Les comparto el enlace del recital de fin de año de parte del taller de piano ITAM.

https://t.co/LcnPIrYLq0

Un fragmento de la intervención de su servidor (min 25)

İktisatçılar için hazırlanmış bir AI “skill” koleksiyonu.

LSE’den Antonio Mele’nin derlediği açık kaynak koleksiyon, iktisatçılara özel 17 hazır AI skill sunuyor.

Claude Code, Cursor, Codex ve Gemini CLI ile uyumlu, ücretsiz.

Link 👇

https://t.co/HQkG69TgGM

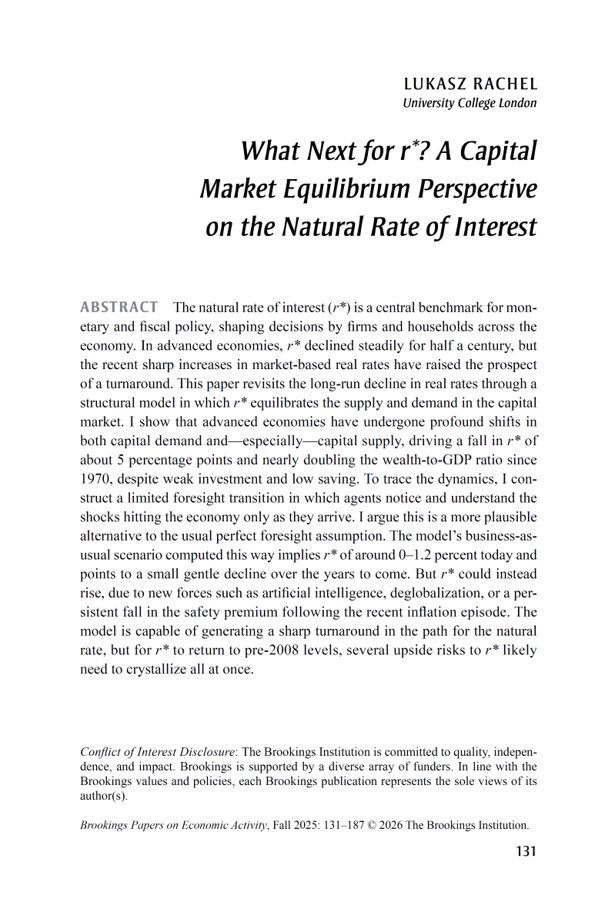

Highly relevant!

"A capital market equilibrium perspective on the natural rate of interest" by Lukasz Rachel.

"The natural rate of interest (r*) is a central benchmark for monetary and fiscal policy, shaping decisions by firms and households across the economy. In advanced economies, r* declined steadily for half a century, but the recent sharp increases in market-based real rates have raised the prospect of a turnaround. This paper revisits the long-run decline in real rates through a structural model in which r* equilibrates the supply and demand in the capital market. I show that advanced economies have undergone profound shifts in both capital demand and—especially—capital supply, driving a fall in r* of about 5 percentage points and nearly doubling the wealth-to-GDP ratio since 1970, despite weak investment and low saving. ...But r* could instead rise, due to new forces such as artificial intelligence, deglobalization, or a persistent fall in the safety premium following the recent inflation episode. The model is capable of generating a sharp turnaround in the path for the natural rate, but for r* to return to pre-2008 levels, several upside risks to r* likely need to crystallize all at once."

https://t.co/19h4RO77ZM

Momentarily set aside the specifics in this thread---can come back to it later to take a second to celebrate a public official laying out their economic arguments for tariffs, engaging with the literature logic and uncertainties. I value that.

📄 New working paper out! 🚨

"The Hand-to-Mouth Share Over the Business Cycle"

Does the Hand-to-Mouth (H2M) share move over the cycle? 👉 Yes — and countercyclically: it rises in recessions, falls in booms.

Link: https://t.co/NW34BUdK3G

New US series, 1989–2024. 🧵👇

Akademisyenler için Claude Code’u nasıl kullanacağınıza dair basit bir giriş.

Alessandro Spina'ya ait sunum slaytları ve GitHub deposu.

🔗 https://t.co/FCfOers2Lw

Sticky wages yes, but how? Sticky wages in most contemporary models assume that all workers belong to a union that has a labor monopoly and charges above market clearing wage. Reality, not many unions, and more worry about employer market power. Unreality of NK model assumptions at some point sticks in throat. So WHICH sticky wage model would you like us to use?

Monetary policy moves labor supply after all! 👇 When policy tightens, aggregate hours fall, but low-income workers work more. In our JEEA paper, we document this surprising left-tail response in U.S. labor market data. 🧵1/N #EconTwitter

Open Access: https://t.co/kb3urJjbcL

New paper: "How Does Monetary and Fiscal Policy Affect the Economy in the Face of Large Shocks?" (with @KenMiyahara ) Paper: https://t.co/76PmxQm9He

Two model features are important for understanding the effects of policy in the COVID era: heterogeneous households + state-dependent pricing.

How would the US economy have evolved under different fiscal and monetary responses? 🧵

Coming back from a great conference at Banca d'Italia: lots of great papers, posters and discussants, and wonderful setting... Rome is a bit toasty right now, but always miraculous. Thanks to the hosts!

This was such a fun workshop! 🙏 Thanks to everyone for coming and to @MathiasTrabandt & Team for organizing! As always, all our materials are public: https://t.co/6NhaAeZqSe Maybe the coolest new thing we tried this year is vibe-coding with SSJ... it's absolutely insane! 🚀

Super interesting!

"Seemingly Anchored Inflation Expectations" by Ulrike M. Malmendier and Stefan Nagel.

"Empirical evidence commonly cited as indicating that inflation expectations have become better anchored includes the declining sensitivity of expectations to inflation surprises over time, particularly around the adoption of inflation targeting. These patterns are typically attributed to the influence of explicit or implicit inflation targets on inflation expectations. We show that this evidence is consistent with a model of experience-based learning in which individuals learn solely from their life-time history of realized inflation, without anchoring their expectations to an announced inflation target. In this model, the prolonged experience of low short-run inflation persistence in the pre-COVID decades renders long-run expectations insensitive to inflation surprises, matching the patterns observed in empirical anchoring tests. A unique prediction of the experience-based learning model is also borne out in the data: the decline in surprise sensitivity since the 1980s is strongest among younger individuals. The memory of low inflation persistence experiences further explains why long-run inflation expectations remained stable in the face of the post-COVID inflation surge. At the same time, simulations indicate that the sensitivity of long-run expectations to inflation surprises would rise sharply if individuals were to experience another sustained episode of highly persistent inflation. Overall, long-run inflation expectations may be less firmly anchored than commonly believed."

https://t.co/y8Z8jX2fdd

This sounds really cool!

Agentic AI for DSGE Modeling: "LLMacro: A Language Server for Dynare."

"A Language Server Protocol implementation and Model Context Protocol (MCP) server for the Dynare modeling language. It gives you live diagnostics, steady-state solving, Blanchard–Kahn checks, and model intelligence in your editor or in an AI coding agent. Structural parsing and validation defer to a bundled Dynare 7.1 preprocessor, so what the language server accepts matches what Dynare itself accepts. On top of that it adds a clean-room Blanchard–Kahn rank check, an automatic steady-state solver, per-equation residuals, and a large family of model, estimation, policy, shocks, and usage diagnostics."

"You can use it three ways:

In VS Code, via the bundled extension (.vsix).

In Claude Code (or any MCP/LSP-capable agent), via the bundled plugin.

From the command line, for one-shot --check runs."

Github:

https://t.co/RFcwsl7Tl9

Working paper: Diercks, Anthony, Philip Howard, and Mehrdad Samadi. 2026. "LLMacro: A Language Server for Dynare." Working paper.

El salario mínimo también sube salarios informales. Este artículo presenta evidencia causal de frontera en Brasil, con lecciones para otros contextos. Buen antídoto contra el libreto de siempre en Colombia: que el mínimo “solo beneficia a unos pocos”.

https://t.co/C5eJwml55J

Today, the Stanford @DigEconLab launches the AI Economic Indicators, a new platform for tracking how AI is reshaping work, productivity, adoption, and the economy.

1/6

There appears to be unanimous agreement that AI will *meaningfully* bolster labor productivity. @DrDaronAcemoglu thinks so too, which seems a change. https://t.co/yDUJPxmEEt

Excited to see this out. Grateful to the referees and editor for their excellent and constructive comments, which greatly improved the paper.

Reposting the earlier 🧵 summarizing the paper:

A new working paper of mine, forthcoming in JPE: Macroeconomics, makes a simple point with data. The point is old and well understood, but easy to forget.

When output is supply-constrained, or close to it, with a steep aggregate supply curve, a central bank can engineer rapid disinflation at little cost to output. Raising rates aggressively does nothing more than withdraw the excess aggregate demand.

Many missed this during COVID and the recent energy shocks. A central bank that accommodates when output is supply-constrained is pushing on a string.

The same withdrawal of excess demand can come through fiscal policy, and in some circumstances, that is the better tool. This was Keynes’ central insight in his 1940 essay, “How to Pay for the War.”

My read is that many central banks drew the wrong lesson from the late 2000s and early 2010s. Expansionary monetary and fiscal policy did not raise inflation then, but only because output was demand-constrained. Accommodation buys output cheaply when demand is the constraint. It buys inflation when supply is.

There is an equivalent reading through the FTPL. For space, we set it aside in the paper, but we are really making a statement about the real value of government debt. When output is supply-constrained, an excess of nominal claims chasing a fixed bundle of goods shows up as inflation: the price level rises until the real value of outstanding nominal liabilities equals the present value of the primary surpluses that back them. Disinflation then requires raising that present value, either through higher future surpluses or by retiring claims today, which is exactly what an absorption of excess demand does. Keynes’ compulsory saving scheme and the central bank’s rate hike become two routes to the same revaluation.

An ungated copied can be found here:

https://t.co/wy4J6g4sLV