Real estate bears were demonized, attacked, and ridiculed for warning that Canada was building an economy on credit and house-price inflation.

Now insolvencies are at the highest level since 2009.

This was preventable.

Debt is not wealth.

Housing inflation is not productivity.

And bubbles always find their victims.

https://t.co/xNqyNMOi5h

What happens when your home falls 33% in value?

According to the Bank of Canada, nearly 1 in 10 Toronto area mortgage holders may not qualify to refinance in 2027.

Meanwhile, GTA mortgage delinquencies have already jumped 57% in a year.

This is the part of the housing downturn most people aren't talking about.

Breaking News: A federal judge said the Trump administration must restart applications for asylum and other immigration processing. https://t.co/J6qdEVUSM9

For new followers, my interest in real estate cycles is personal.

I bought a condo at the Toronto peak in February 1989. Four years later, prices had collapsed. The only thing that saved me from bankruptcy was that interest rates also collapsed.

Today, Toronto homeowners face a very different setup.

Four years after the 2022 peak, prices are down, but interest rates are higher, not lower. That is why we are now seeing rising insolvencies, forced sales, and heartbreaking stories from people who simply bought at the wrong point in the credit cycle.

That experience is what drives me.

My goal is not to be negative. It is to help people understand the Economic LongWave, recognize the risks of Economic Winter, and reduce the amplitude of the damage before the system forces the adjustment on them.

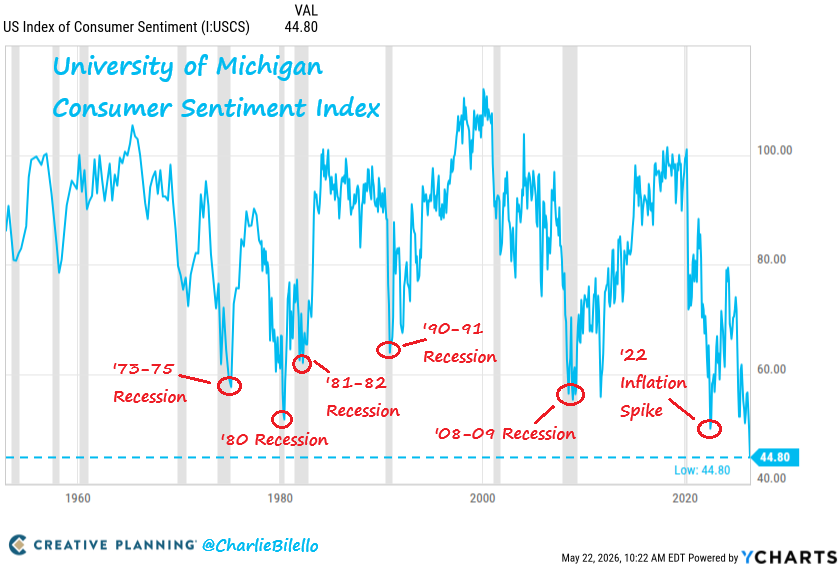

The US consumer sentiment index from the University of Michigan goes back to 1952.

It has never been lower than it is today.

Video: https://t.co/8USvFpWxZN

Canada’s household psychology has changed.

That matters more than most people understand.

People are not robots. They do not simply change their minds because policymakers cut rates, increase immigration, print money, or try to restart the real estate mania.

Once a speculative bubble breaks, psychology changes with it.

The belief that “housing only goes up” gives way to doubt.

Doubt becomes caution.

Caution becomes lower bids.

Lower bids become falling prices.

That is how a credit bubble turns into a debt-deflation cycle. ❄️

For years, Canada treated rising home prices as a sign of prosperity.

But much of it was not real prosperity.

It was credit expansion, leverage, and financial speculation.

Now the psychology is shifting.

Young people who were locked out of the market are not desperate to rescue the bubble.

Many are waiting for value to return.

And frankly, after two decades of unaffordable housing, lower prices would be a welcome relief for the next generation.

That is the part many people still do not understand:

You cannot easily restimulate a mania once the public stops believing in it.

Economic Winter is not just about falling prices.

It is about a change in psychology.

And once psychology turns, the old playbook stops working. 🌨️

There are two Canadas. There is the one the Boomers live in, where their homes are paid off, they go to their cottages, their homes have increased in value to insane levels. These people love Mark Carney. Then there is the rest of us, who are watching the entire system collapse.

@123headhunter@603859658@ShaneWenzel He is crying cuz he is loaded up with “sound investments” that he and other “real estate geniuses” like him only expected to go up. Well, tide is going out right now and they are flailing.

The Bank of Canada just said the quiet part out loud:

There is no path to affordability in Canada without home prices coming down.

Housing is already weakening.

No one is coming to save this market.

Homeowners with good credit scores are now defaulting on mortgages.

Near-prime delinquencies jumped 31% in one year.

In Toronto, Vancouver, Brampton and Markham the spike is 55%+.

The mortgage shock is no longer a subprime problem.

It’s spreading into the middle class.

🚨 “REALTORS ARE SCAM ARTISTS” — VIRAL VIDEO TORCHING THE INDUSTRY IS GOING NUCLEAR

A skit exploding across social media is ripping into the real estate industry, and it’s hitting a nerve.

In the video, a homebuyer slowly realizes something about the process that makes it look suspicious.

Every time she tries to make an offer, the real estate agent suddenly claims there’s “another bid.”

But when the buyer asks basic questions like who the bidder is, what they offered, or if they’re even real, the response is always the same:

“I can’t say.”

Then the realization hits.

If the price goes up… the agent’s commission goes up too.

Seconds later the house is “sold” and the real estate agent walks away with a $50,000 commission.

Now the internet is arguing.

Some say agents protect buyers through complex deals.

Others say it’s just the most expensive middleman job in America.

Be honest: are realtors worth it… or is the whole system a scam?

Canadian subprime lender Goeasy https://t.co/xVuHJwjdJo drops 58% today, but share prices of Cdn banks are up, though the customer base is generally the same. Are investors too complacent about the risks of lending to Cdn households?

We're watching a financial crisis unfold in real time.

The last time funds started blocking investors from getting their money back, Bear Stearns collapsed six months later.

In 2007, BNP Paribas froze €1.6 billion in funds.

Bear Stearns declared 2 funds "essentially worthless" and gated a third.

Everyone said it was "contained."

6 months later the entire financial system nearly went under.

I'm not saying we're there YET...

But I am saying the pattern is rhyming.

BlackRock just capped withdrawals from its $26 billion HPS Corporate Lending Fund after investors demanded 9.3% of their shares back - nearly DOUBLE the fund's 5% quarterly limit.

Investors wanted $1.2 billion out. BlackRock gave them $620 million and said no to the rest.

BlackRock stock dropped 7%. KKR, Ares, Apollo, Blue Owl - all down 5-6% on the same day. The financial sector ETF is off 9% in a month.

This is the same BlackRock that just slashed a $25 million private credit loan from 100 to ZERO in 3 months. Full value one quarter. Worthless the next.

And they'd already done the exact same thing months earlier with Renovo Home Partners.

But this isn't just a BlackRock problem.

Look at the dominoes:

Last summer, Tricolor and First Brands went unexpectedly bankrupt. $10-15 billion in combined liabilities. Write-offs hit JPMorgan, UBS, and Jefferies.

Then a UK lender called Market Financial Solutions collapsed with a £2.4 billion loan book.

Fraud allegations. Double-pledged collateral. Barclays exposed for £500 million. Apollo, Elliott, Santander - all caught in the wreckage.

Then Blue Owl permanently halted redemptions. Stock cut in HALF.

Then Blackstone's $82 billion flagship fund got hit with $3.8 billion in redemption requests. They had to pump in $400 million of their own money just to meet demands.

Now BlackRock is literally blocking the exits.

Even Apollo's own CEO warned a shakeout is coming.

When EVERYONE at the top is waving red flags - pay attention.

UBS raised its worst-case default forecast to 15%. Defaults sit at 3-5% today. The trajectory is ugly.

Here's the structural problem:

After 2008, regulations pushed risky lending OUT of banks and INTO private credit.

The sector ballooned to $3 trillion. But these funds make 5-7 year loans while promising investors quarterly liquidity.

That works until everyone wants out at once. Which is exactly what's happening.

40% of sponsor-backed loans are tied to the software industry - the same sector AI is threatening to destroy.

The Fed pumped 40% more money into the system after Covid and kept rates at zero.

That easy money funded garbage underwriting. And now there's a $162 billion maturity wall hitting THIS YEAR.

I've been warning about private credit for weeks. The story is always the same:

Opaque valuations. Illiquid assets. Limited transparency. And the false promise of steady returns with no volatility.

The whole sales pitch was equity-like returns with bond-like stability. But you can't eliminate volatility - you can only HIDE it...

Until you can't.

When the WORLD'S LARGEST ASSET MANAGER starts blocking investors from getting their money back, that's not "noise".

That's an alarm.

Get out before the exit gets more crowded.