The Same AI Engine is Firing the Workers and Funding the S&P Rally.

Today's Jobs Number Is the Last Screen You Should Be Watching.

In a few hours the BLS prints the May jobs report. Consensus: 85,000 to 105,000 jobs, unemployment holding at 4.3%. The tape will lurch, the headlines will write themselves... and almost all of it is noise.

The number that actually matters is buried elsewhere: the $725 billion four companies are spending on AI this year, up 77%, the same flood of capital powering the S&P to records while quietly removing the bottom rung of the career ladder. One engine, both jobs at once.

👉 Watch the print if you care about the next two hours. Watch the engine if you care about the next two years. One is a data release. The other is a regime change.

🔹The calm surface, the rotting interior🔹

The headline will say soft landing: 4.3%, steady for months, a modest gain. Underneath, the rot.

▫️ Hiring froze and firing froze with it.

The payroll growth that exists comes from people not being let go, not from people being hired.

▫️ The real trend is near 21,000 jobs a month...

So even an in line 100,000 print is flattered by revisions and noise.

▫️ Claims ticked up to 225,000. Openings sit near a five year low.

A market holding its breath, and frozen markets thaw in one direction far faster than the other.

🔹The bottom rung is being sawn off🔹

This is the part the headline rate hides, and it is the most human number in the report.

For the first time in memory, recent graduates have higher unemployment than the overall workforce.

🔎Stanford's payroll microdata shows workers aged 22 to 25 in the most AI exposed jobs, software, marketing, customer service, down roughly 16% in relative employment since late 2022, young developers closer to 20%.

👉 The ladder still stands while someone saws off its first rung. Challenger logged 38,579 AI attributed layoffs in May, about 40% of all cuts, a record.

✋ The honest counter: claims have not exploded, Goldman pegs the net AI drag at only about 16,000 jobs a month, and some CEOs are "AI washing" ordinary cuts.

👉 The aggregate is still small. That is the point.

A surgical force aimed at the entry point of white collar work compounds faster than a broad recession ever shows up in a headline.

🔹Why the Fed cannot fix it this time🔹

I wrote in May about Warsh inheriting the Burns Trap. This is that trap with a worse floor.

▫️Funds rate stuck at 3.50 to 3.75%.

▫️April CPI at 3.8%, the hottest since mid 2023.

▫️Four dissents last meeting, the most since 1992.

👉 The market prices near zero cuts for all of 2026.

▫️Doves see cooling labor and want a cut.

▫️Hawks see 3.8% inflation and refuse.

👉Both miss the deeper problem: the softness is partly structural, AI removing roles, not a weak economy shedding them.

➡️ A rate cut cannot rehire a 23 year old whose task got automated. It can only pour liquidity into an inflation impulse energy is already feeding.

👉One blade of the scissors ignores cheaper money, the other sharpens on it, which is why higher for longer stopped being a forecast and became the structure.

🔹The reflexive loop🔹

The same $725 billion AI capex hollowing out entry level work is the primary bid under the equity market.

Microsoft $MSFT, Google $GOOG, Amazon $AMZN, and Meta $META are spending more on AI than almost anything else in the economy, and Zuckerberg said outright that Meta's roughly 8,000 cuts were a direct consequence of that spend.

Labor weakness and equity strength, produced by one machine, holding until either the inflation forces real tightening or the low fire half of the labor market snaps.

🔹Actionable Opinion for Wise Investors🔹

Today, I will not trade the headline direction.

The revisions and the unemployment rate carry more signal than the print.

▫️ NFP in line: 85 to 105k, 4.3%:

Muted the June hold is locked, the melt up survives. Watch the revisions.

▫️ Hot NFP: above 130k, or rate down:

Hawkish. Dollar up, gold and Treasurys down, the overbought tape gets a "no cuts" wobble.

▫️ Weak NFP: below 50k, or rate to 4.4%+:

Not clean risk on. Against 3.8% inflation it reads as stagflation, not stimulus. Gold wins both halves.

Structurally:

1️⃣ Long the capex, compute and power.

That $725 billion is the most bankable spend in the market. Semis via ( $NVDA ) and ( $SMH ), plus the grid names feeding the data centers. But RSI 73 is froth, so scale in on pullbacks.

2️⃣ Underweight businesses whose moat is entry level human labor in AI exposed services. That is where the Stanford bleed is real and unpriced.

3️⃣ Robotics is a 2028 to 2030 venture theme. Own the deployment curve, not 2026 multiples for 2030 revenue.

4️⃣ Gold ( $GLD ) is the cleanest expression of the regime, bid by both a weak print and the energy plus policy trap underneath. Keep duration short.

🔹 The takeaway 🔹

The labor market is cooling under a calm 4.3% surface, AI is a real but surgical driver aimed at the youngest, and the decisive variable is not the drag itself but where it lands: on top of an energy inflation that already stripped the Fed of its cushion.

A cooling labor market that would normally buy rate relief buys none this time, because the tool no longer fits the problem.

The market will spend the morning pricing a number that changes almost nothing, while the engine writing the real story never clocks in at 8:30.

The same machine is firing the juniors and funding the rally, and rate cuts cannot touch either end of it.

👉 As usual: Watch the number and the headlines if you want the morning. Watch the engine if you want the decade...

What about you wise investors?

Which scenario are you positioned for into the print? 👇

@Cointelegraph FYI: Coinbase and Circle's USDC revenue share comes up for renewal in August.

Coinbase exploring equity in a consortium built to compete with USDC, weeks before that renewal, is the real story here.

👉 The distributor is shopping for leverage over the issuer.

As debate continues over AI’s true impact on the labor force, OpenAI CEO Sam Altman said some companies are engaging in “AI washing” when it comes to layoffs, or falsely attributing workforce reductions to the technology’s impact. https://t.co/mnNx1Z9cgE

The Same AI Engine is Firing the Workers and Funding the S&P Rally.

Today's Jobs Number Is the Last Screen You Should Be Watching.

In a few hours the BLS prints the May jobs report. Consensus: 85,000 to 105,000 jobs, unemployment holding at 4.3%. The tape will lurch, the headlines will write themselves... and almost all of it is noise.

The number that actually matters is buried elsewhere: the $725 billion four companies are spending on AI this year, up 77%, the same flood of capital powering the S&P to records while quietly removing the bottom rung of the career ladder. One engine, both jobs at once.

👉 Watch the print if you care about the next two hours. Watch the engine if you care about the next two years. One is a data release. The other is a regime change.

🔹The calm surface, the rotting interior🔹

The headline will say soft landing: 4.3%, steady for months, a modest gain. Underneath, the rot.

▫️ Hiring froze and firing froze with it.

The payroll growth that exists comes from people not being let go, not from people being hired.

▫️ The real trend is near 21,000 jobs a month...

So even an in line 100,000 print is flattered by revisions and noise.

▫️ Claims ticked up to 225,000. Openings sit near a five year low.

A market holding its breath, and frozen markets thaw in one direction far faster than the other.

🔹The bottom rung is being sawn off🔹

This is the part the headline rate hides, and it is the most human number in the report.

For the first time in memory, recent graduates have higher unemployment than the overall workforce.

🔎Stanford's payroll microdata shows workers aged 22 to 25 in the most AI exposed jobs, software, marketing, customer service, down roughly 16% in relative employment since late 2022, young developers closer to 20%.

👉 The ladder still stands while someone saws off its first rung. Challenger logged 38,579 AI attributed layoffs in May, about 40% of all cuts, a record.

✋ The honest counter: claims have not exploded, Goldman pegs the net AI drag at only about 16,000 jobs a month, and some CEOs are "AI washing" ordinary cuts.

👉 The aggregate is still small. That is the point.

A surgical force aimed at the entry point of white collar work compounds faster than a broad recession ever shows up in a headline.

🔹Why the Fed cannot fix it this time🔹

I wrote in May about Warsh inheriting the Burns Trap. This is that trap with a worse floor.

▫️Funds rate stuck at 3.50 to 3.75%.

▫️April CPI at 3.8%, the hottest since mid 2023.

▫️Four dissents last meeting, the most since 1992.

👉 The market prices near zero cuts for all of 2026.

▫️Doves see cooling labor and want a cut.

▫️Hawks see 3.8% inflation and refuse.

👉Both miss the deeper problem: the softness is partly structural, AI removing roles, not a weak economy shedding them.

➡️ A rate cut cannot rehire a 23 year old whose task got automated. It can only pour liquidity into an inflation impulse energy is already feeding.

👉One blade of the scissors ignores cheaper money, the other sharpens on it, which is why higher for longer stopped being a forecast and became the structure.

🔹The reflexive loop🔹

The same $725 billion AI capex hollowing out entry level work is the primary bid under the equity market.

Microsoft $MSFT, Google $GOOG, Amazon $AMZN, and Meta $META are spending more on AI than almost anything else in the economy, and Zuckerberg said outright that Meta's roughly 8,000 cuts were a direct consequence of that spend.

Labor weakness and equity strength, produced by one machine, holding until either the inflation forces real tightening or the low fire half of the labor market snaps.

🔹Actionable Opinion for Wise Investors🔹

Today, I will not trade the headline direction.

The revisions and the unemployment rate carry more signal than the print.

▫️ NFP in line: 85 to 105k, 4.3%:

Muted the June hold is locked, the melt up survives. Watch the revisions.

▫️ Hot NFP: above 130k, or rate down:

Hawkish. Dollar up, gold and Treasurys down, the overbought tape gets a "no cuts" wobble.

▫️ Weak NFP: below 50k, or rate to 4.4%+:

Not clean risk on. Against 3.8% inflation it reads as stagflation, not stimulus. Gold wins both halves.

Structurally:

1️⃣ Long the capex, compute and power.

That $725 billion is the most bankable spend in the market. Semis via ( $NVDA ) and ( $SMH ), plus the grid names feeding the data centers. But RSI 73 is froth, so scale in on pullbacks.

2️⃣ Underweight businesses whose moat is entry level human labor in AI exposed services. That is where the Stanford bleed is real and unpriced.

3️⃣ Robotics is a 2028 to 2030 venture theme. Own the deployment curve, not 2026 multiples for 2030 revenue.

4️⃣ Gold ( $GLD ) is the cleanest expression of the regime, bid by both a weak print and the energy plus policy trap underneath. Keep duration short.

🔹 The takeaway 🔹

The labor market is cooling under a calm 4.3% surface, AI is a real but surgical driver aimed at the youngest, and the decisive variable is not the drag itself but where it lands: on top of an energy inflation that already stripped the Fed of its cushion.

A cooling labor market that would normally buy rate relief buys none this time, because the tool no longer fits the problem.

The market will spend the morning pricing a number that changes almost nothing, while the engine writing the real story never clocks in at 8:30.

The same machine is firing the juniors and funding the rally, and rate cuts cannot touch either end of it.

👉 As usual: Watch the number and the headlines if you want the morning. Watch the engine if you want the decade...

What about you wise investors?

Which scenario are you positioned for into the print? 👇

The question I cannot settle: is the AI layoff wave real, or are CEOs blaming AI for cuts they wanted to make anyway?..

Challenger says it is 40% of May cuts.

Altman calls it AI washing.

Both can be partly true. 🤷

What is your take? 👇

Good news or bad news, NFP is not really relevant anymore...

Previously, the Fed was cutting rates to print money to save jobs.

👉 Now, there are no more jobs to be saved because they have been replaced by AI agents.

We are living a proper change of paradigm in our economy.

Check my pinned post for the full details with all sources.

NEW: @JPMorgan, @Citi and @BankofAmerica are building a shared blockchain network to give bank deposits crypto-like speed and programmability in direct response to the stablecoin 'threat', targeting a mid-2027 launch.

@elerianm Volatility is incoming as usual for the day, but what at stakes here is much bigger than april's data...

With AI we are not reducing jobs, we are replacing them... No rate cute will ever fill these positions again.

This is a real change of paradigm

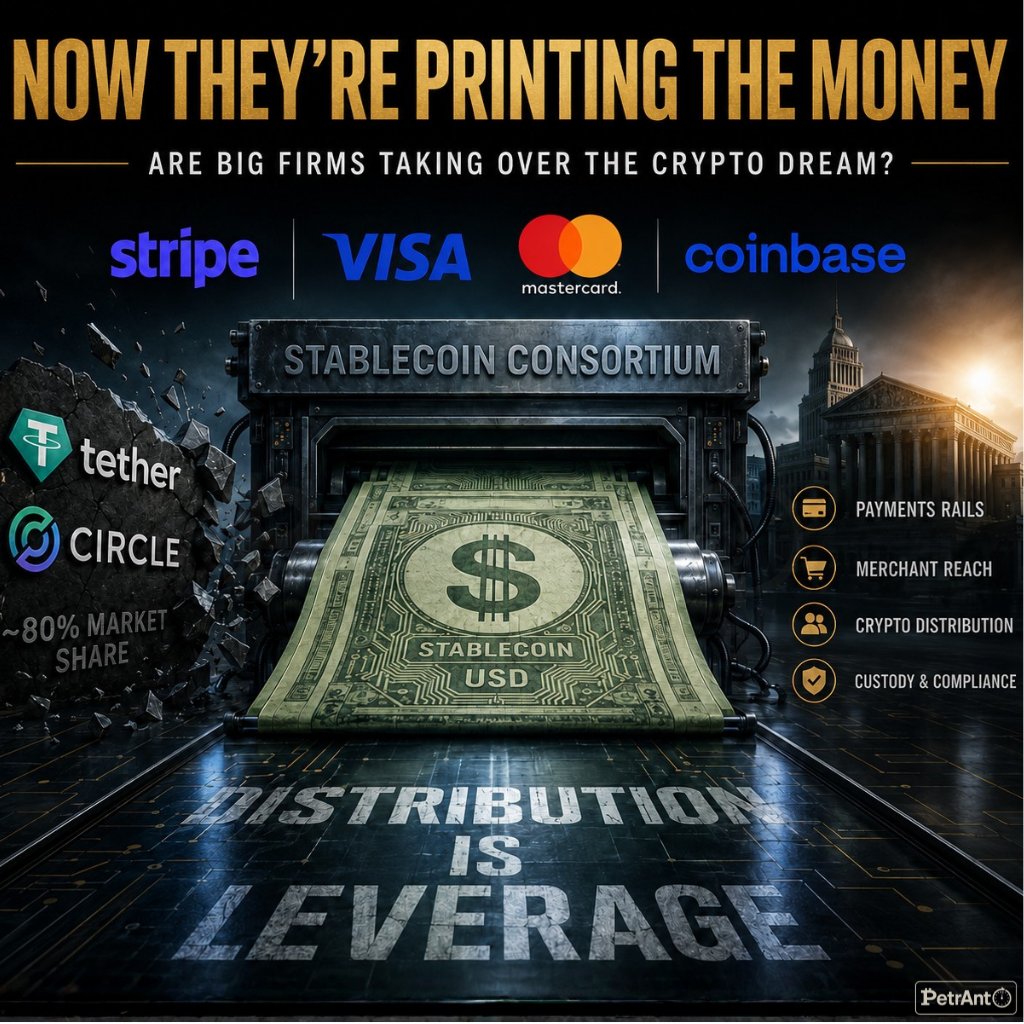

Now They're Printing the Money.

Are Big Firms Taking Over the Crypto Dream?

One day. That is how long it took to go from Mastercard settling other people's stablecoins to Stripe, Visa, Mastercard, and Coinbase reportedly forming a consortium to issue their own.

Yesterday I wrote: "You can't kill what you need", today, big firms just confirmed what they don't need any more...

Bitcoin is red on the day, but watch the hands, not the price. The CLARITY Act is stuck in the Senate on a single fight, whether stablecoin yield survives, and that yield is roughly 20% of Coinbase's revenue.

So Coinbase moving to help issue its own dollar reads less like a narrative play and more like a company getting ahead of the law before the law gets ahead of it.

Yesterday, credit card businesses were absorbing stablecoins rather than being killed by them, taking a fee on the rails the disruptors built. I did not expect the next move quite this fast. They are no longer content to own the road and charge a toll. They want to print the currency that drives on it.

👉 The two companies that make up roughly 80% of the stablecoin market, Tether and Circle, just watched the most powerful distribution alliance in payments announce it intends to compete with them directly. 👇

🔹What was actually reported🔹

Per The Information, with follow ups across CoinDesk and PYMNTS, the shape of it is this.

▫️ Stripe, Visa, and Mastercard are near launching a unified stablecoin platform, with Coinbase in talks to join, reportedly for an equity stake.

▫️ The explicit target is Circle's USDC and Tether's USDT, the two issuers that control about 80% of a $325 billion market.

▫️ Each member brings a different weapon.

Visa and Mastercard bring the card rails and 150 million plus acceptance points.

Stripe brings merchant reach and Bridge, the issuance infrastructure it bought in 2024.

Coinbase brings crypto distribution, custody, and compliance.

Put plainly, four companies are not dabbling here. They are assembling every layer a dollar needs to live on chain, issuance, settlement, merchant acceptance, and exchange liquidity, under one roof, aimed squarely at the incumbents who got there first.

🔹The knife nobody is pointing at🔹

Here is the detail that turns this from a partnership story into a betrayal story, and almost no one is saying it out loud.

Coinbase and Circle have been joined at the hip since 2023 through a revenue sharing deal on USDC. Coinbase keeps all the yield on USDC held on its platform and splits the rest fifty fifty. That agreement comes up for renewal this August.

So months before it has to re sign the deal that pays it hundreds of millions, Coinbase is reportedly exploring an equity stake in a consortium built to compete with the very coin that deal is based on.

➡️ Circle's single most important distribution partner is shopping for a way to own the competitor instead of renting from the issuer. Circle stock slipped on the news, and that is the market starting to price what this means: the company everyone crowned as the regulated winner of the stablecoin race is suddenly the one most exposed to being disintermediated by its own allies.

👉 Distribution is leverage, and Coinbase just reminded Circle who actually holds it.

🔹Why distribution eats the issuer🔹

This is the lesson the whole week has been building toward, and the consortium makes it impossible to ignore.

A stablecoin is trivial to mint. 🤷

The hard part, the only part that matters, is getting it into hands and making it spendable:

- Circle solved that by renting Coinbase's distribution.

- Tether solved it offshore through exchanges.

Both are, underneath the branding, issuers dependent on someone else's reach.

Now look at who just teamed up. 👀

1⃣ Card networks that touch nearly every merchant on earth.

2⃣ A payments platform embedded in millions of businesses.

3⃣ An exchange with tens of millions of funded accounts.

They already own the distribution that USDC and USDT have to rent. Adding their own coin on top costs them almost nothing and lets them keep the issuance economics they currently hand to Circle.

👉 When the distributor decides to issue, the independent issuer becomes a middleman it no longer needs. That is the existential threat here. The consortium does not have to make a better stablecoin. It only has to make a good enough one and put it where it already controls the shelf.

🔹The part that should bother the crypto believers🔹

Step back from the tickers and the irony gets heavy.

Stablecoins were sold as the open, permissionless dollar that routed around the gatekeepers.

What is forming instead is an oligopoly, three of the largest payment companies on earth plus the biggest US exchange, proposing to issue the dollar, settle the dollar, accept the dollar, and clear the dollar, all within one alliance.

Call it what it is, the existing financial cartel re forming on faster rails, with a blockchain underneath for efficiency rather than for freedom.

👉 The technology delivered everything it promised. Cheaper, faster, programmable dollars. It just handed all of it to the same handful of institutions that ran the old system, and gave them a new layer to consolidate.

🔹Actionable Advice for Wise Investors🔹

1️⃣ Reprice Circle ( $CRCL ) on distribution risk, not adoption hype.

The bull case was always that USDC is the regulated, institutional dollar. The consortium attacks the one thing that case quietly depended on, Coinbase's distribution and the August revenue share renewal.

👉 Watch that renewal like a hawk. The terms Coinbase demands, or whether it walks, will tell you more about Circle's future than any supply chart.

2️⃣ The card networks keep being the trade, not the victim.

Visa ( $V ) and Mastercard ( $MA ) spent a cycle priced for disruption. In one week they have moved from settling stablecoins to issuing them. They are converting every phase of the stablecoin build into a fee line they collect.

👉 Keep reading them as the consolidators, because that is how they keep behaving.

3️⃣ Coinbase ( $COIN ) is the swing factor, and the most interesting name here.

If it joins, it trades a revenue share check from Circle for equity in the platform meant to replace Circle.

👉 That is a structurally better position. The risk is execution and antitrust attention on a four way payments alliance, but the strategic logic is sound, and the optionality is real.

4️⃣ And (again) the conclusion only sharpens towards Bitcoin if you still want to believe in crypto.

Every layer of this, issuance, settlement, distribution, is one more place the dollar gets owned and gated by a shrinking club.

The more the on chain dollar consolidates into a cartel, the cleaner the case for the asset with no consortium, no issuer, and no shelf to control.

👉 Bitcoin ( $BTC ) very much like gold ( $GLD ) is the hedge against exactly this, the financialization of the exit itself.

🔹The (stable) Takeaway🔹

For two years the story was that stablecoins would disrupt traditional finance. This week (definitely) wrote the ending.

Traditional finance looked at the disruptor, decided it was a good idea, and is now building its own, on its own rails, with its own coin, behind its own walls.

👉 Circle taught the giants that a branded dollar was worth issuing... The giants thanked it by deciding they would rather issue their own.

@br9ay let's say they have all they need to keep Circle quiet and disciplined...

and I don't think they will allow Circle keeping today's profit margin for long

Now They're Printing the Money.

Are Big Firms Taking Over the Crypto Dream?

One day. That is how long it took to go from Mastercard settling other people's stablecoins to Stripe, Visa, Mastercard, and Coinbase reportedly forming a consortium to issue their own.

Yesterday I wrote: "You can't kill what you need", today, big firms just confirmed what they don't need any more...

Bitcoin is red on the day, but watch the hands, not the price. The CLARITY Act is stuck in the Senate on a single fight, whether stablecoin yield survives, and that yield is roughly 20% of Coinbase's revenue.

So Coinbase moving to help issue its own dollar reads less like a narrative play and more like a company getting ahead of the law before the law gets ahead of it.

Yesterday, credit card businesses were absorbing stablecoins rather than being killed by them, taking a fee on the rails the disruptors built. I did not expect the next move quite this fast. They are no longer content to own the road and charge a toll. They want to print the currency that drives on it.

👉 The two companies that make up roughly 80% of the stablecoin market, Tether and Circle, just watched the most powerful distribution alliance in payments announce it intends to compete with them directly. 👇

🔹What was actually reported🔹

Per The Information, with follow ups across CoinDesk and PYMNTS, the shape of it is this.

▫️ Stripe, Visa, and Mastercard are near launching a unified stablecoin platform, with Coinbase in talks to join, reportedly for an equity stake.

▫️ The explicit target is Circle's USDC and Tether's USDT, the two issuers that control about 80% of a $325 billion market.

▫️ Each member brings a different weapon.

Visa and Mastercard bring the card rails and 150 million plus acceptance points.

Stripe brings merchant reach and Bridge, the issuance infrastructure it bought in 2024.

Coinbase brings crypto distribution, custody, and compliance.

Put plainly, four companies are not dabbling here. They are assembling every layer a dollar needs to live on chain, issuance, settlement, merchant acceptance, and exchange liquidity, under one roof, aimed squarely at the incumbents who got there first.

🔹The knife nobody is pointing at🔹

Here is the detail that turns this from a partnership story into a betrayal story, and almost no one is saying it out loud.

Coinbase and Circle have been joined at the hip since 2023 through a revenue sharing deal on USDC. Coinbase keeps all the yield on USDC held on its platform and splits the rest fifty fifty. That agreement comes up for renewal this August.

So months before it has to re sign the deal that pays it hundreds of millions, Coinbase is reportedly exploring an equity stake in a consortium built to compete with the very coin that deal is based on.

➡️ Circle's single most important distribution partner is shopping for a way to own the competitor instead of renting from the issuer. Circle stock slipped on the news, and that is the market starting to price what this means: the company everyone crowned as the regulated winner of the stablecoin race is suddenly the one most exposed to being disintermediated by its own allies.

👉 Distribution is leverage, and Coinbase just reminded Circle who actually holds it.

🔹Why distribution eats the issuer🔹

This is the lesson the whole week has been building toward, and the consortium makes it impossible to ignore.

A stablecoin is trivial to mint. 🤷

The hard part, the only part that matters, is getting it into hands and making it spendable:

- Circle solved that by renting Coinbase's distribution.

- Tether solved it offshore through exchanges.

Both are, underneath the branding, issuers dependent on someone else's reach.

Now look at who just teamed up. 👀

1⃣ Card networks that touch nearly every merchant on earth.

2⃣ A payments platform embedded in millions of businesses.

3⃣ An exchange with tens of millions of funded accounts.

They already own the distribution that USDC and USDT have to rent. Adding their own coin on top costs them almost nothing and lets them keep the issuance economics they currently hand to Circle.

👉 When the distributor decides to issue, the independent issuer becomes a middleman it no longer needs. That is the existential threat here. The consortium does not have to make a better stablecoin. It only has to make a good enough one and put it where it already controls the shelf.

🔹The part that should bother the crypto believers🔹

Step back from the tickers and the irony gets heavy.

Stablecoins were sold as the open, permissionless dollar that routed around the gatekeepers.

What is forming instead is an oligopoly, three of the largest payment companies on earth plus the biggest US exchange, proposing to issue the dollar, settle the dollar, accept the dollar, and clear the dollar, all within one alliance.

Call it what it is, the existing financial cartel re forming on faster rails, with a blockchain underneath for efficiency rather than for freedom.

👉 The technology delivered everything it promised. Cheaper, faster, programmable dollars. It just handed all of it to the same handful of institutions that ran the old system, and gave them a new layer to consolidate.

🔹Actionable Advice for Wise Investors🔹

1️⃣ Reprice Circle ( $CRCL ) on distribution risk, not adoption hype.

The bull case was always that USDC is the regulated, institutional dollar. The consortium attacks the one thing that case quietly depended on, Coinbase's distribution and the August revenue share renewal.

👉 Watch that renewal like a hawk. The terms Coinbase demands, or whether it walks, will tell you more about Circle's future than any supply chart.

2️⃣ The card networks keep being the trade, not the victim.

Visa ( $V ) and Mastercard ( $MA ) spent a cycle priced for disruption. In one week they have moved from settling stablecoins to issuing them. They are converting every phase of the stablecoin build into a fee line they collect.

👉 Keep reading them as the consolidators, because that is how they keep behaving.

3️⃣ Coinbase ( $COIN ) is the swing factor, and the most interesting name here.

If it joins, it trades a revenue share check from Circle for equity in the platform meant to replace Circle.

👉 That is a structurally better position. The risk is execution and antitrust attention on a four way payments alliance, but the strategic logic is sound, and the optionality is real.

4️⃣ And (again) the conclusion only sharpens towards Bitcoin if you still want to believe in crypto.

Every layer of this, issuance, settlement, distribution, is one more place the dollar gets owned and gated by a shrinking club.

The more the on chain dollar consolidates into a cartel, the cleaner the case for the asset with no consortium, no issuer, and no shelf to control.

👉 Bitcoin ( $BTC ) very much like gold ( $GLD ) is the hedge against exactly this, the financialization of the exit itself.

🔹The (stable) Takeaway🔹

For two years the story was that stablecoins would disrupt traditional finance. This week (definitely) wrote the ending.

Traditional finance looked at the disruptor, decided it was a good idea, and is now building its own, on its own rails, with its own coin, behind its own walls.

👉 Circle taught the giants that a branded dollar was worth issuing... The giants thanked it by deciding they would rather issue their own.

1976 Burns vs 2026 Warsh - Why Warsh Inherits the One Configuration No Fed Chair Can Survive Cleanly

This morning the Fed's preferred inflation gauge printed 3.8% - the hottest since May 2023 - and core PCE hit 3.3%, the highest since October 2023.

But the number nobody put in the headline is the one that matters: the effective funds rate sits near 3.58%, inside a 3.50–3.75% target.

👉 Headline inflation is now running above the policy rate. The real policy rate just went negative again.

That is the whole story in a single line.

The Fed cut three times into the back half of 2025, held through 2026 so far, and is now easing - in real terms - straight into a re-accelerating inflation impulse driven by the Hormuz oil shock.

I have argued for two years that we were heading into a regime change. We are now living in it... And the man who has to navigate it spent the last decade warning anyone who would listen about exactly this trap.

🔹The projections are already obsolete 🔹

Read the Fed's March Summary of Economic Projections (SEP) and you see a central bank that did not see this coming. The median dot penciled in one more 25bp cut for 2026 and one for 2027.

Participants saw PCE cooling to 2.7% by December 2026. We are in April - eight months early - and the print is 3.8%.

➡️ The Fed's own year-end forecast has been overshot by more than a full point before the summer has even started.

When the June 16–17 meeting arrives, the dots will not be revised - they will be rebuilt.

The easing bias that has anchored every rally in rate-sensitive assets since last autumn is about to be quietly euthanized.

➡️ Watch the 2026 median: if it moves to zero cuts, that is a signal. If a single dot starts pricing a hike, the regime change has become official policy.

🔹 Enter Warsh - the hawk hired to cut 🔹

Kevin Warsh was sworn in on May 22.

Understand the paradox I laid out in my post (The Warsh Paradox) back in February: on the record, he is the most hawkish chair in a generation. He spent years attacking QE, demanding faster balance-sheet runoff, calling for a narrower mandate and - his words, not mine - "regime change" at the central bank...

But he is also a Trump appointee, installed by a president who has been screaming for rapid cuts and who told a rally crowd the day Warsh took the oath that rates would come down "very quickly."

So the new chair walks in with a mandate from his patron that is the precise opposite of his own stated convictions, at the exact moment inflation turns back up.

He cannot deliver fast cuts without torching the credibility he built a career on.

He cannot hold firm without defying the man who gave him the job, and...

He does not even have a clean board - Powell stayed on as a governor with a vote, alongside an institutionalist bloc already nervous about easing with inflation above target and rising.

🔹 The stagflation vise makes it worse 🔹

Here is the cruel part.

Q1 GDP was just revised down to 1.6% annualized. Unemployment is drifting toward the Fed's 4.4% projection. Growth is softening while inflation accelerates - the textbook stagflationary bind.

Warsh cannot even lean on a red-hot labor market to justify a hold. He has to tighten the message into slowing growth, which is the single hardest political position a chair can occupy: defending price stability while the other half of the dual mandate visibly deteriorates and the White House points at every weak data point as proof he should cut.

🔹We have seen this movie before... and it does not end well 🔹

This is what should keep every macro investor up at night.

The configuration we have today is not new. It is 1976:

▫️ Oil-driven inflation spike,

▫️ Fed running negative real rates,

▫️ A chair under intense political pressure to keep policy loose.

Arthur Burns eased after the first oil-shock wave crested in 1974.

Inflation obligingly fell from ~12% toward 5% by 1976, and the Fed - with Nixon's thumb on the scale - kept real rates low rather than finishing the job.

The second wave came anyway.

CPI ran back to 14.6% by 1980, and it took Volcker, 20% funds rates and two recessions to break it.

➡️ The lesson of the Great Inflation was never that the Fed failed to hike. It was that the Fed cut too early, declared victory at 5%, and let a supply shock metastasize into an expectations problem.

The cleaner, more recent rhyme is 1998:

The Fed cut 75bp as insurance against LTCM and Russia, the cuts proved premature, and it spent 1999–2000 hiking to 6.5% - straight into the dot-com top.

➡️ Premature easing is rarely free. It is borrowed, and the bond market always collects with interest.

🔹 Actionable Advice for Wise Investors 🔹

I do not think Warsh cuts in June.

I think his first act is a hawkish hold dressed as data-dependence, an SEP that drops the easing bias, and - watch this closely - a signal on accelerating the balance-sheet runoff.

QT is his tell. It lets him tighten financial conditions while leaving the headline funds rate untouched: precisely the move a chair makes when he wants to fight inflation without publicly humiliating the president who hired him.

The risk case is the one that matters for portfolios.

If political pressure wins and he cuts into a 3.8% print, he does not become the dove Trump wants - he becomes Burns.

The long end will not cooperate. You would see the curve bear-steepen, 10s grind back toward 4.8–5%, the dollar wobble on credibility rather than rate differentials, and gold ( $GLD ) and bitcoin ( $BTC ) do what they always do when the market stops trusting the central bank's spine...

Either way, the era of the Fed put on "meeting by meeting" autopilot is over.

Warsh knows the Burns story cold. The only question left is whether knowing it is enough to keep from repeating it.

The Fed spent a decade printing the inflation. Now the man who warned about it runs the building.

The first cut he makes - or refuses to make - tells you which chair he intends to be.

Read this as the next chapter, not a one off...

Yesterday they started settling other people's stablecoins.

Today they are reportedly forming a consortium to issue their own... and probably bury Circle and Tether.

👉 The toll booth owners just decided to print the currency too.

My full breakdown is pinned to my profile. 📌

Read this as the next chapter, not a one off...

Yesterday they started settling other people's stablecoins.

Today they are reportedly forming a consortium to issue their own... and probably bury Circle and Tether.

👉 The toll booth owners just decided to print the currency too.

My full breakdown is pinned to my profile. 📌

Imagine this combination for a moment...

Stripe + Visa + Mastercard + Coinbase.

Four giants from payments and crypto potentially joining forces around a stablecoin.

If this becomes reality, it wouldn't just be another stablecoin launch. It could be one of the biggest collaborations the digital payments industry has ever seen.

Why this combination is so powerful:

▪️ Stripe powers online payments for millions of businesses worldwide.

▪️ Visa connects billions of cards and merchants across more than 200 countries and territories.

▪️ Mastercard operates one of the largest payment networks on the planet.

▪️ Coinbase is one of the most recognized crypto platforms, with deep blockchain and stablecoin infrastructure.

Together, they bring:

▪️ Massive merchant reach.

▪️ Global payment infrastructure.

▪️ Crypto-native technology.

▪️ Regulatory experience.

▪️ Consumer trust and brand recognition.

▪️ Direct access to both traditional finance and digital assets.

What makes this different?

Most stablecoins are built by crypto companies and then try to gain mainstream adoption. This consortium would be approaching the market from the opposite direction:

➡️ Existing global payment networks

➡️ Existing merchant relationships

➡️ Existing consumer reach

➡️ Existing crypto infrastructure

That's a powerful starting point. The scale is hard to ignore.

A stablecoin backed by this group could instantly enter conversations with banks, payment processors, fintech apps, merchants, and crypto users worldwide.

It wouldn't just be competing with Circle and Tether.

It could accelerate the entire stablecoin industry by bringing together the biggest names from both traditional payments and crypto.

IMO, it is worth reading everything but...

... the detail almost everyone is skipping: Coinbase and Circle's USDC revenue share renews in August.

👉 That one date now matters more than any supply chart, because it is where the distributor decides whether to keep renting to the issuer or replace it.

🔖Bookmark this for when the renewal headline drops.