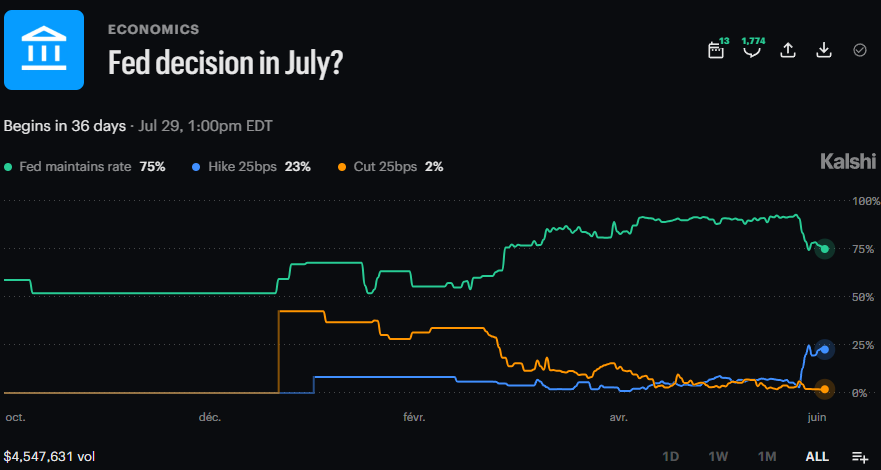

📊UBS SAYS MARKETS ARE TOO HAWKISH

Markets are increasingly pricing in Federal Reserve rate hikes, with prediction markets showing rising odds of tighter policy.

UBS disagrees, saying investors are overestimating the likelihood of hikes and still expects the Fed's next move to be a rate cut in 2027.

The gap between market pricing and UBS's outlook continues to widen.

https://t.co/KAtYHiA1dR

@pakpakchicken But the conversion means that new shares are issued , i.e they don’t need to buy the stock on the open market to close the shorts but rather just use the converted newly minted shares.

the upside of this is they wouldn’t need to use the att funds to pay down this debt?

Most detailed, accurate calculation of $SATS i’ve seen.

Includes all concerns of tax, debt after sale and whatever minimal dilution.

This is a short squeeze in the making. I’ll explain the thesis next time.

Are AI labs headed toward airline-level competition and capex intensity, PLUS utility-level regulation and public dislike?

Tough recipe for supporting multiple trillion-dollar valuations.

SENIOR ADMINISTRATION OFFICIAL: IRAN DEAL ACCOMPLISHES CORE U.S. OBJECTIVES

IRAN DEAL REOPENS STRAIT OF HORMUZ - OFFICIAL

SENIOR ADMINISTRATION OFFICIAL: U.S. TO GET ENRICHED MATERIAL UNDER IRAN DEAL

U.S. OFFICIAL: IRAN DEAL GUARANTEES LONG-TERM PEACE IN REGION

SENIOR ADMINISTRATION OFFICIAL: IRAN DEAL INCLUDES INSPECTION REGIME

SENIOR ADMINISTRATION OFFICIAL: IF IRAN COMPLIES WILL BE REWARDED ECONOMICALLY

SENIOR ADMINISTRATION OFFICIAL: BENEFITS FOR IRAN ACCRUE IF THEY ACTUALLY DELIVER

SENIOR ADMINISTRATION OFFICIAL: U.S. EXPECTS TO SIGN AGREEMENT OVER NEXT FEW DAYS

SENIOR ADMINISTRATION OFFICIAL: DRAFT AGREEMENT ALSO LIFTS U.S. BLOCKADE AND LEADS TO DISMANTLEMENT OF IRAN NUCLEAR PROGRAM

Why I went all in $SATS

Here’s the maths:

SpaceX IPO at $135

SpaceX S1 disclosed Echostar owns 261.8 million shares

🔸$135 X 261.8 million shares = $35 Billion

While echostar was worth less than $35 Billion yesterday

Question:

Do you really think that you can put a $135 limit order on ipo day to get the shares?

NO!! Hyperliquid premarket AT $180 already 😂

Your best chance is do a market order buy on $sats before spacex ipo if you are bullish on spaceX

Here is where it gets crazier:

FCC APPROVED deal $22.65 Billion Cash for selling low to mid-band spectrum to AT&T

🔸So that’s worth ZERO? or NOBODY FKING CARED LMAO

My valuation ex- spaceX:

Net cash after debt paydown

$8.5 billion

Remaining unsold spectrum

$10 billion

Core operating business

$10 billion

Total Ex-SpaceX $28.5 billion

🔸Value per share EX- SpaceX ~ $86 ( Conservative )

Now let’s go from crazier to NUTS:

Short interest is 31% !!!! WTF LMAO

But the issue is founder owns 50.5% stake and 86.8% voting rights.

So the short interest on the remaining whatever available float? What’s that? 60++++%???

Seldom market hands you free money. When it does, go all in.

____

P.S. I seldom write long thesis anymore. Why? The hardworking ones will be rewarded with their own DD. You make your own conviction rather than relying on me for customer support.

And what do you want more when I put my own $$ on the line? Who does this transparently? Action speak more than words.

Once in a while, I'll write. But don't count on me mansplaining often. It's better for you to build your own conviction.

Paul Gu @paulxgu Morgan Stanley US Financials Conference 2026 Summary ✏️ $UPST

Executive Summary ⚔️

Co-founder Paul Gu frames Upstart as an "ultramarathon business" in an unusually hard credit underwriting space. The reason no one innovates here: third parties have to trust your models and fund your loans under heavy regulation, while your first ML models inevitably make bad loans causing you to lose money and credibility simultaneously for years before the payoff.

Having pushed through that, Upstart has built a roughly 3x model-accuracy advantage versus legacy players and is now prioritizing structural funding stability, shifting focus back to its high-margin core personal loan (<720 FICO) product, scaling new products, and guiding to 35% annual topline growth for three years, with the expectation of growing well beyond that.

Funding, Capital Markets, & Co-Investments 💰

Capital Demand & Spreads: Upstart recently completed an oversubscribed securitization. Upstart delivers consistently high spreads against Treasuries at scale, reflected in a 100% renewal rate among capital partners. Gu's framing: capital flows to the best risk-adjusted returns, and in normal times capital is not a constraint on growth.

Securing Longer Commitments: In a tougher capital environment, the top priority is longer-dated, committed capital (e.g., a recent 24-month deal) to insulate the business from 3-to-6-month liquidity shocks. The goal is a majority of capital long dated and committed but not 100%.

Co-Investment Structure: To secure durable funding, Upstart shares underlying credit risk via co-investments, funded by putting a portion of contribution profits from originations at risk. Gu views this as a good trade to resolve capital-market volatility. Consistent with Upstart's pattern, the first deal won't carry the best terms, and he expects them to improve from there and noted he's been "very happy with the progression of deal terms" even in this environment.

Long-Term Vision: Gu believes the scale of this business could make it one of the most important sources of yield for all of Upstart's partners.

Macro & Upstart Macro Index (UMI) 💥

Energy Shock: A recent energy shock has pressured consumers, pushing UMI up, Gu believes this is a real effect.

Historical Context: Prior UMI peaks of 1.6–1.7 came when inflation was near 10%. With inflation around 4% today, an energy shock can't bridge that gap. Gu doesn't see a path back to those extreme levels.

Resilience: Upstart's advances compound fast enough to absorb modest macro fluctuations, though a severe consumer deterioration would still be a significant problem.

Technology Advantage & Underwriting 🤖

Model Accuracy: Upstart's models are nearly 3x as accurate as traditional models, closing 12.6% of the gap toward a perfect credit model vs. the industry's 4.6%. The internal metric measures NPV of expected cash flows vs. NPV of realized cash flows. Significant advantage built over a decade, with substantial room left.

Tech Over Quarterly Smoothing: Upstart won't manage quarterly earnings at the expense of listening to the model (hello 3Q25!). To survive multiple credit cycles, Upstart responds to real-time data as fast as possible rather than trying to predict, accepting more short-term volatility. Real value comes from compounding tech advances over multiple years. Relatedly, Gu cautioned against over-indexing to the post-COVID period, which he views as having unusual features.

Growth Efficiency: Better models drive approvals, pricing, automation, and targeting, showing up as efficiency rather than marketing spend. Throughout the year, investors should watch topline growth "walk down the income statement" rather than being consumed above the line.

Product Mix & Margin Outlook 💵

Core vs. Super Prime: Upstart unlocked the Super Prime segment over the last year, big growth, but low margins. Two years ago, those borrowers would've gotten a terrible rate at Upstart. Now best rates for all have unlocked more general / broad marketing. Gu says mission accomplished with Super Prime, stating it's no longer a top priority, and focus is shifting back to the higher-margin core personal loan product.

New Products (HELOC, Auto, Cash Line): Currently quite negative margins, but expected to improve very rapidly near-term and to keep improving for years, without reaching a mature margin any time soon. Margin capture is tied to tech differentiation, which drives pricing power (better rates → higher take rates), mirroring Upstart's personal loan product which grew at expanding margins for nearly a full decade.

Overall Margin Impact: Even as new products scale at expanding margins, they'll "certainly" be dilutive to overall contribution margin near-term. Despite this, Gu "feels good about where the lower half of the income statement is going this year."

Strategic Bets & Capital Allocation 🏦

Bank Charter: Viewed as significant but not qualitatively different from Upstart's other strategic bets, and already factored into 3-year guidance. Upstart needs some of its bets to land to hit targets, but not all. Timeline is in regulators' hands (they remain optimistic), investors should expect sparse updates.

The business Upstart envisions is so large it would be nearly impossible to fund balance-sheet-centric in the short term, and a bank brings a much better cost of funding on the finance piece.

Balance Sheet: Upstart wants to stay highly efficient with equity to maximize per-share returns. They expect a tactical, not strategic reduction in the balance sheet, but Gu pushed back on a continuously shrinking balance sheet. He doesn't believe a modestly lower number is ideal and sees nothing wrong with where the balance sheet sits today. Gu expects more equity to deploy over time on the balance sheet (R&D on the balance sheet, new-product incubation, occasionally aggregation/sales or yield generation).

$RDDT Amid May Ad Metrics, RDDT Among Strongest Outperformers - Piper

May ad spend growth was above estimates and our buyer revised his estimates higher for 2Q and 2026. Positive standouts in our coverage were Youtube, ROKU, and RDDT, while notable underperformers included NFLX, TTD, and AMZN. Reddit ads manager data has been volatile, but we believe it is not an exact proxy for underlying user trends. May Ahrefs data shows a notable improvement in Reddit as a share of citations fueling AI Overview and AI Mode, and it now ranks #2 in share of domains by citations. RDDT Users Volatile (-): Reddit audience data in the Reddit Ads Manager fell 2% from April to May, but it was impacted by a 13% drop in users reported on May 20th that recovered two days later. We wonder if this was a glitch? Excluding the brief volatility, May users fell 0.6% vs. April. While the ads manager audience is an interesting directional data point, it may be more volatile/unreliable than we had appreciated. We believe strong commentary from management and improving performance in AI Search are more important positive signals for Reddit. Ad Spend (+): May ad spend was 30bps above estimates. Our buyer raised his 2Q spending estimates by 30bps and his 2026 estimates by 50bps. The strongest outperformers in May were X, Youtube, TikTok, Roku, and Reddit.

Sources: Anthropic is planning to release a public version of Mythos tomorrow

- Will have substantial guardrails and not be as cyber permissive as what Project Glasswing partners can access

- Will be dramatically better at long-horizon, multi-turn tasks https://t.co/cqq3Y5CVb0

HEDGE FUNDS LOADED UP BEFORE FRIDAY SELLOFF

Hedge funds bought global equities at the fastest pace in four months through June 4, according to Goldman Sachs Prime desk data, with North America and Asian emerging markets leading inflows. Consumer discretionary stocks were bought for a fifth straight week, and nine of 11 sectors saw net purchases.

Days later, U.S. markets sold off sharply, with the Nasdaq down 4.2%, the S&P 500 falling 2.6%, and the Dow losing 1.4%.