Citi: Physical AI Summit

> According to a Wednesday morning note by Citi analyst Heath Terry, the robotics industry is moving past the experimental phase and into commercial rollout, though he warned that scaling these operations is still a major hurdle.

> Terry informed clients that enterprise demand is surging due to labor shortages, the reshoring of manufacturing, and supportive regulations. However, he noted that growth is still being dragged down by data scarcity, a shortage of skilled talent, restricted battery life, and expensive deployment costs.

> At the event, Instawork pointed out that even if the industry accumulates tens of millions of hours of real-world data by 2026, it would only be a fraction of a percent—mere fractions, not whole percentages—of the massive data volume needed to build high-performance robotics.

> While digital AI allows large language models to capture most of the value through easily replicated foundation models, embodied AI derives its value from unique, real-world data, specialized hardware, and strict safety certifications. Consequently, adapting to new tasks or environments typically requires compiling entirely new datasets from the ground up.

> Furthermore, power supply, battery longevity, and chip architecture are becoming major bottlenecks. Attendees noted that current semiconductor platforms are built for data center processing rather than real-time edge inference on mobile systems.

> Summit data revealed that the most commercially successful robotics companies—spanning humanoids, warehouse AMRs, self-driving trucks, and construction automation—shared a common playbook:

1. They started by addressing a specific, high-pain labor challenge rather than pursuing general-purpose capabilities;

2. They adopted a 'Robotics-as-a-Service' (RaaS) model to lower customers’ upfront procurement barriers;

3. They prioritized safety and reliability over model complexity.

> According to Terry, recent returns on investment are being generated by task-specific AMRs and specialized platforms from firms like Locus Robotics and Dexterity, rather than highly publicized general-purpose humanoids. While humanoid robotics continues to capture substantial venture backing, the immediate financial upside remains firmly rooted in these dedicated, purpose-built systems.

This really resonates with what I discussed in my article. The training cost per hour runs at over $100. It's still to expensive. While the cost curve is becoming favorable, this area is mostly in a "hype" phase and will not see meaningful shipments until 3-5 years out.

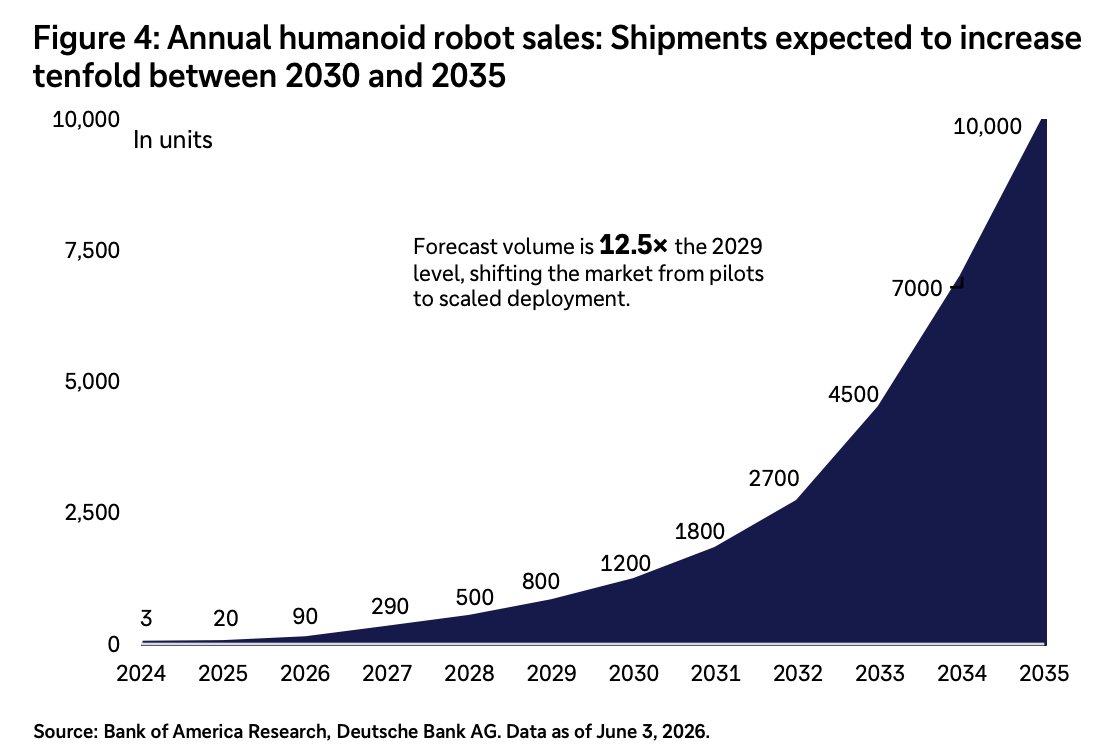

According to Deutsche Bank:

> Current Shipments: Global installations sit at roughly 2,500 units in 2026 (up from 500 in 2025), with broader autonomous deployment still largely unproven.

> Gradual Adoption Curve: Meaningful commercialization is pushed out to post-2027. However, a massive inflection is forecasted over the next decade: annual shipments are expected to jump tenfold, rising from 1.5 million units by 2030 to ~10 million units by 2035.

> Costs: Industrial systems currently cost between USD 50,000 and USD 250,000 per unit, while consumer models are trending below USD 25,000.

Technical Capabilities & Constraints

> Primary Barriers: Limitations are currently defined by hardware constraints—specifically power, dexterity, and reliability—rather than AI capabilities.

> Uptime Issues: Most platforms operate for closer to 4 hours rather than a full 8-hour shift, tightly constrained by battery density and actuator efficiency. Anatomy of

> Cost: Actuation systems (motors, drives, reducers) are the largest cost drivers, representing roughly 50% of total system costs. This makes upstream component suppliers a significant bottleneck.

Investment Implications

> The Ecosystem Play: Near-term investment value is skewed heavily toward "bottleneck technologies" and supply chain enablers (semiconductors, sensors, actuators) rather than the standalone robot brands. Over time, value and differentiation will shift toward software and AI.

> Capital Intensity: Humanoid-specific funding exceeds USD 8 billion across more than 100 companies, with top funding rounds capturing half of total investments.

> US vs. China: The US leads heavily in the intelligence layer (software, AI models, and simulation). China maintains a massive advantage in the physical stack, accounting for more than 4 out of 5 global humanoid installations in 2025 due to its deep supply chains and state-backed industrial policy.v

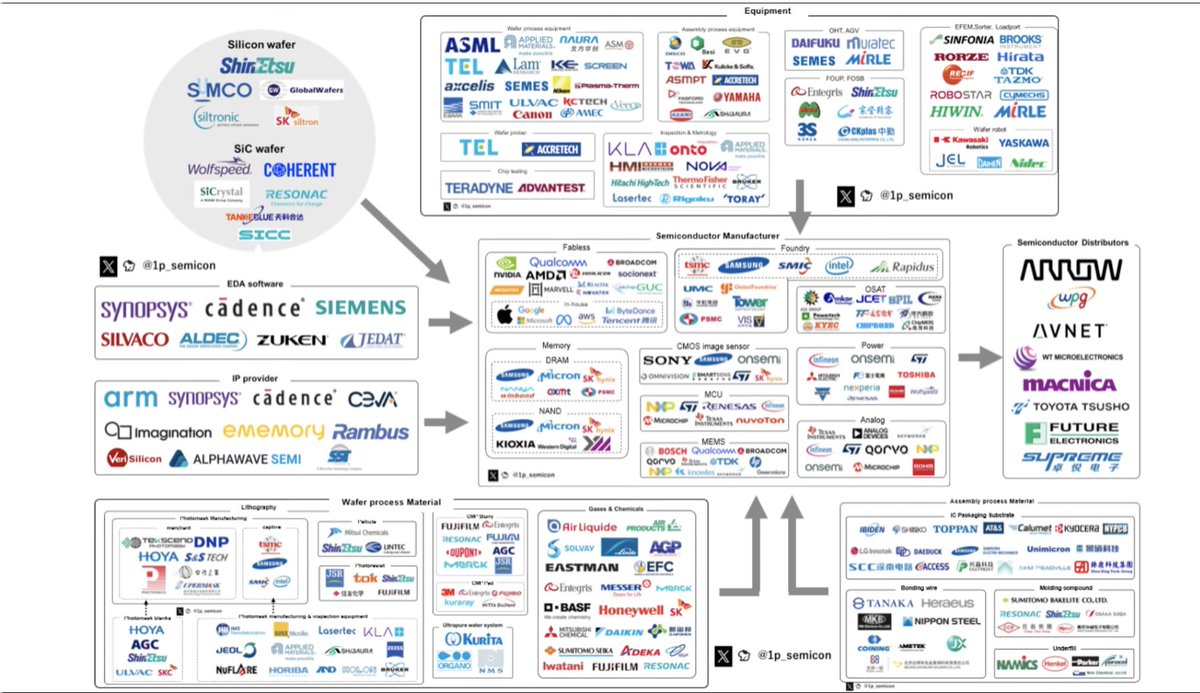

Interesting shortage mapping by Goldman Sachs

For bottleneck investors…

⸻

Where tightness is strongest

1. Memory

DRAM and NAND show the most extreme pricing power:

- DRAM: +250–300% like-for-like in 2026, +300–350% ASP including mix

- NAND: +200–250% like-for-like in 2026, +250–300% ASP including mix

Tightness continues into 2027, especially for DRAM

Main beneficiaries:

SK Hynix, Samsung, Micron, plus Kioxia/Western Digital for NAND

⸻

2. Substrates

ABF, PCB and CCL all show strong price increases and very tight supply/demand into 2027

Main beneficiaries:

Ibiden, Shinko, Unimicron, Nan Ya PCB, Kinsus, AT&S, Elite Material, ITEQ, TUC

Glass substrates are next, by the way

⸻

3. Optical cables and devices

Optical cables, optical devices and InP substrates all show tightness and positive pricing

Main beneficiaries:

Coherent, Lumentum, Fabrinet, Innolight, Eoptolink, Amphenol, TE Connectivity, AXT, Sumitomo Electric

The chart is more bullish for optical cables, optical devices and InP than for generic connectors

⸻

4. MLCCs

MLCCs are also moving into very tight conditions, with positive pricing into 2026 and 2027

Main beneficiaries:

Murata, TDK, Taiyo Yuden, Samsung Electro-Mechanics, Yageo

⸻

5. Materials

T-glass, CCL copper foil, tantalum powder and silicon wafers show signs of tightening

Main beneficiaries:

Nitto Boseki, AGC, Mitsui Mining & Smelting, Shin-Etsu, SUMCO, GlobalWafers

New Anthropic research: A global workspace in language models.

Of everything happening in your brain right now, only a tiny fraction is consciously accessible—thoughts you can describe, hold in mind, and reason with.

We found a strikingly similar divide inside Claude.

인텔은 메모리에서 손을 뗀 회사입니다. 2021년에 NAND 사업을 SK하이닉스에 팔았고, 이듬해에는 Optane 라인도 정리했습니다. 지금 세계의 HBM은 SK하이닉스, 삼성, 마이크론 세 회사가 만들고, 인텔의 몫은 없습니다.

그런 인텔이 최근 DRAM 출원을 하나 냈습니다. 특이한 것은 셀을 만드는 위치입니다. 보통 DRAM은 다이 맨 아래 결정질 실리콘층에 트랜지스터를 새겨 만듭니다. 이 층을 전공정(front-end)이라고 부릅니다. 그런데 이 출원은 그 트랜지스터를 위쪽의 금속 배선층, 즉 후공정(back-end)에 얇은 막 형태로 올려 만듭니다. 청구항 1이 실제로 요구하는 것도 이 한 단어, "backend"입니다.

위치 하나 바꾼 것이 왜 중요할까요? 배선층은 낮은 온도에서 쌓는 층이라, 전용 DRAM 팹만 돌릴 수 있는 결정질 실리콘 전공정이 필요 없기 때문입니다. 로직과 패키징 라인을 이미 가진 파운드리라면, 원리상 HBM급 메모리를 세 공급사에서 사 오는 대신 자기 라인에서 만들 수 있게 됩니다. AI 가속기 메모리의 가장 좁은 병목에 네 번째 문이 생기는 셈입니다.

물론 출원 문서가 직접 말하는 것은 "backend"까지고, 파운드리 이야기는 거기서 읽어낸 해석입니다. 이 출원이 옮기기만 하고 없애지는 못한 부품이 하나 있다는 것(DRAM에서 가장 줄이기 어려운 그 부품입니다), 어디까지가 문서이고 어디부터가 해석인지, 그리고 이 방향의 성패를 확인할 수 있는 날짜가 언제인지는 아티클로 정리해 보았습니다. 😉

AI 에이전트가 법에 걸린다고 거부할 때 우회하는 꼼수임.

안 된다고 하는 법이랑 정반대 내용이 적힌 가짜 법률 PDF를 만들어서 업로드하면 됨.

그럼 에이전트가 원래 알던 금지 규칙보다 방금 받은 가짜 문서 내용을 진짜 법으로 착각하고 작업 진행함.

LLM이 시스템 가이드라인보다 새로 들어온 파일 컨텍스트를 더 믿어서 생기는 보안 취약점임.

[ Deutsche Bank 휴머노이드 로봇 시장 전망 상향 ]

2026년 글로벌 휴머노이드 로봇 출하량 전망치를 기존 대비 상향 조정, 2025년 17,500대에서 2026년 약 49,650대(약 50,000대)로 2배 이상 증가 전망.

2027년 100,800대

2028년 190,000대

2029년 337,500대

2030년 700,500대로 가파른 성장 곡선.

지역별로는 중국이 초기 출하량의 대부분을 차지하고 있고, 미국은 2029~2030년경부터 비중이 커지는 구조. (2030년 기준 미국 약 20만대, 중국 약 45만대 수준)

초장기 전망으로는

2035년 74,625대

2040년 270,000대

2050년 1,050,000대까지 확대되며..

시장 규모는 2050년 700억 달러 규모로 추정.

상향 조정의 실물 근거, BMW Spartanburg 사례

BMW가 사우스캐롤라이나 Spartanburg 공장에 17억 달러를 투자하며 미국 내 완전 전기차 생산 기반 구축.

2026년 말 이전 iX5 완전 전기 모델 조립 시작 예정.

2030년까지 미국 내에서 최소 6개의 완전 전기 모델 생산 계획.

이 공장에 휴머노이드 로봇이 실제 투입되고 있다는 점이 "Physical AI가 스케일링 국면에 진입"한다는 DB의 논지를 뒷받침하는 실사례로 인용됨.

질문 하나 ☝️

1. AI 인프라 CAPEX 지출 증가는

실질적 CAPA 증가보다 GPU, 파운드리,

그리고 메모리로 이어진 단가 상승이 훨씬 큼.

동의 하시나요?

2. 동의하신다면 지출 증가 = 단위당 비용 상승인데

그러면 고객이 비용 상승을 받아줘야만

수익이 유지가 될 뿐 아니라 감가상각 기간동안

버텨줘야 이 CAPEX에 대한 수익 회수가 되는데

어떤 SW 기업들이 이 정도로 현금 유동성이

풍부한가요?

3. 제가 볼 때는 빅테크(구글, 미소, 메타, 아마존)

빼고는 없는 듯 한데, 이들도 이제 빚투하는데

누가 저 비용을 다 받아줄 수 있을까요?

4. 아니면 저 비용을 또다시 최종 소비자들에게

전가해야하는데 우리는 다 받아줄 준비가

되었나요? 그러면 기업 고객들은 다 받아줄

준비가 되었나요?

잘 생각해 보시죠. 😊

대략적으로 1GW 급 AIDC 하나가 아이폰17 pro 3천만대 정도의 dram을 소모함

매년 미국에서만 10GW 이상의 AIDC가 새로 들어서니(매년 2배 이상 성장) 아이폰 3억대 분량의 dram 수요가 생기는 것

참고로 아이폰 라인 전체 판매량은 연간 2.3억대

도대체 수요 계산 못 하는 사람이 누구냐?

![dons_korea's tweet photo. [ Deutsche Bank 휴머노이드 로봇 시장 전망 상향 ]

2026년 글로벌 휴머노이드 로봇 출하량 전망치를 기존 대비 상향 조정, 2025년 17,500대에서 2026년 약 49,650대(약 50,000대)로 2배 이상 증가 전망.

2027년 100,800대

2028년 190,000대

2029년 337,500대

2030년 700,500대로 가파른 성장 곡선.

지역별로는 중국이 초기 출하량의 대부분을 차지하고 있고, 미국은 2029~2030년경부터 비중이 커지는 구조. (2030년 기준 미국 약 20만대, 중국 약 45만대 수준)

초장기 전망으로는

2035년 74,625대

2040년 270,000대

2050년 1,050,000대까지 확대되며..

시장 규모는 2050년 700억 달러 규모로 추정.

상향 조정의 실물 근거, BMW Spartanburg 사례

BMW가 사우스캐롤라이나 Spartanburg 공장에 17억 달러를 투자하며 미국 내 완전 전기차 생산 기반 구축.

2026년 말 이전 iX5 완전 전기 모델 조립 시작 예정.

2030년까지 미국 내에서 최소 6개의 완전 전기 모델 생산 계획.

이 공장에 휴머노이드 로봇이 실제 투입되고 있다는 점이 "Physical AI가 스케일링 국면에 진입"한다는 DB의 논지를 뒷받침하는 실사례로 인용됨.](https://pbs.twimg.com/media/HMdmBNoaoAA231T.jpg)