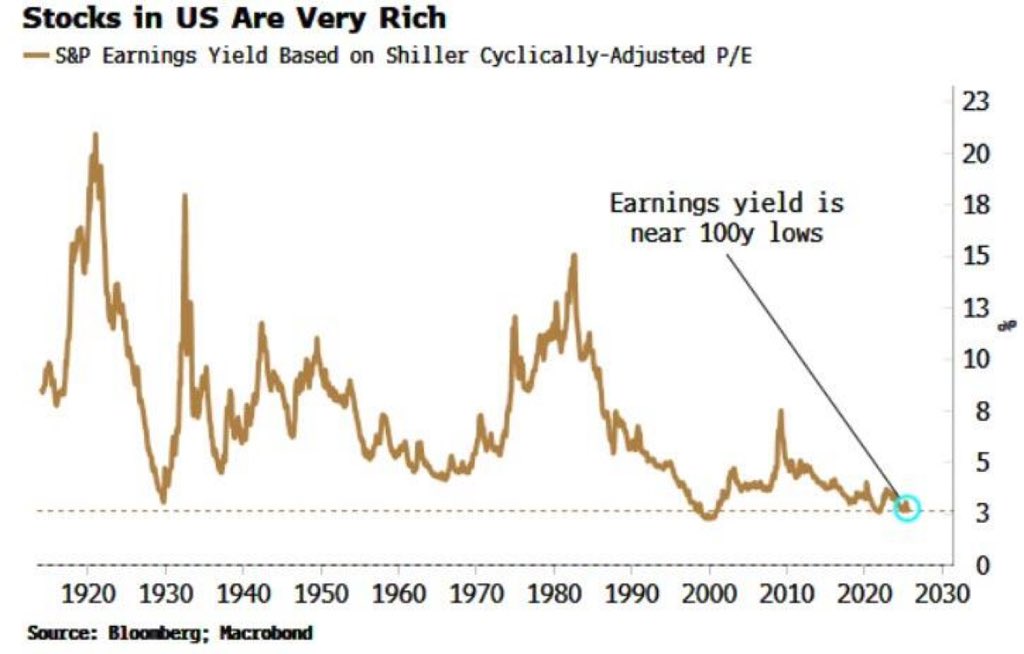

Chart: Multpl

Paul Tudor Jones just said something the market really doesn't want to hear.

"We're clearly so leveraged in equities in this country. We're 252% of stock market cap to GDP. In 1929, we were at 65%. In 1987, about 85%. In 2000, we got to 170%. And now we're at 252."

Every number he listed, 1929, 1987, 2000 ended the same way.

"If you think about the periodicity of significant bear markets since 1970, we get a mean reversion about every ten years. That would be a 30 to 35% decline. Well, 35% on 250% of GDP is 89% of GDP. The reverse wealth effect, oh my gosh. 10% of our tax revenues are capital gains; they go to zero."

This isn't a perma bear making noise but Paul Tudor Jones called the 1987 crash before it happened and made 200% that year.

When he talks about mean reversion, he's speaking from a track record that almost nobody in finance can match and then he said this:

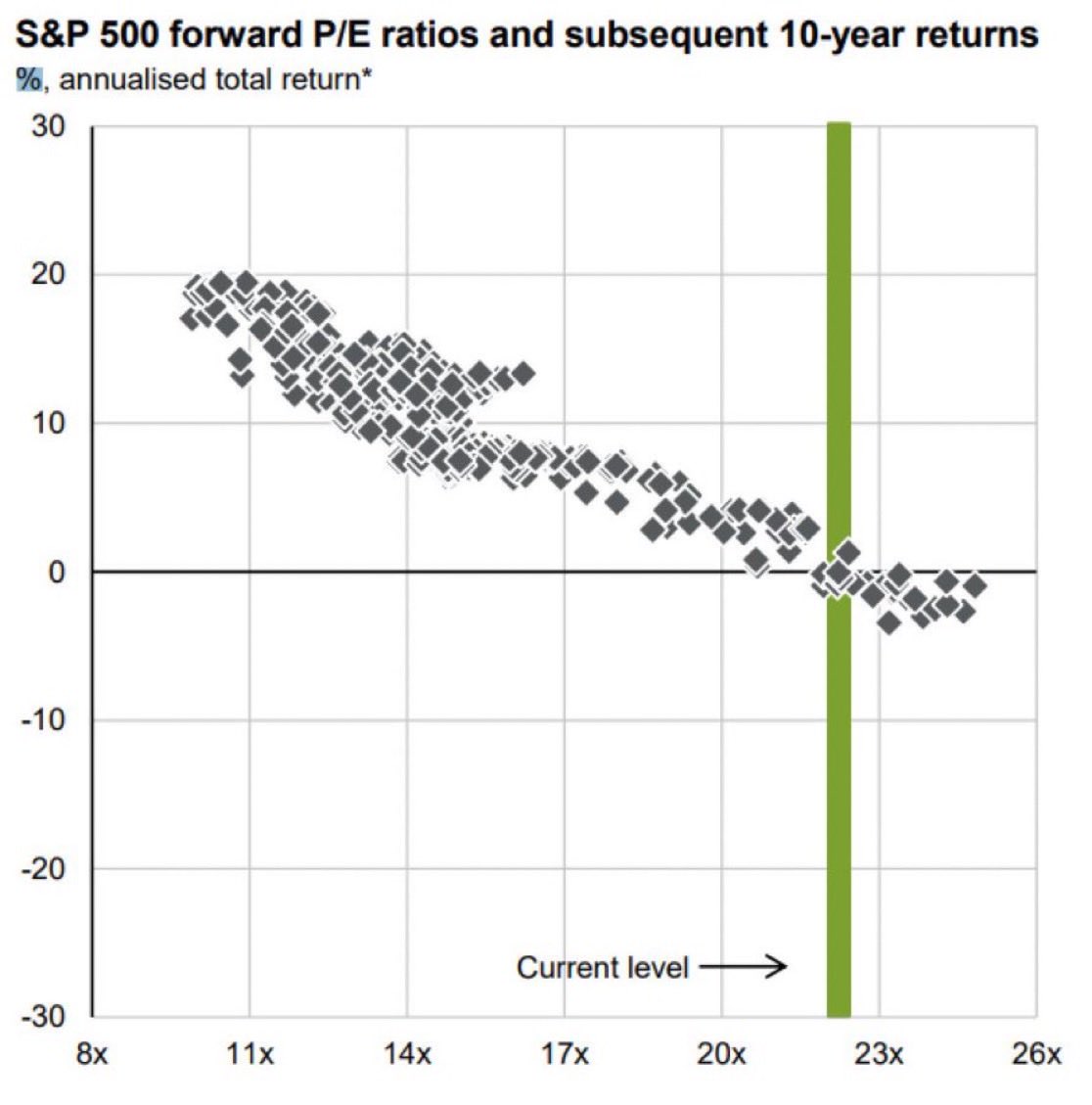

"If you buy the S&P at this current valuation, the 10-year forward returns are negative when you buy with the S&P P/E of 22. That's what history shows."

He's right, every major study on long-term equity returns shows that starting valuation is the single most predictive variable for 10-year forward performance.

At a P/E of 22, history doesn't give you a great answer.

"The real problem is, if you look at private equity in 2007 and 2008, that was about 7% of institutional portfolios. Now it's about 16%. Real estate's gone up. Infrastructure bets have gone up. We're so much more illiquid than we were in 2008."

In 2008, the crisis was bad because the system was leveraged.

Today the system is leveraged and illiquid, pension funds, endowments, and sovereign wealth funds can't hit a sell button on private equity.

They can't exit real estate in a week, when forced deleveraging starts in a system this illiquid, the exit doors are half the size they were last time.

Jones didn't say a crash is coming tomorrow.

He said the conditions that produce the worst outcomes in financial history are more present right now than at any prior peak he's seen in 50 years of trading.

He said buying the S&P at these levels and expecting the same returns as the past 100 years is math that doesn't work because those 100-year averages include decades when stocks were priced at 6 or 7 times earnings, not 22.

"Valuation matters a lot, and the stock market's really high, and it's going to be really hard to make money from here."

Warren Buffett was asked if Berkshire’s purchase of $AMZN (2019 at $89) was a departure from value investing.

His answer cuts straight to the heart of what value investing actually means:

“The idea that value is somehow connected to book value or low price to earnings ratios or anything, as Charlie has said all investing is value investing. You’re putting out money now to get more later — and making a calculation on the probability of getting it, and when.”

___

Buffett dismantles one of the most common misconceptions in investing. Value investing was never about low price-to-book ratios or cheap multiples. That’s a methodology — not a definition.

The definition is simple: you’re paying a price today for a stream of future cash flows, and you’re asking whether you’re being adequately compensated.

The label “value” vs. “growth” has always been a false dichotomy. All intelligent investing is value investing.

___

🎙️ Berkshire 2019 Annual Meeting | CNBC Warren Buffett Archive (05/04/2019)

Warren Buffett’s greatest lesson: NEVER CHASE.

In the market, you have time. If an exceptional company trades at insane prices, don’t buy it.

Wait for an exceptional company at a reasonable price. When you find it, invest heavily.

If you don’t, wait.

What's embarrassing to me is it's the start of the NCAA Wrestling Championships ESPN has not a single word about the Championships. Full coverage of WNBA which nobody watches and even information about women's boxing. Not a peep about the NCAA Wrestling Championships absolutely incredible

People really expect the S&P 500 to deliver a +10% annual return.

Not realizing that from 2000 - 2009 the market was flat.

An entire decade of no returns.

Americans are defaulting on debt at a crisis pace.

The share of U.S. credit card balances that are 90+ days delinquent rose to 12.7% in Q4 2025, the highest level since Q4 2011.

“90% of people don’t think about stocks the way I do. They think of it as something which will go up next week.”

“I think about what a company will be worth in 20 years. When prices fall, I hope they drop more so I can buy more. Most people do just opposite.”

- Warren Buffett

Credo Technology $CRDO on track for largest loss in 14 months 🚨 But perhaps a glimmer of hope for Bulls as it approaches a level that has held strong since July ✅ For magnified exposure, consider the Tradr 2X Long CRDO Daily ETF $CRDU from @TradrETFs

⚠️US auto loan delinquencies are SKYROCKETING:

The 60+ day delinquency rate on US subprime auto loans hit 6.9%, an ALL-TIME HIGH.

They are now higher than the 1996 peak and way above the Great Financial Crisis levels.

Subprime delinquencies have also more than DOUBLED over the last 4 years.

Meanwhile, US total auto loan debt surged +$12 billion in Q4 2025, to a RECORD $1.7 trillion, driven by higher car prices.

Americans are falling behind on their debt at an alarming rate.

⚠️ US households are ALL-IN on stocks:

Household equity holdings jumped to a record 33% of S&P 500 market capitalization.

The percentage has nearly DOUBLED since the 2020 Crisis low.

This now exceeds the 2000 Dot-Com Bubble high by 8 percentage points.

By comparison, the previous record was ~28% in the 1960s.

Meanwhile, cash allocations have dropped to near the lowest levels in 26 years.

Americans have never held so many stocks.

Are they aware of potential risks?